Developed Countries

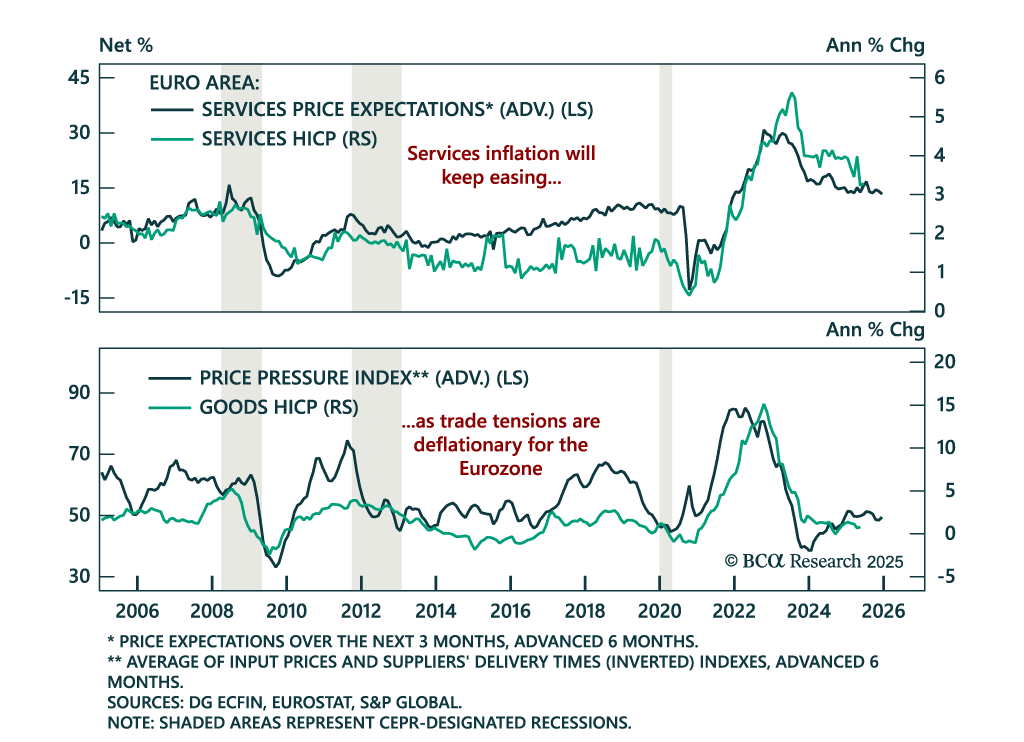

June Eurozone inflation data and soft growth backdrop support further ECB easing and reinforce the case for long European bond exposure. Flash HICP inflation ticked up to 2.0% y/y from 1.9%, while core inflation held steady at 2.3%, both in line with…

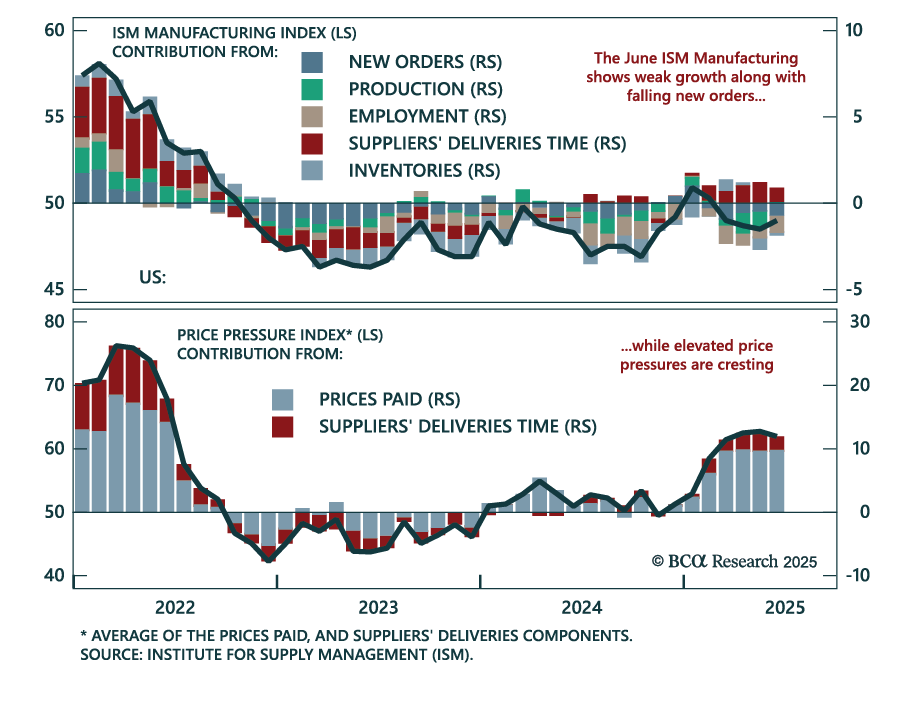

The June ISM points to sluggish US manufacturing and reinforces long duration positioning amid peaking price pressures. The index rose modestly to 49.0 from 48.5 in May, with the rebound driven by slightly higher production and slower supplier deliveries due…

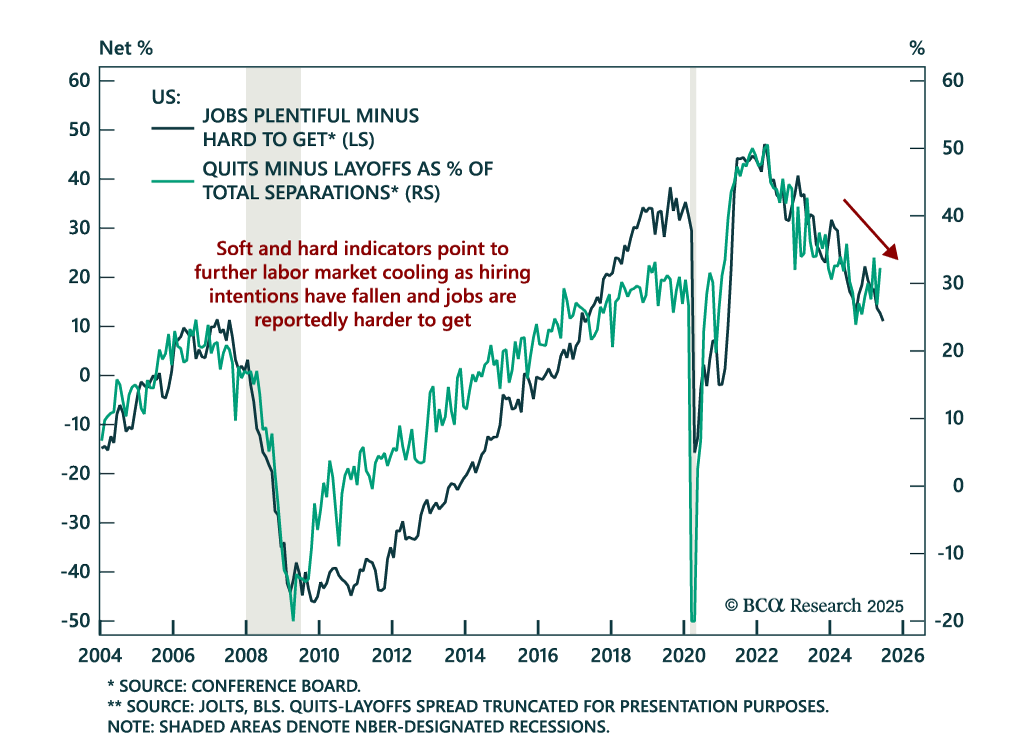

May JOLTS data suggest labor market softening beneath the surface, reinforcing a defensive stance across portfolios. Job openings rose to 7.7m from 7.4m, beating estimates, while quits ticked up to 3.3m and layoffs fell to 1.6m. However, hiring edged lower to…

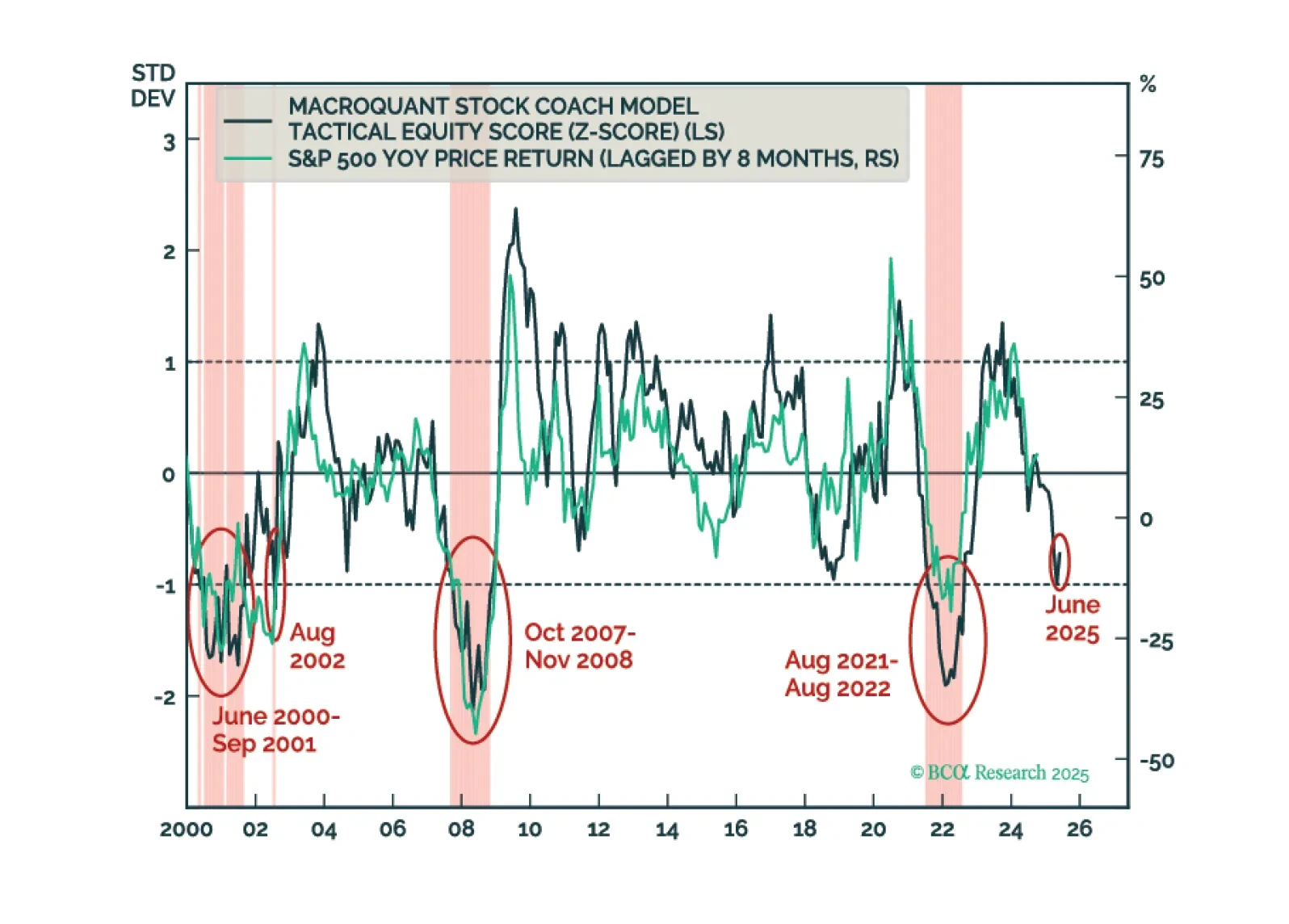

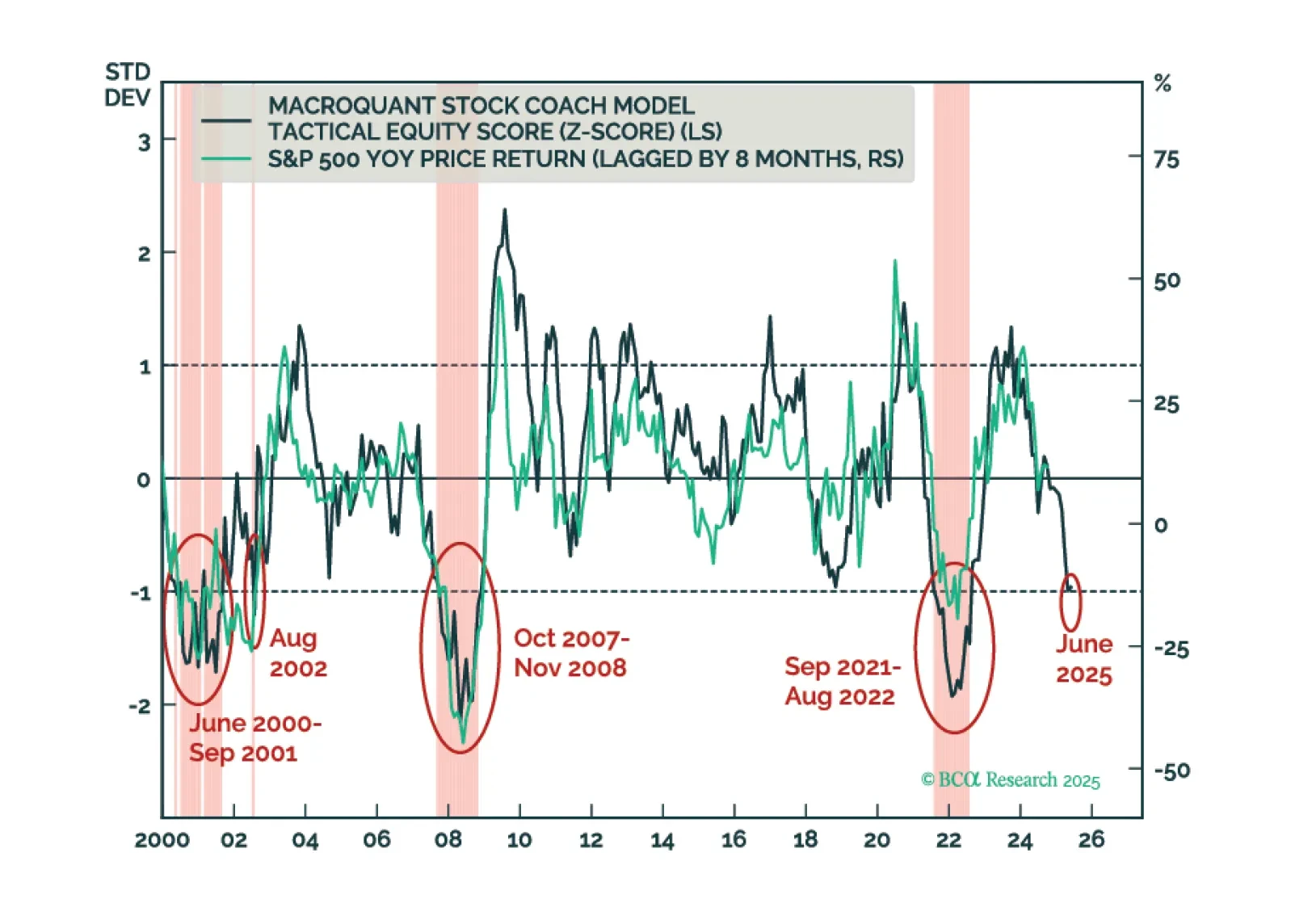

MacroQuant’s US equity z-score is dangerously close to the -1 threshold. Moves below that threshold have reliably coincided with equity bear markets in the past. As such, MacroQuant recommends an underweight on stocks, offset by an overweight on bonds and cash.

Tech-led momentum is driving the S&P 500 to new highs despite weak growth and rising cyclical risks. The rally has accelerated following a de-escalation in geopolitical tensions and ongoing hopes for positive trade developments. Momentum signals confirm…

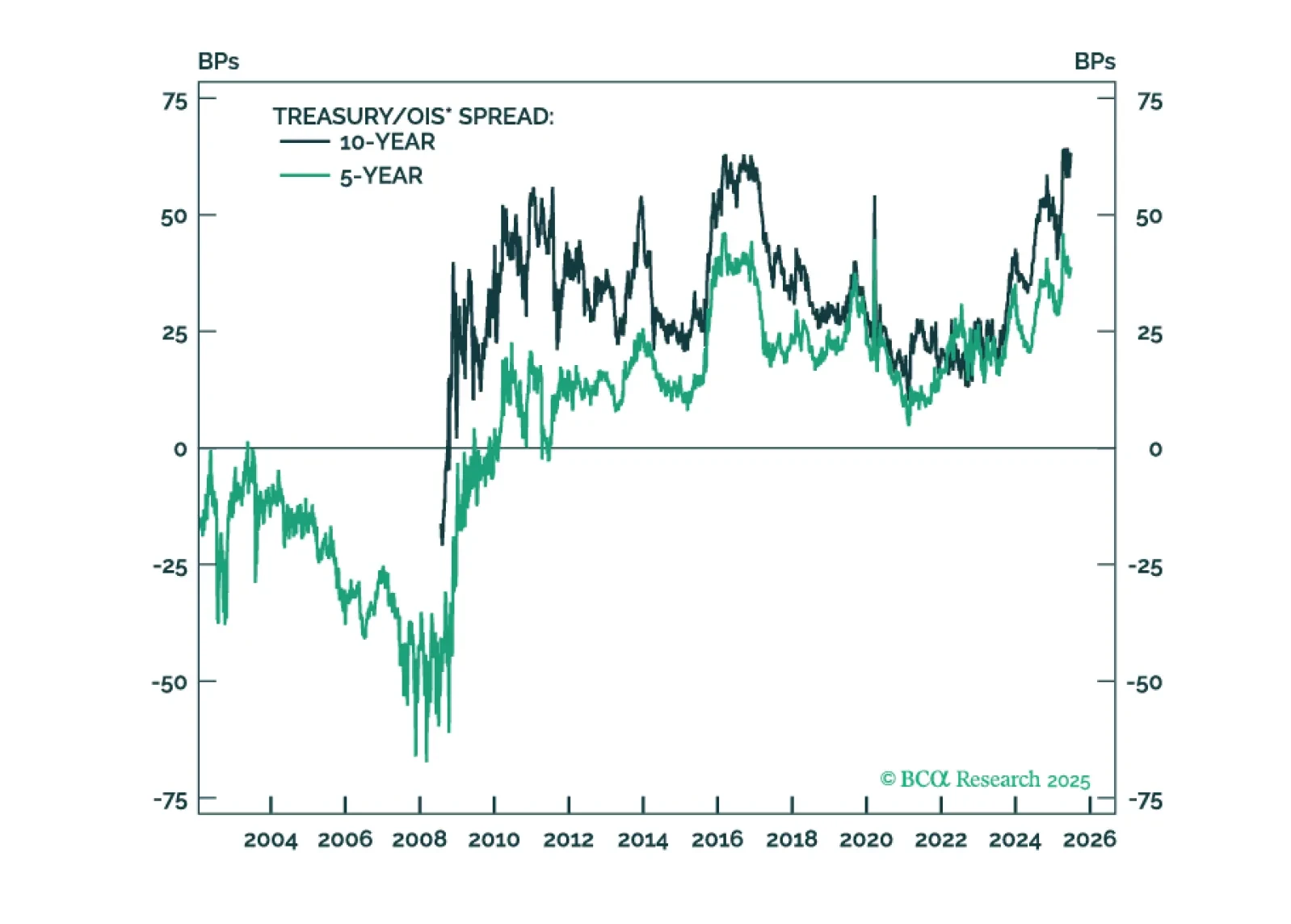

Our US Bond strategists expect a modest narrowing of the Treasury/OIS spread, supporting a cyclical long-duration stance and 2s10s steepeners. Over the past year, the spread has added roughly 30 bps to the 10-year Treasury yield, driven by factors such as…

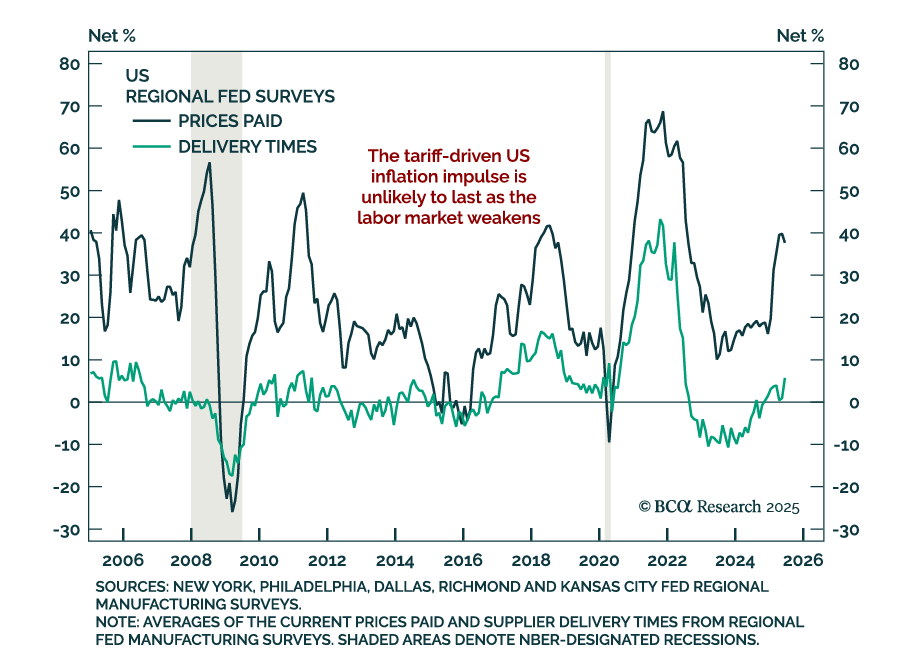

Regional Fed surveys confirm sluggish US manufacturing and tame inflation, supporting long duration positioning outside the US. The June Dallas Fed Manufacturing survey missed expectations, rising to -12.7 from -15.3, still deep in contraction. New orders…

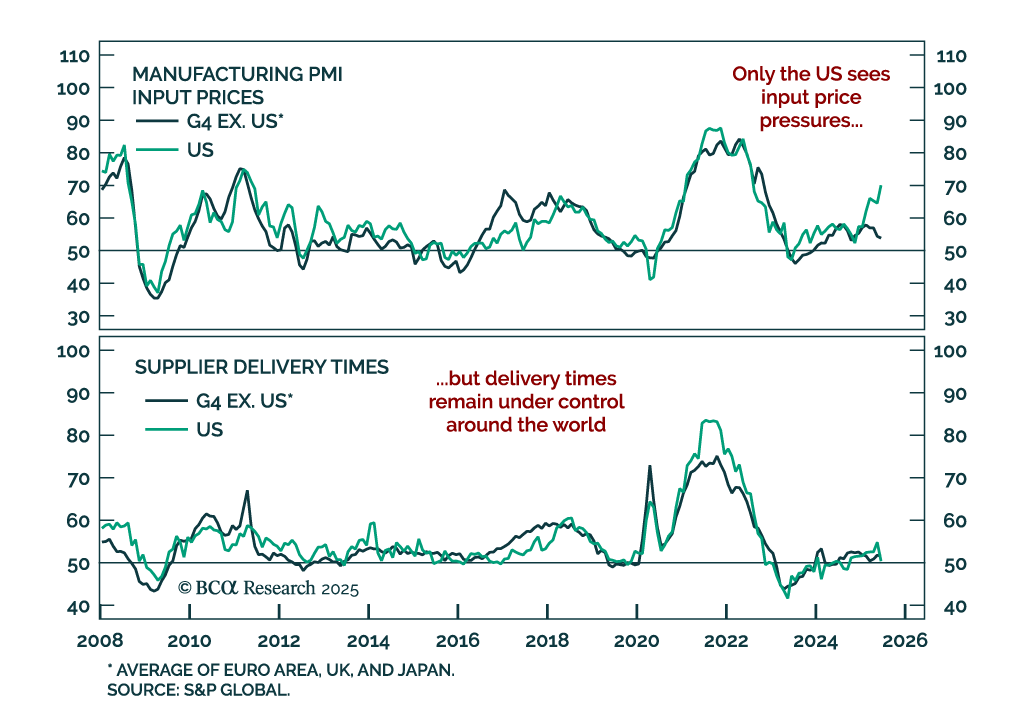

Global inflation risks remain subdued, reinforcing a long duration stance across select DM government bonds. Our price pressure index shows moderate input price inflation outside the US and stable delivery times globally. Inflation blends…

The Treasury/OIS spread has exerted notable upward pressure on Treasury yields during the past year, but the factors driving the spread are now turning more favorable.

Investors should modestly underweight equities in their portfolios and look to turn more aggressively defensive once the whites of the recession’s eyes are visible. We think that will happen within the next few months.