Currencies

The new Labour government will have flexibility to respond to macro shocks, which is positive for the UK in general, namely GBP-EUR, and also gilts in absolute terms. But over the long run, tax hikes will likely surprise to the upside, which poses a risk to corporate earnings.

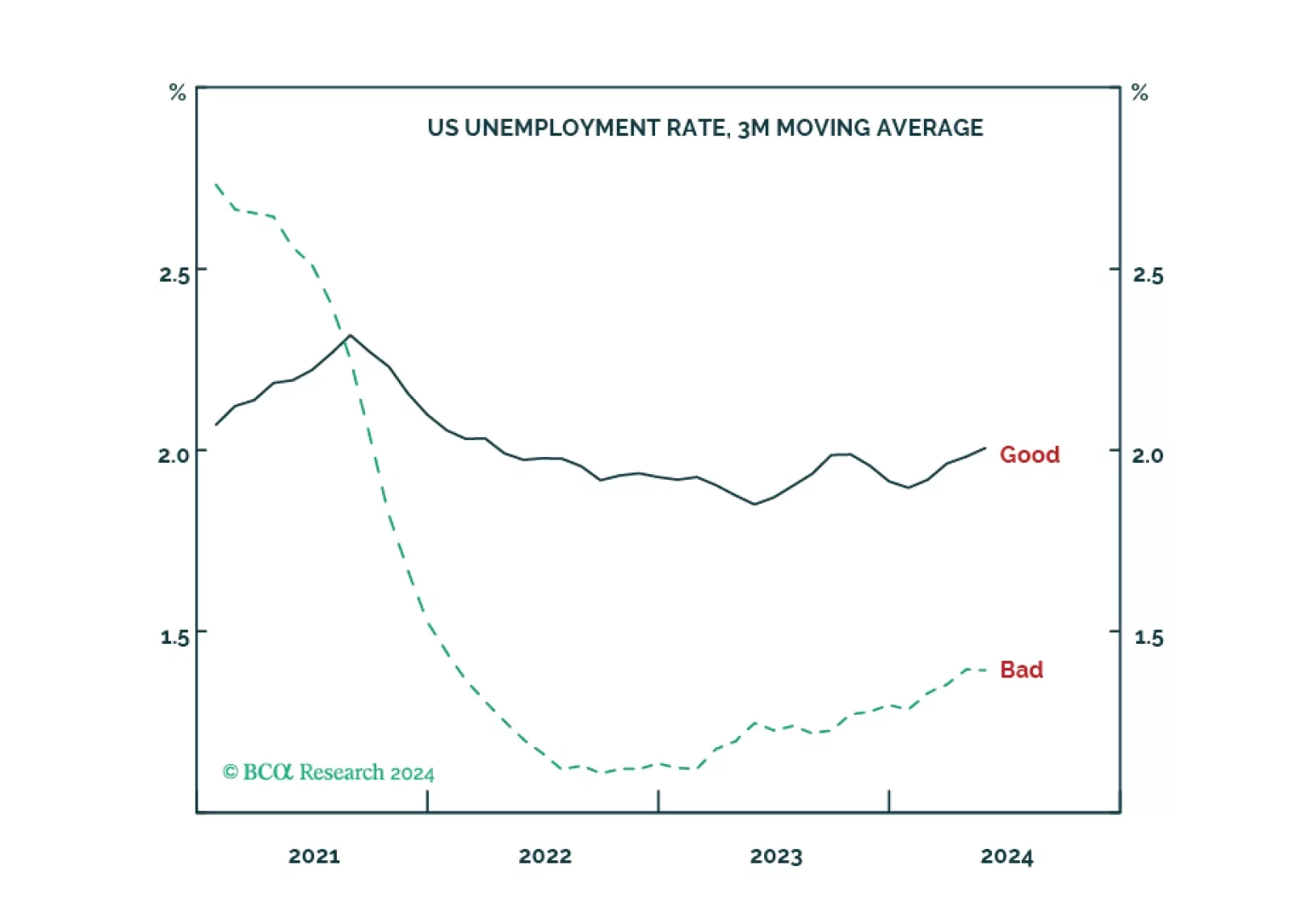

We explain how to distinguish between ‘good’, ‘bad’ and ‘ugly’ unemployment, why bad unemployment is a much better gauge of the jobs market than headline unemployment, and what this means for the tactical positioning in bonds and stocks. Plus: base metals (XBM) have already sold off sharply, so take profits in the short position and open a tactical overweight in global materials (MXI).

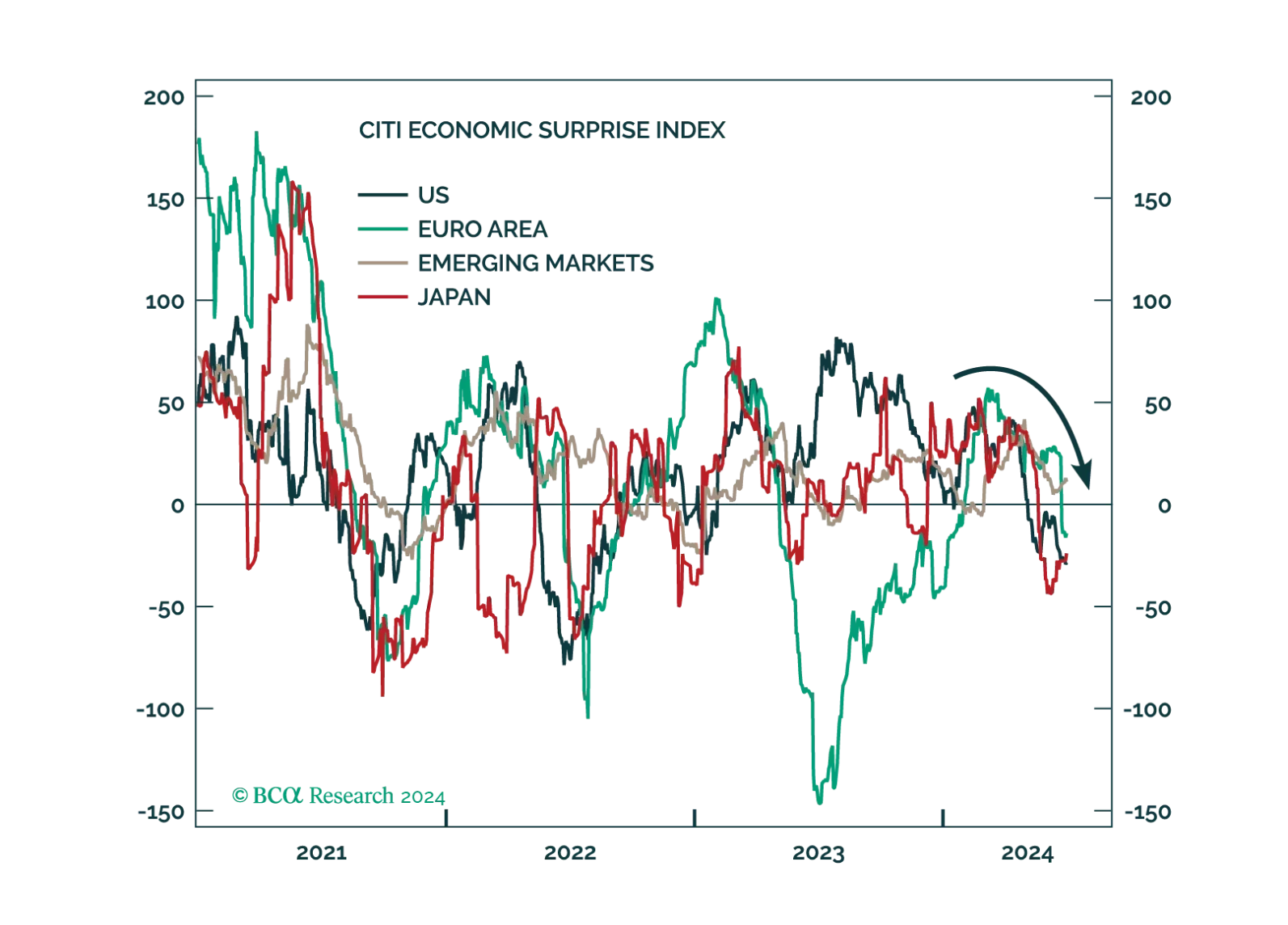

Concerns about the global economy have shifted from sticky inflation to faltering growth. Tight monetary policy is finally starting to bite. We suggest increasing portfolio defensiveness.

In this report, we try to gauge how long the exceptional performance of the US can last, but from a more nuanced angle – inflows into US assets and the impact on the dollar and bond yields. Our work suggests that investors should not make any huge bets on the dollar today, but should be short over the longer term (3-5 years). Empirical evidence also suggests you want to be long US bonds into any downturn, relative to global-ex-US duration-matched government securities, but that view becomes less certain if the global economy avoids a downturn in the next few months. What is interesting in this report are high some conviction views across currencies, bonds and precious metals.

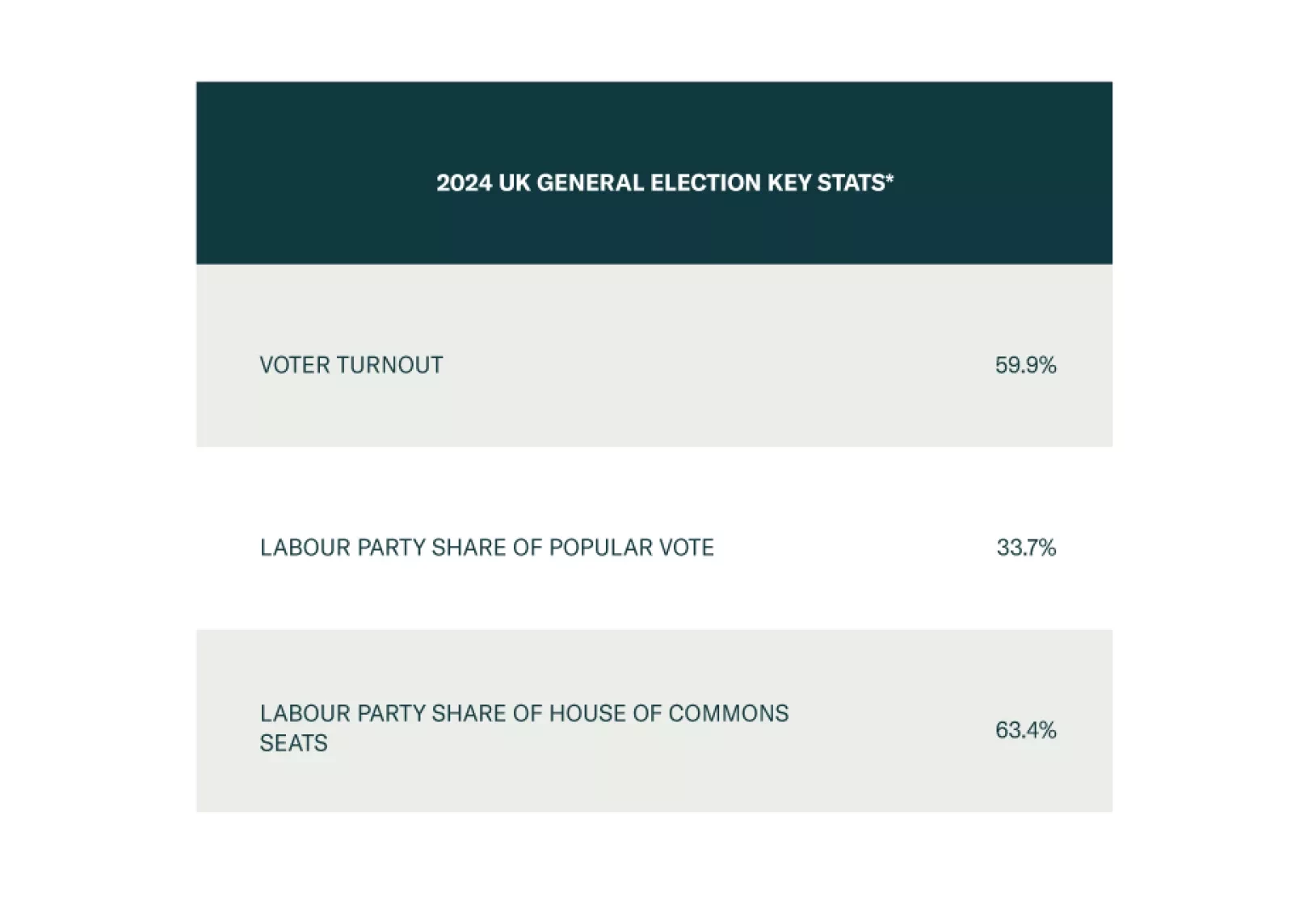

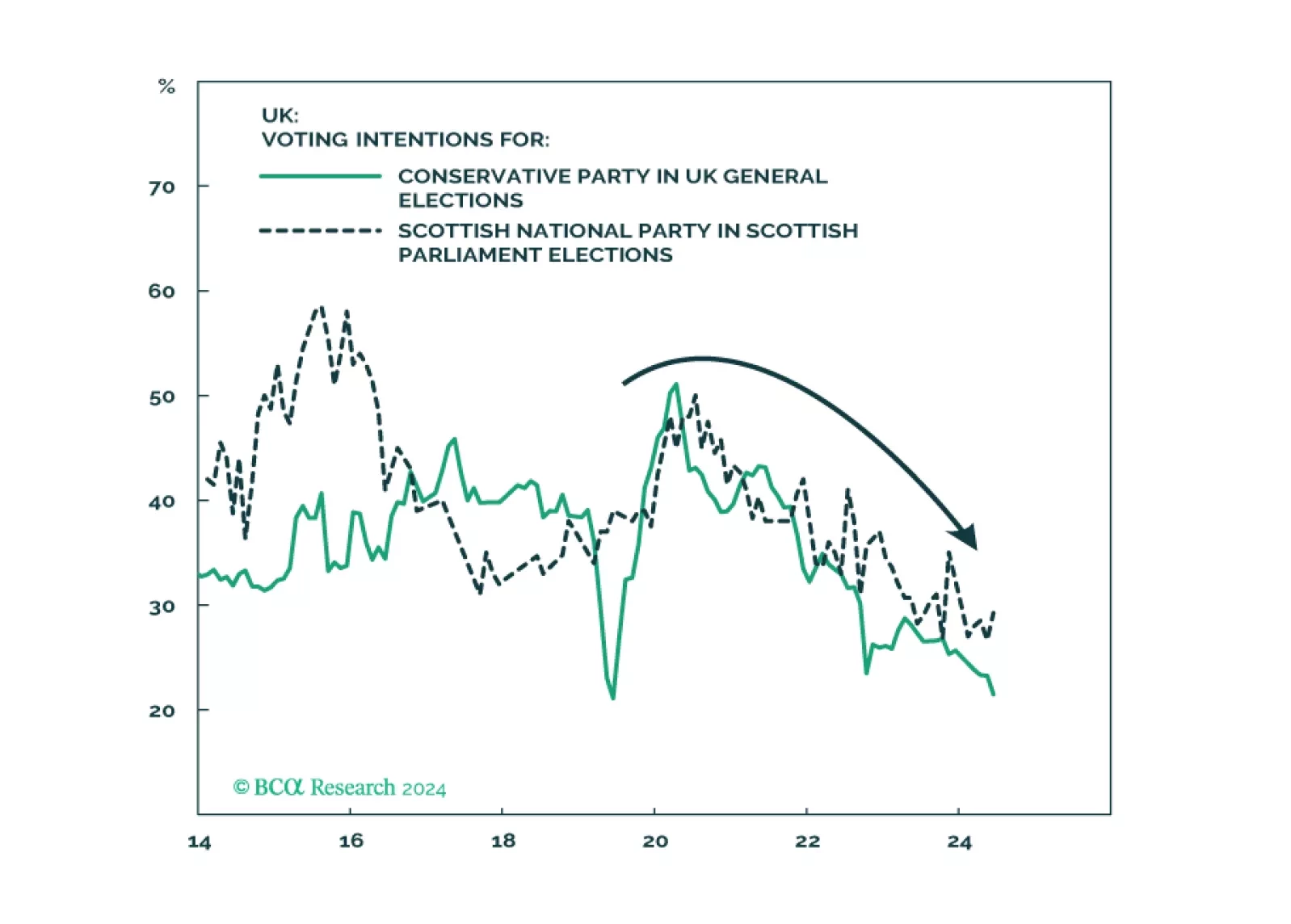

The Labour Party’s comeback in the UK is widely expected and will lead to fiscal stimulus consisting of increased public spending with minimal tax hikes. But a sweeping single-party majority will reduce social unrest only at the cost of higher taxes over the medium term. The paradigm has shifted away from the Thatcherite low-tax regime of the now-discredited Tories. v

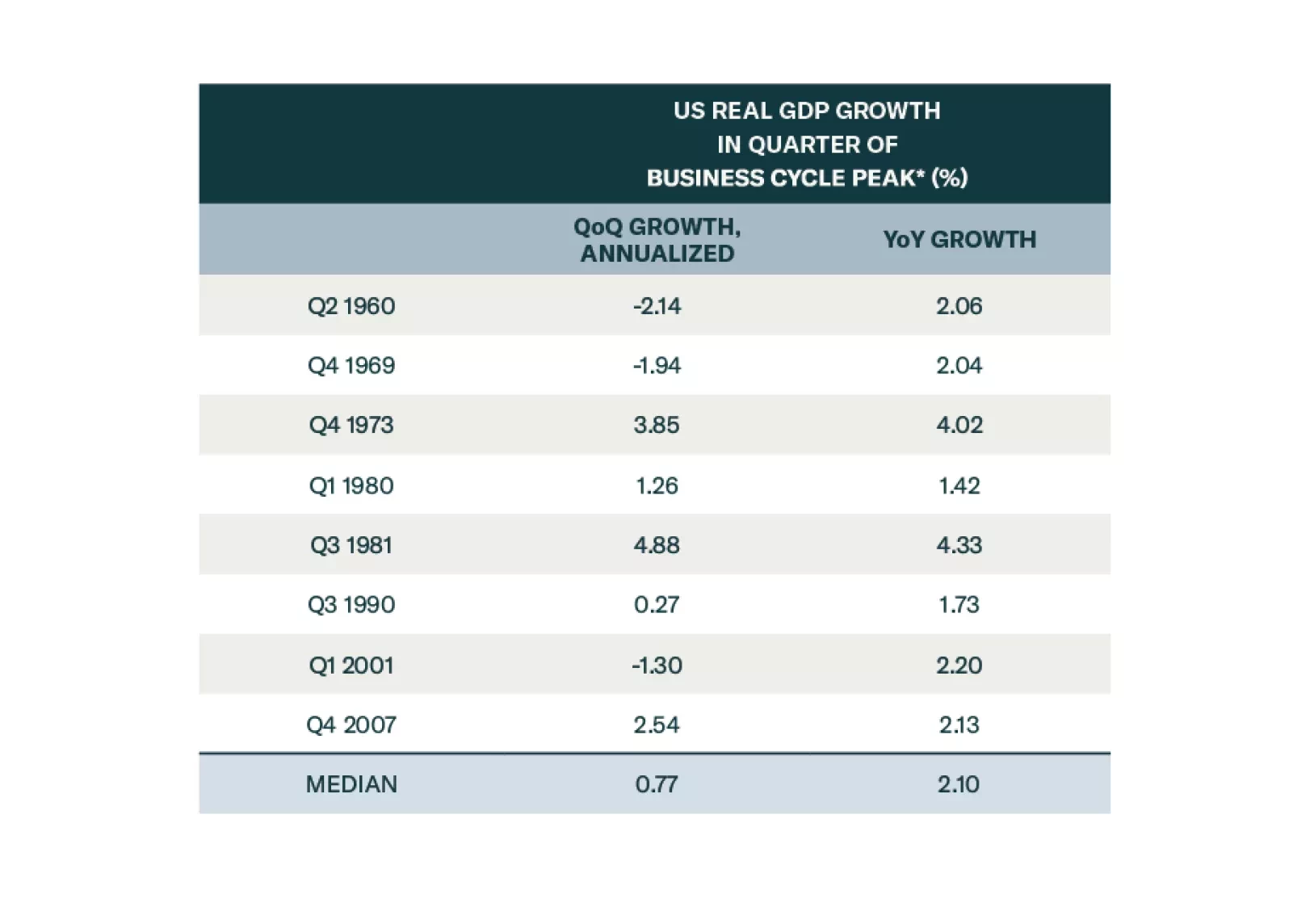

The consensus soft-landing narrative is wrong. The US will fall into a recession in late 2024 or early 2025. We were tactically bullish on stocks most of last year, turned neutral earlier this year, and are going underweight today. We conservatively expect the S&P 500 to drop to 3750 during the coming recession.