Currencies

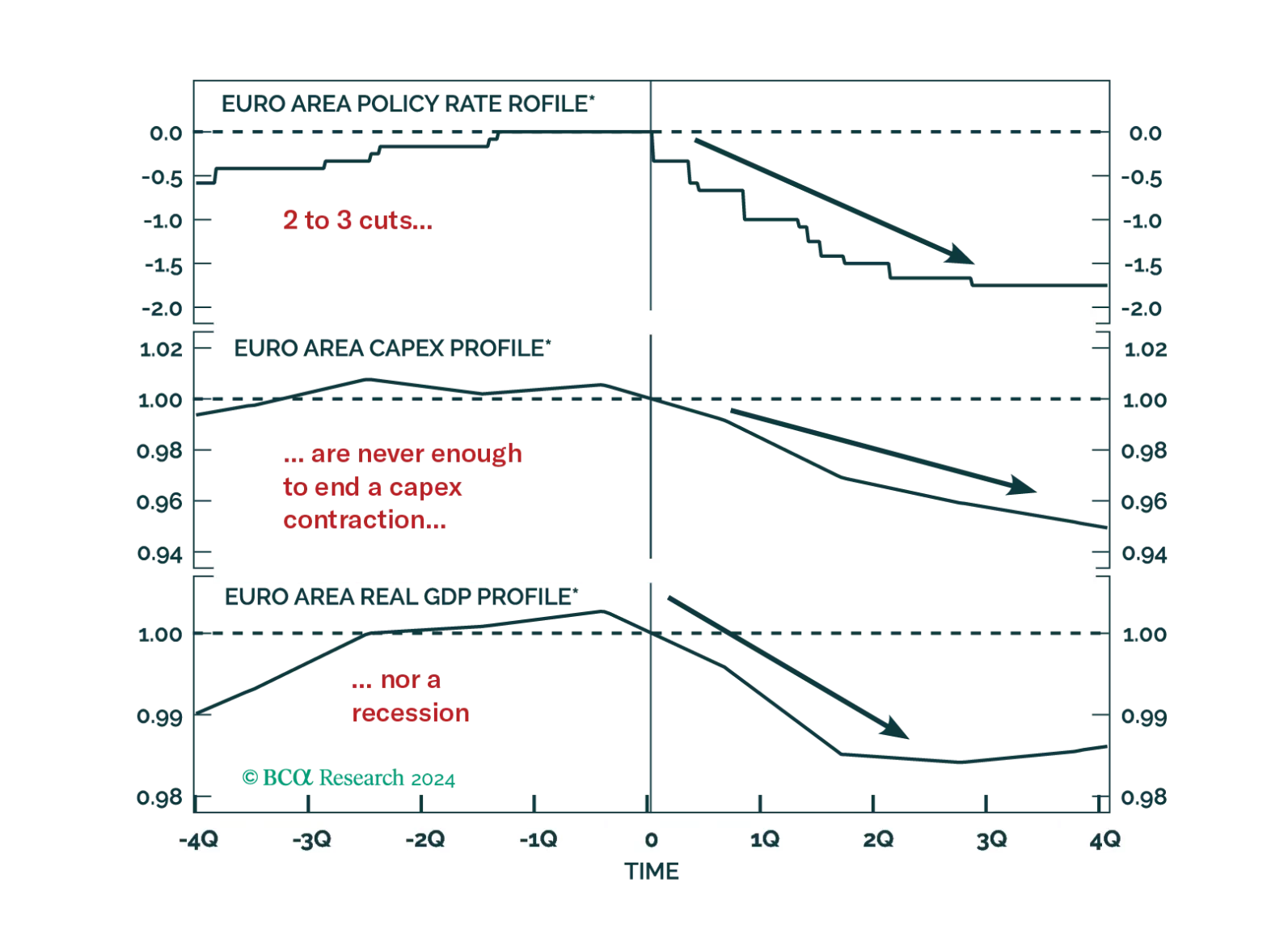

Investors hope that the ECB rate cuts priced into the curve will be sufficient to achieve a soft landing in Europe. History argues against this view, but will this time be different?

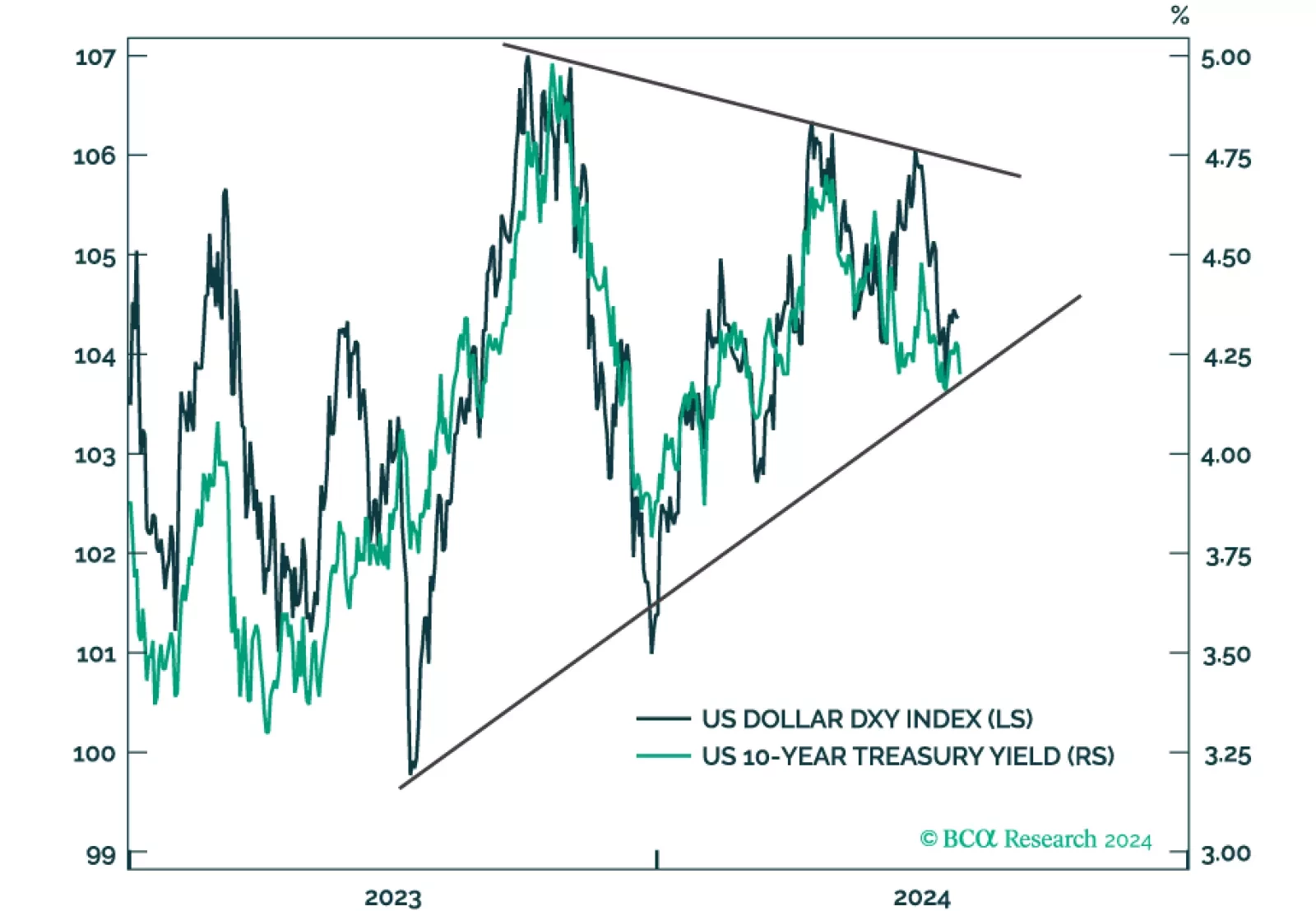

This report takes a look at bond and FX market technical indicators and calibrates the decision to increase portfolio duration and get long the US dollar.

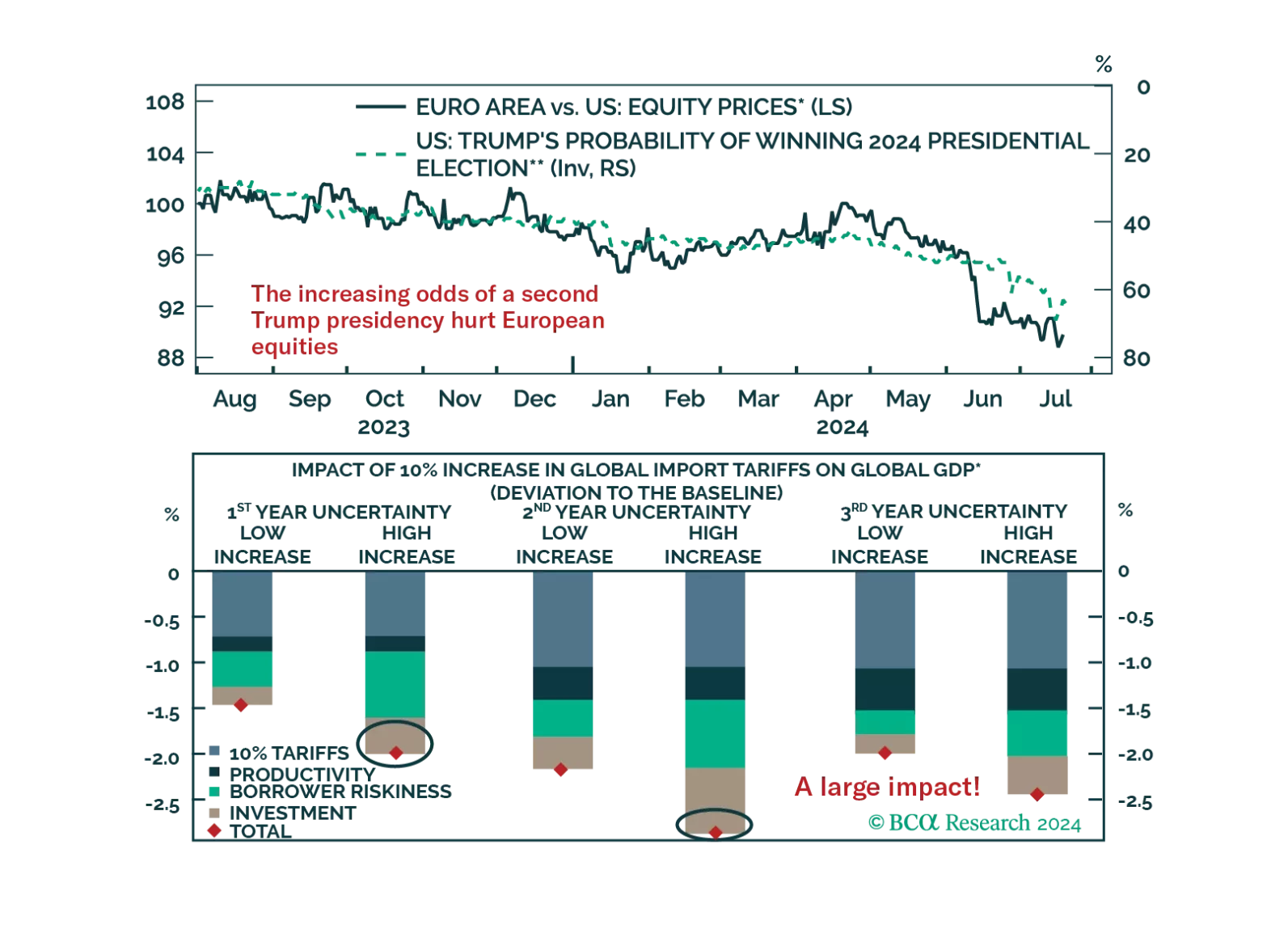

As Trump’s victory odds rise, the underperformance of European equities deepens. How negative would a global trade war be for European assets?

We review some of the key data releases this week that we find have an impact on our currency strategy. Long yen positions make sense today. Long sterling and the euro bets are more of a judgment call, and we will fade any strength in these currencies. This report delves into these nuances, and suggests a few trade ideas.

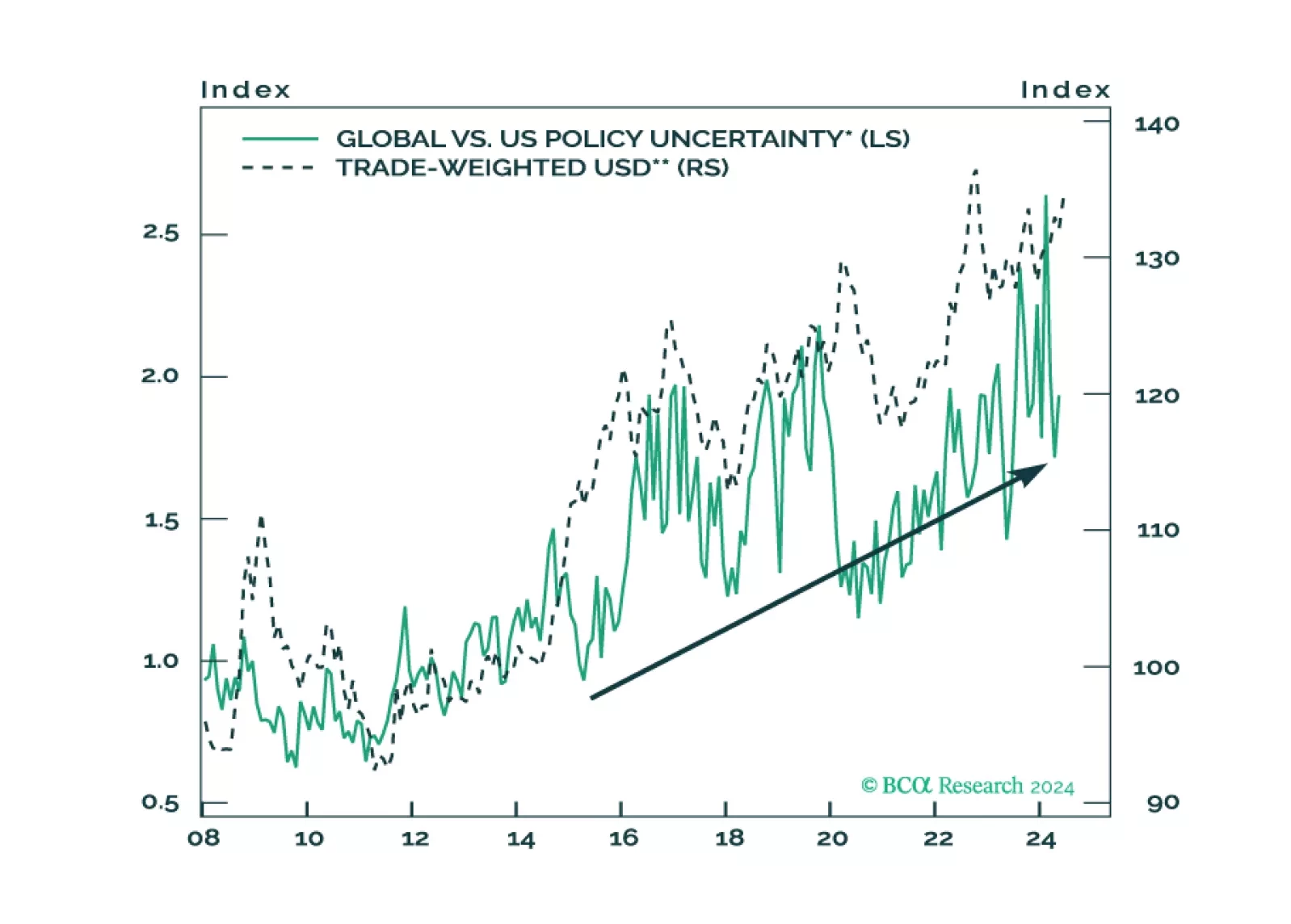

Investors should overweight US assets and de-risk their portfolios in anticipation of a major increase in policy uncertainty and geopolitical risk surrounding the US election and its global ramifications.