Defensive/Risk

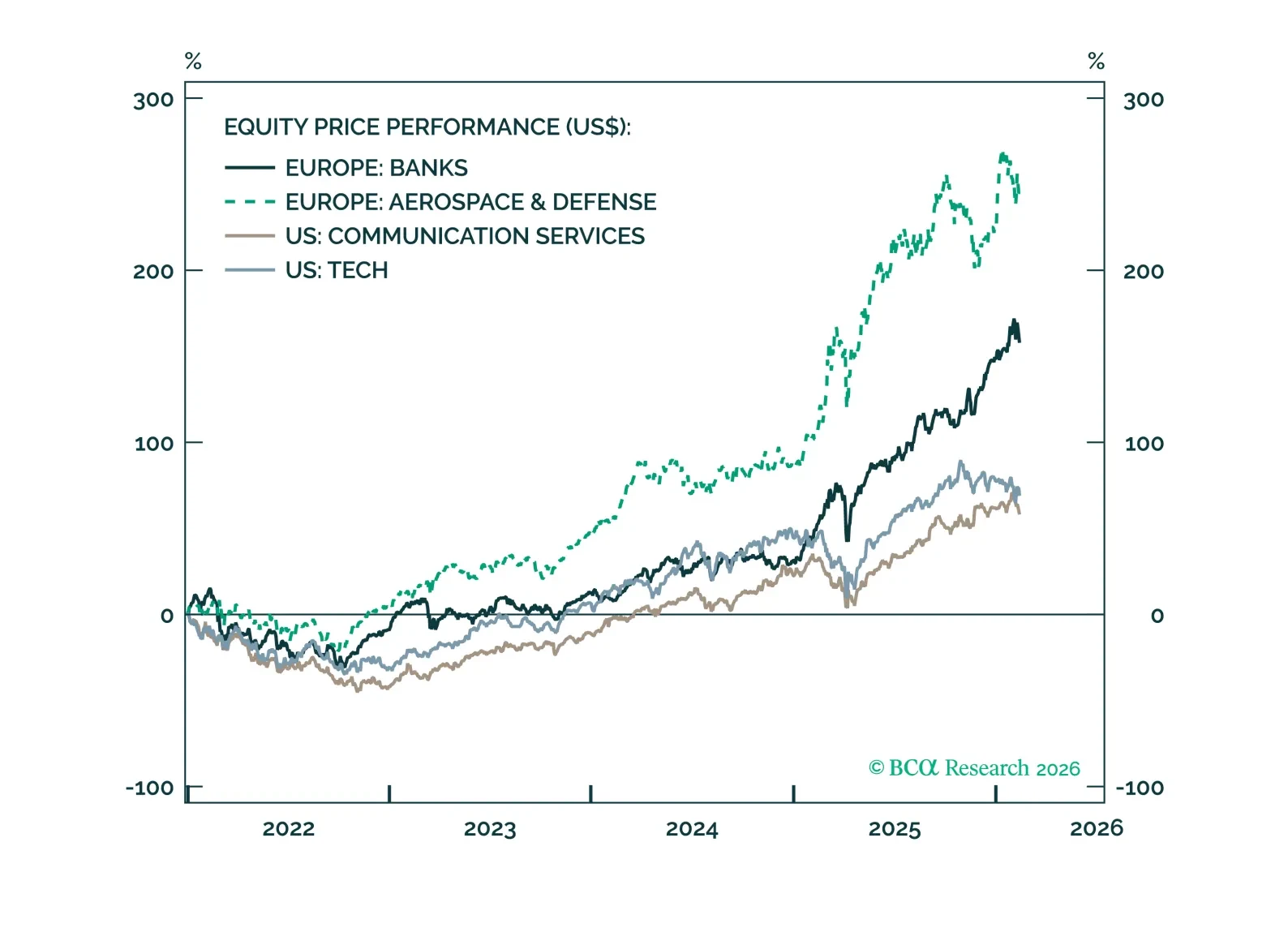

The near-term outlook is less supportive for European banks and defense equities. We downgrade banks to neutral and continue to expect defense stocks to trade in a “sell the rumor, buy the news” pattern.

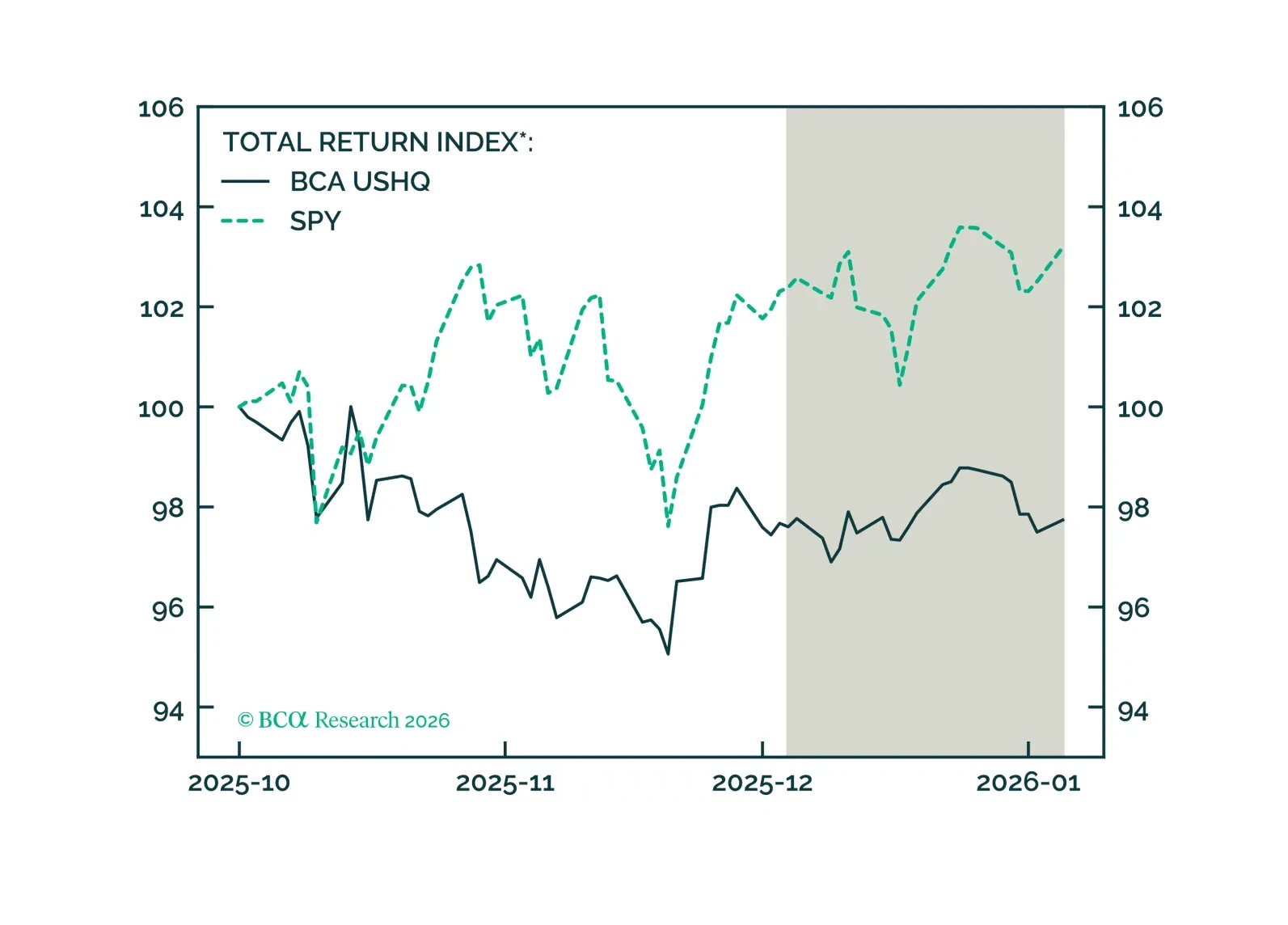

The US High Quality portfolio underperformed its benchmark through December, returning 0.14%, while its SPY benchmark returned 0.78%. On a trailing three-month basis, the USHQ portfolio’s performance was weaker than the benchmark, with USHQ underperforming by approx. 545bps.

We discuss which variables we are tracking to assess the risks to the bull market in the absence of government data. So far, we do not see any obvious red flags. Remain overweight on equities and fixed income.

Five questions, five answers from the road. We unpack what Europe’s biggest investors are worried about right now, from trade‑war whiplash to bund‑versus‑Treasury positioning; and where the real opportunities still lie.

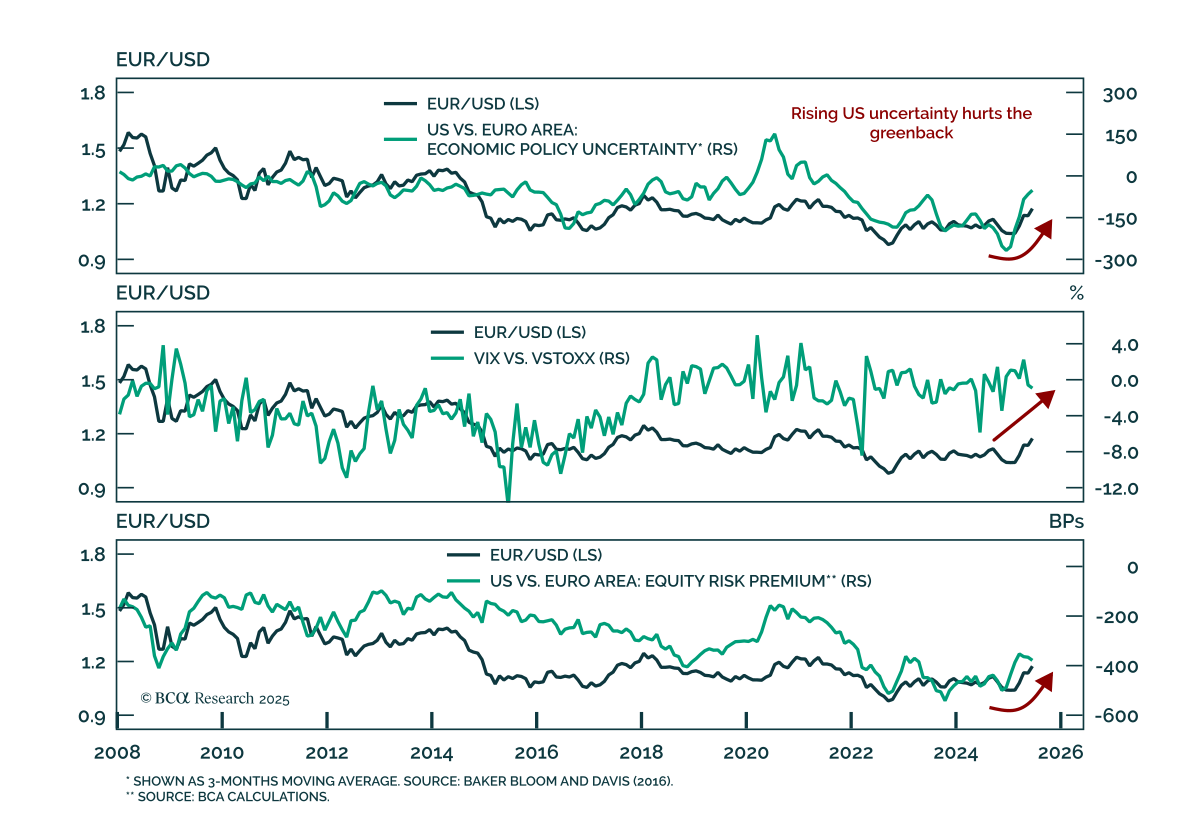

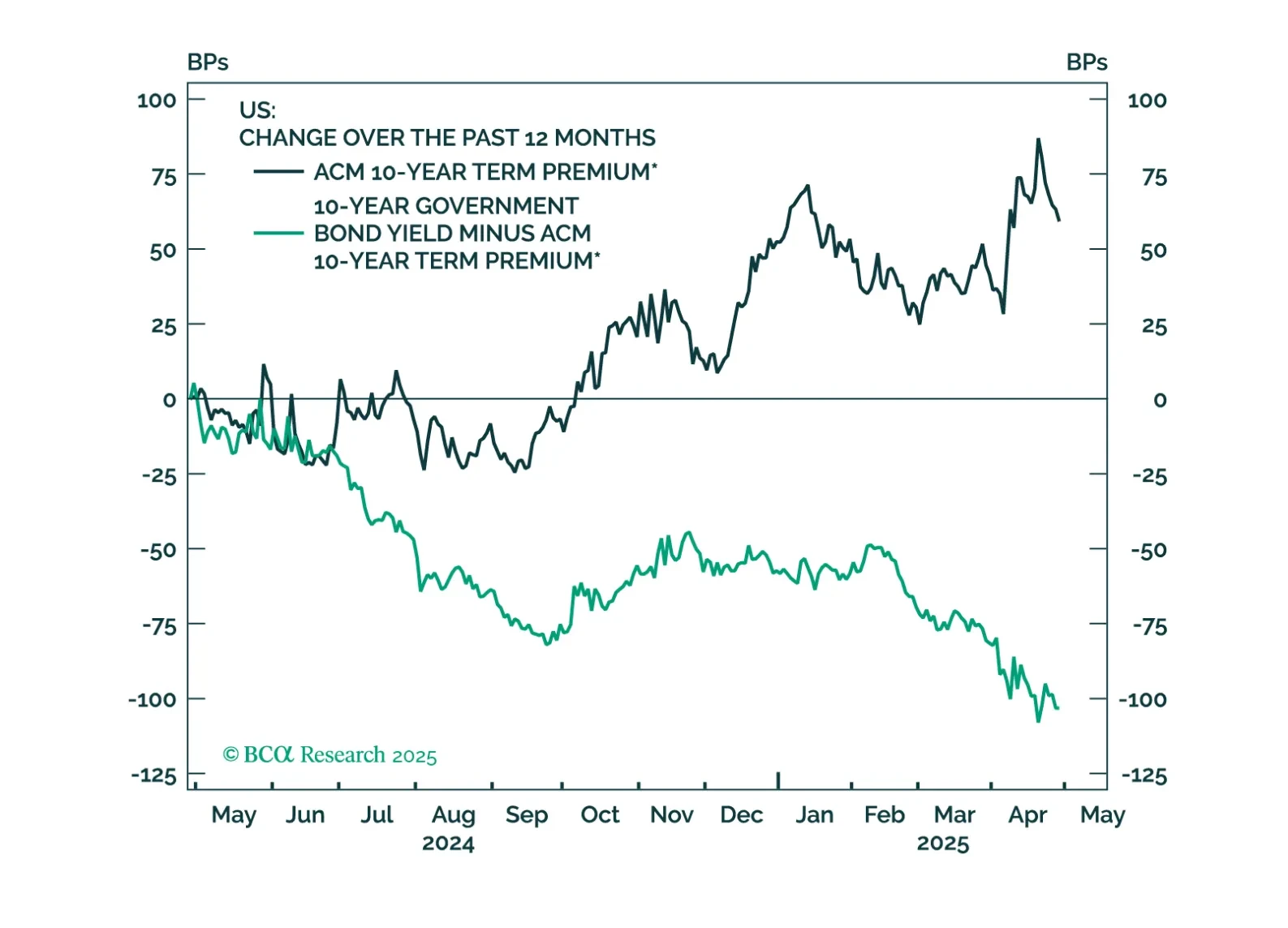

While most investors spent the month of April frantically refreshing their Twitter feeds for the next tariff announcement, we reiterate our stance that details on tariffs should be left to day traders. Long-term investors should be focused on the bigger story: the triple selloff in US stocks, bonds and the dollar. Foreign investors perceive that there has been a deterioration in governance in the US, and are requiring a higher risk premium from America. While Trump has walked back some of his most aggressive rhetoric, business investment will not resume unless we get clarity in policy. We continue to recommend a defensive stance, but downgrade duration from overweight to neutral to protect ourselves against shocks to the term premium. We also introduce Bitcoin to ours asset coverage. We upgrade it from underweight to neutral.

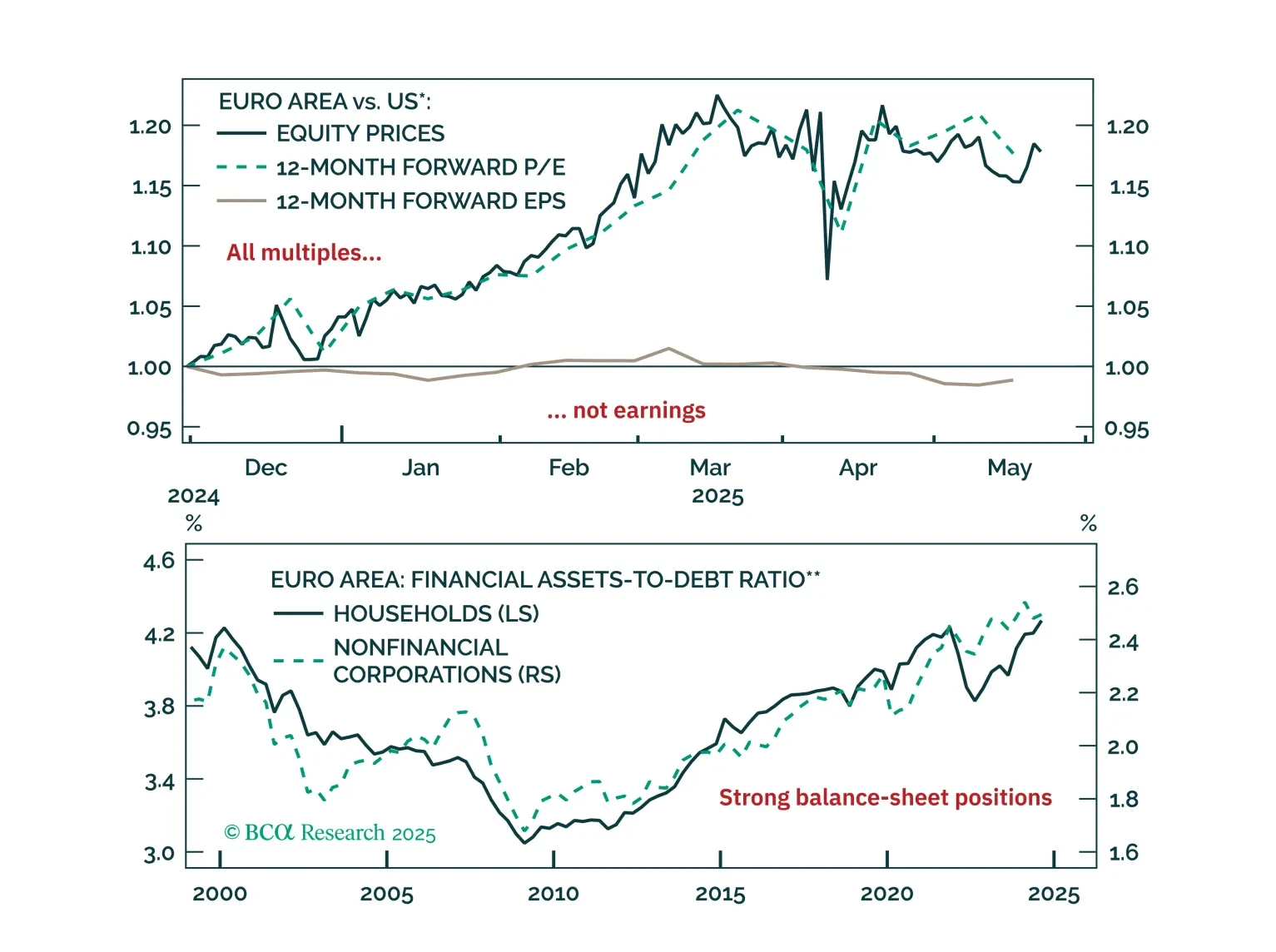

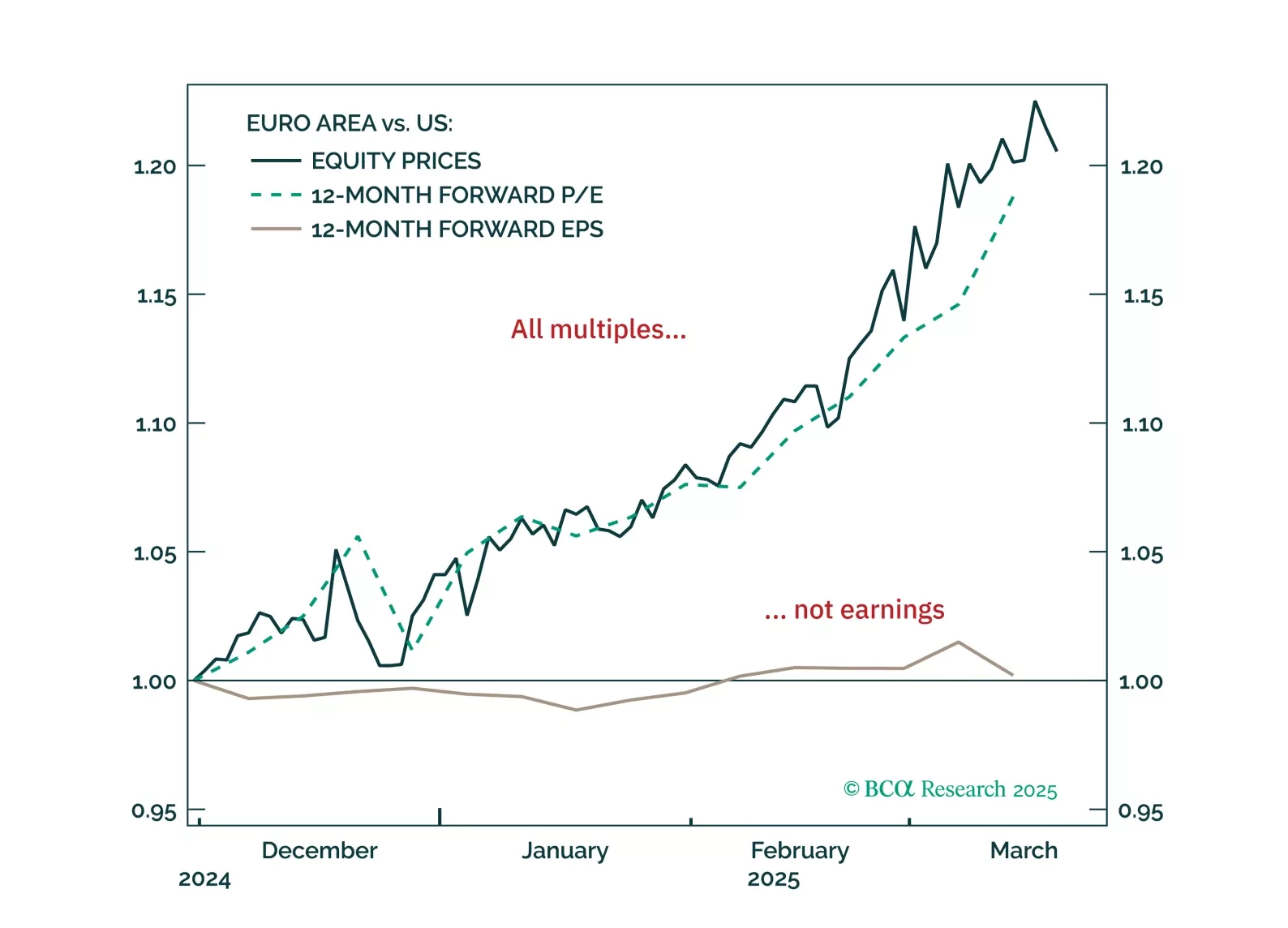

European equities have surged on hopes of a low-inflation boom—but the rally has likely gone too far, too fast. With a pullback now likely, how should investors position themselves over the next 3–6 months?

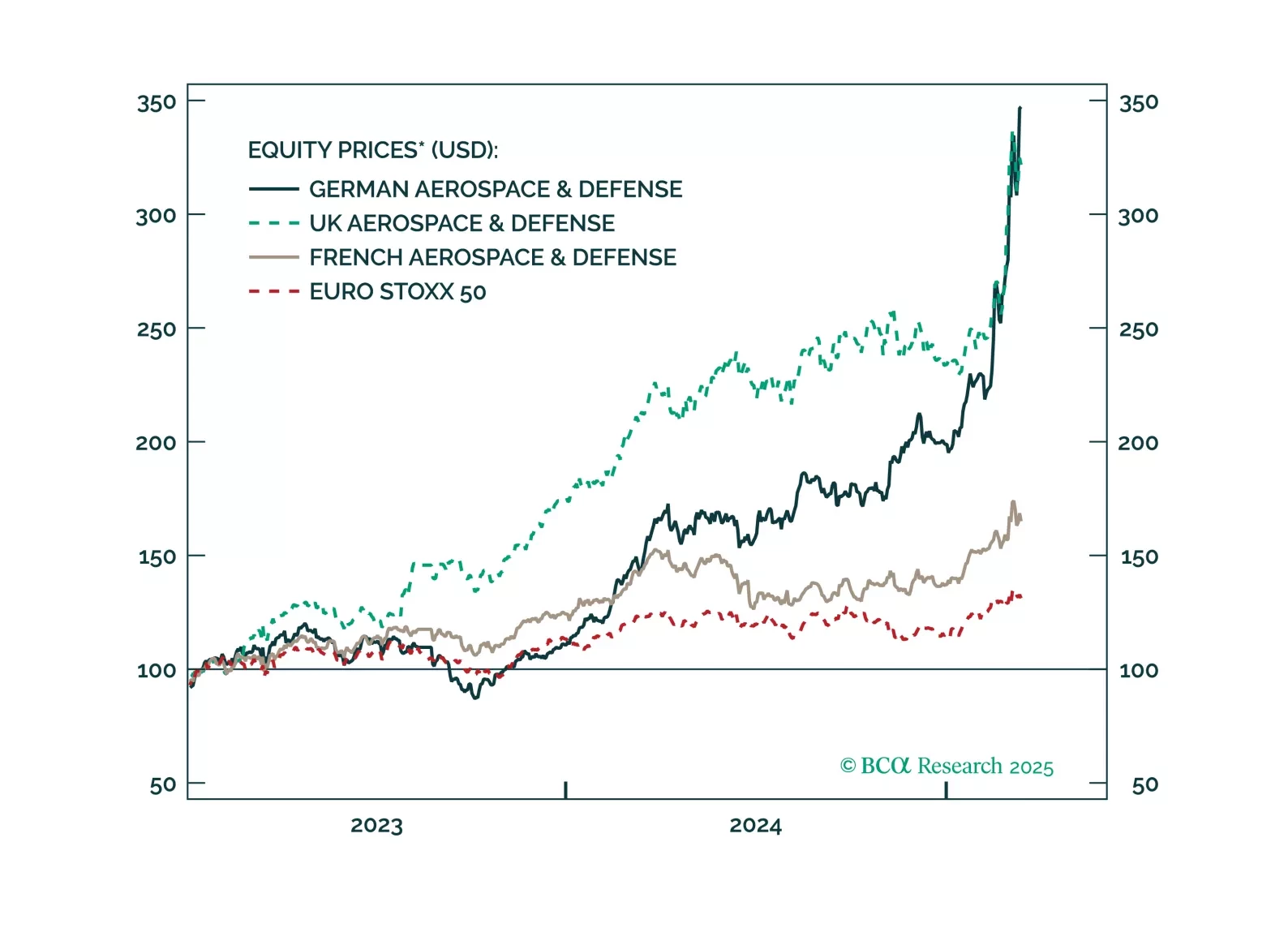

Investors should not chase the rally in European defense names any further. Too much good news has been priced in too quickly.

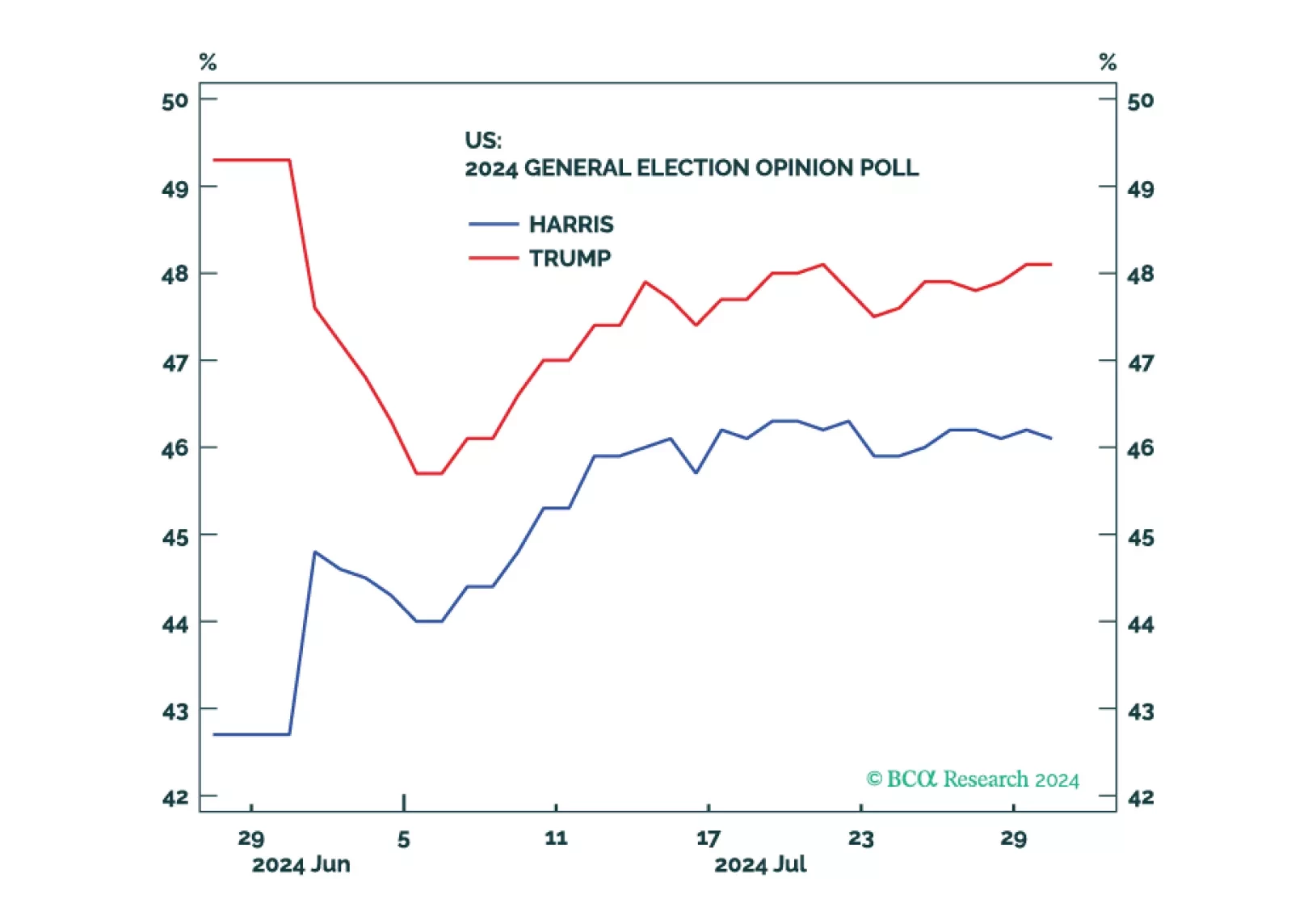

Republicans are favored but the election is still competitive. Equities, corporate credit, and cyclical sectors will fall until policy uncertainty is reduced.