Developed Countries

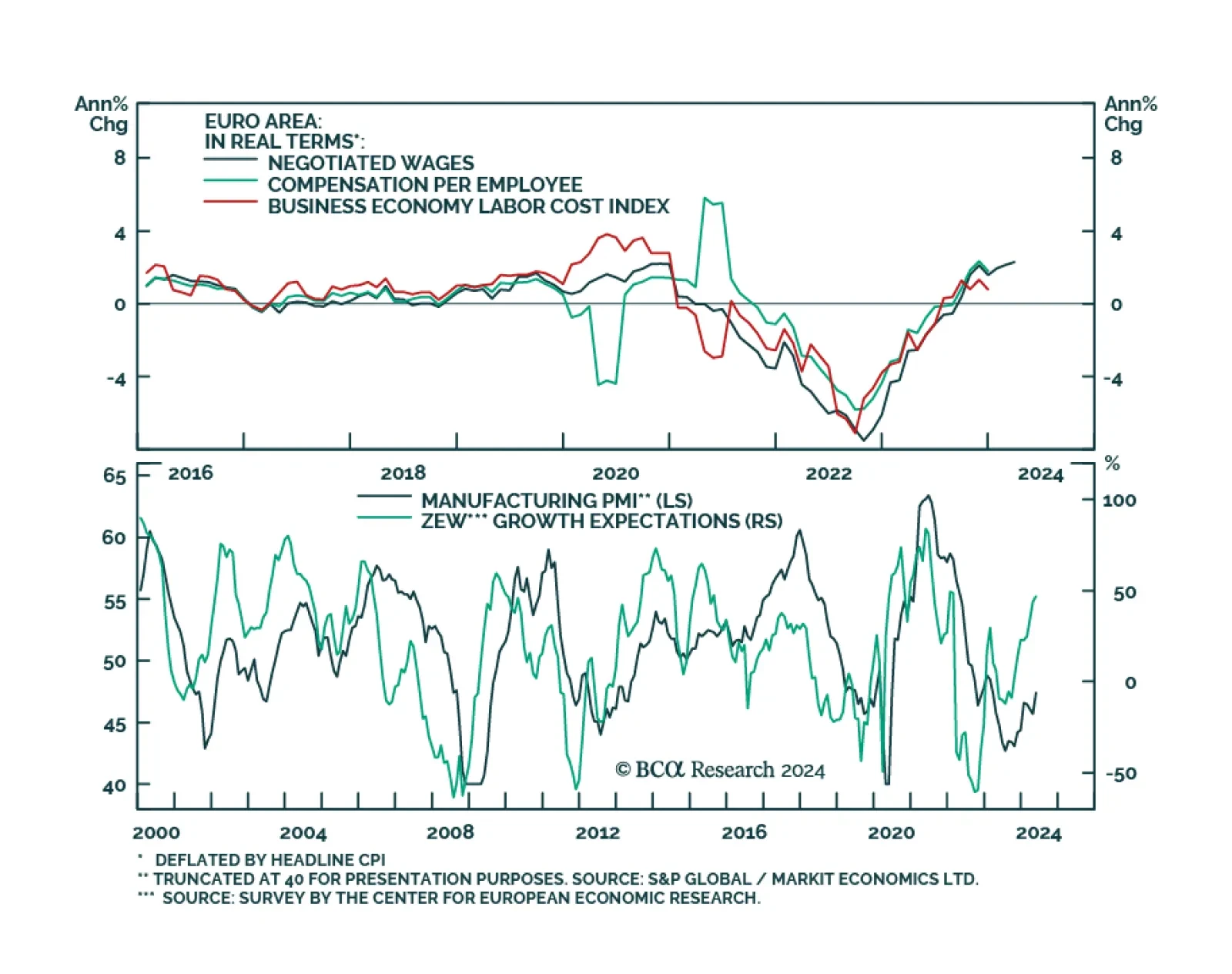

Negotiated wages rose 4.7% y/y in Q1, from 4.5% y/y in Q4 in the Eurozone. Meanwhile, preliminary estimates for the Eurozone Composite PMI surprised to the upside in May. Although wage growth is the main driver of services inflation and Euro Area economic…

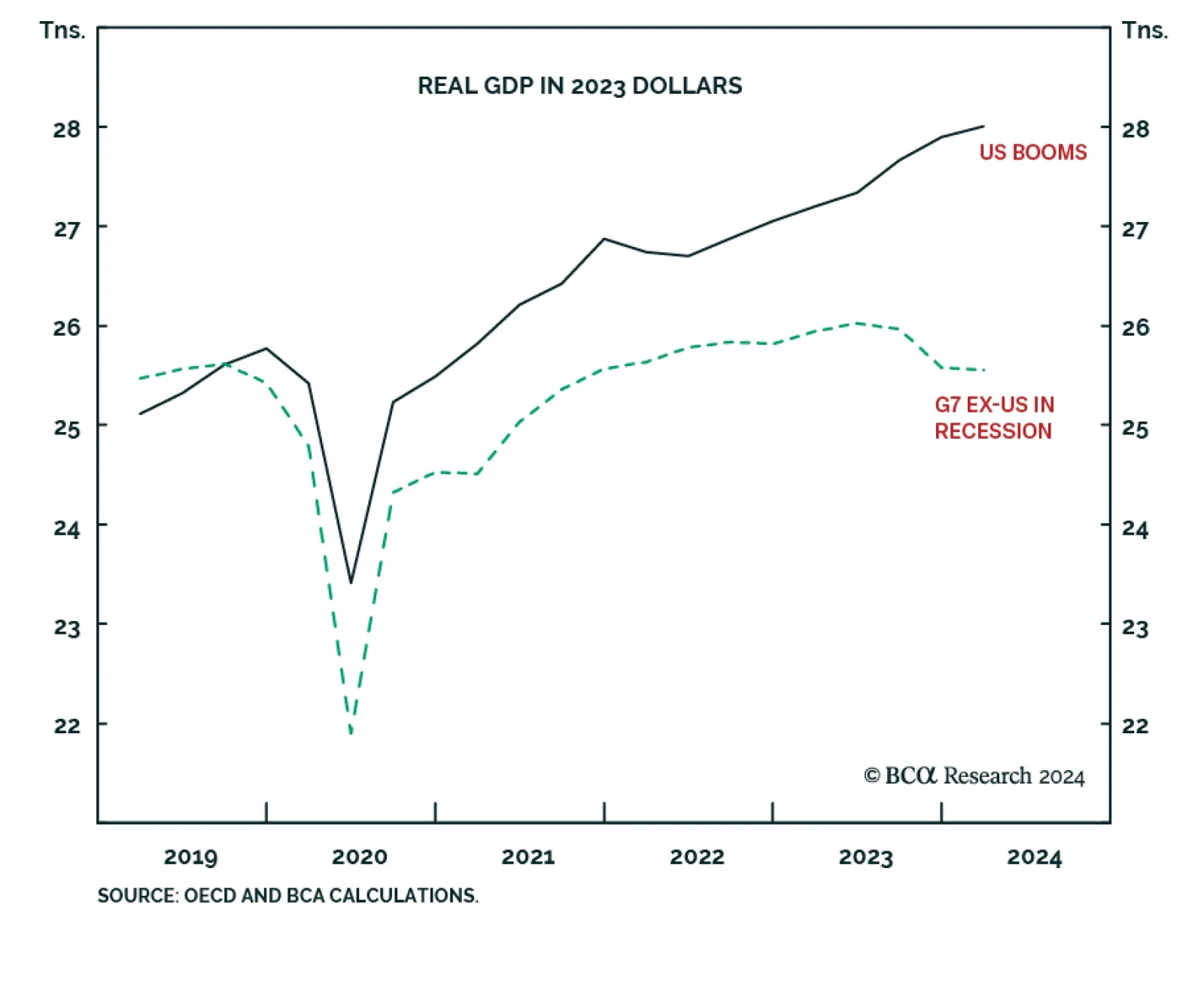

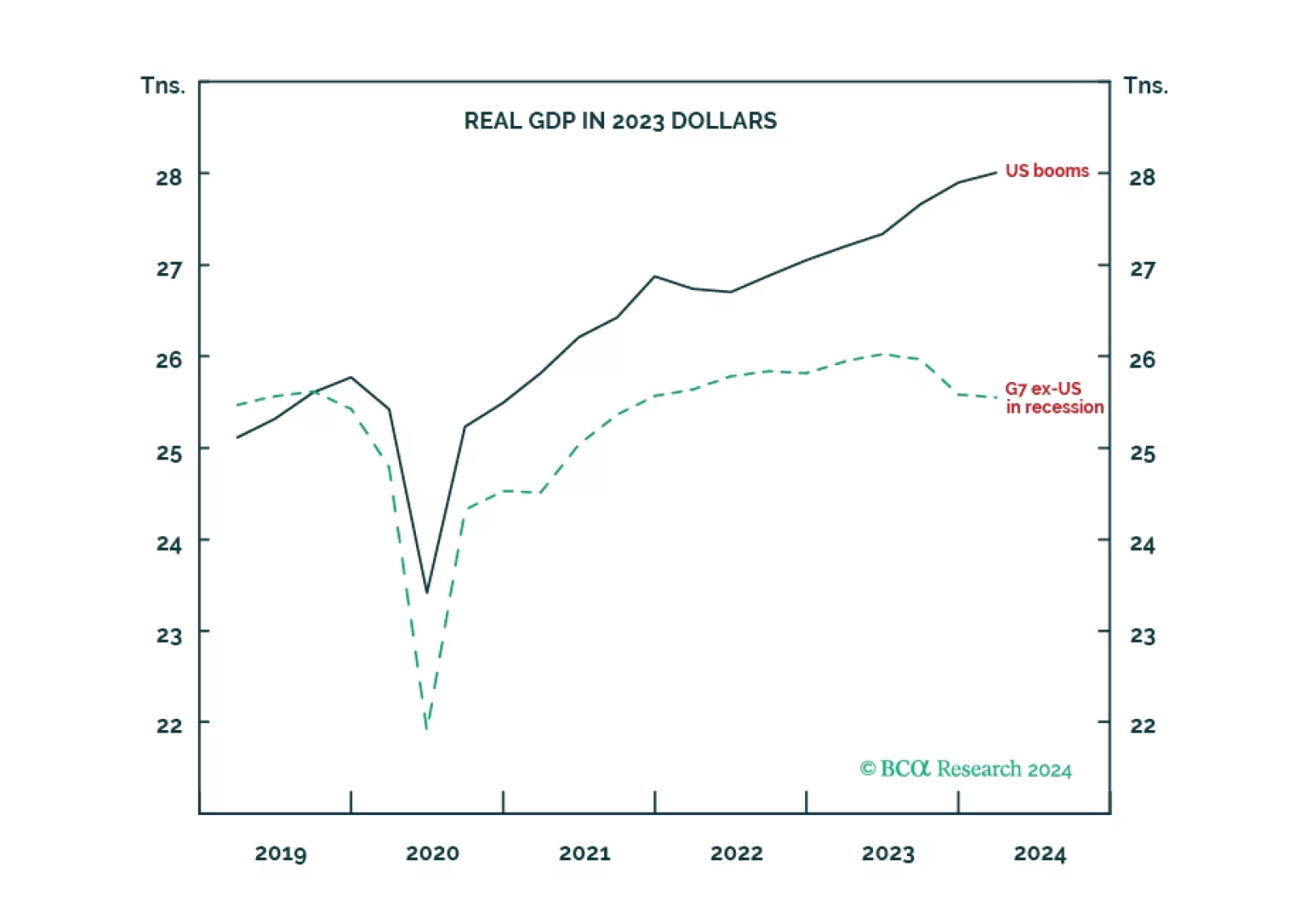

According to BCA Research’s Counterpoint service, the non-US developed economy is “demand-constrained” whereas the US economy is “supply-constrained”. This schism will continue but in reverse. The team has highlighted that following the surge in…

Minutes from the April 30 - May 1 FOMC meeting struck a hawkish tone on the latest discussions among Fed officials. Notably, the reference to “Various participants mention[ing] a willingness to tighten policy further should risks to inflation materialize in a…

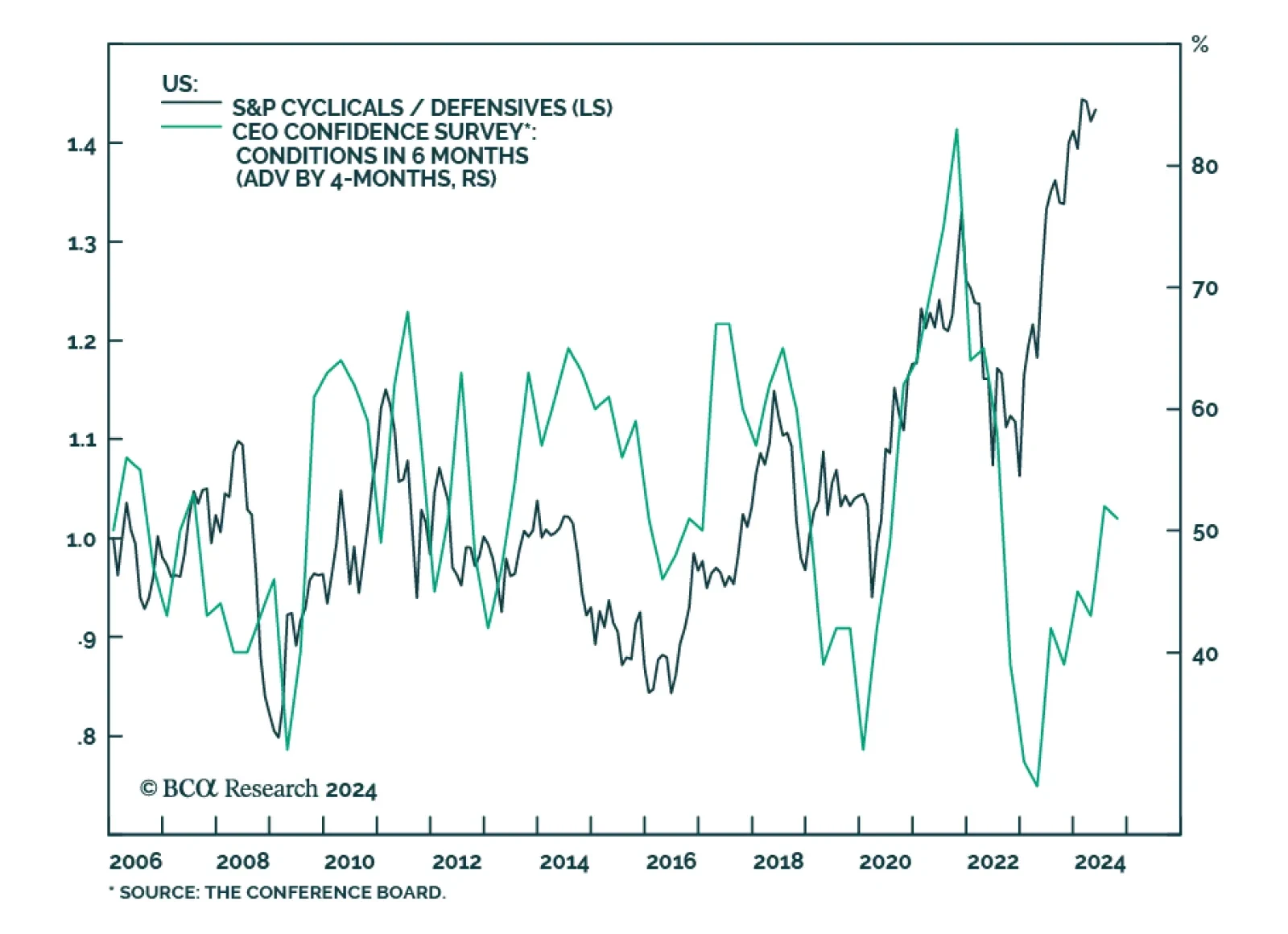

The Conference Board measure of CEO Confidence improved slightly in Q2, from 53 to 54. A reading above 50 indicates that optimistic perceptions of business conditions outweigh pessimistic assessments. The Q2 survey result marks a second consecutive quarter of…

In this Insight, we revisit our "higher for longer" theme for the Reserve Bank of New Zealand, in light of the latest central bank meeting. In conclusion, we are inching towards a more dovish RBNZ ahead. Ergo, we recommend some fixed income and currency trades.

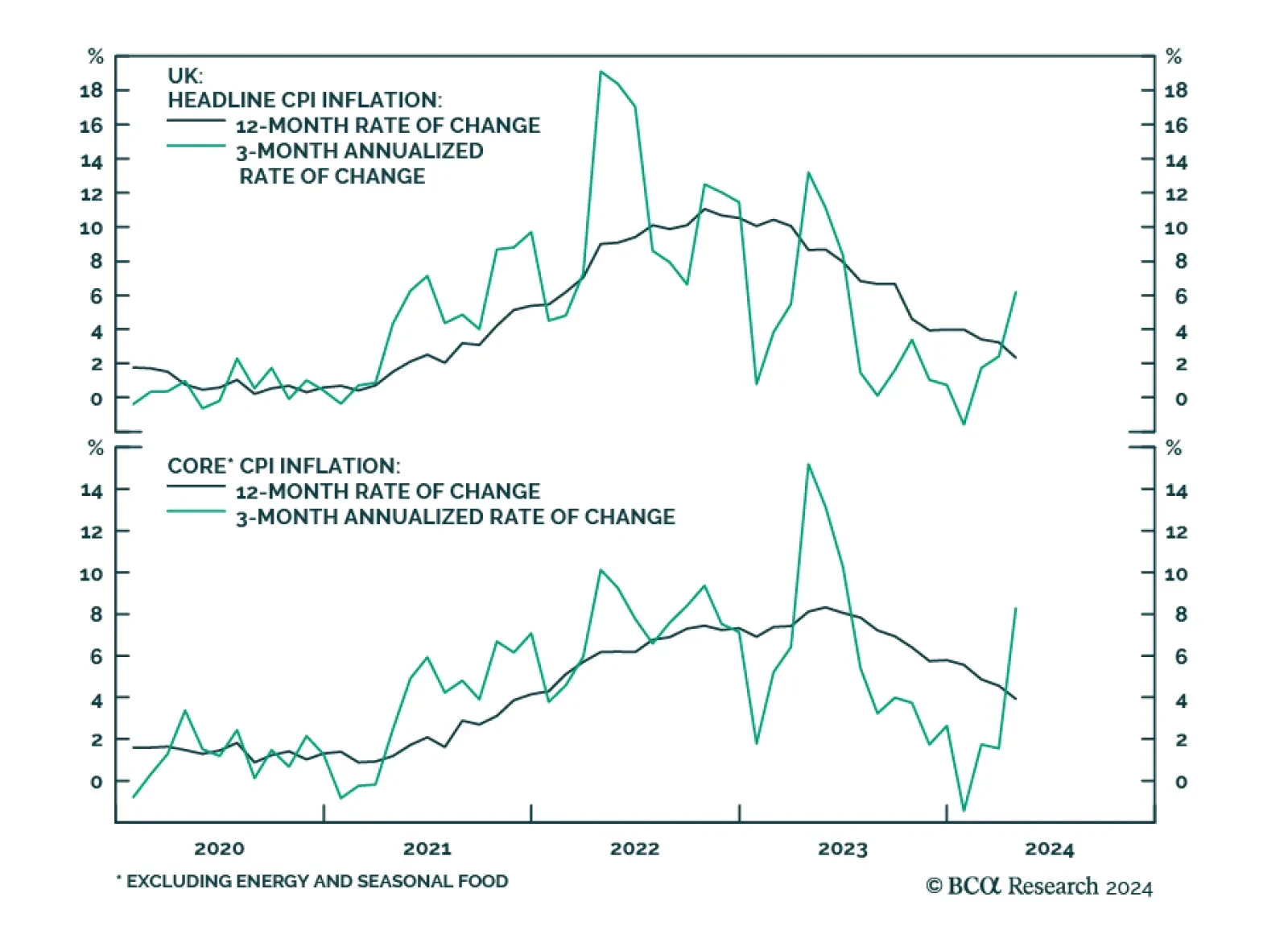

The UK CPI release surprised markets to the upside across the board on Wednesday. Headline CPI increased 2.3% year-on-year, above expectations of 2.1%. Core surprised to the upside as well, moderating from 4.2% to 3.9%y/y, less than the moderation embedded in…

We do not subscribe to the Goldilocks scenario in which price pressures continue to ease while economic growth remains robust. We expect that softening labor demand will eventually hinder consumption as wage and payrolls growth slows, at the same time that…

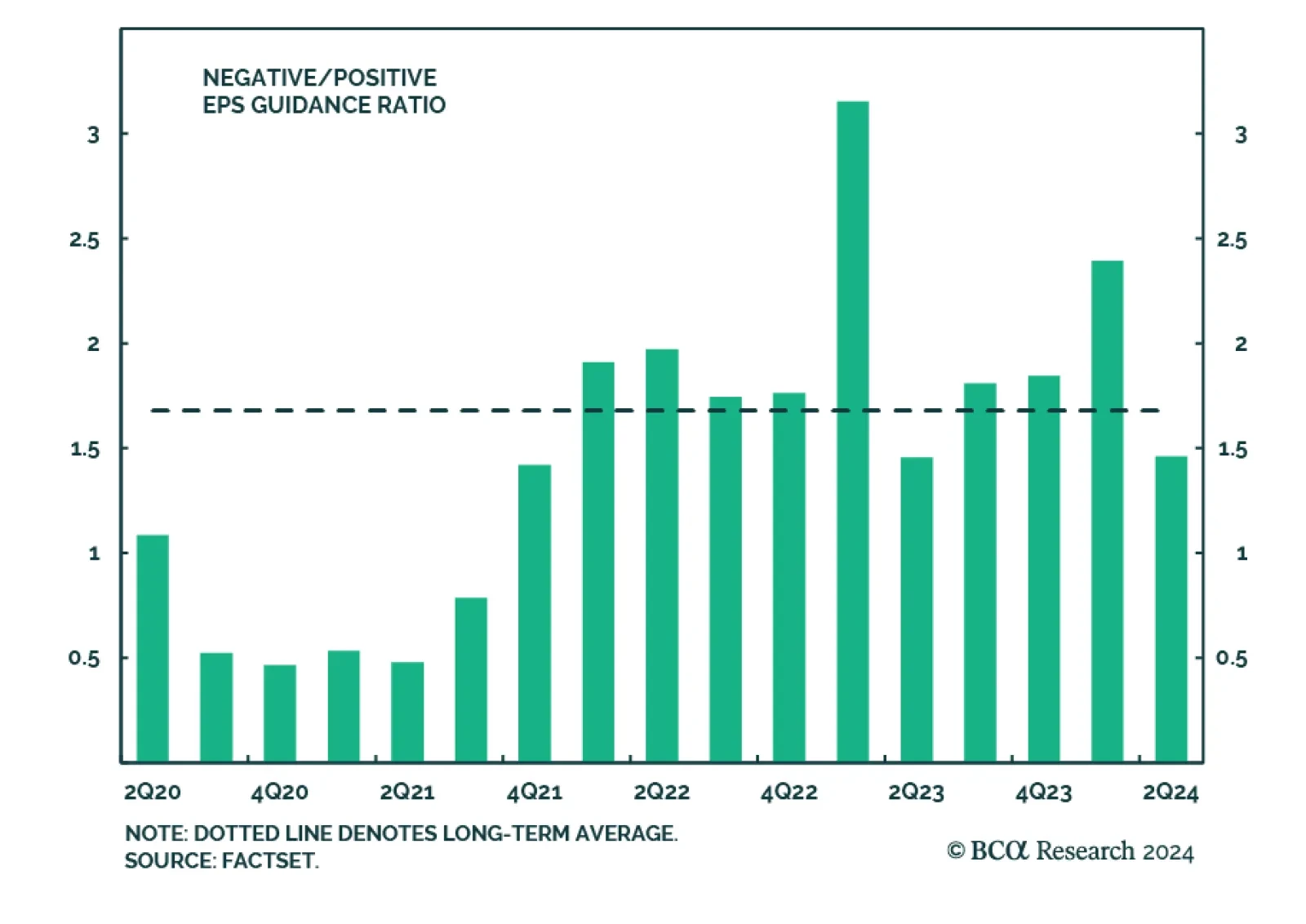

The Q1 2024 earnings season is drawing to a close with 93% of S&P 500 companies having reported results as we go to press. Three-quarters (two-thirds) of companies have topped earnings (sales) expectations in Q1, according to Factset. Next quarter’s…

The economic schism in the world economy, between the non-US developed economy in recession and the US in strong growth, is unprecedented during our lifetimes. Now the schism will continue in reverse, as the non-US developed economy rebounds while the US fades. There are important implications for rates, the dollar, and sector and regional equity allocation which we discuss. Plus: base metals are a tactical short.

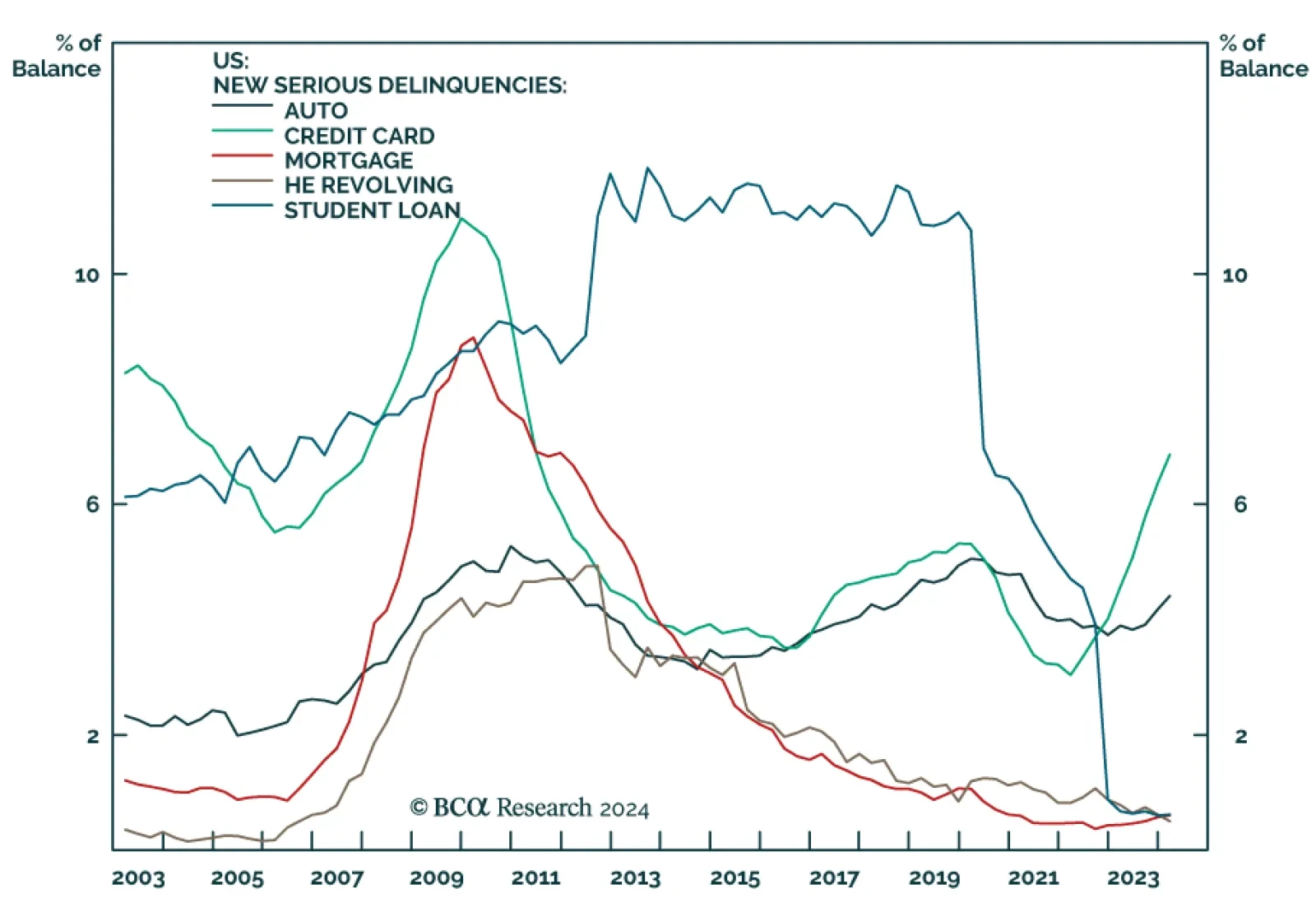

The New York Fed Quarterly Report on Household Debt and Credit indicates that US household debt rose 1.1% q/q in Q1 to $17.7 trillion. Higher mortgage, home equity loan and auto loan balances drove the bulk of the Q1 increase, while credit card balances…