Developed Countries

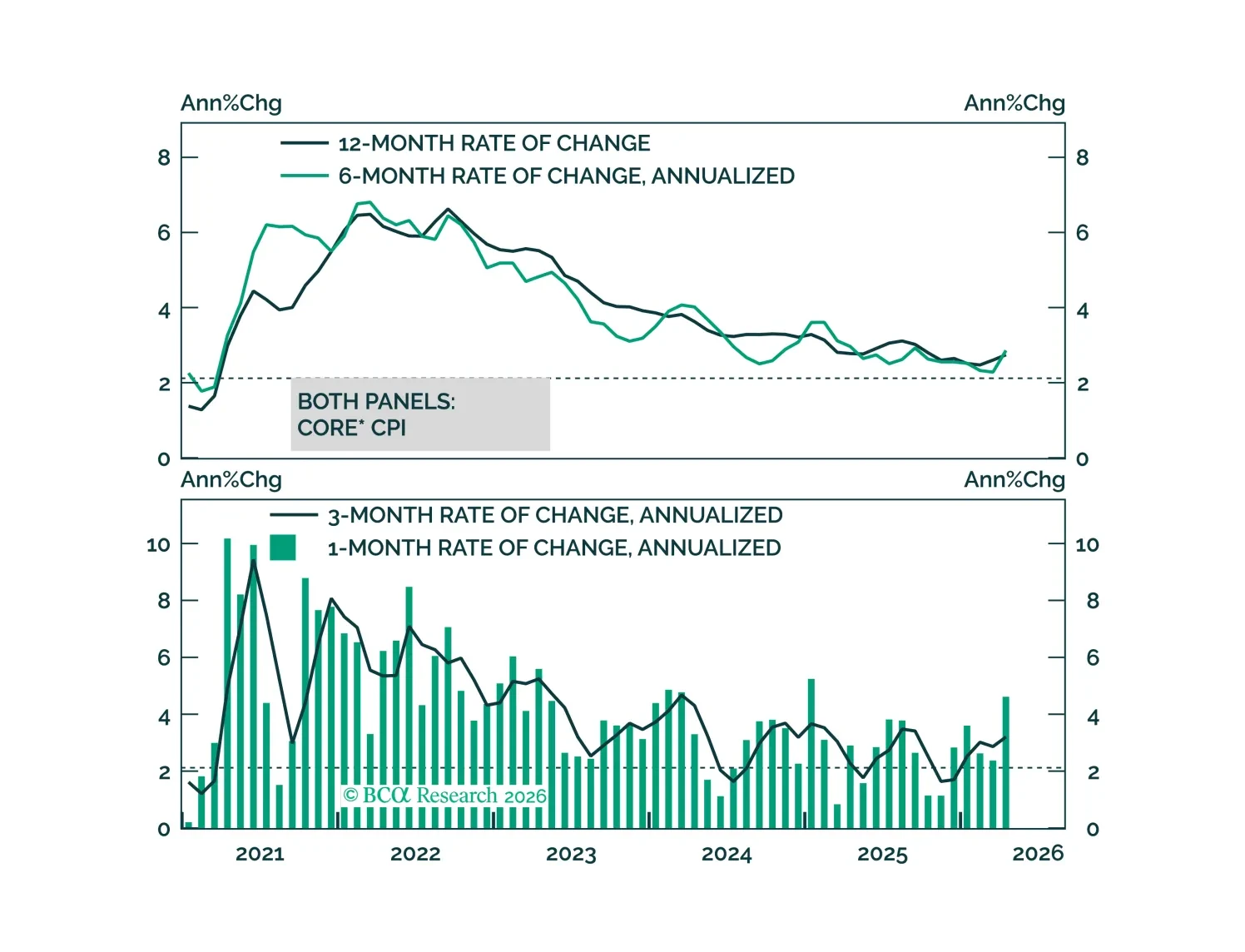

The April CPI report showed clear evidence of the direct effect of higher oil prices on inflation but, so far, limited evidence of passthrough to core.

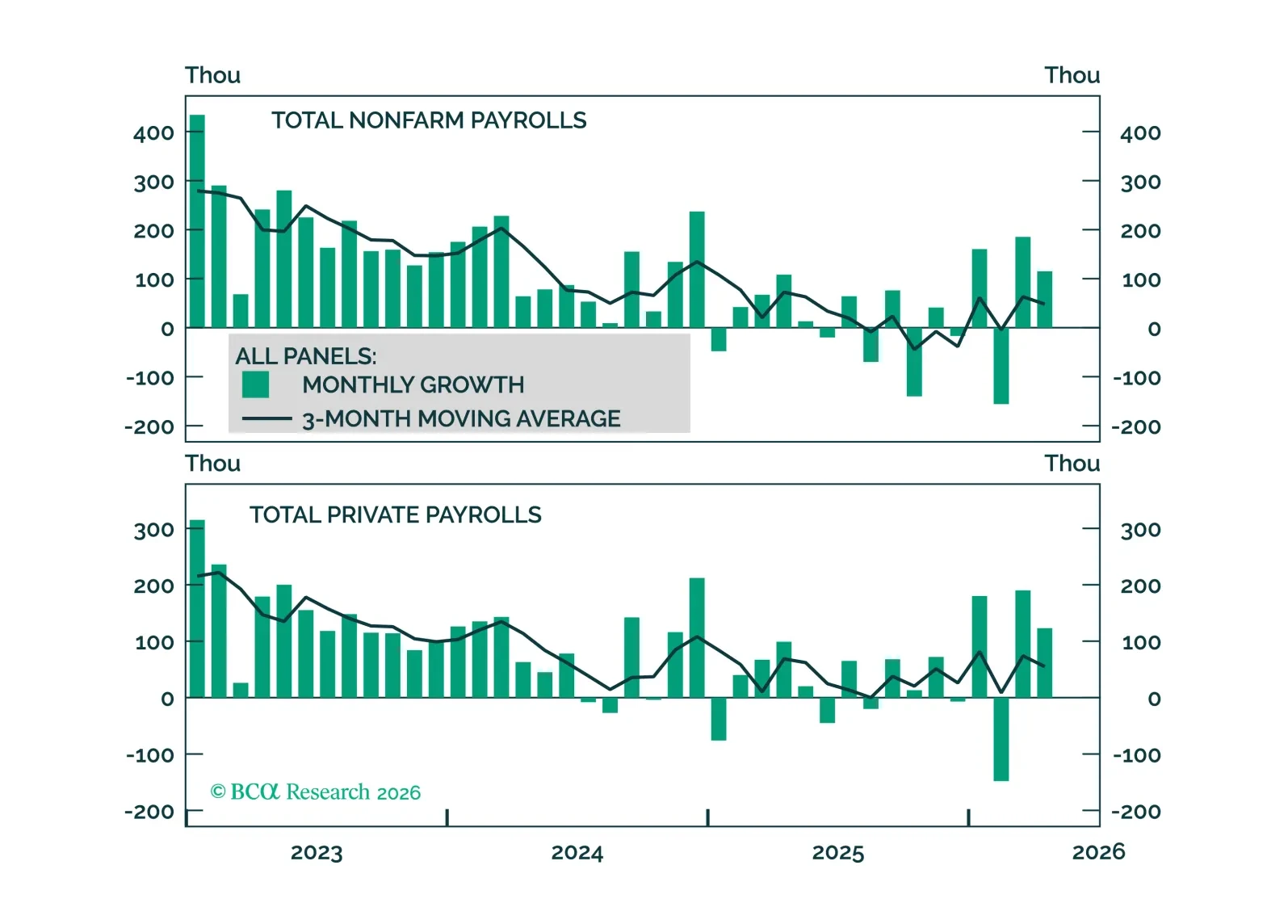

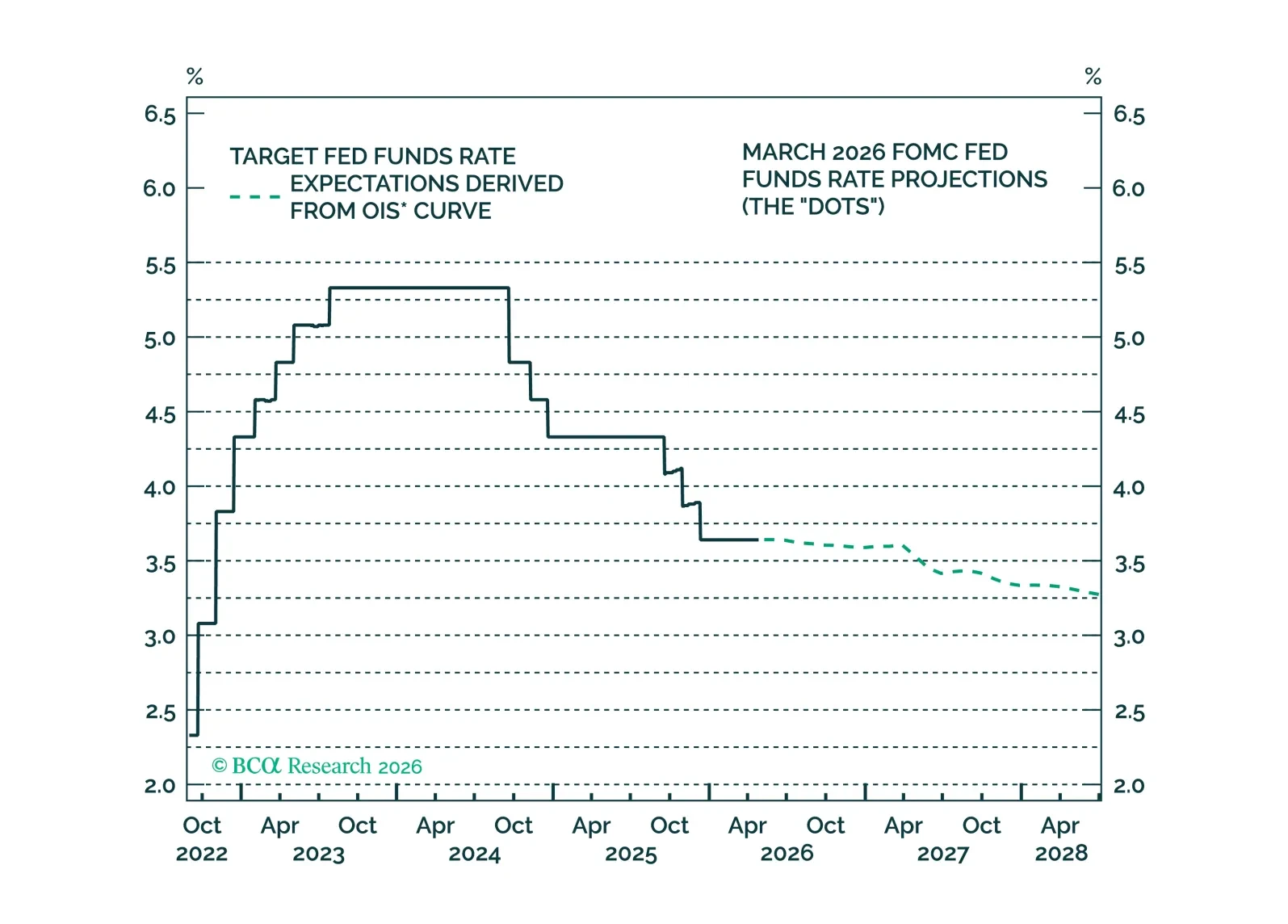

Improving job growth keeps Fed rate cuts off the table, but evidence of labor market tightening will be required before rate hikes become part of the discussion.

Our Portfolio Allocation Summary for May 2026.

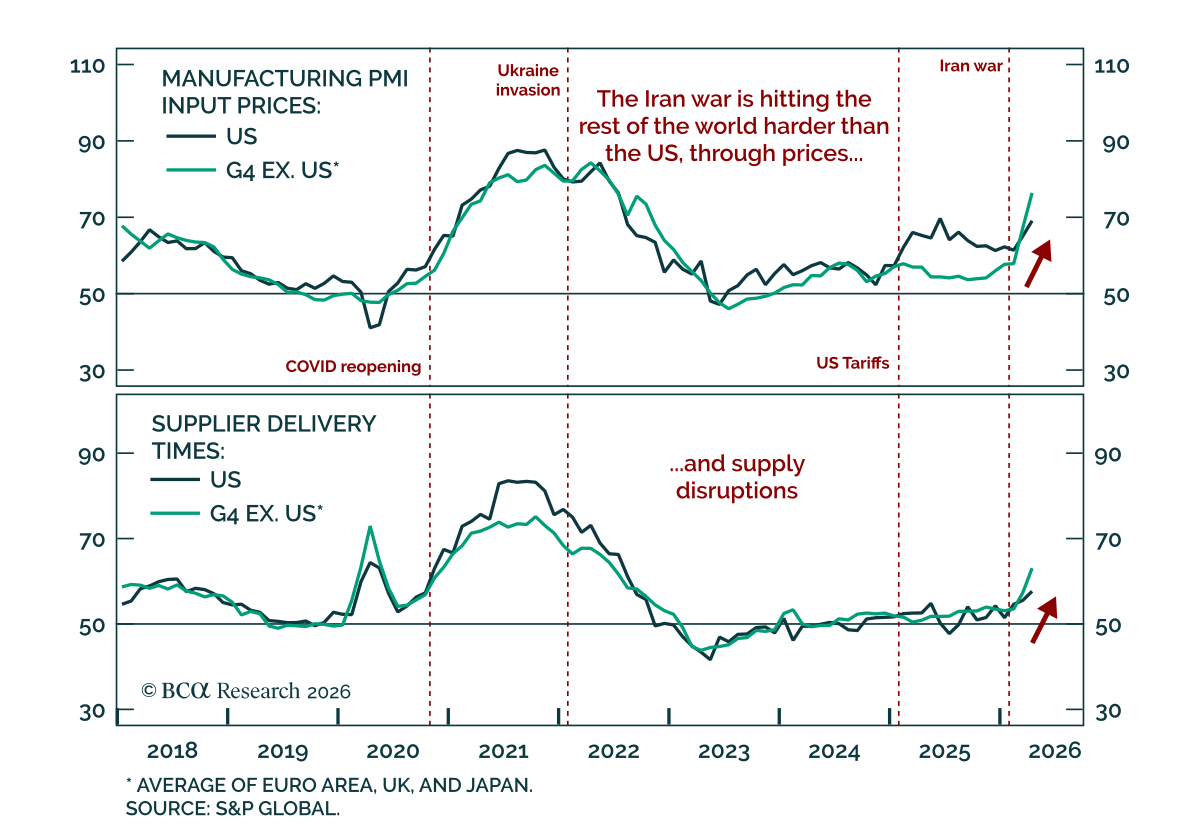

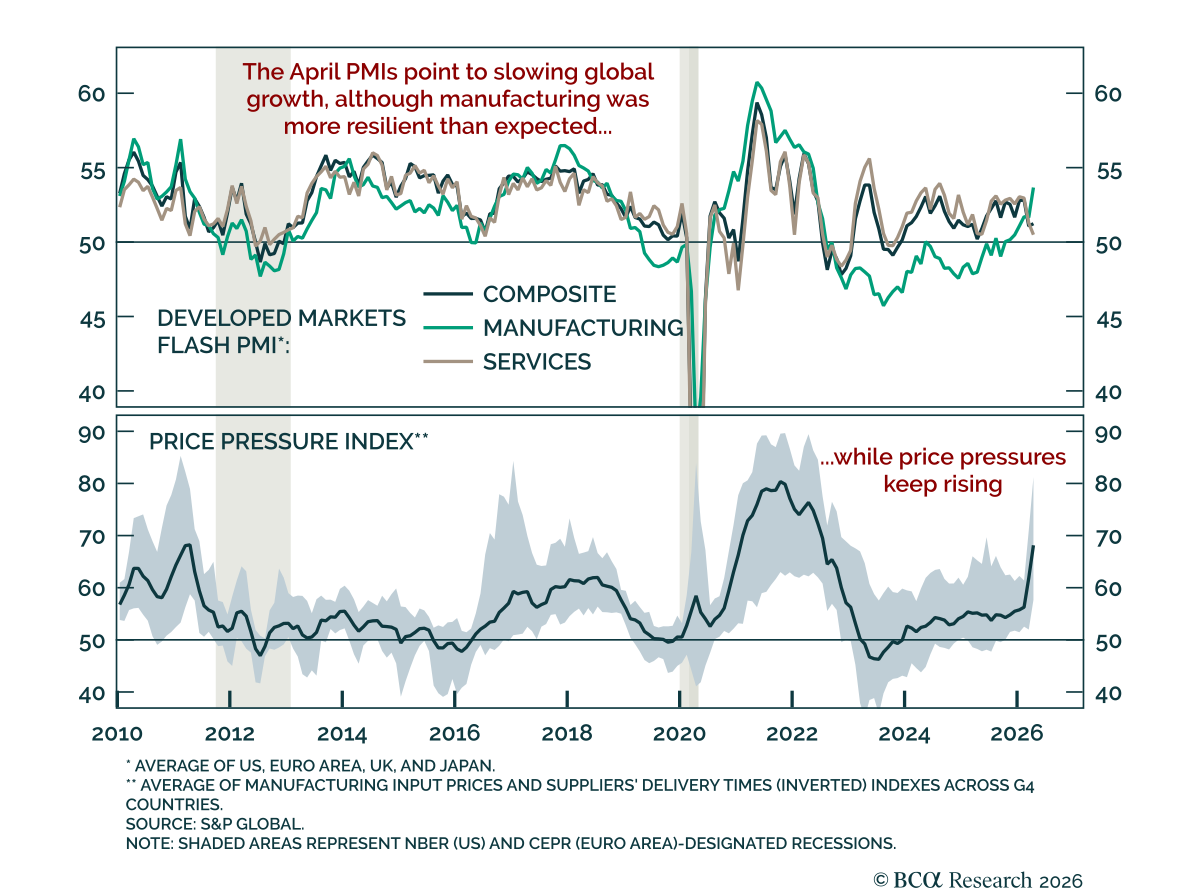

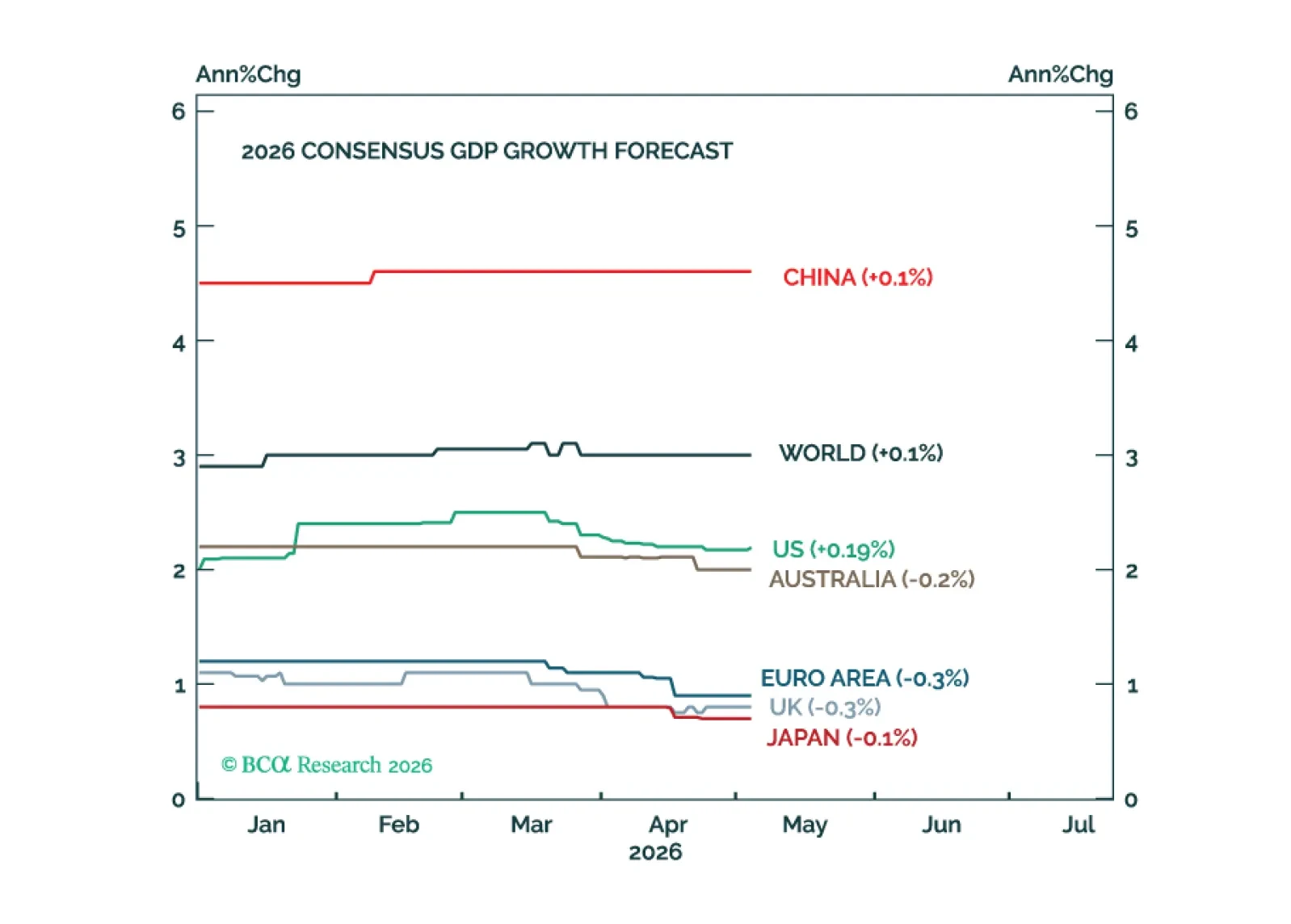

The global economy has weathered the oil shock reasonably well so far. However, the risk of a recession will increase meaningfully if the Strait of Hormuz remains closed into June.

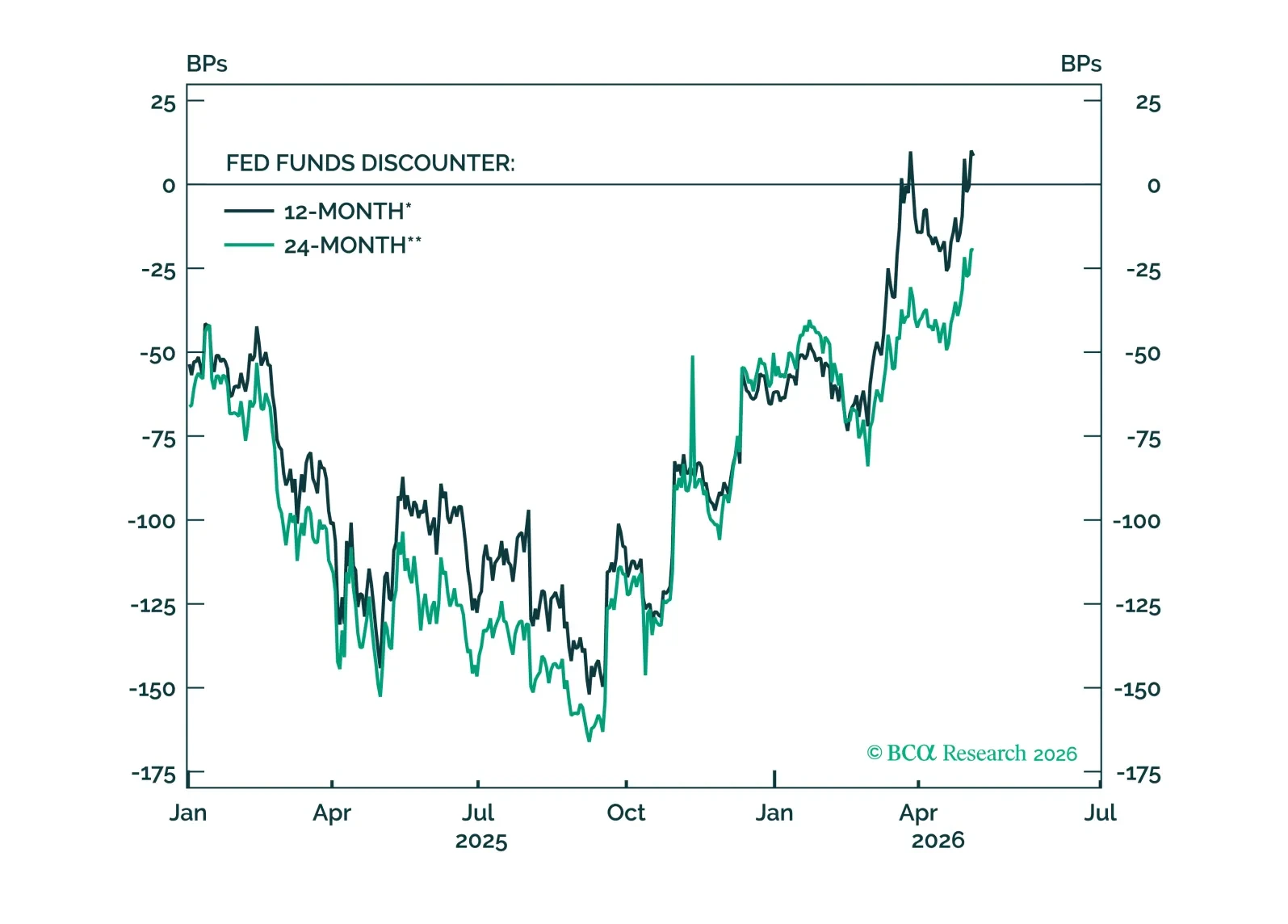

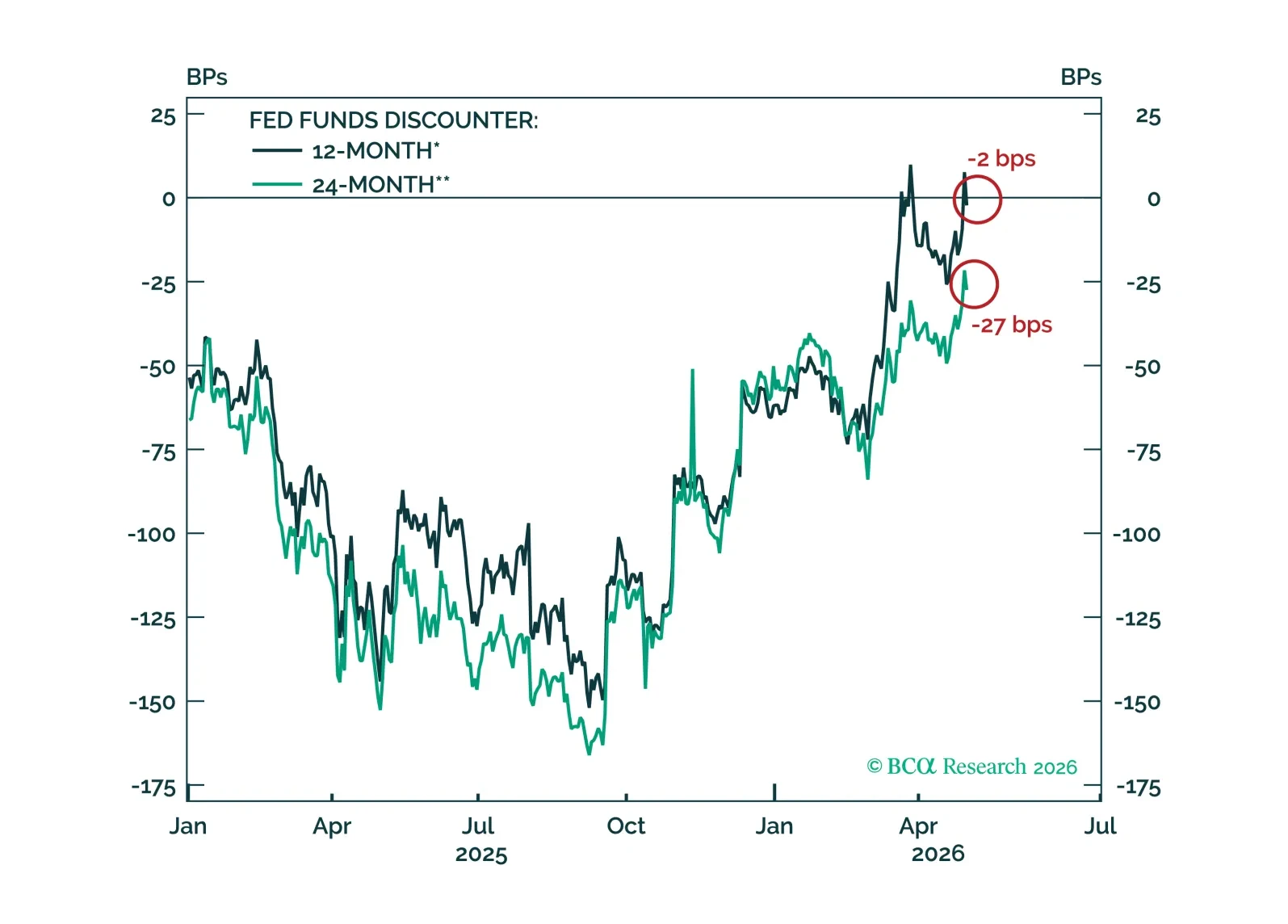

So far, there is no evidence of second-round effects from the oil price shock showing up in the US economy. Fed rate hikes are off the table unless those effects emerge.

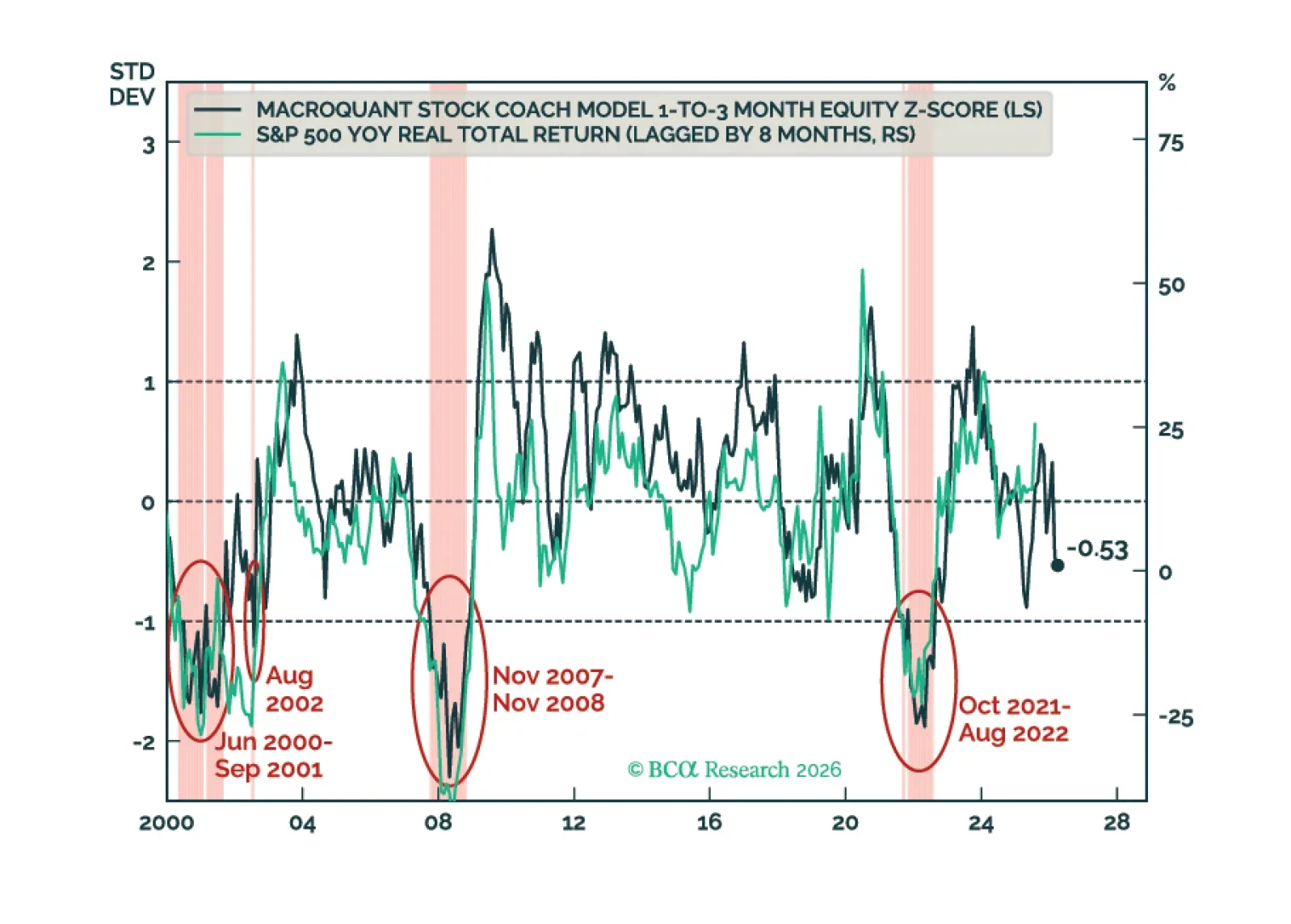

MacroQuant recommends an underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, is neutral-to-slightly positive on the US dollar, remains neutral on gold, upgrades copper to neutral, and is very bullish on oil.

FOMC participants are coalescing around the idea that the funds rate will stay on hold for some time, an outcome that is now well priced in the bond market and that will not materially change under a new Fed Chair.