Developed Countries

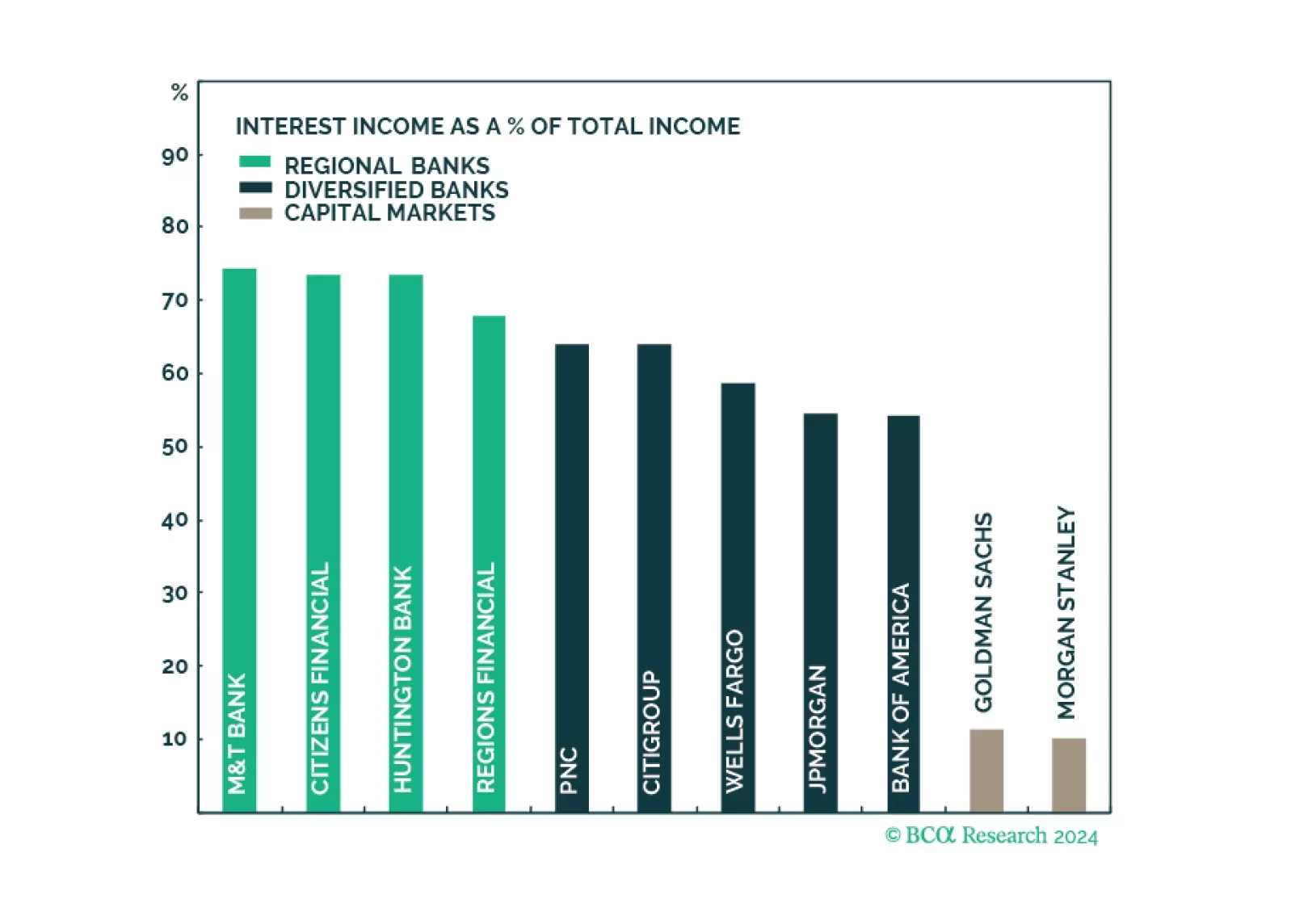

Q1 earnings results of the largest US banks have demonstrated that the engine of recent growth in profitability, NII, has faltered as funding costs are rising fast. However, the resurgence in non-NII thanks to a revival in corporate activity has been a saving grace. Earnings growth appears to have bottomed, while valuations are attractive. To play up portfolio exposure to an upcoming surge in capital markets activity, and minimize exposure to declining profitability in traditional banking services, overweight Diversified Banks and Capital Markets, and underweight Regional Banks.

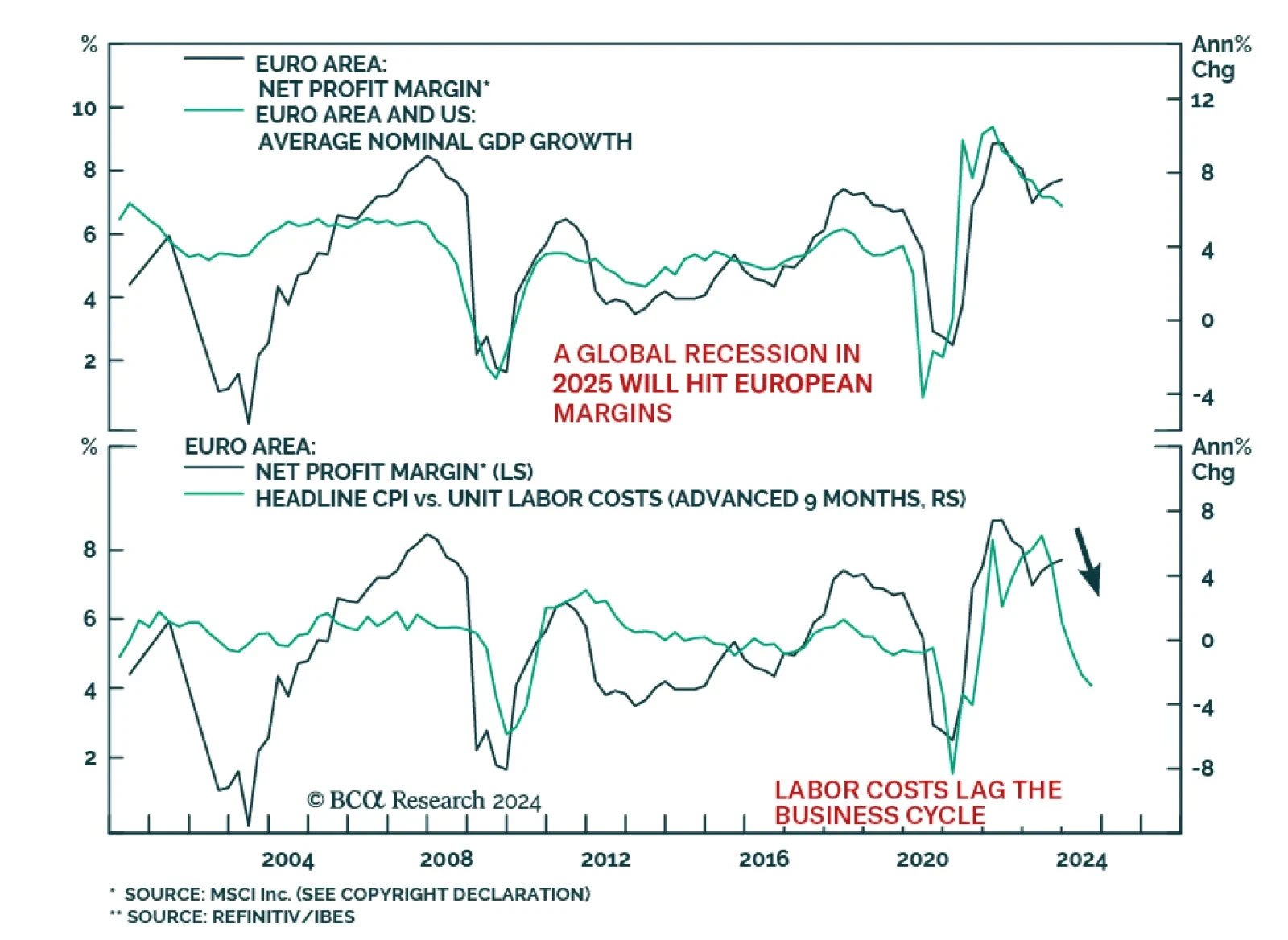

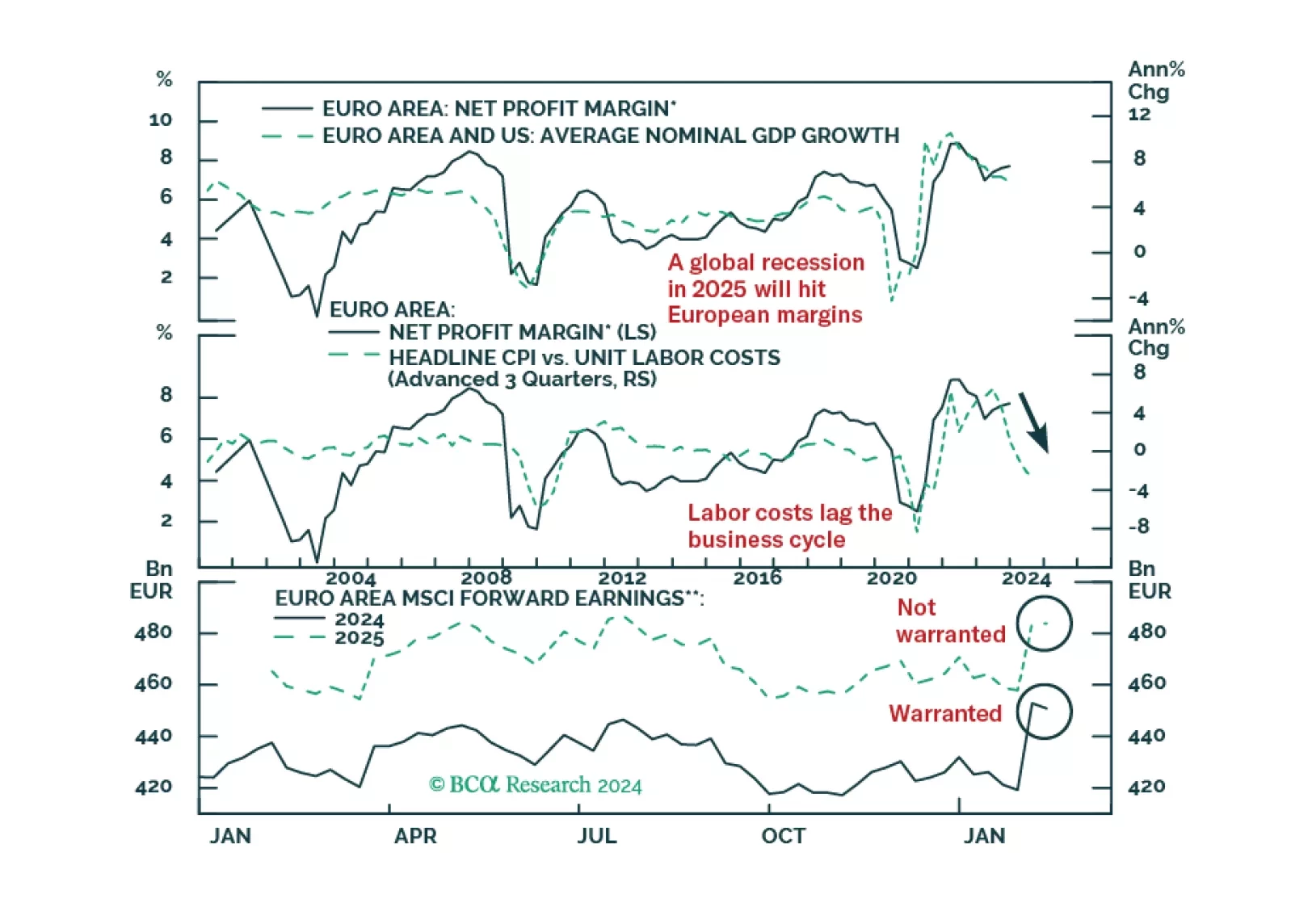

European profits margins are elevated. Will a mild recession be enough to bring them down?

This Special Report introduces a framework for assessing the relative importance of slope change and initial yield in curve trade performance. The yield penalty for curve steepeners has fallen significantly since the beginning of the year, and we recommend shifting out of Treasury curve flatteners and into Treasury curve steepeners in US bond portfolios.