Developed Countries

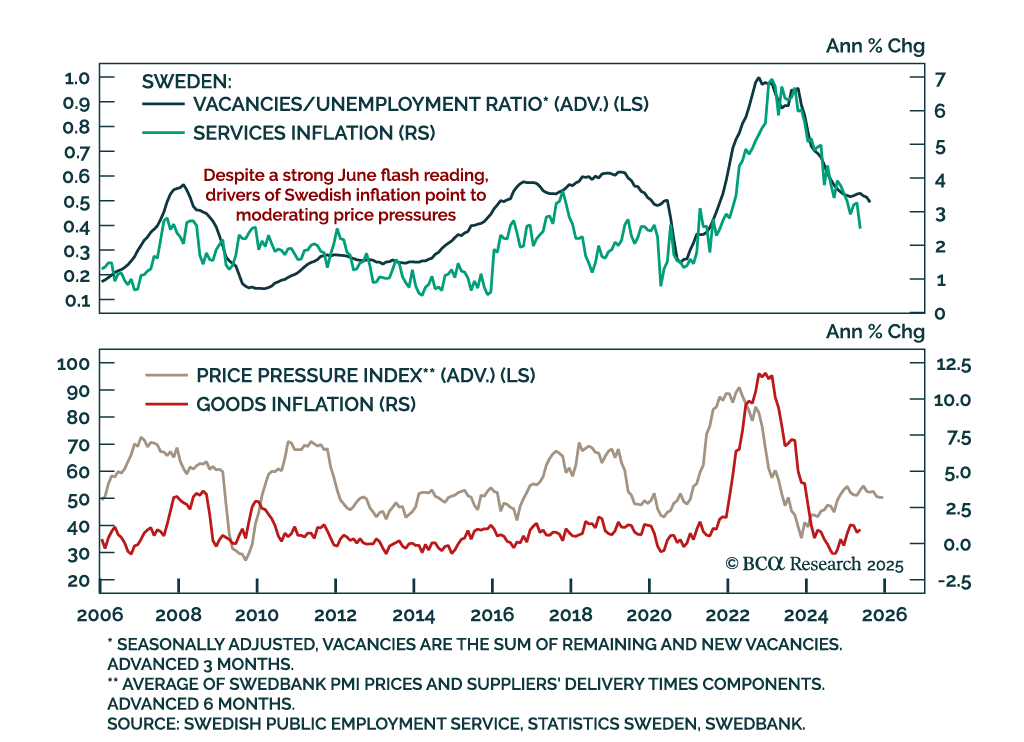

Stronger-than-expected June inflation will likely keep the Riksbank on hold in August, despite soft underlying trends. Headline inflation accelerated more than expected to 0.5% m/m (0.8% y/y), while CPI ex-housing rose to 2.9% y/y and core inflation to 3.3%…

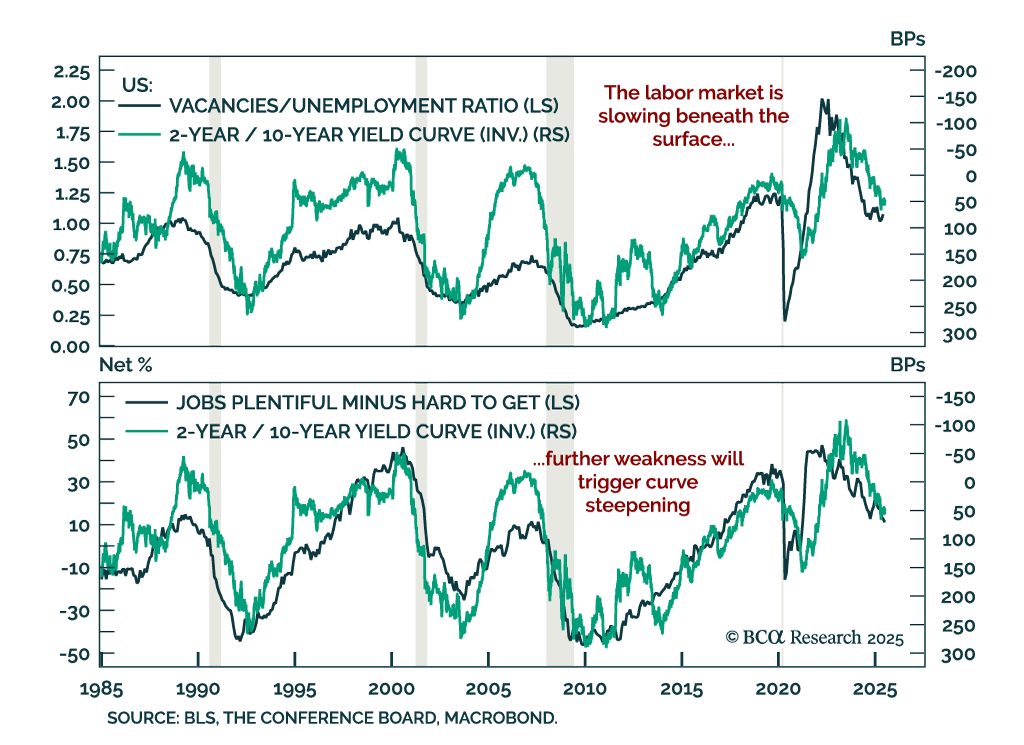

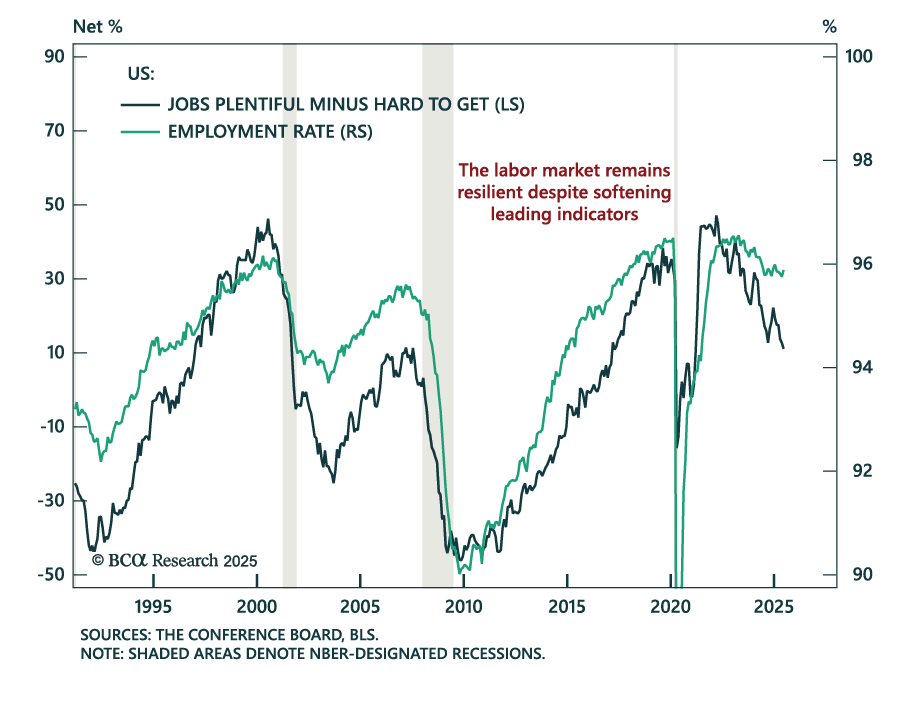

Labor market cracks reinforce long duration and steepener positioning as growth risks mount. Job market data has looked strong on the surface, but the details of the June employment and JOLTS reports confirm a slowing trend within the “low hiring, low firing”…

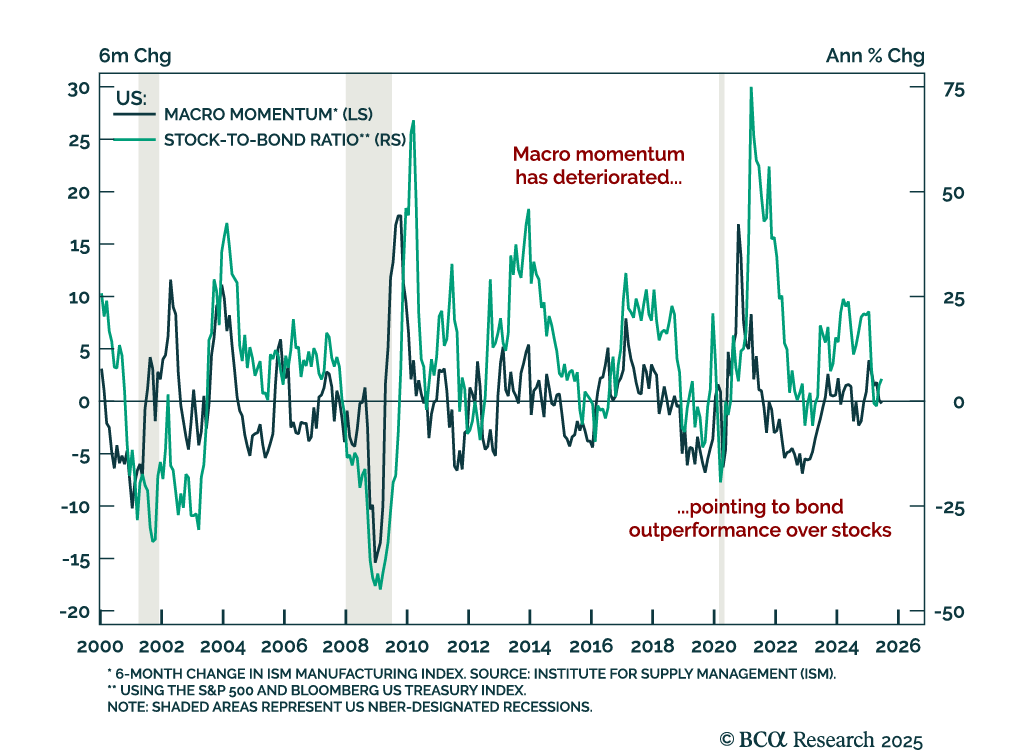

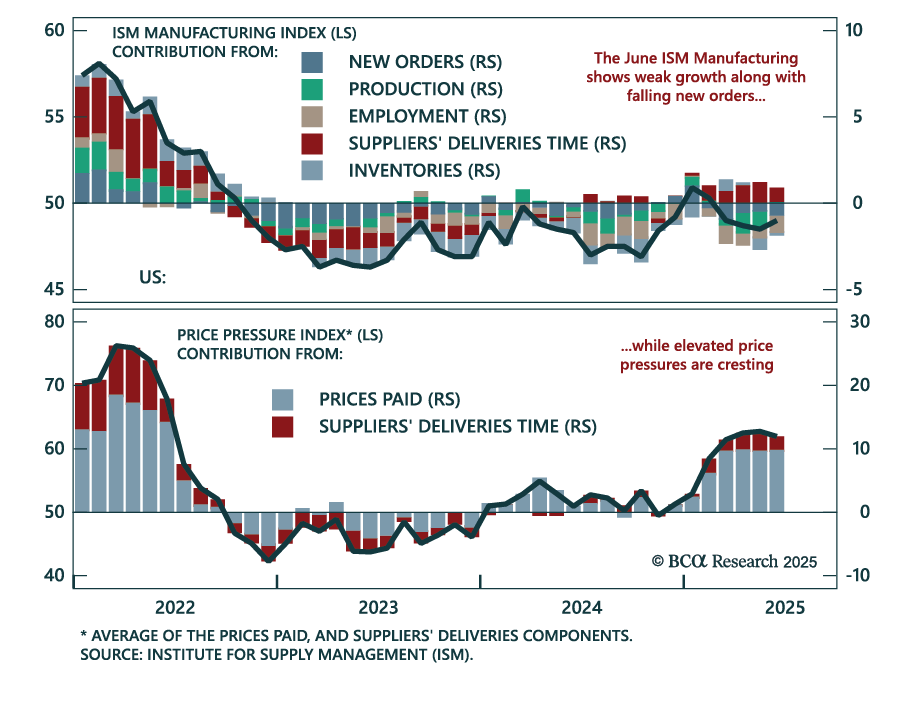

Deteriorating macro momentum supports a defensive asset allocation stance as hard data deteriorates. Last week’s ISM Manufacturing and Services PMIs confirmed that growth is slowing and price pressures are easing from a high level. The ISM Manufacturing index…

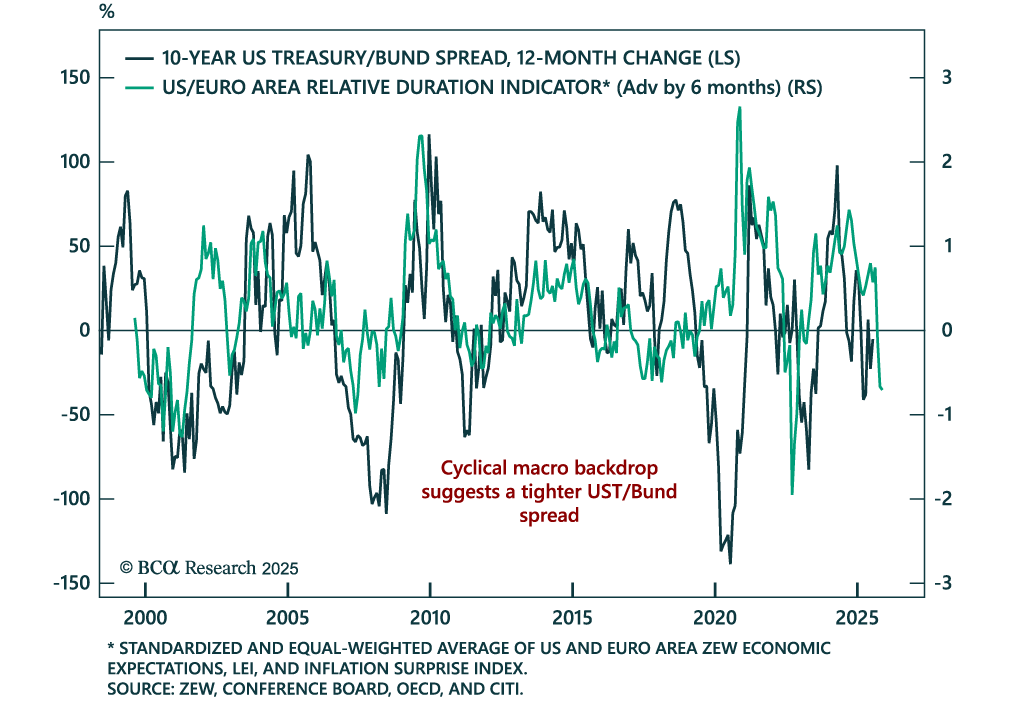

Relative growth and inflation trends point to a narrower UST/Bund spread. Our Chart Of The Week comes from Robert Timper, Global Fixed Income Strategist. This week, our rates strategists introduced a new US/Euro Area Relative Duration Indicator, designed to…

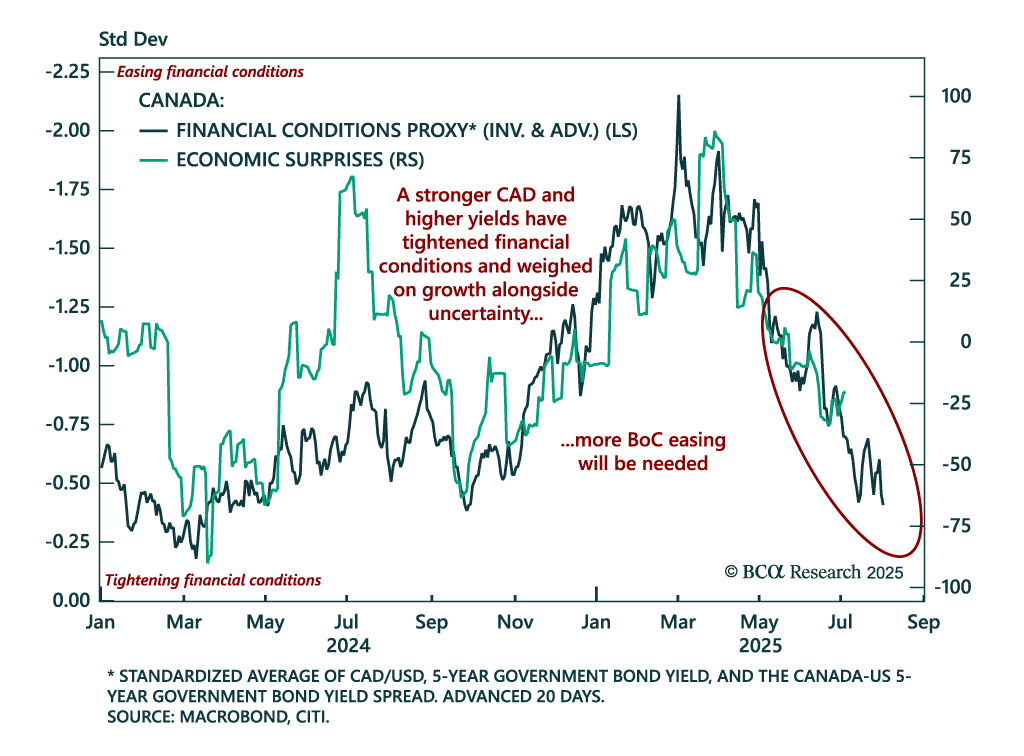

Canada’s stronger currency and tightening financial conditions point to further BoC easing and support long Canadian bond positions. The CAD has appreciated this year alongside the global push to diversify away from USD assets, which has weakened the US…

Stronger-than-expected June payrolls rule out a July Fed cut, but the report does not derail the case for long duration and curve steepeners. Nonfarm payrolls printed at 147k, with the two prior months revised up by 16k, leaving the 3-month average at 150k.…

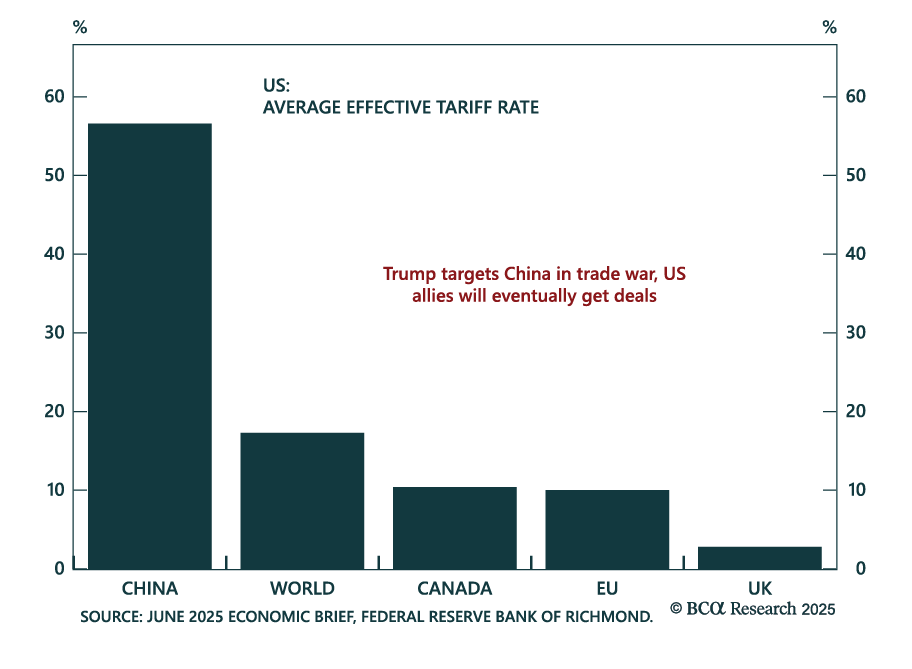

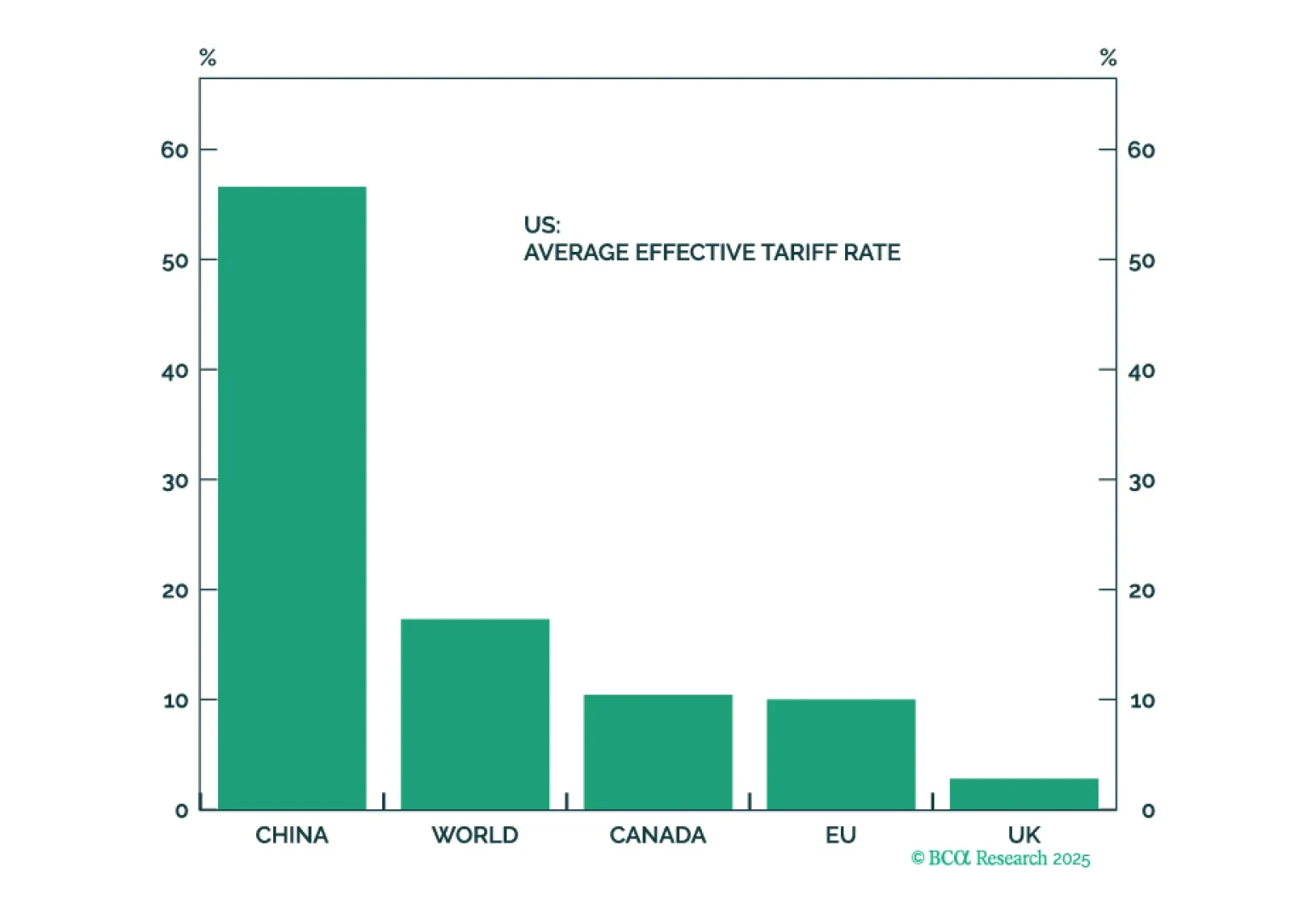

Our Geopolitical strategists warn that structural and cyclical risks remain elevated despite a fading threat of acute shocks, and recommend booking profits ahead of tariffs and weaker data. President Trump is passing his signature legislation and pivoting to…

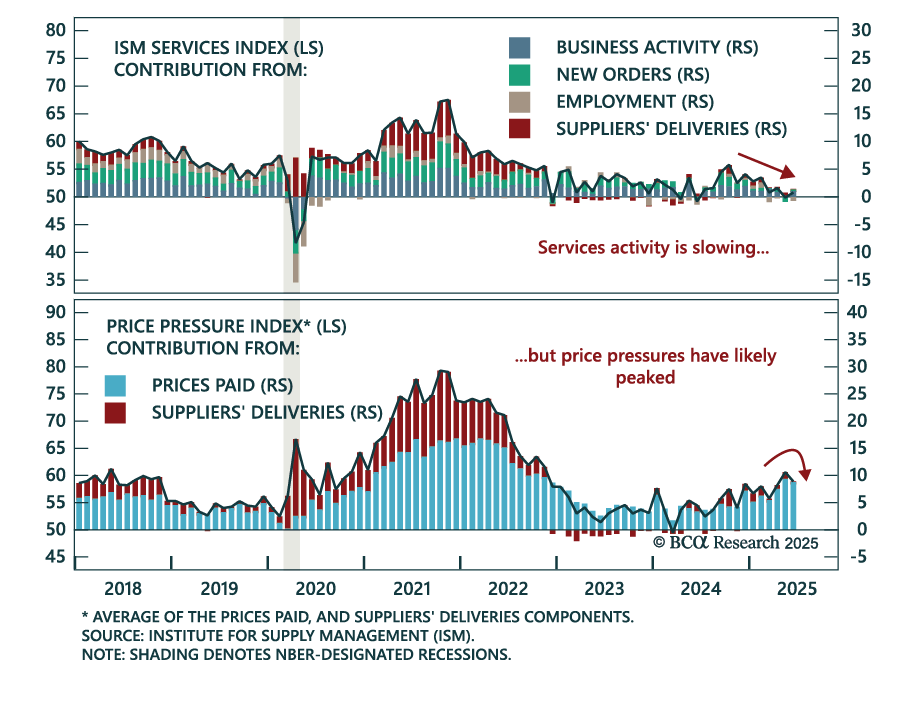

ISM Services data confirm slowing growth and cooling inflation, reinforcing a defensive allocation stance. The index rose slightly to 50.8 in June from 49.9 in May, with new orders rebounding into expansion at 51.3. However, the employment subcomponent…

Acute geopolitical risks, like a massive oil shock, may be abating. But structural geopolitical risk remains high and could upset a blithe market. Cyclical economic risks are underrated as the US slows down and China continues to stumble. Investors should book some profits in anticipation of tariff implementation and a downturn in hard economic data.

The June ISM points to sluggish US manufacturing and reinforces long duration positioning amid peaking price pressures. The index rose modestly to 49.0 from 48.5 in May, with the rebound driven by slightly higher production and slower supplier deliveries due…