Currencies

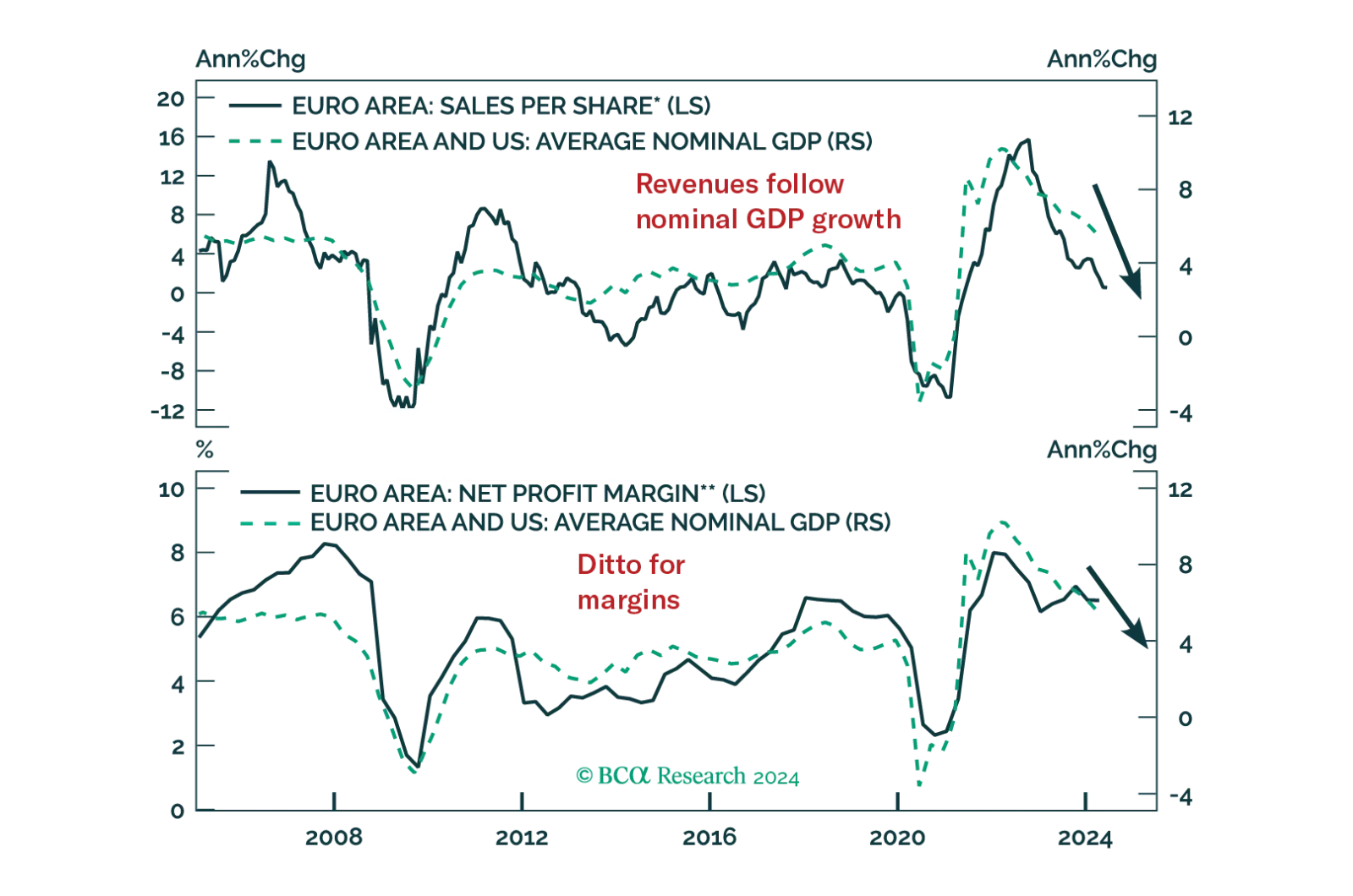

The real threat to European equities is growth, not political risk. How low will Eurozone earnings fall during the coming recession and how much will equities decline in response?

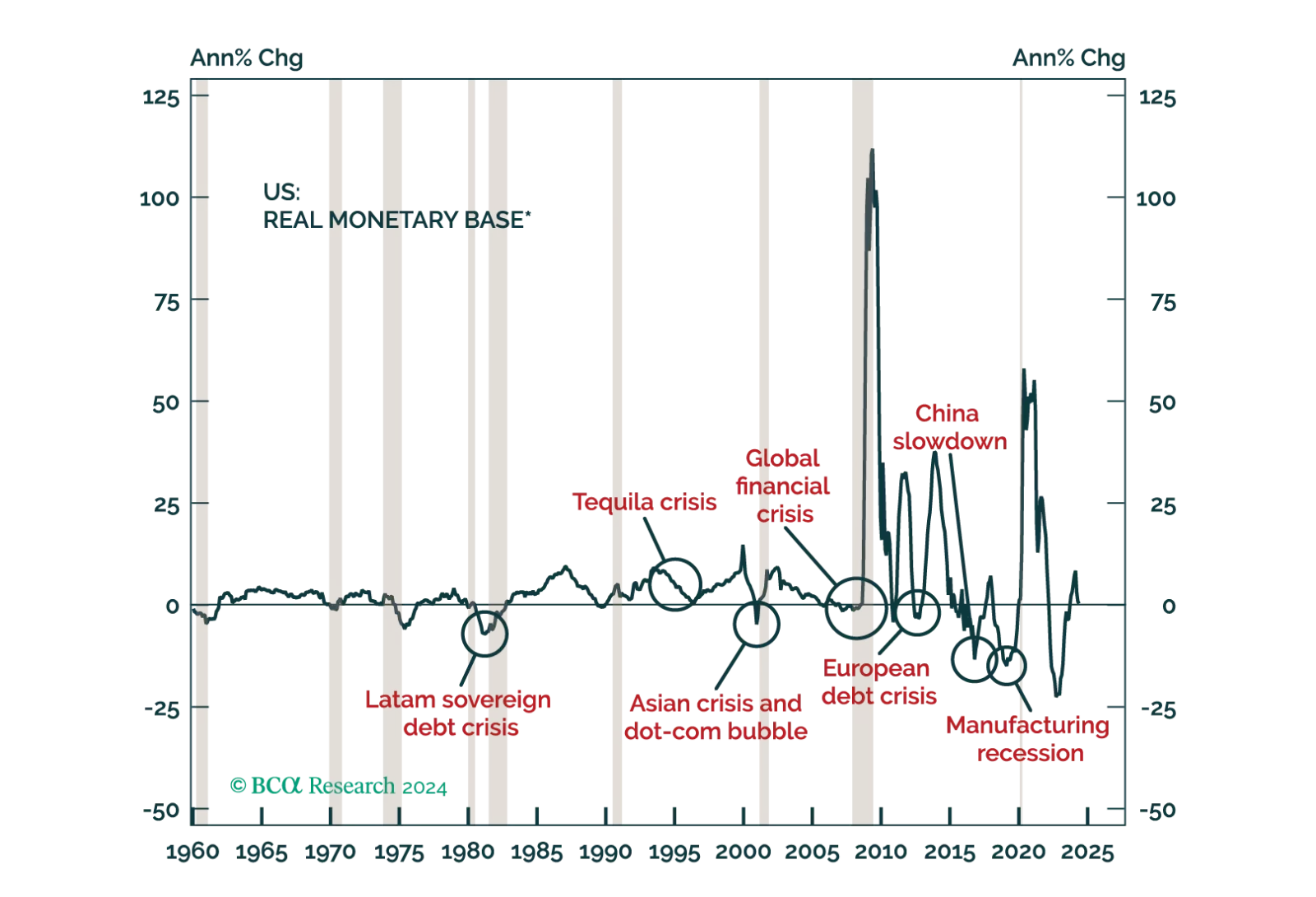

US dollar liquidity has been shrinking, which has important ramifications for global asset prices, including currencies. In this report, we delve into the process of dollar liquidity creation and the outlook for currencies over the next six-to-twelve months.

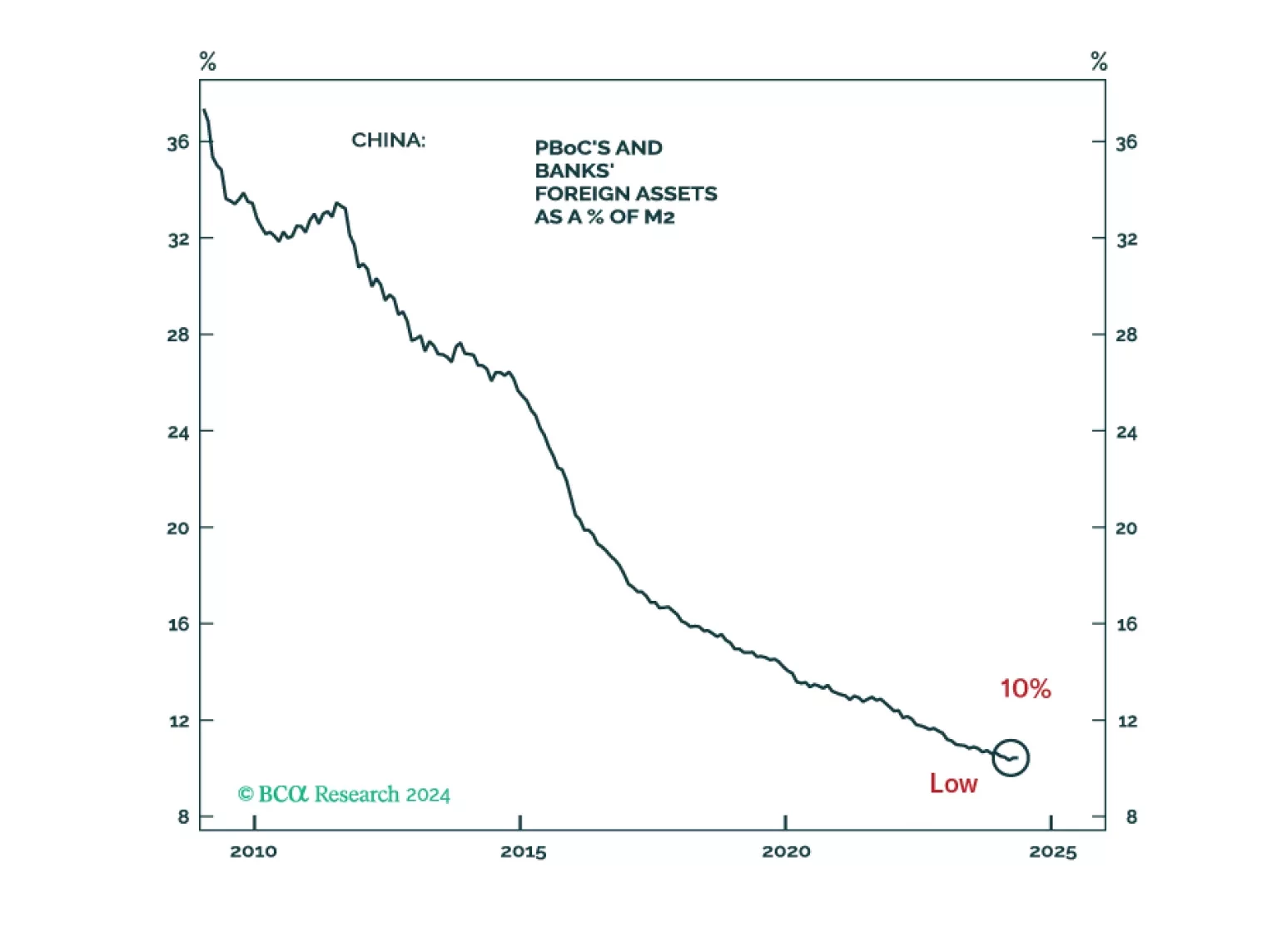

Is the RMB cheap or expensive? Based on trade accounts, the yuan is inexpensive, but the RMB is vulnerable due to capital outflows. Yet, Beijing will not resort to a rapid devaluation for now, and the option of floating the currency is improbable. The PBoC will allow a gradual depreciation of the yuan versus the dollar, say around 5%, in the next six months.

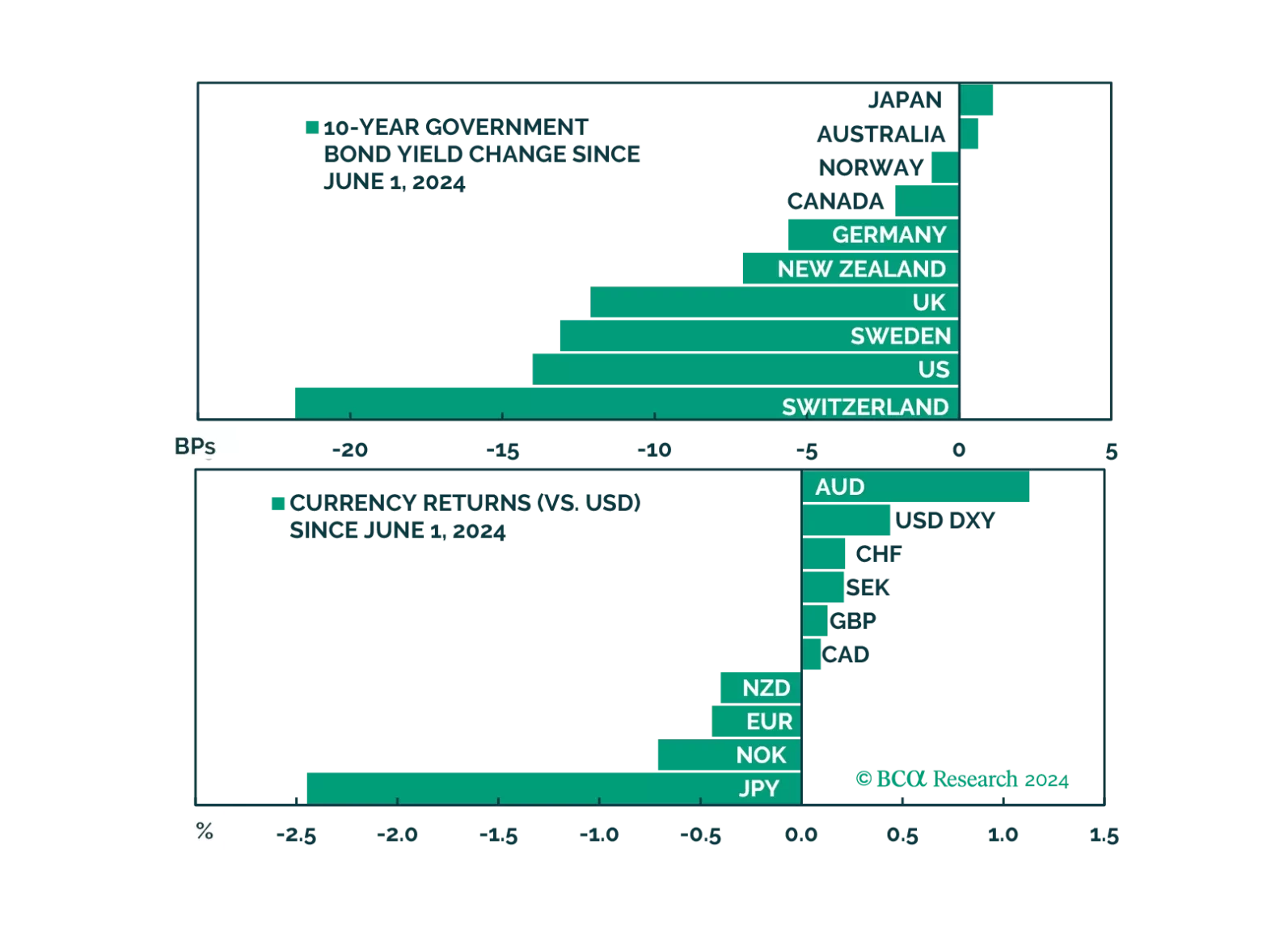

In this week's report, we review the impact of political developments, as well as incoming fundamental data, on our positioning.