Currencies

According to BCA Research’s European Investment Strategy service, the BoE will start cutting rates in September, but the pace of subsequent rate cuts will be modest until a recession engulfs Western economies in early 2025. The UK’s monetary policy remains…

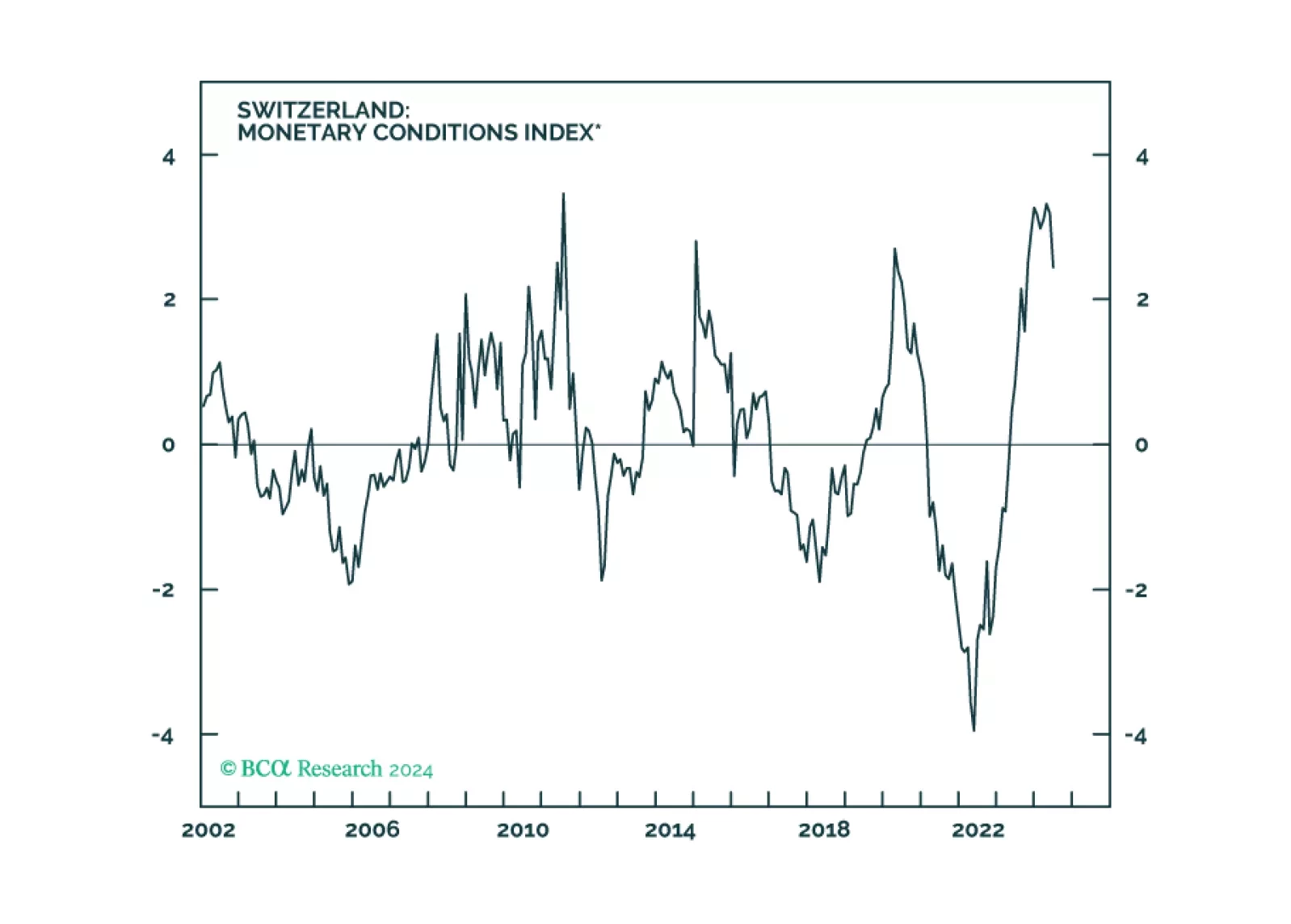

According to BCA Research’s Foreign Exchange Strategy service, the Norges Bank will be one of the last central banks to cut rates. The Swiss National Bank, Bank of England, and Norges Bank all held policy meetings on Thursday. The SNB continued its dovish…

We look at the implications a various European central bank meetings this week, for currency strategy.

Japanese exports in JPY increased from 8.3% y/y to 13.5% in May, surpassing expectations of 12.7%. 23.9% and 17.8% y/y growth in exports to the US and China, respectively, led the overall surge. Trade data from Asian export-oriented economies are generally…

The Swiss National Bank (SNB) was the first major central bank to embark on a dovish pivot back in March. It lowered borrowing costs Thursday for a second consecutive meeting, from 1.5% to 1.25%, despite expectations that it would hold the policy rate…

The Reserve Bank of Australia kept its cash rate at 4.35% at its policy meeting on Tuesday, in line with market expectations. Australia’s monthly measure of headline inflation came in at 3.6% in April, still considerably above the midpoint of the RBA’s 2-3%…

According to BCA Research’s Geopolitical Strategy service, the South African election presents a window of opportunity for productivity-boosting structural reforms, such as privatization, to coincide with monetary and fiscal easing necessary to fend off…

In this insight, we update our thinking on the recent BoJ move in terms of positioning for the yen and JGB yields.

The new national unity government in South Africa creates a geopolitical opportunity that investors should not bet against in the short term. A broad-based rally is likely to unfold relative to other emerging markets. However, structural problems and distrust within the new coalition hold out significant risks over the long run.

In a largely expected move, the Bank of Japan kept its policy rate unchanged at 0-0.1% in June. It maintained the pace of bond buying at JPY 6tr per month but signaled it would lay out a plan to reduce its balance sheet next month, without offering any…