Dairy

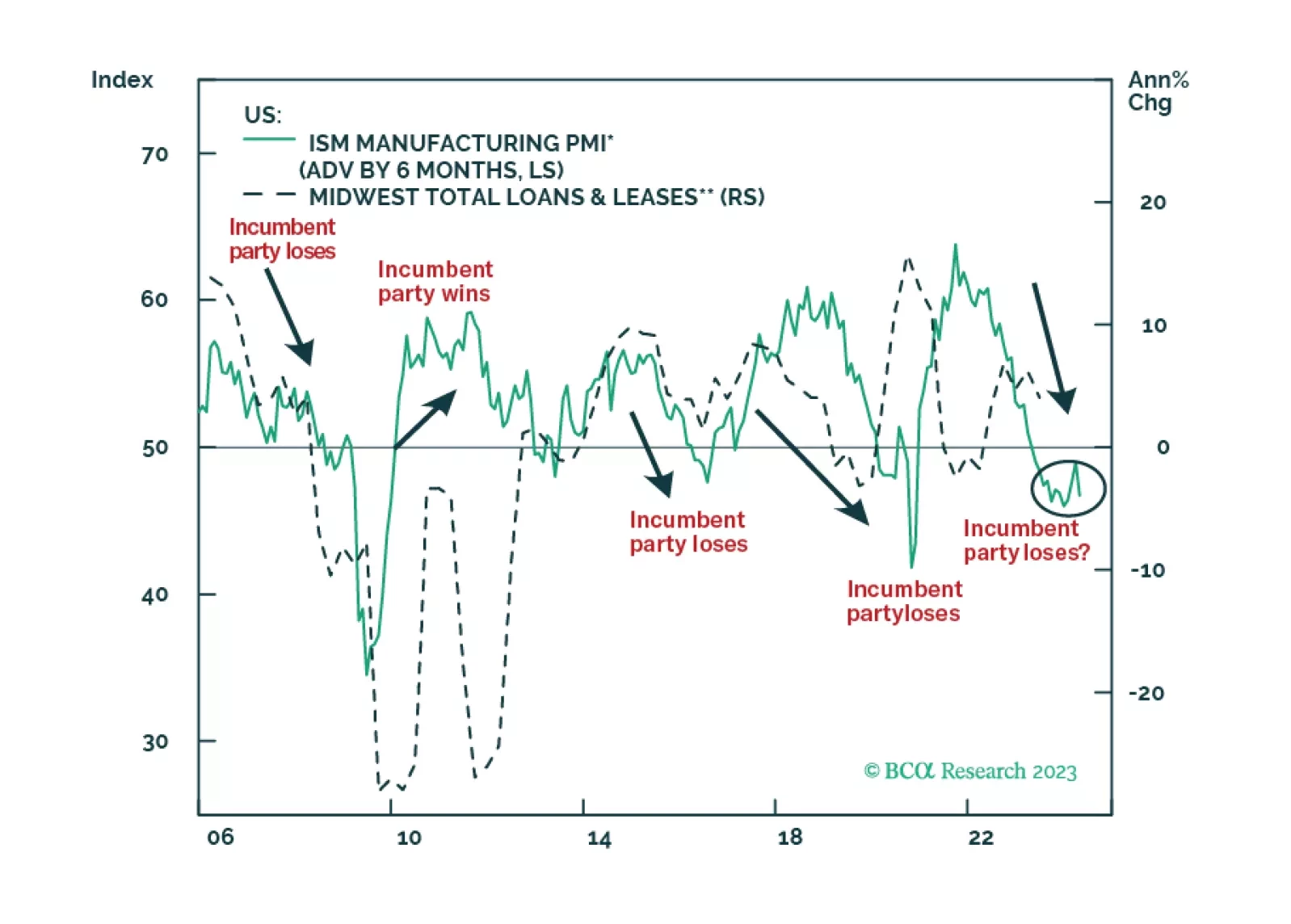

President Biden is facing foreign challenges on three fronts and these challenges are coalescing around the critical states of the Midwest. Take risks off the table and stay defensive in 2024.

Feature Happy Thanksgiving to all our U.S. clients. We wish you the best the holiday has to offer, as you share blessings with friends and family. In this holiday-shortened week, we are publishing a joint report with our colleagues at BCA's Energy Sector Strategy (NRG) service. We succinctly examine the pros and cons of the debate over whether OPEC will or will not agree to and uphold a *real* production cut, as it has promised, at its much-anticipated meeting on November 30. Disagreement on the likely outcome of the meeting runs high. In late September, OPEC announced an agreement in principle to cut oil production at the formal November meeting to a level of 32.5-33.0 MMb/d. This would represent a 500,000-750,000 b/d reduction from August production levels, and an 830,000-1,330,000 b/d reduction from the IEA's latest OPEC production estimate for October of 33.83 MMb/d. In addition, non-OPEC behemoth Russia has signaled a potential willingness to contribute its own production freeze or cut to the agreement in an effort to support higher oil prices. Chart 1With A 1 MMb/d Cut, ##br##Draws Would Be Greater There are compelling arguments to be made both supporting the likelihood of a production cut as well as for being skeptical that such an agreement will be reached and adhered to. Even within BCA, there is disagreement. This service, the Commodity & Energy Strategy (CES), which sets the BCA house view on oil prices, pegs the odds at greater than 50% that there will be a meaningful cut of 1 MMb/d+, anchored by large cut pledges from OPEC's leader, the Kingdom of Saudi Arabia (KSA), and Russia. The NRG team, dissents; they think it is more likely that no deal is reached, and if a deal is announced, it will not be adhered to. Regardless of whether there is an announced agreement to cut production or not, both CES and NRG expect KSA's production to decline by 400,000-500,000 b/d between August and December according to KSA's normal seasonal management of production levels; we would not include this expected seasonal reduction in the calculation of a *real* cut. In our analysis on Chart 1, we include a *real* cut of 1MMB/d below the normal seasonality of KSA's production, which lasts for six months. In H2 2017, we assume the cut is dissolved and the market also receives an extra 200,000 b/d of price-incentivized production from the U.S. shales. How To Bet On A Cut, The Out-Of-Consensus Call Chart 2Without A Cut,##br## Inventories Still Will Be Drawn In 2017 CES's view for a cut (established November 3) was significantly out-of-consensus until recent chatter from OPEC increased the perception that an agreement could be reached. Still, there remains significant doubt a freeze or cut can be accomplished. Without a cut, NRG and CES share a constructive outlook for oil markets heading towards steepening deficits during 2017 (Chart 2). Note: BCA's estimates show a tighter oil market than the EIA's estimates: Our Q3 2016 production estimates are lower than the EIA's by ~300,000 b/d due to differences in our assessments in Brazilian, Russian and Chinese production; our Q3 2016 consumption estimate is higher than the EIA due to our higher assessment of U.S. summer-time demand (the EIA has consistently underestimated U.S. demand over the past few years). A production cut coupled with a natural tightening in the market brought about by the price-induced supply destruction over the past 18 months would make 2017 inventory draws even greater, lifting oil prices higher, and providing even greater upward support to our favorite investment recommendations (Chart 1). Below we outline the investment recommendations that would benefit from an OPEC cut, spanning individual equities, ETFs, and commodity calls: Direct Commodity Investment: CES recommends two pair trades on oil contracts and call options. Long February 2017 $50/bbl Brent Calls vs. short February 2017 $55/bbl Brent Calls to play the spike in oil prices that would come from a successful OPEC cut, which was recommended November 3 and was up 50.41% as of Tuesday's close. Long August 2017 WTI contract vs. short November 2017 WTI contract to play an expected flattening of the forward curve, which also was recommended November 3 and it up 48.61% as of Tuesday's close. Oil Producers: NRG recommends overweight-rated Permian oil producers EOG, PXD, FANG and PE, which will be leaders in expanding production into an improving oil price market. Service Companies: NRG recommends overweight-rated completion-oriented services companies HAL, SLB and SLCA, which will benefit most from increased U.S. shale spending. Equity-Backed ETFs: NRG recommends overweight-rated ETFs XLE, FRAK, and OIH as vehicles that provide more diversified investment exposure to higher oil prices and oilfield service activity than individual equities. Oil-Backed ETF. Tactically buying the U.S. Oil Fund ETF (USO) would provide good direct exposure to a quick oil price surge. However, USO should not be held as a longer-term investment because the inherent cost of continually rolling contracts consistently erodes USO's value versus the equity-backed ETFs XLE and OIH. This longer-term underperformance informs NRG's underweight rating on USO. Risks To Our Views: Oil and natural gas prices that differ materially from our forecasts, possibly due to slower-than-expected global economic growth and/or greater than expected supply growth. Poor operational execution and/or changes to regulatory restrictions could negatively impact the financial and stock performance of our recommendations. A week ahead of the OPEC meeting, in the wake of recently recovering production in Libya and Nigeria, and amid campaigning by Iran and Iraq to be excluded from participation in the cuts, it is impossible to know for certain how the complicated politics of OPEC and Russia will play out. Below we outline the competing objectives and risks that will be in play. Case Against A Cut Undeniably, a cut in production, particularly a coordinated cut where several countries share the burden of restricting production, would raise oil prices and enhance 2017 oil export revenues for all OPEC producers. However, that near-term benefit for pricing and revenue has been obvious for the past two years, and yet neither KSA nor Russia has been willing to cut production, feeling the potential to lose longer-term market share outweighed the immediate revenue benefits of a cut. The hazard of a price-increasing production cut, is that the higher oil price would essentially subsidize non-OPEC competitors with higher cash flows, and would simultaneously bolster the confidence of capital markets that OPEC will support prices at a floor of $50, reducing the risk of future investments. These two effects would jointly encourage increased capital investment into establishing new production, especially by the fast-acting U.S. shale producers, whose rampant investment and production growth from 2010-2015 was, by far, the leading contributor to the 2015-2016 oversupply of oil. Encouraging a resurgence of drilling and production would certainly lead to faster production growth from the U.S. shales in 2017-2018, allowing those producers to grow market share under the umbrella of OPEC's production sacrifices that created the higher prices. OPEC has just endured a lot of economic pain through the oil price decline. The economic purpose of this pain was to starve global producers of operational cash flow and dissuade the inflow of new capital, thus choking off the reinvestment required to continue to grow oil production. By and large, this goal has been achieved, with U.S. shale producers slashing capital expenditures by 65% from 2014 to 2016, and the International Oil Companies (IOCs) cutting capital expenditures by 40% over the same period. As a result, after the substantial surge in global oil production in 2014-2015 that created the current over-supply, the capital starvation caused by low oil prices will result in essentially no global production growth in either 2017 or 2018, allowing for demand growth to erode the oversupply of production during 2016, and to eat into the overstocked inventories of crude during 2017-2018. KSA has created fear and uncertainty throughout global producers and capital markets by steadfastly refusing to use its production-management powers to support a floor under oil prices. We are skeptical that KSA will ultimately agree to reverse this strategy, by now establishing a price floor. Such a reversal would undermine the profound market-share message KSA has delivered to competitors (at the cost of great financial pain), and weaken its perceived resolve to allow oil prices to be set by the market. As such, the NRG team believes KSA will not agree to cut production beyond the already-expected seasonal reduction in production, and that this position will scuttle September's tacit agreement to cut production at the official meeting next week. Such a scenario would be fairly similar to how KSA undermined the production-freeze discussions in Doha in April, by insisting other OPEC members - Iran, in particular - share in the production limitations in order to engender KSA's support; a condition that other members were unwilling to accept. The Case For A Cut The case to expect a cut agreement acknowledges that such a cut would subsidize competitors and diminish the impression of KSA's resolve and/or ability to out-last competitors through an oil price down-cycle. The case for a cut concludes that the benefits of higher 2017 oil prices simply outweigh these market share and reputational costs. The benefits that OPEC and Russia would receive are: Critical Need For Higher Revenue. If KSA and Russia each cut 2017 production by 500,000 below current expectations, and oil prices jumped $10/bbl as a result, KSA's 2017 oil export revenues would increase by close to $17.5 billion, and Russia's would increase by almost $8.25 billion. If the financial pain endured by these countries is substantially greater than NRG has estimated, this near-term revenue lift could be more critical than we appreciate, overwhelming the reputational and longer-term market-share losses resulting from the reversal of policy. Borrowing capacity for each country also would increase, as a result of higher revenues. With both states seeking to tap international debt and equity markets, this increased revenue would increase their borrowing capacity. Higher Value For Asset Sales. KSA is preparing to IPO Saudi Aramco. Bolstering the spirits of capital markets with higher oil prices would be expected to increase the proceeds received from this equity sale, increase the market value of the company, reduce debt-service costs, and improve access to debt markets, which KSA and Saudi Aramco are both likely to tap more frequently in the future as the country tries to diversify the economy away from oil. Similarly, two weeks ago, Russia signed a decree to sell a 19.5% stake in Rosneft by the end of 2016. An immediate oil price strengthening and messaging that KSA and Russia would support a pricing floor would inflate the value of this sale, given the high correlation between Brent crude oil prices and Rosneft's equity price. Production Stability Not As Strong As It Seems. Russia's production levels in 2016 have been surprisingly strong, exceeding our expectations. The collapse of the Russian Ruble has allowed for continued internal investment despite the substantial reduction to dollar-denominated oil revenues. Still, it is likely that Russian producers are pulling very hard on their fields, over-producing the optimal level in an effort to scratch out higher revenues. Such over-production is not sustainable ad infinitum, and Russia may know that its fields need a rest in 2017 anyhow, so a 4-5% production cut is ultimately not much of a sacrifice. Make Room For Libya & Nigeria. Both Libya and Nigeria are trying to overcome substantial civil obstacles to allow production to increase back towards oilfield capabilities. If these problems were solved, we estimate Libya could increase production by 400,000-600,000 b/d while Nigeria could add 200,000-300,000 b/d. If KSA, OPEC, and Russia believe these countries will be able to re-establish shut-in production, they may conclude a production cut is necessary to make room for the growth, and to keep prices from collapsing. Entrenching U.S. Shale As The Marginal Barrel: If KSA and Russia can agree to a 1 MMb/d cut, U.S. shale-oil producers would be the first to take advantage of expected higher prices, given the fast-response nature of this production. This actually would work to the advantage of KSA and Russia and other low-cost producers in and outside OPEC, by firmly entrenching U.S. shale oil as the marginal barrel for the world market. On the global cost curve, shale sits in the middle some $30 to $40/bbl above KSA and Russia, which means that, as long as the global market is pricing to shale economics at the margin, these mega-producers earn economic rents on their production. In order to retain those rents, KSA and Russia will have to find a way to keep shale on the margin - i.e., regulate their production so that prices do not rise too quickly and encourage more expensive output to come on line. For KSA and Russia, it is better to climb the shale cost curve than to encourage the next tranche of production - such as Canadian oil sands - to come on to the market too quickly, or to further incentivize electric vehicles and conservation with run-away price increases, with too-sharp a production cut. Allowing prices to trade through a $65 - $75/bbl range or higher would no doubt produce a short-term revenue jump for cash-strapped producers - particularly those OPEC members outside the GCC. But it also would make most of the U.S. shales economic to develop, and incentivize other "lumpy," expensive production that does not turn off quickly once it is developed (e.g., oil sands and deepwater). This ultimately would crash prices over the longer term, making it difficult for the industry to attract capital. This is not an ideal outcome for KSA's planned IPO of Aramco, or Russia's sale of 19.5% of Rosneft, or their investors. Global Reinvestment Needs To Be Re-Stimulated. Stimulating non-OPEC reinvestment with higher oil prices and increased price-floor confidence may actually be needed in the not-too-distant future. IOCs have barely started to show the negative production ramifications of their 40% cuts to capex; cuts which will grow deeper in 2018. We expect these production declines to show up increasingly over the next four years, and there is not much the IOCs can do to stop it, since their mega-project investments generally require 3-5 years from the time that spending decisions are made until first oil is produced. With such huge cuts to future expenditures, and enormous amounts of debt incurred by the IOCs to pay for the completion of legacy mega-projects that will need to be repaid ($130B in debt added in the past two years), OPEC could see a looming shortage of oil developing later this decade if IOC-sponsored offshore production falls into steep declines, as we think is likely. To orchestrate a softer landing, to prevent oil prices from spiking too high due to a shortage of production, to head-off an acceleration in the pursuit of alternative fuels and/or the recessionary impact of an oil price spike, KSA may actually want to accelerate the re-start of global investment. Bottom Line: There are strongly credible and well-reasoned arguments that support the expectations for a successful establishment of a production cut from OPEC and Russia, as well as to doubt that such an agreement will be achieved (and adhered to) amid the political and economic competition between OPEC members and against non-OPEC producers. A successful agreement to cut production in excess of 1 MMb/d, as CES believes is likely, would be the more out-of-consensus call, with substantially bullish implications for oil prices and for our oil-levered investment strategy and stock recommendations. Even without a production cut, the NRG service remains strongly constructive on the investment strengths of high-quality Permian oil producers and the completion-oriented service companies that will benefit from increased U.S. shale spending. If a production cut is achieved, our investment cases become even stronger, as the U.S. shale producers and service companies would be the greatest beneficiaries of an upward step-change in oil prices. Matt Conlan, Vice President Energy Sector Strategy mattconlan@bcaresearchny.com Robert P. Ryan, Senior Vice President Commodity & Energy Strategy rryan@bcaresearch.com SOFTS Dairy: Moderate Upside In 2017H1 Dairy prices may have another 5%-10% upside over next three to six months, based on tightening supply in the global dairy market. China will become more important in the global dairy market. The country's dairy imports will continue heading north. Downside risks include elevated global dairy product inventory, a supply boost from major exporters, and a continuing strengthening dollar. We have been cautiously bullish on global dairy market since last October.1 Since then, the Global Dairy Trade (GDT) All-Products Price Index, which is widely used as a benchmark price for the market, has rallied over 50% in the past seven months off its November - March lows (Chart 3, panel 1). Chart 3Dairy: Tactically Bullish Now the question is: will the rally continue? A review of what had happened in 2015 and so far this year may be a good start of our analysis. A Terrible 2015 The GDT index tumbled to the lowest level on record in early August 2015. A sharply drop in Chinese dairy imports; the Russian import ban on dairy products; robust supply growth across major dairy producing countries; and the EU's decision to scrap its production quotas created a perfect storm for the global dairy market last year - resulting in an extremely oversupplied market, stock builds and depressed dairy prices (Chart 3, panels 2, 3 and 4). An Improving 2016 Fundamentals have improved since April, as major dairy exporting countries responded to low dairy prices, while Chinese dairy imports revived. Fonterra, the world's biggest dairy exporter, and Murray Goulburn, Australian's biggest dairy company, both announced retrospective price cuts in April to dairy farmers in New Zealand and Australia, which hit both countries' dairy industries hard. Many farmers exited the dairy business, given their production costs were well above farm-gate milk prices. As a result, dairy farmers In New Zealand have cut the national dairy cow herd size by 3.3% yoy in 2015 and then a further 1.5% in 2016, based on USDA data. In Australia, dairy farmers have sent more cows into slaughterhouse as well. According to Dairy Australia, in the past 12 months to August 2016, 109,102 head were sold, an increase of 33% on the previous year. New Zealand and Australia are the world's largest and the fourth largest dairy exporters, respectively. In June, one month before the start of the new season (July 2016 to June 2017), farm-gate milk prices set by major dairy processors in Australia were still much lower than most dairy farmers' production costs, further damaging the country's dairy production outlook for the 2016/17 season. In July, August and September, Australian milk production fell sharply for three consecutive months, with a yoy contraction of 10.3%, 9.3%, and 10.2%, respectively. In July, the European Commission funded a €150 million program to pay farmers to cut their milk production. At the same time, the region also intervened with a stock purchase program and a private-storage aid scheme to help remove excess supply from the market. The EU region is the world's second biggest exporter. Its production increase due to the removal of its quota system was one main reason for last year's price drop. The recent supportive policy has worked well - the region's milk volumes decreased in September for the third consecutive month. In the meantime, Chinese dairy imports have rebounded 9.7% yoy for the first nine months of this year, a significant improvement from last year's 44.4% contraction over the same period. China is the world biggest dairy importer, accounting for 51% of global fluid milk imports, and 40% of dry, whole-milk powder imports (Chart 4, panel 1). Chart 4China Needs More Dairy Imports In comparison, the number of Chinese cow herds only accounts for 6% of global total cows for milk production, which is clearly far from meeting its domestic demand (Chart 4, panel 2). Early this year the country loosened up the "one-child" policy, and now allows "two-kids" in a family, starting this year. This will increase the country's baby formula's demand. The country's dairy product intake per capita is still far below Asian peers like Japan and Korea. Growing family wealth and increasing demand for healthy dairy food will continue boosting the dairy consumption in China. Due to the limited pasture land in the country for raising cows, we expect China's dairy imports will continue heading north. What about the price outlook in the remainder of 2016 and 2017? Most of the positive factors aforementioned are still in place. In the near term, we do not see significant supply increase. Despite the 61% price rally in the GDT price index over the past seven months, most of the price increase still has not passed to farm-gate milk prices in major producing countries (except New Zealand). Hence, for the remainder of 2016 and 2017H1, we expect prices will be prone to the upside. Pullbacks are always possible. But overall we still expect another 5% to 10% upside over next three to six months for the GDT price index. Beyond 2017H1, the price outlook is less clear. If prices either go sideways or up, milk production in major producing countries should eventually recover. For now, we hold a neutral view for dairy prices in 2017H2. Downside Risks Chart 5Downside Risks First, global dairy stockpiles are much higher than previous years (Chart 5, panel 1). According to the European Commission, at the end of September, around 428 thousand metric tons (kt) of skimmed-milk powder (SMP) was in public intervention stocks, while another 73 kt SMP was in private storage. In addition, there also is about 90 kt butter and 19 kt cheese stored privately. As the EU still is aiming to cut milk production to boost dairy prices, we believe the odds of an unexpected release from storage in a fast and massive manner is low. The release will likely be gradual. Second, much of New Zealand's milk production is dependent on weather conditions, which have improved from mid-August. Moreover, Fonterra increased its farm-gate milk price to $6 per kgMS (kilogram milk solid) from $5.25 per kgMS last week, which was the third increase over the past four months. Since August, farm-gate milk price in New Zealand has already been up 41% and well above the country's production cost. A combination of both factors may boost the country's milk production more than the market expected. In this case, prices could decline in 2017H1. Third, if the U.S. dollar continues strengthening versus the RMB and other major exporters' currencies, this will tend to discourage purchases from China and encourage sales from New Zealand, the EU and Australia, which will be negative to dairy prices (Chart 5, panel 2). We will monitor these risks closely. Ellen JingYuan He, Editor/Strategist ellenj@bcaresearch.com 1 please see Commodity & Energy Strategy Weekly Report for softs section "Oil Markets Pricing In $20/Bbl Downside," dated October 1, 2015, available at ces.bcaresearch.com Investment Views And Themes Recommendations Tactical Trades Commodity Prices And Plays Reference Table Closed Trades

In this <i>Special Report</i>, we discuss the state of the New Zealand business cycle and propose some trade ideas to capitalize on the excessive pessimism currently at play in New Zealand bond and currency markets.