Currencies

The undercurrents of global financial markets signal deteriorating global growth conditions. There is little cash on the sidelines in the US, the Euro Area, and Japan. If the budding bear market resembles the 2000-2003 one, EM stock prices are unlikely to outperform global equities in the initial leg but could outperform in the latter stage of the global selloff.

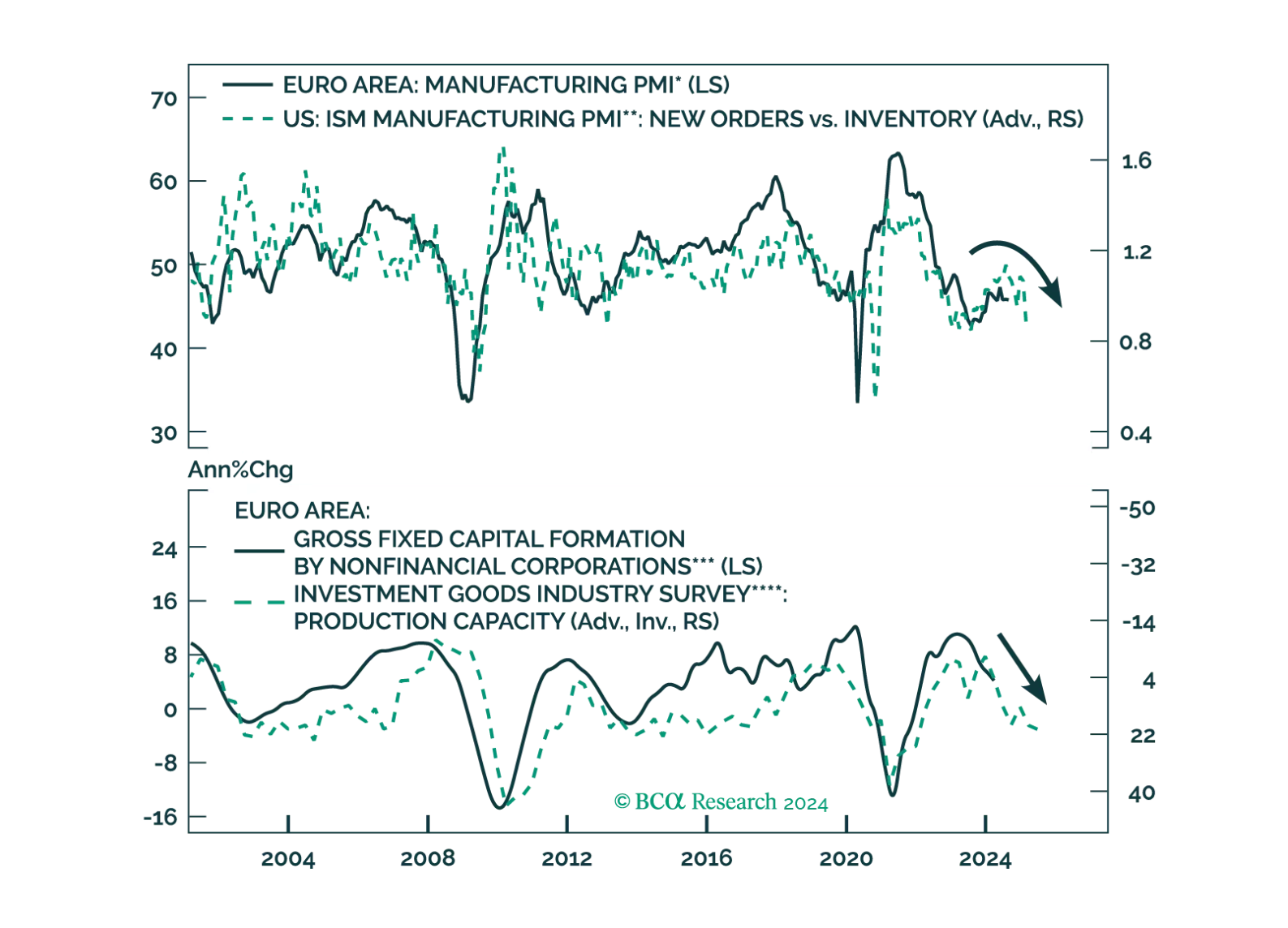

Crucial leading indicators of the global and European economies continue to deteriorate. How should investors position their European portfolios to benefit from these trends?

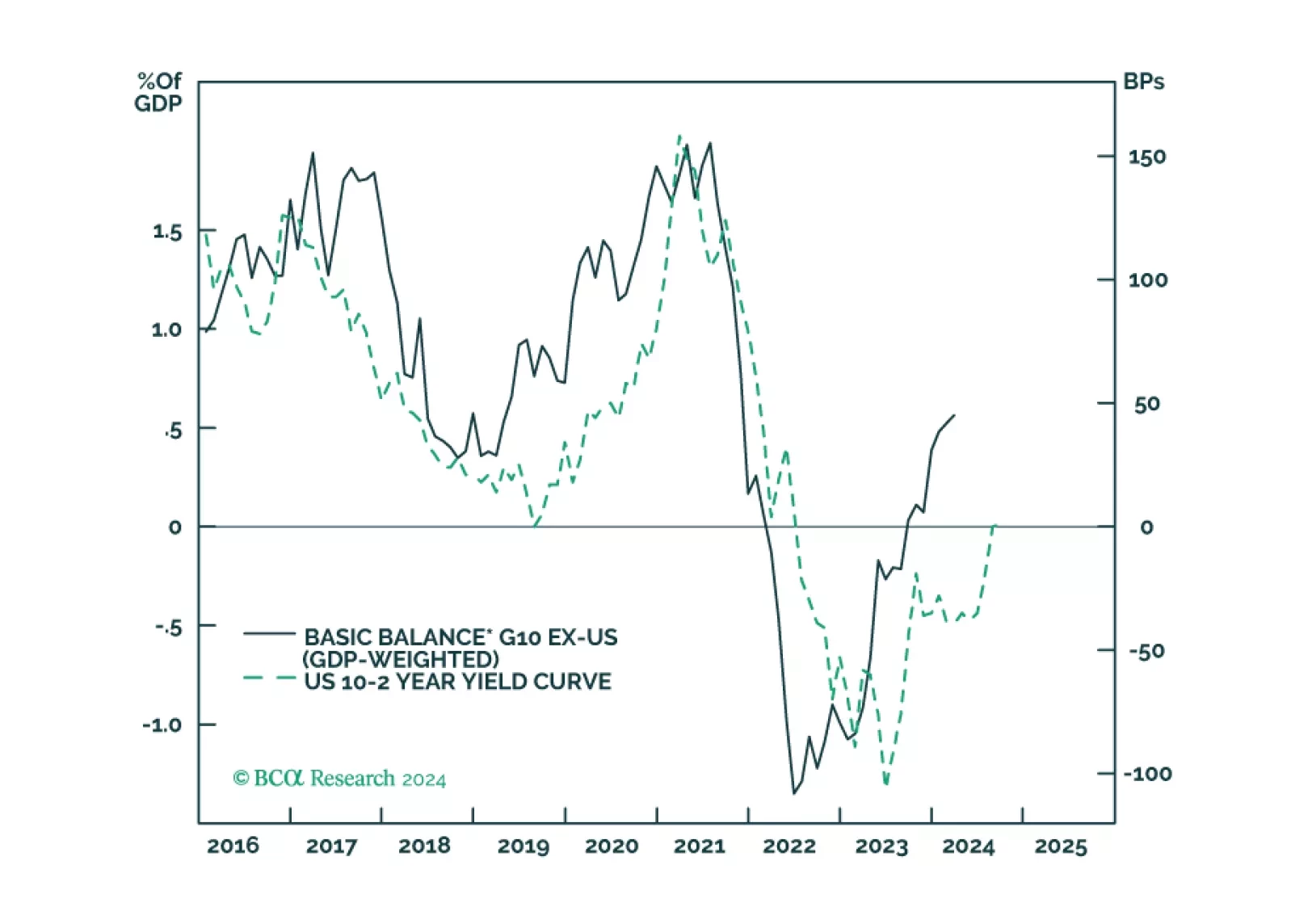

This report looks at the latest developments in G10 economies and implications for bond and FX market strategy.

The ongoing rally in ASEAN currencies will fizzle sooner rather than later as they are not supported by fundamentals. The ringgit and the baht, however, will fare better than the peso and the rupiah during the coming global risk-off period. This report explains why.