Currencies

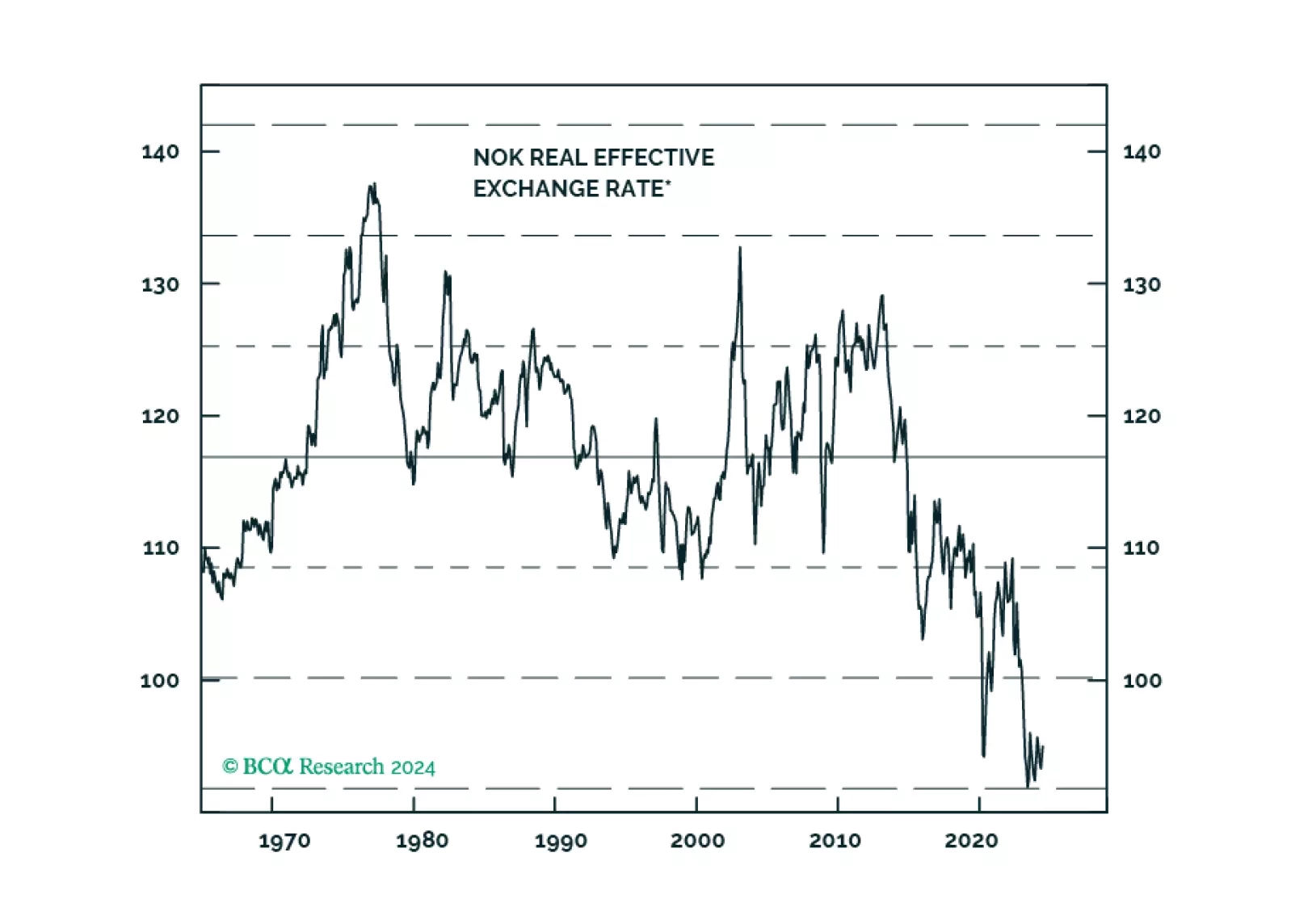

In this report, we gauge the reasons behind the persistently weak Norwegian krone, despite what appears to be benign domestic economic conditions.

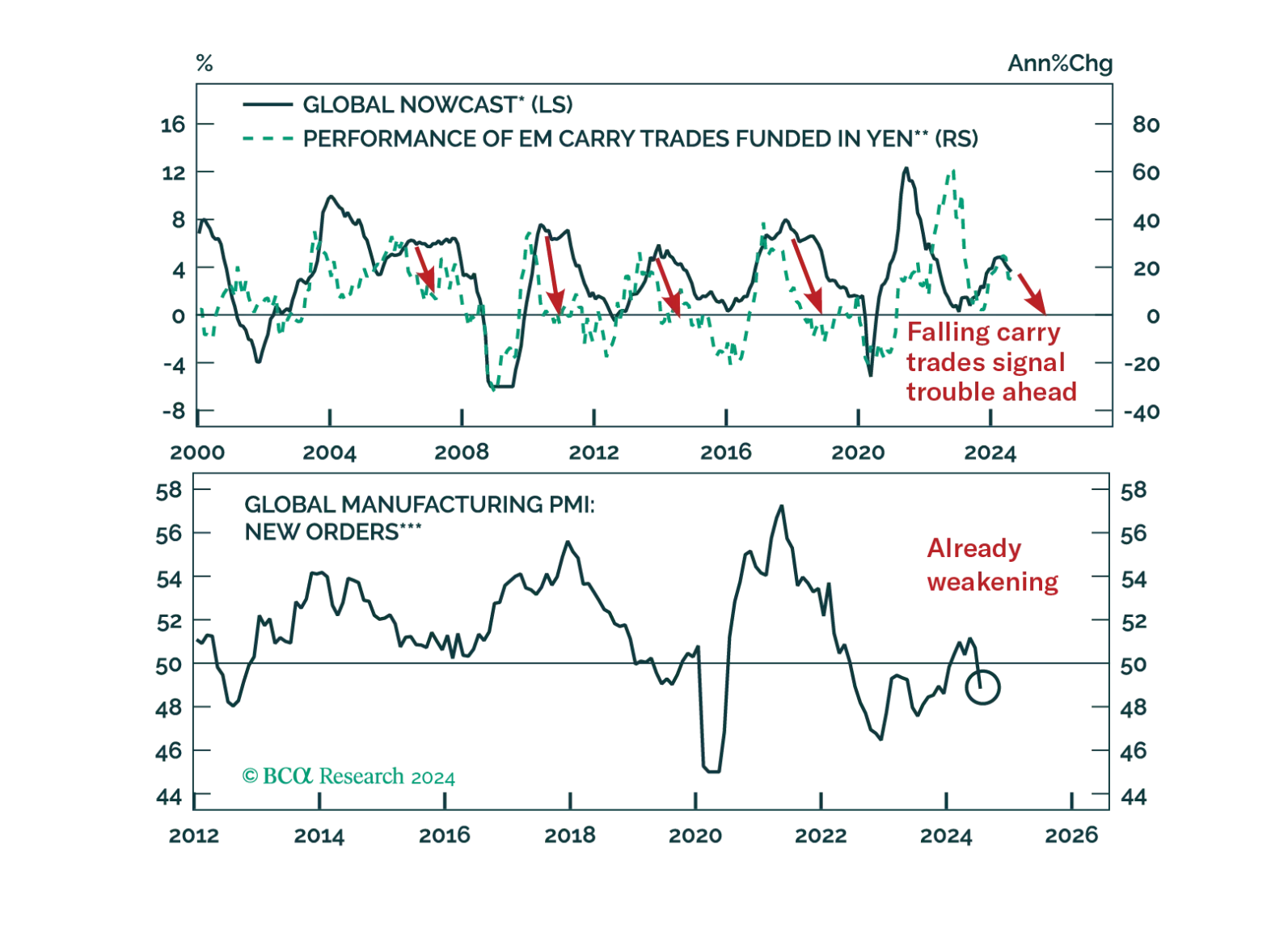

The current Fed easing cycle will likely be a “buy the rumor, sell the news” phenomenon. The basis is our expectation that the US economy is heading into a rough landing. The primary driver of EM currencies is not US interest rates but the global manufacturing cycle.

The unwind of yen carry trades caused violent tremors across the globe. Was this shock a one-off event or the prelude to more troubles?

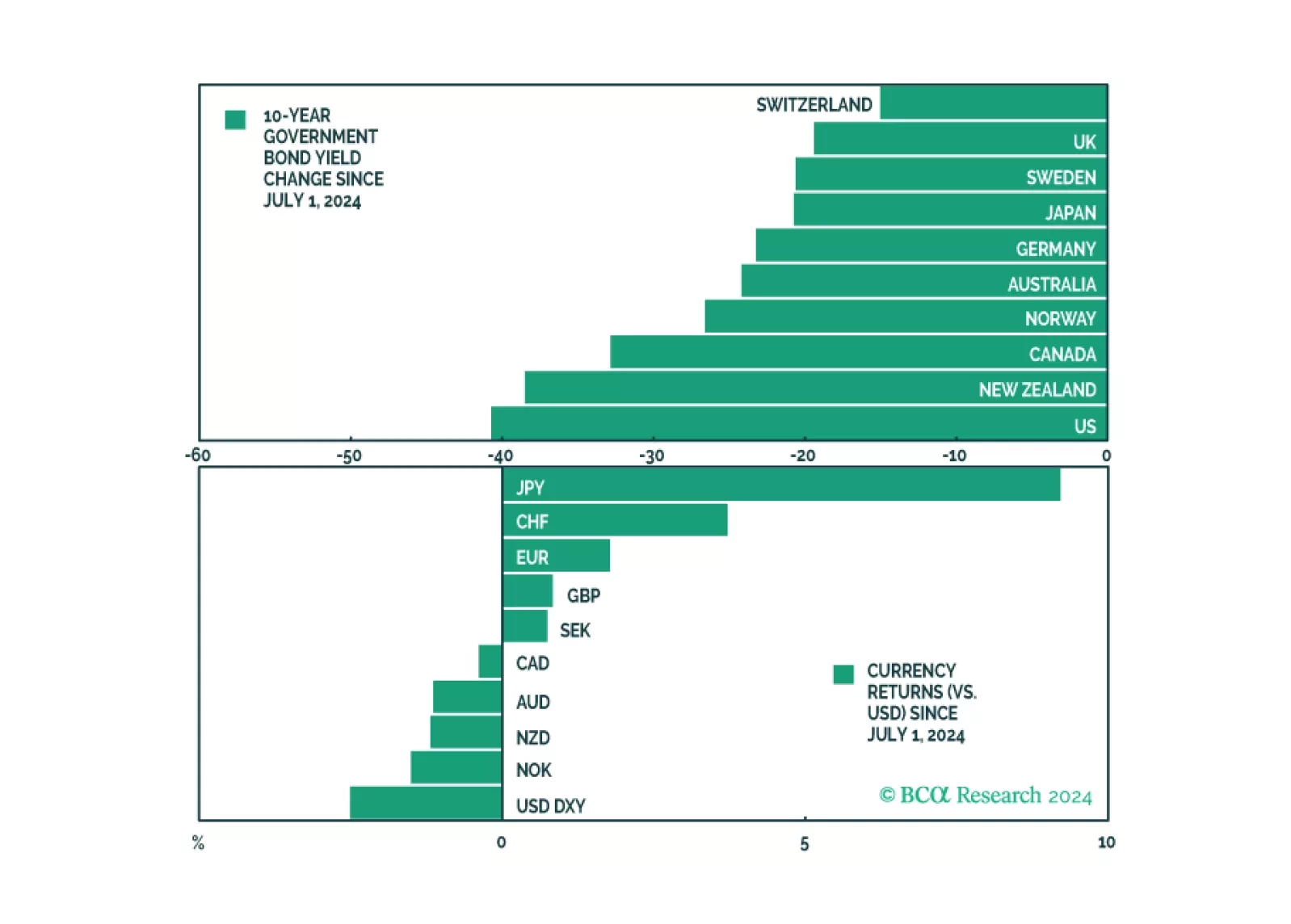

In this monthly review, we give our take on where bond yields and the dollar are headed. This is within the lens of revisiting our fundamental indicators.

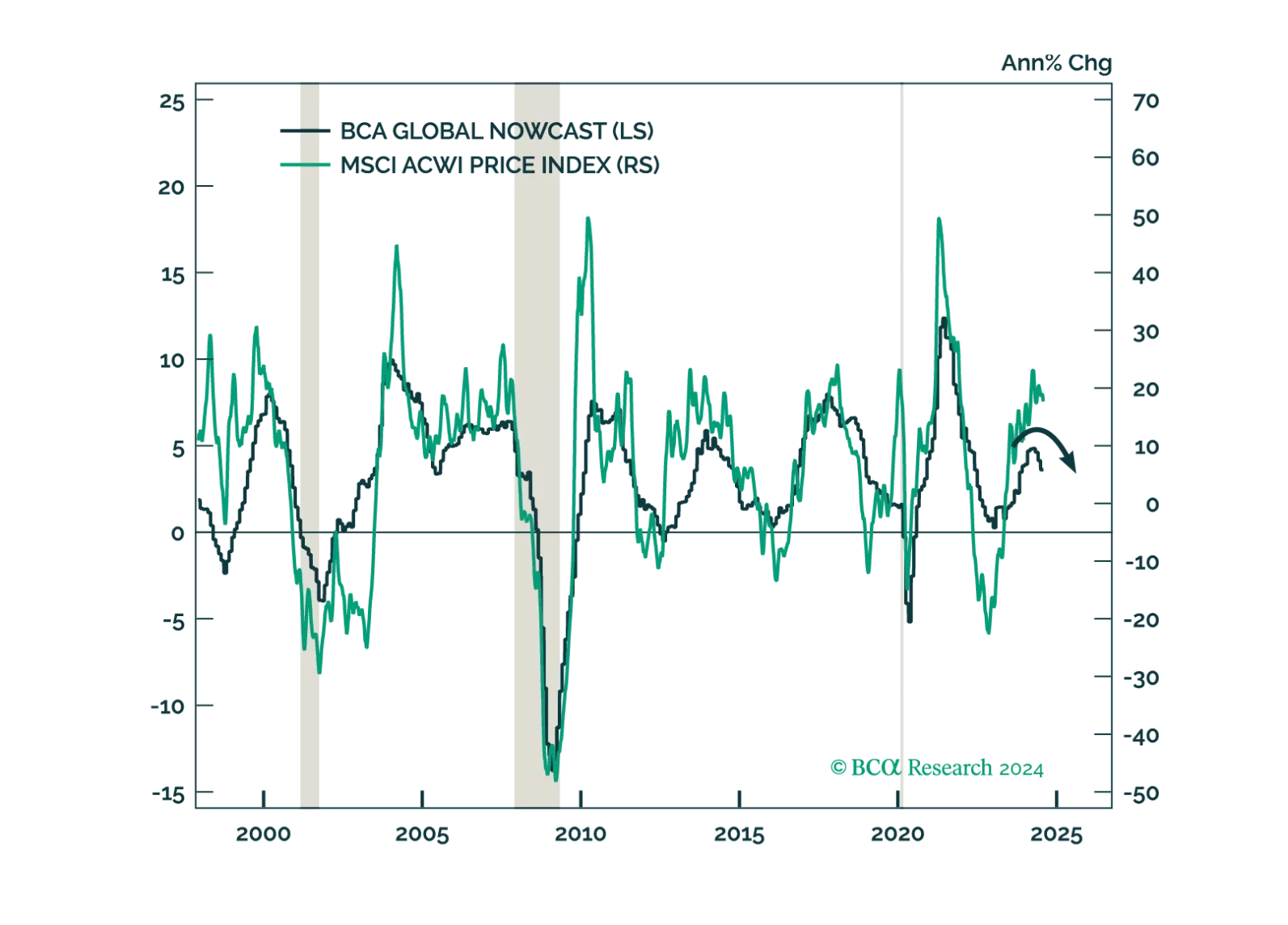

The prices of multiple financial assets have failed to break above their technical resistances. When this occurs, a breakdown ensues. In brief, global risk assets remain vulnerable. We are upgrading Chinese onshore stocks from neutral to overweight and offshore ones from underweight to neutral within EM and global equity portfolios.

The market is pricing in a soft landing, but we see growing signs that the global economy is faltering. Investors should be defensively positioned.

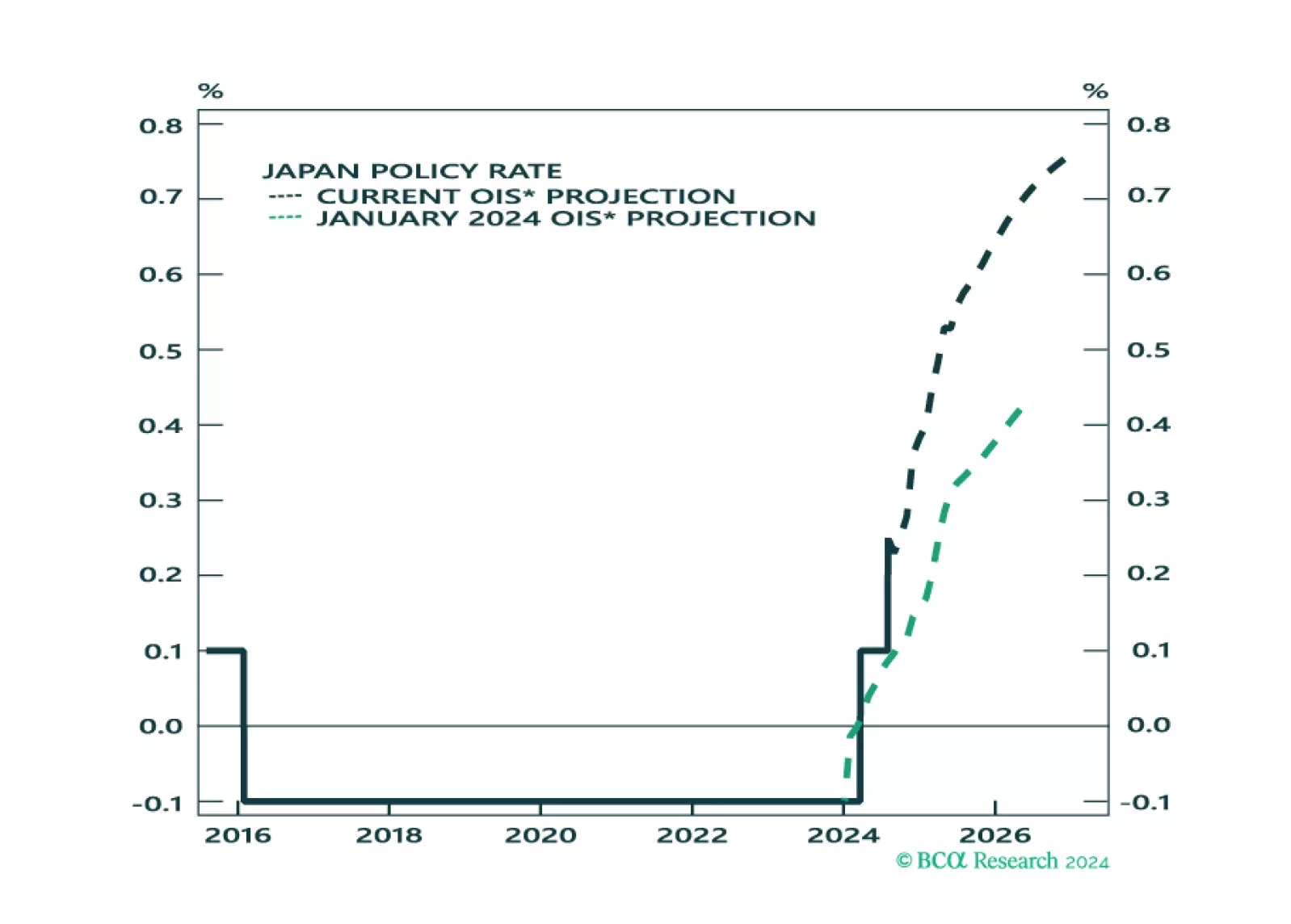

We assess the investment implications of the BoJ and Fed meetings, and give our take on the next policy moves. We also assess the impact on asset markets.