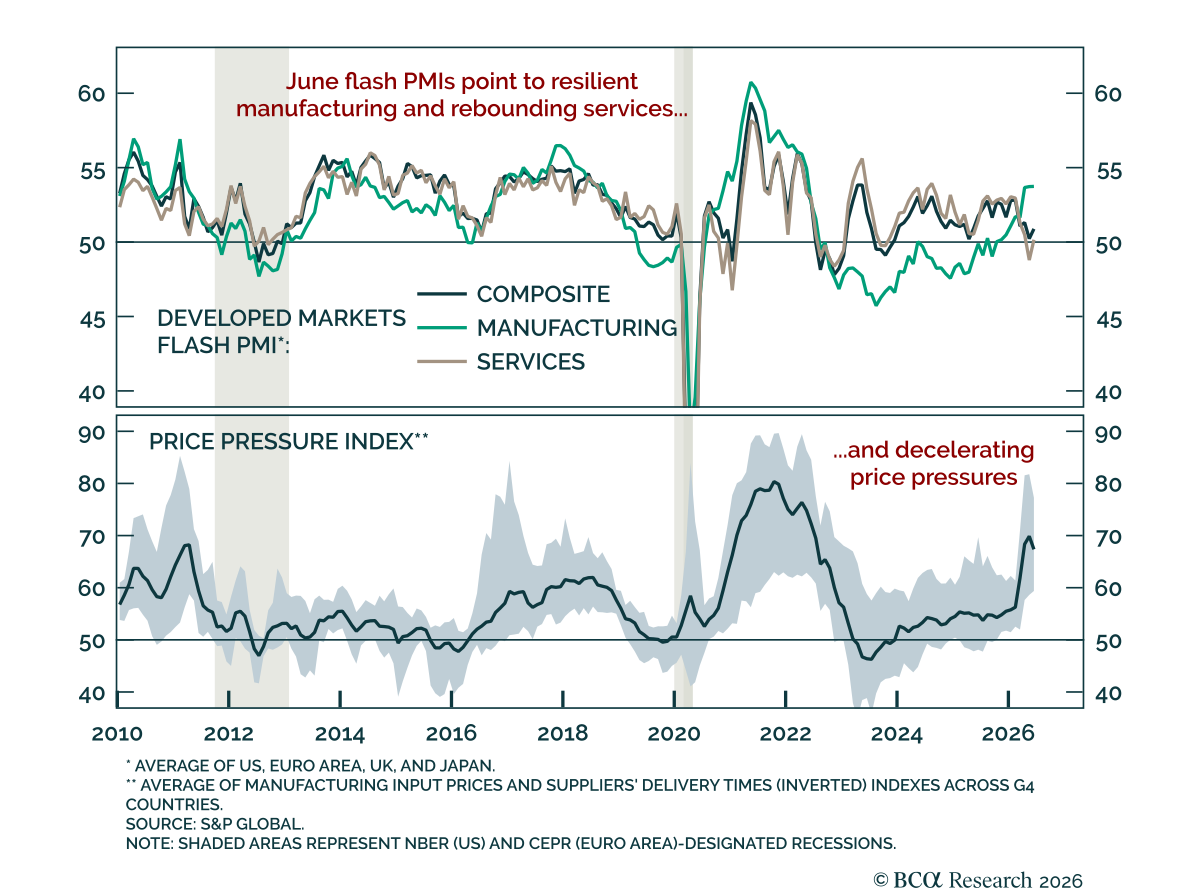

Developed Countries

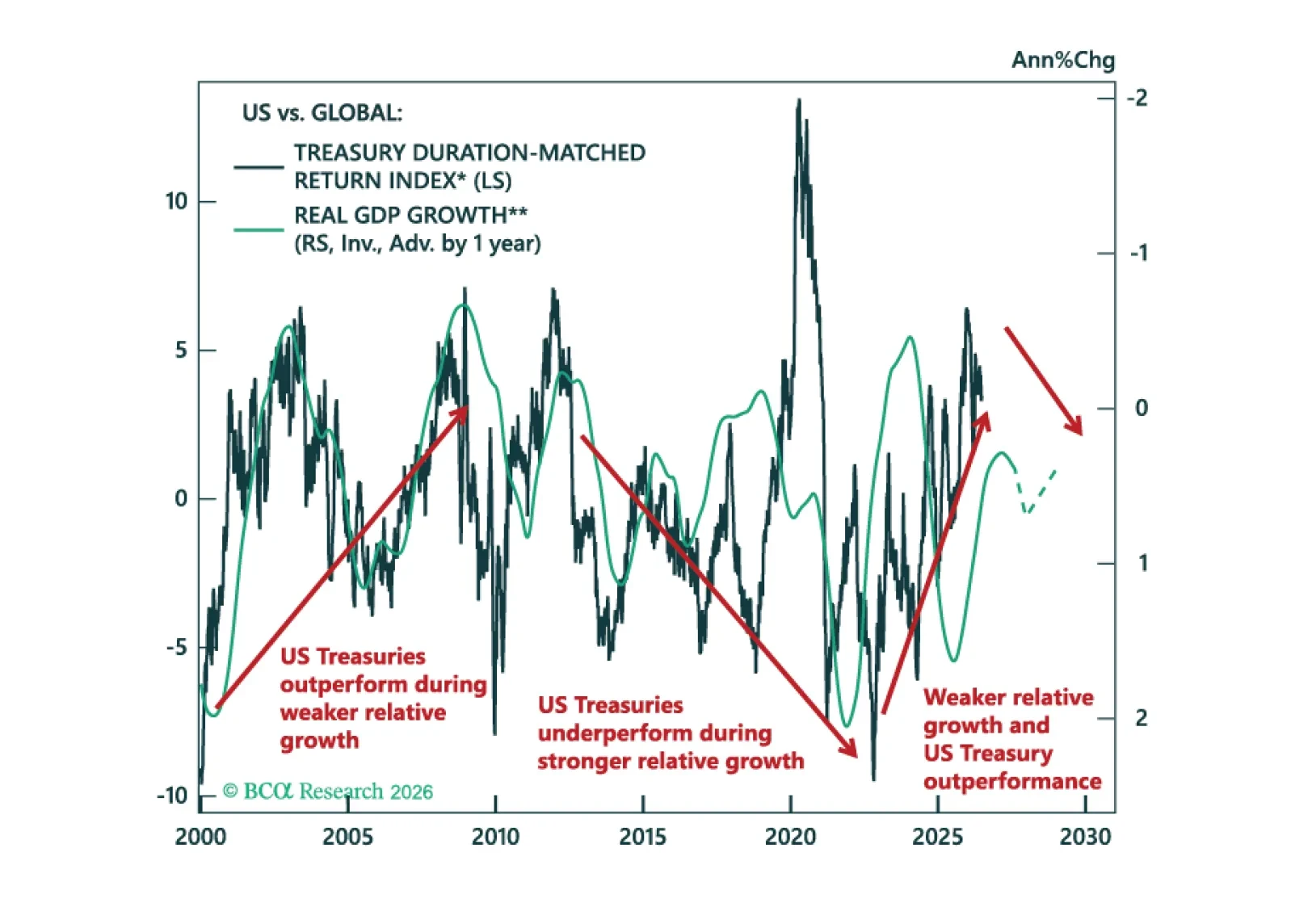

We review our Model Bond Portfolio performance for Q2 and look ahead as fixed income markets move beyond the US-Iran conflict, which is finding its kinetic equilibrium. Valuations and growth differentials are moving against continued US Treasury outperformance.

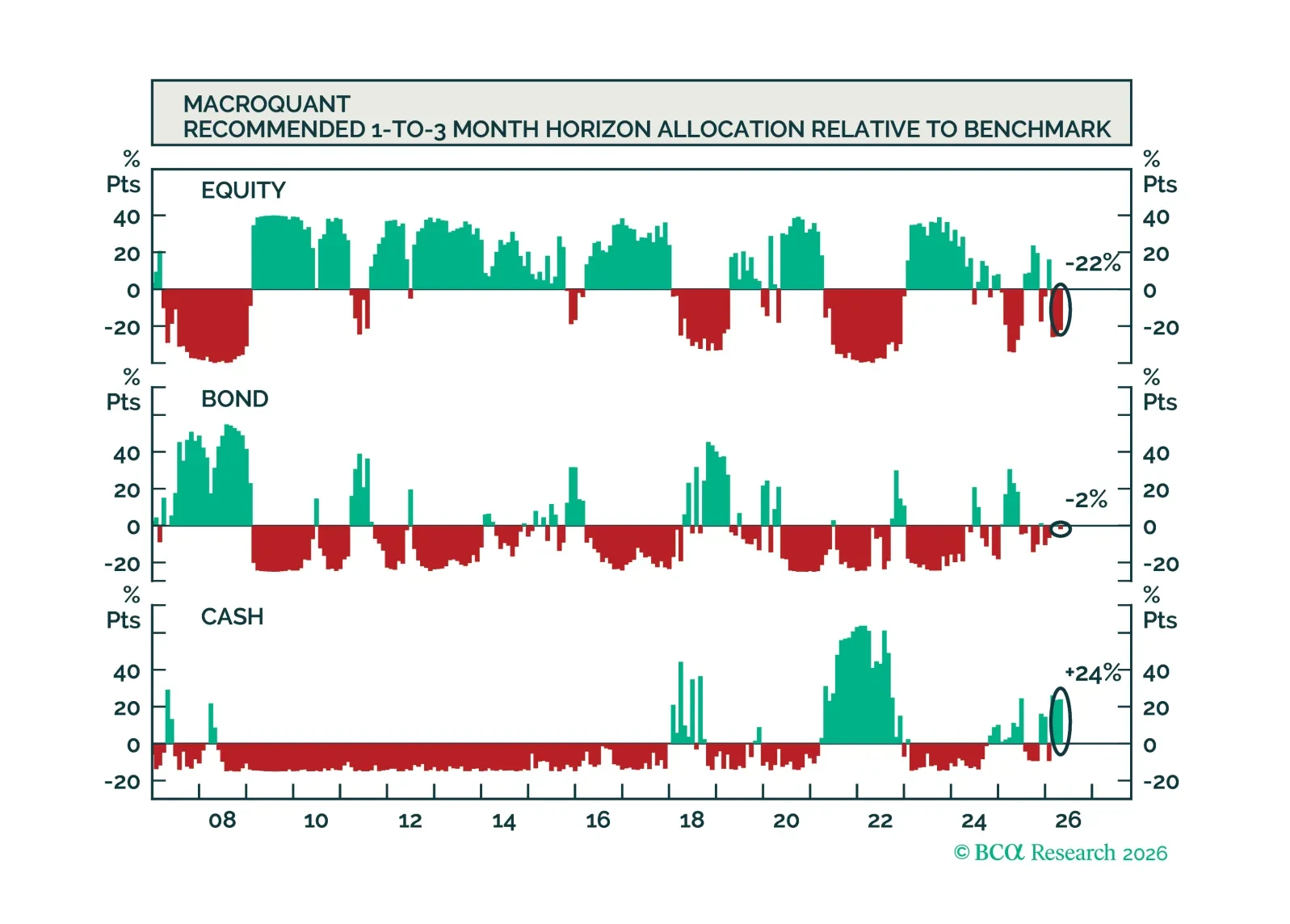

Our Portfolio Allocation Summary for July 2026.

MacroQuant recommends underweighting equities and adopting a benchmark duration stance in fixed-income portfolios. The model is very positive on the US dollar, bearish on gold, neutral on copper, and bullish on oil.

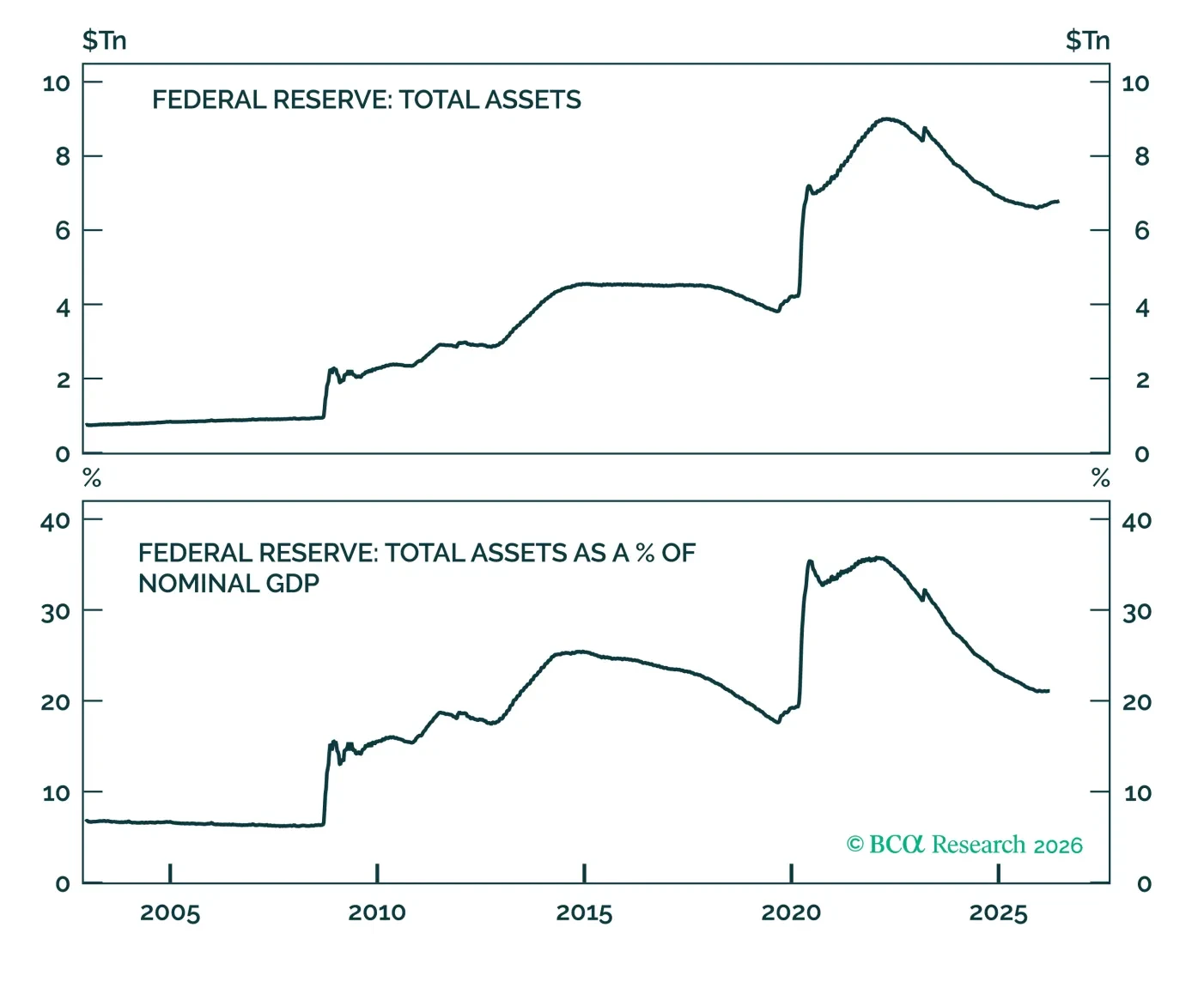

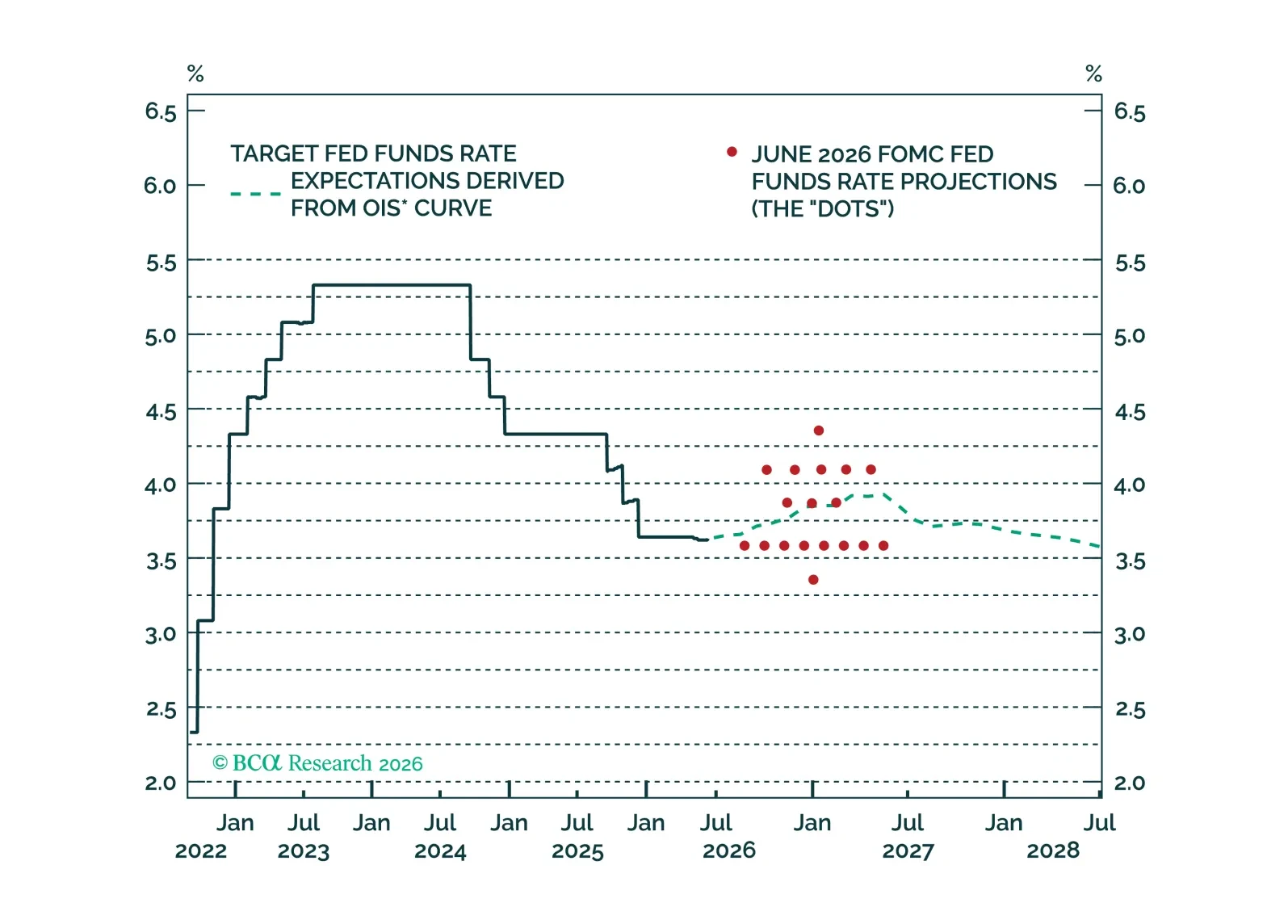

We discuss what recommendations to expect from the Fed’s balance sheet task force. We conclude that any future balance sheet consolidation will be smaller than many anticipate.

Kevin Warsh announced an ambitious reform agenda for the Federal Reserve. We discuss the potential impact and the current outlook for interest rates.

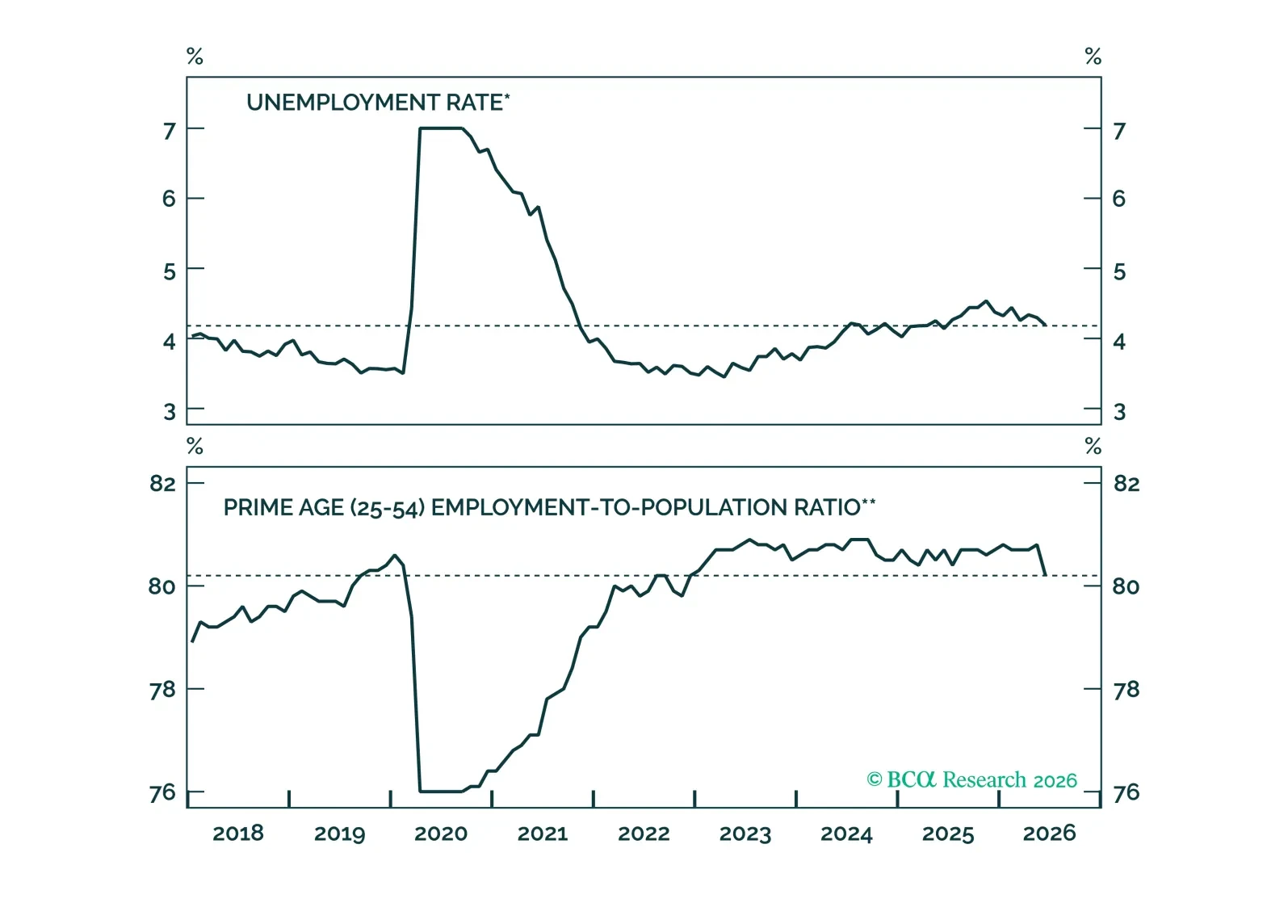

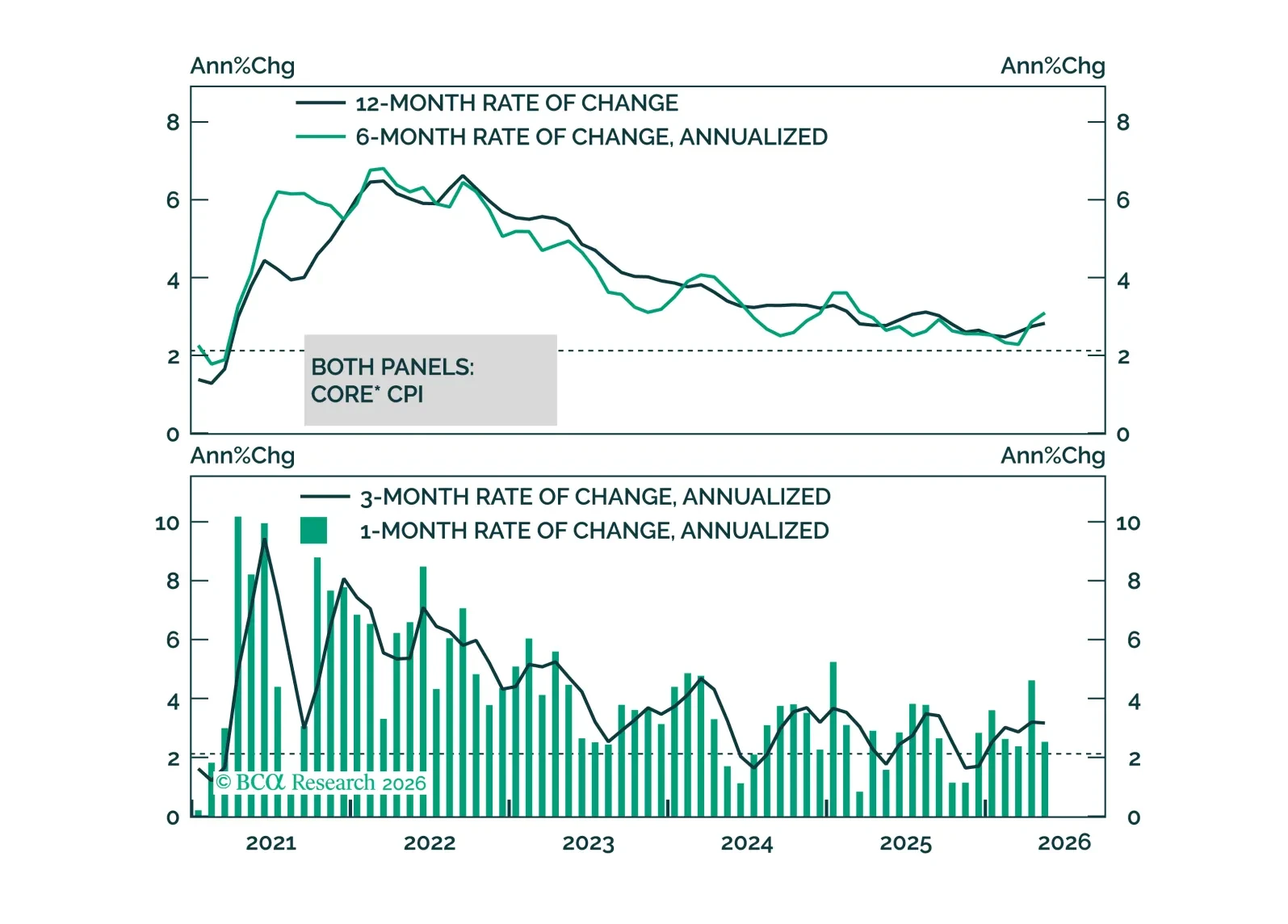

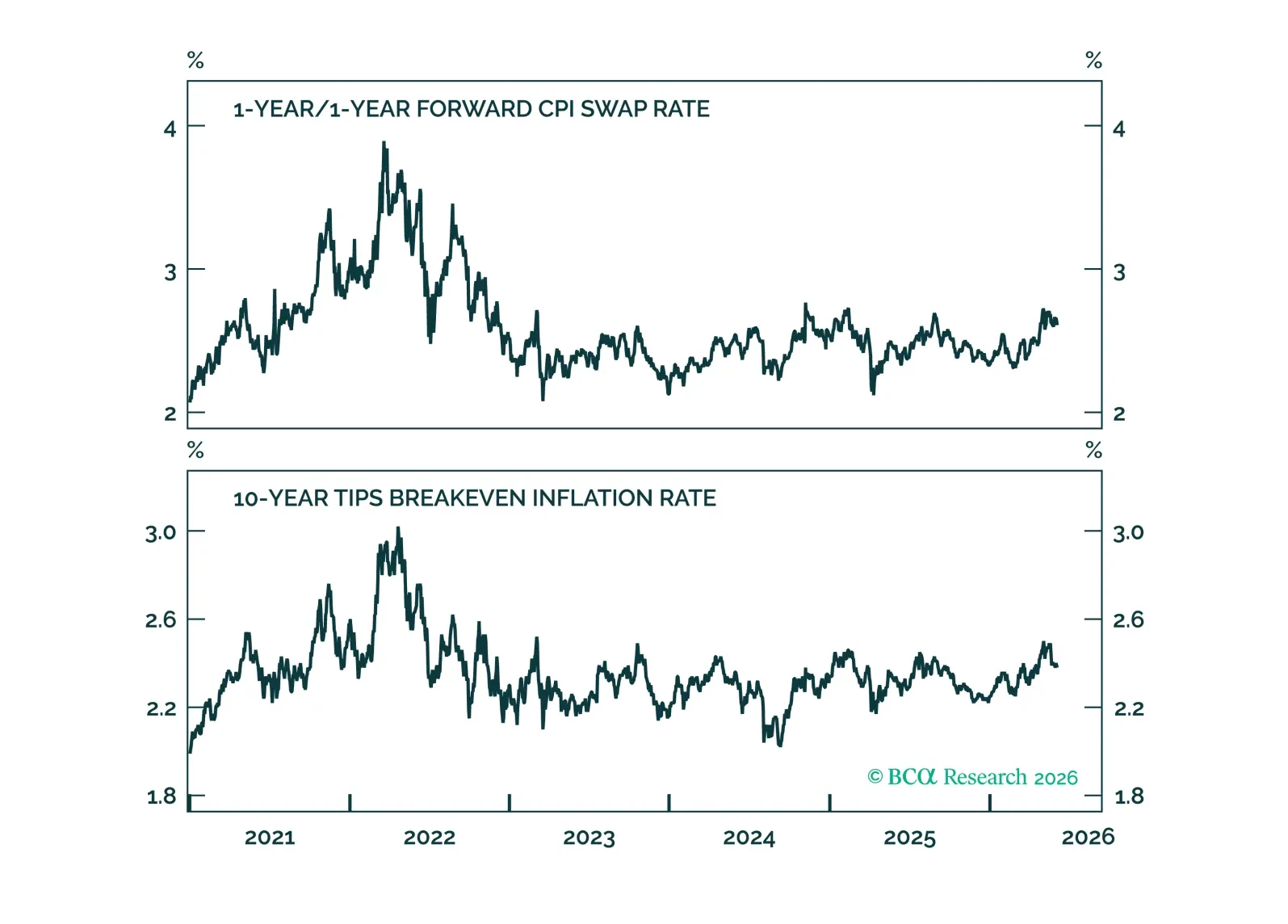

May CPI data show no evidence of passthrough from energy prices to core inflation. This will keep the Fed on hold for the time being.

Our Portfolio Allocation Summary for June 2026.

MacroQuant recommends a slight underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, is very positive on the US dollar, downgrades gold to underweight, upgrades copper to overweight, and remains very bullish on oil.

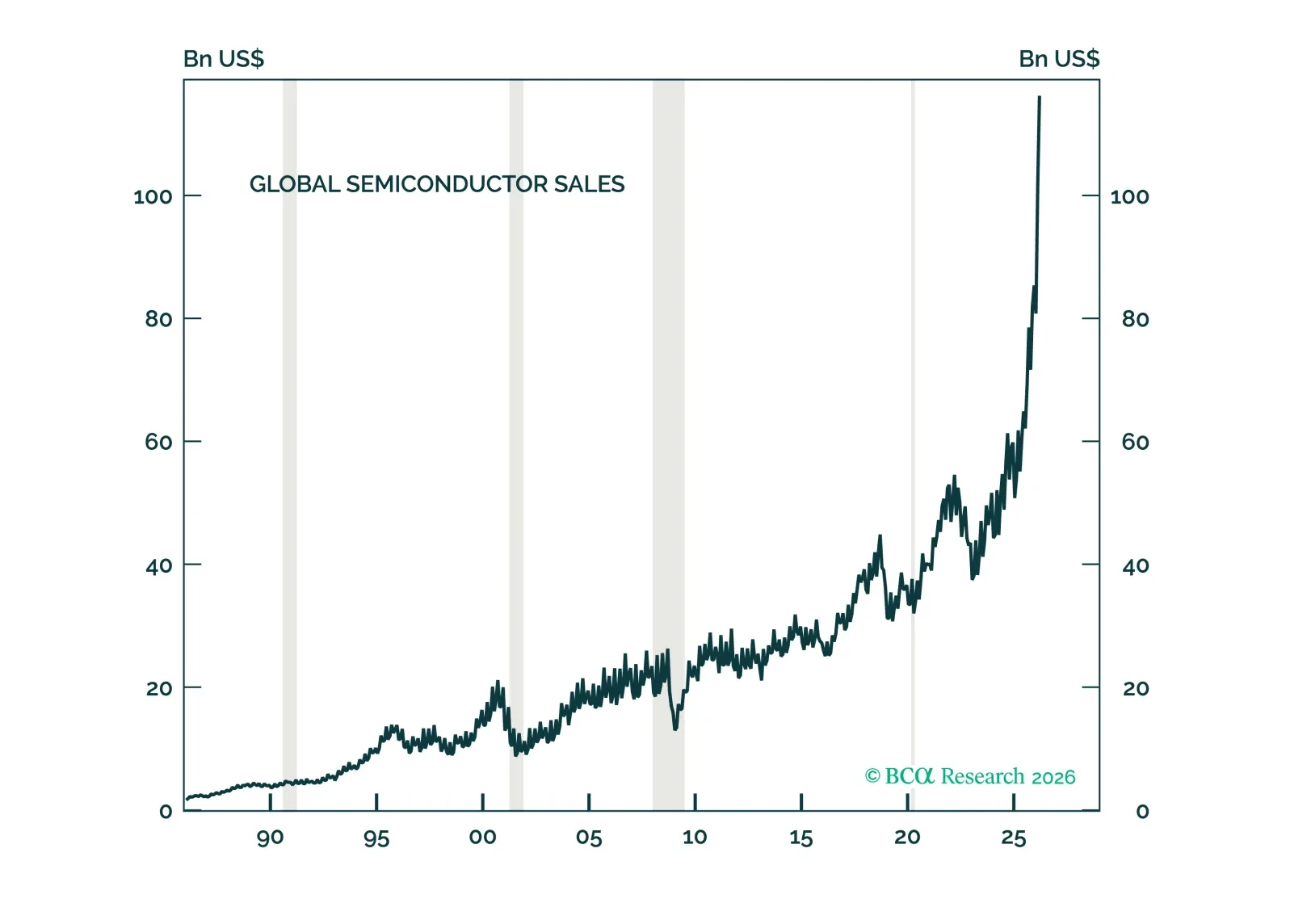

The AI bubble is a different type of bubble. It is primarily an earnings bubble rather than a valuation bubble. Like all bubbles, the AI bubble will burst. For now, however, our AI demand indicators do not suggest that this is imminent.