Developed Countries

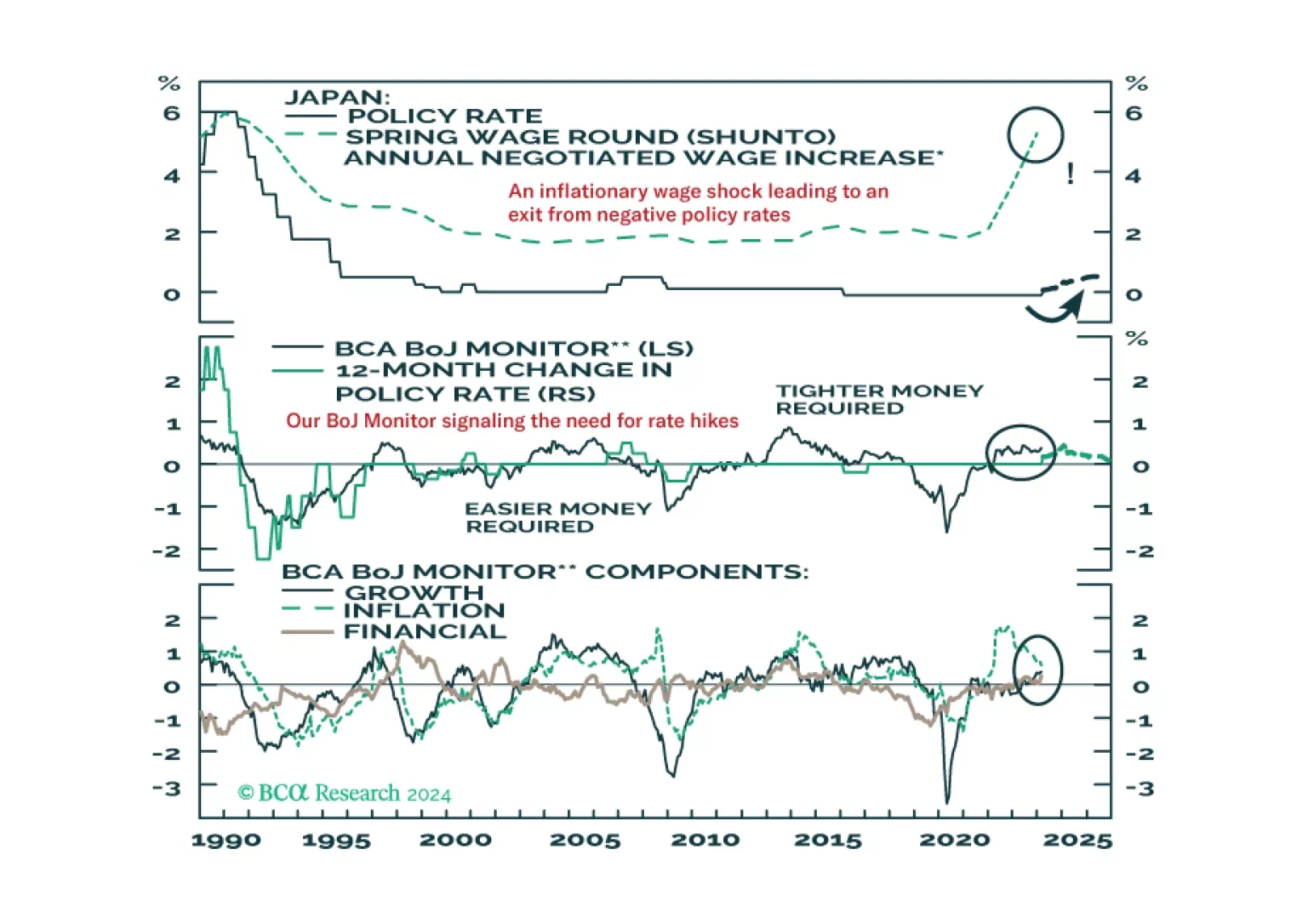

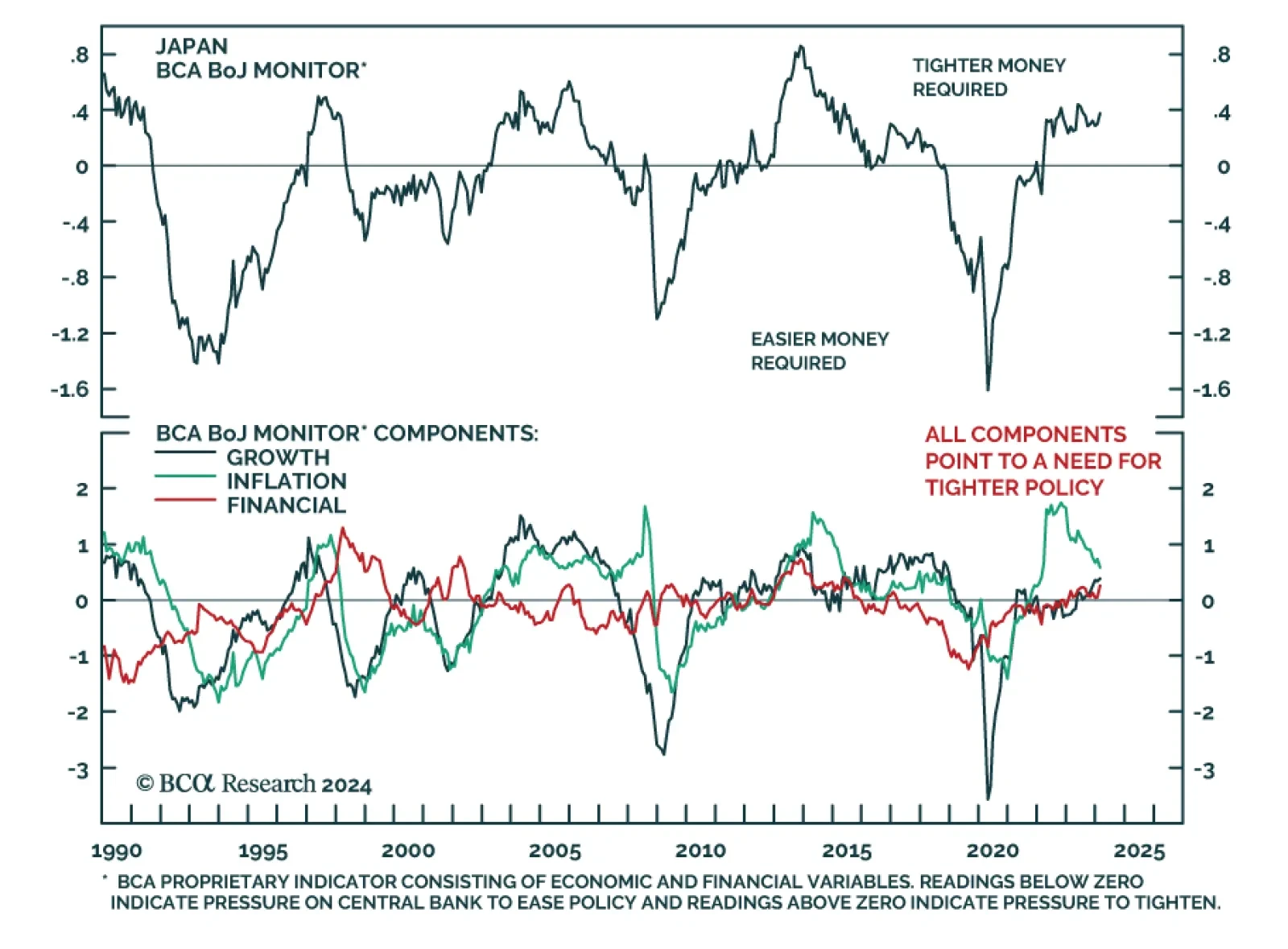

The Bank of Japan delivered a historic policy adjustment this week, ending both negative interest rates and Yield Curve Control. In this Insight, BCA’s global fixed income and currency strategists discuss the immediate implications of the move for Japanese bond yields and the yen, and the potential for additional tightening actions.

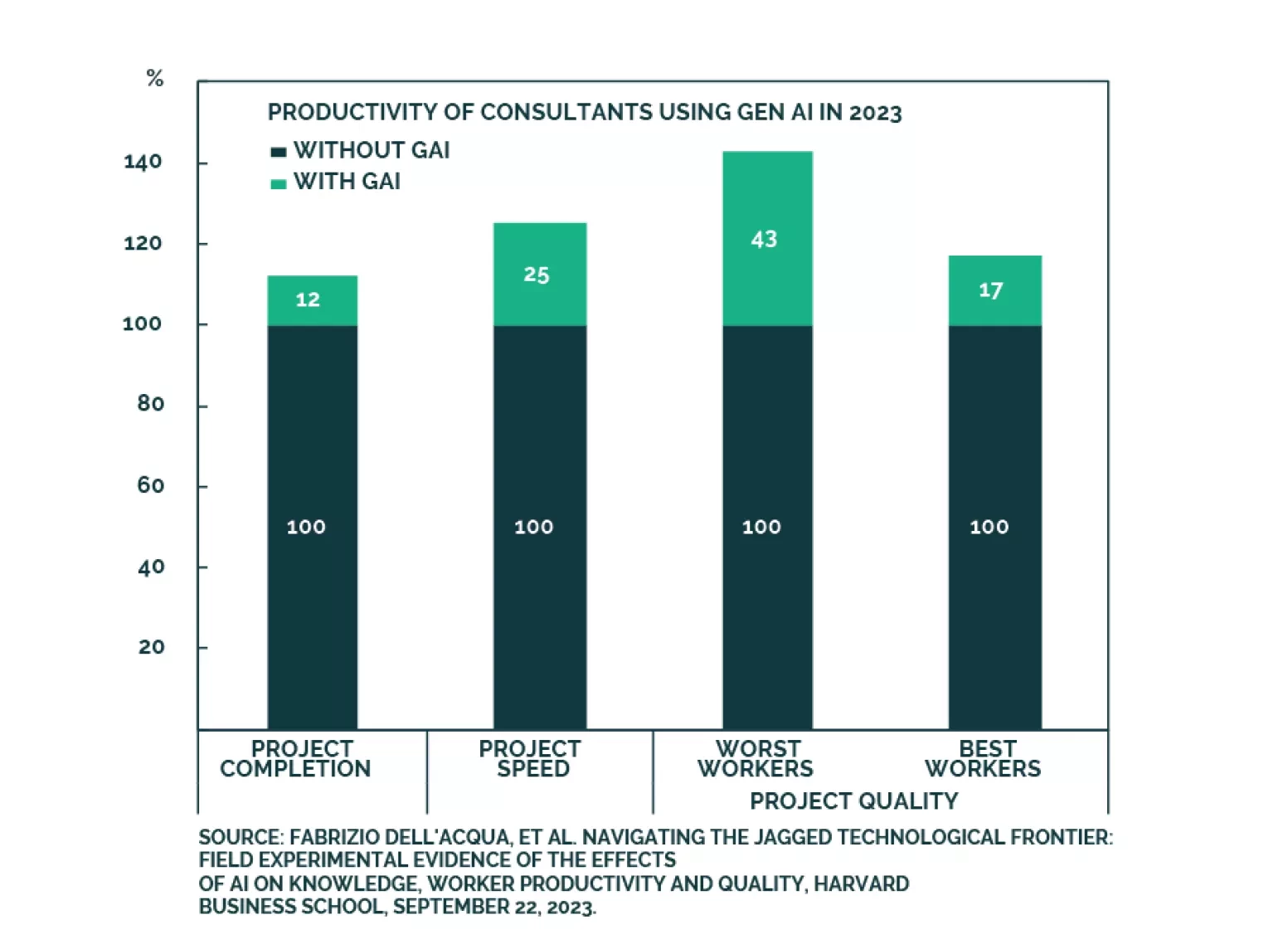

GAI technology has made tremendous gains over the past year. It has advanced from being a mere “curiosity” to becoming an everyday helper. While the promise of GAI is enormous, its effects are still limited: Companies are still struggling with monetization while productivity improvement is still at least a year away. In terms of evolution, the focus is shifting away from “picks and shovels” infrastructure companies toward model and application developers.

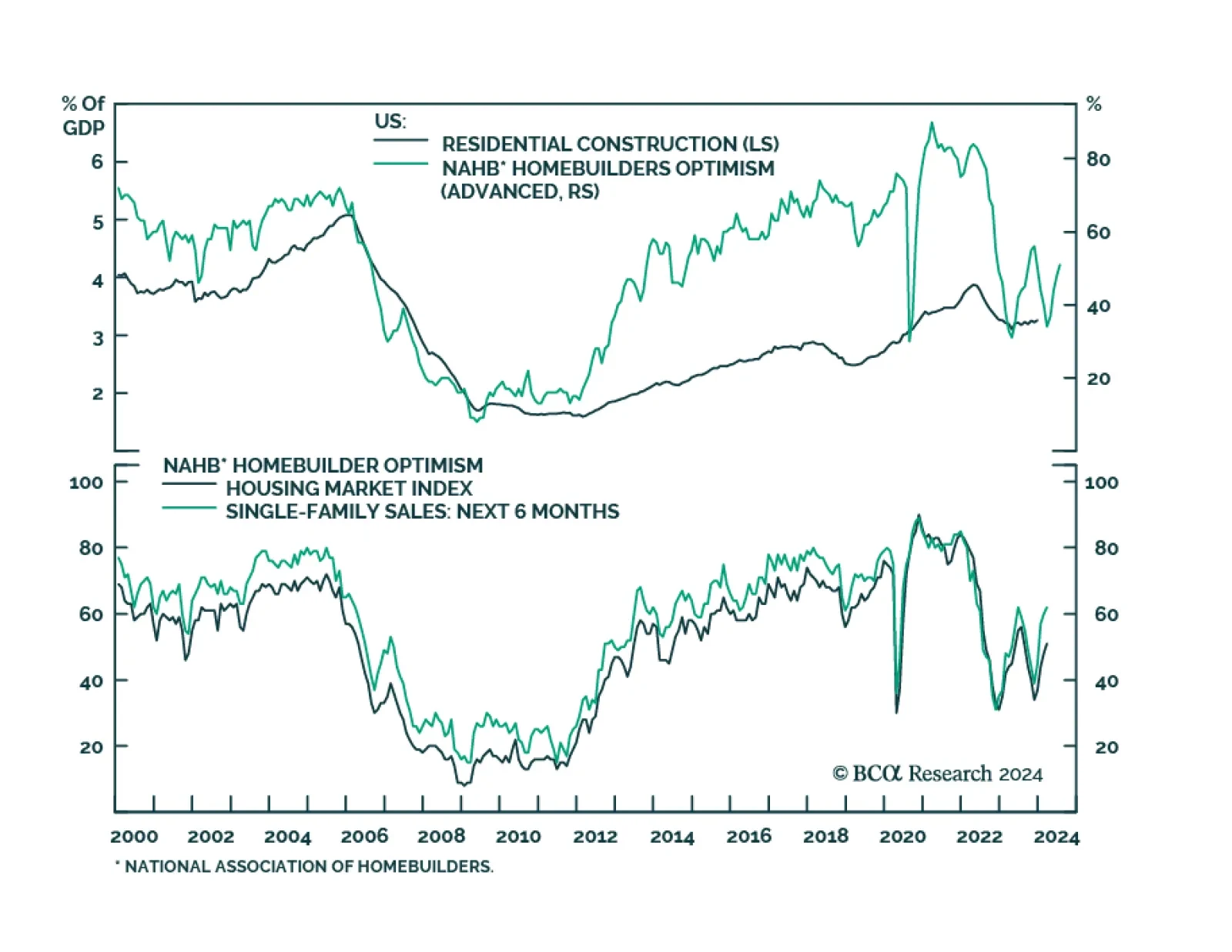

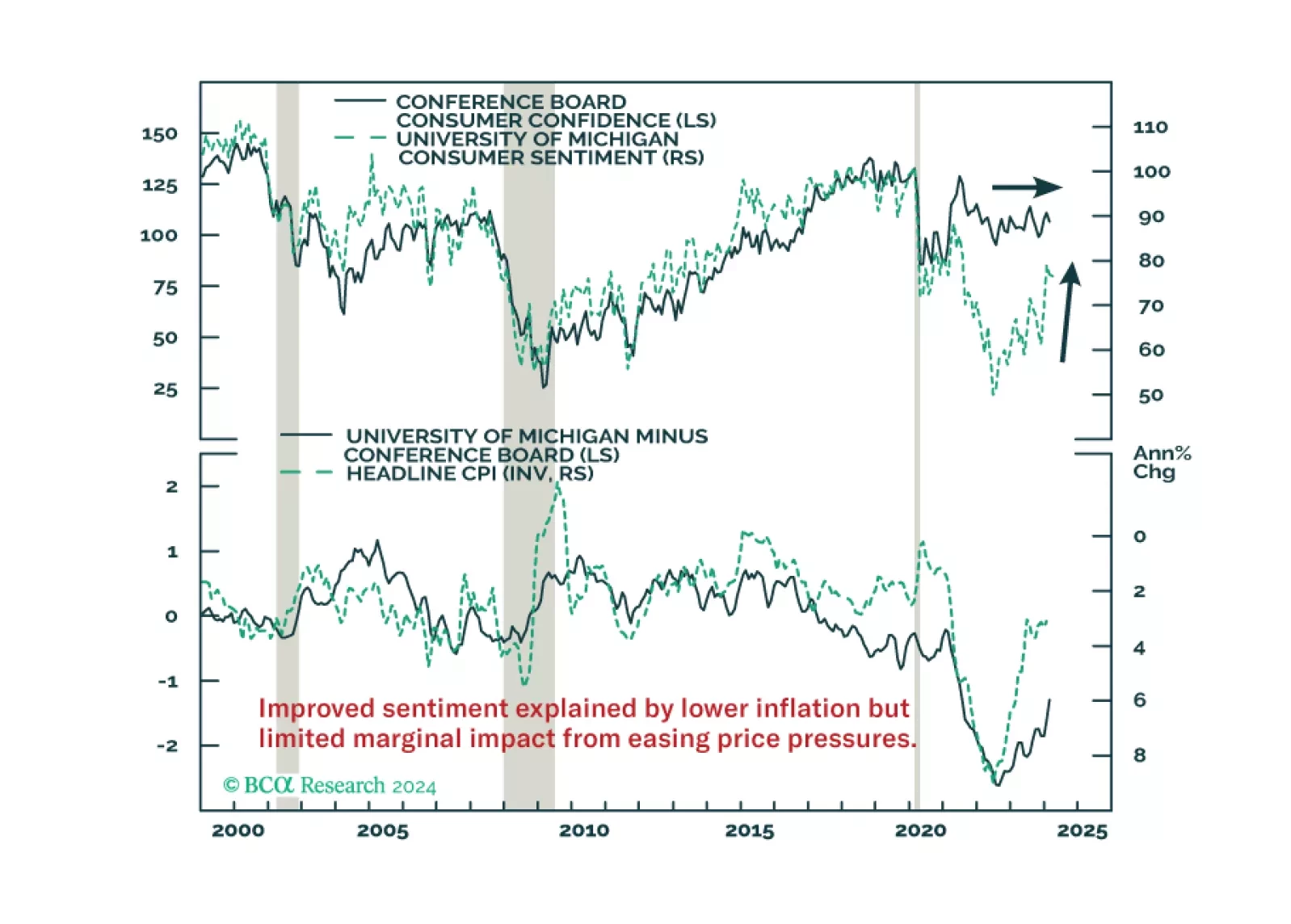

Improved consumer morale will not compensate for the fading tailwinds to consumption. Neither will the wealth effects from higher stocks and home prices.