Developed Countries

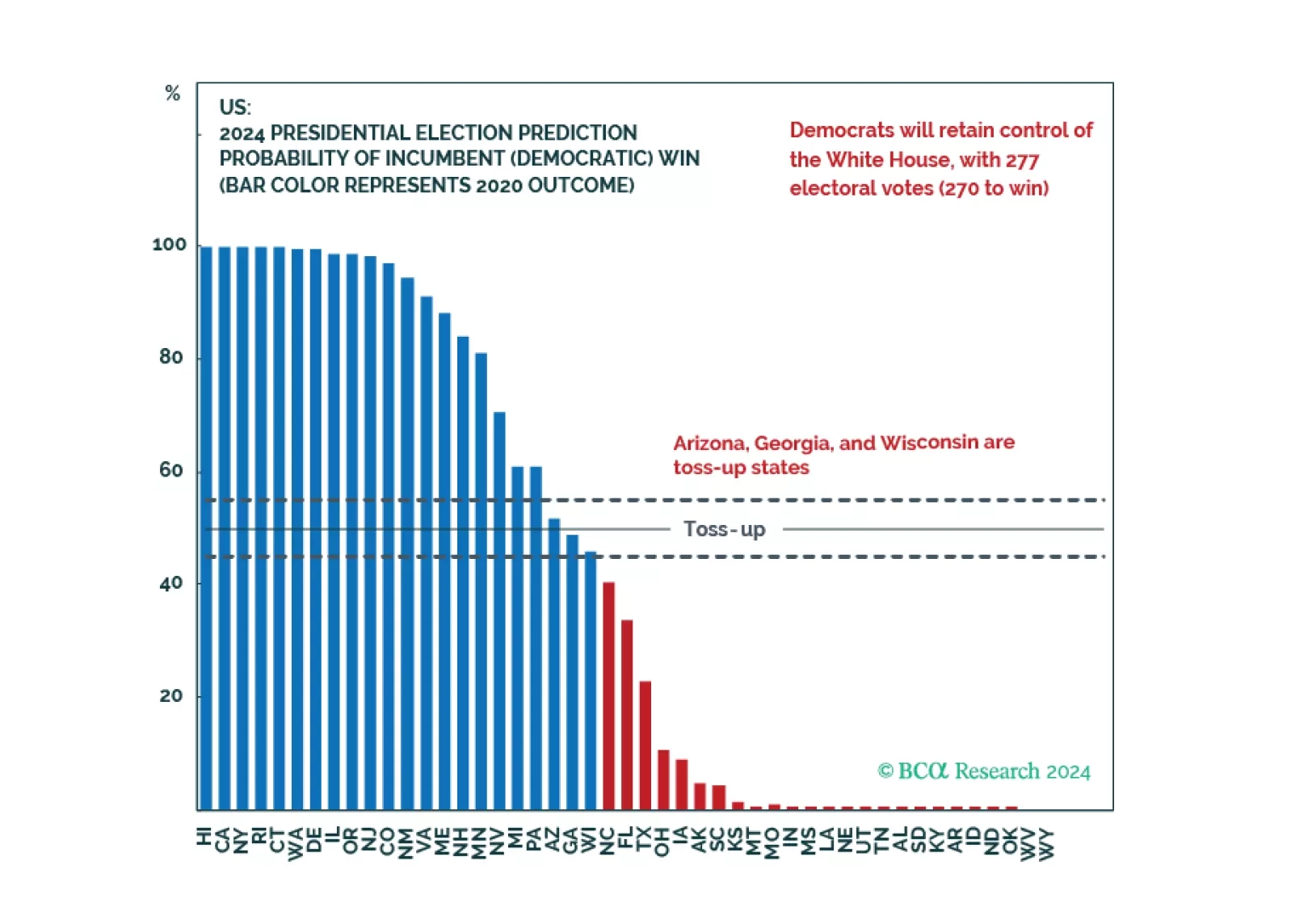

Though there are some positive signals recently for the Democrats, it is still hard for them to close the gap and turn things around. The Republicans are still favored to win the Senate as well as the House in the upcoming election.

The first in a series of Strategy Insights where we present a checklist for extending duration in each major government bond market. This first entry focuses on the US.

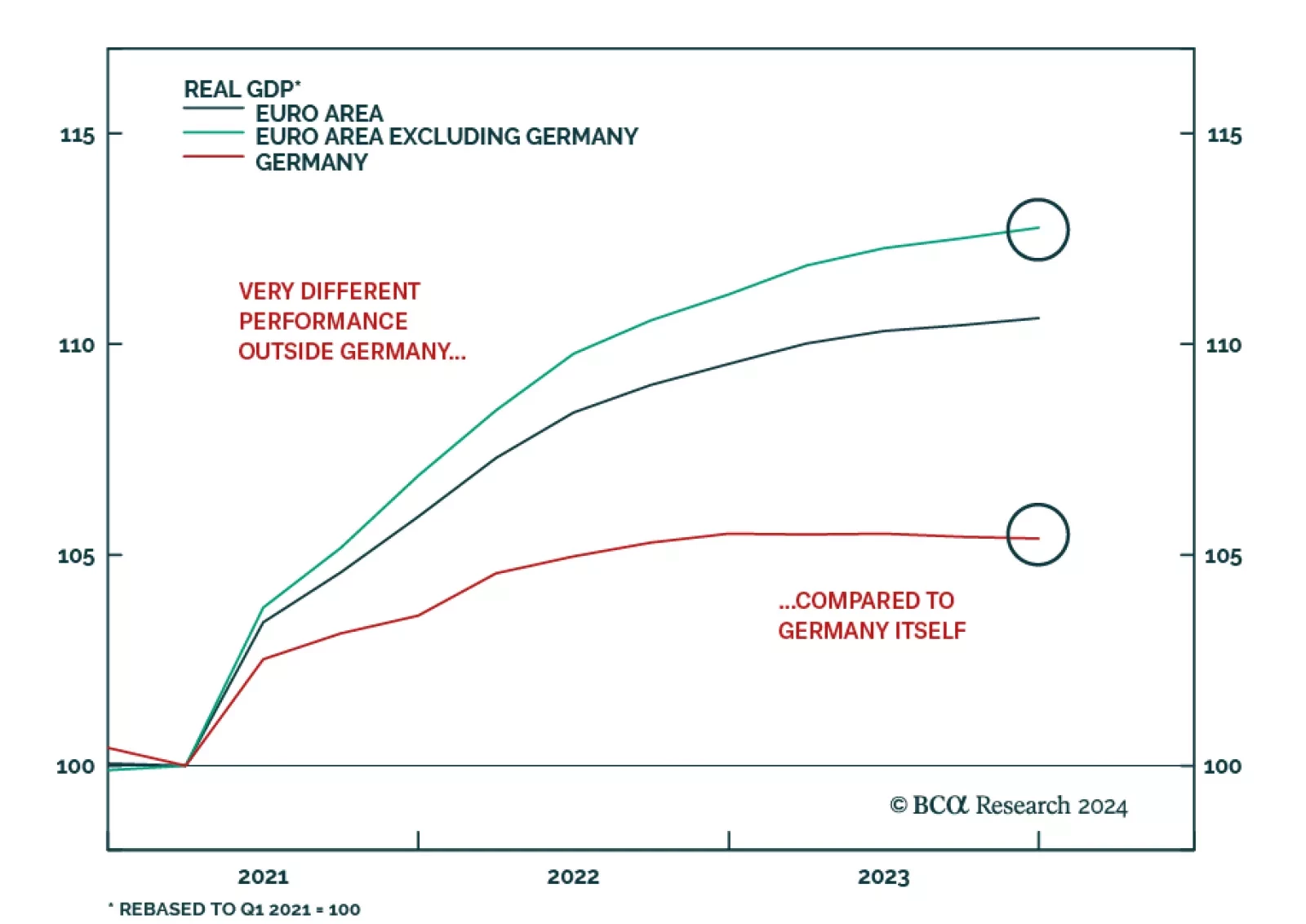

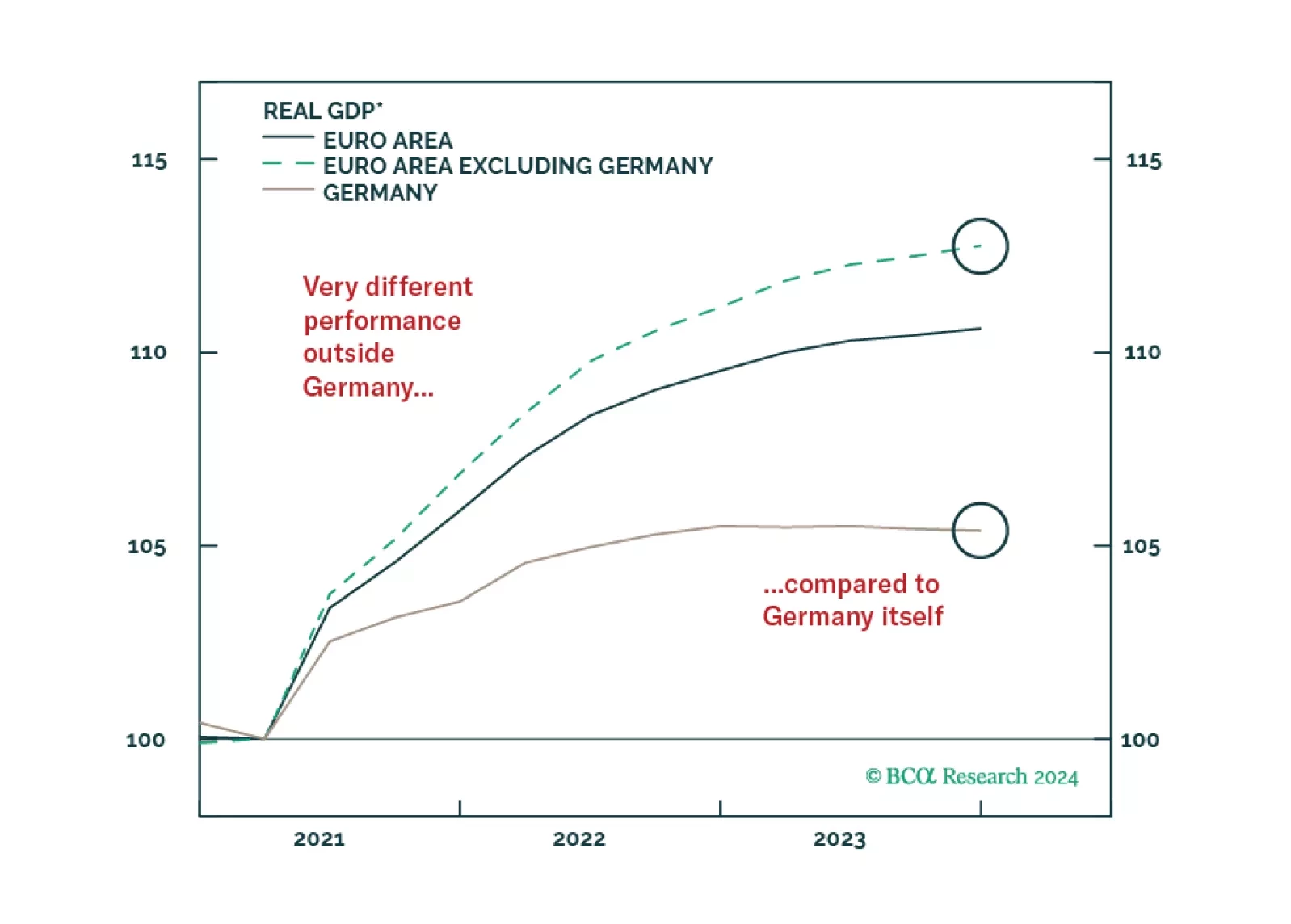

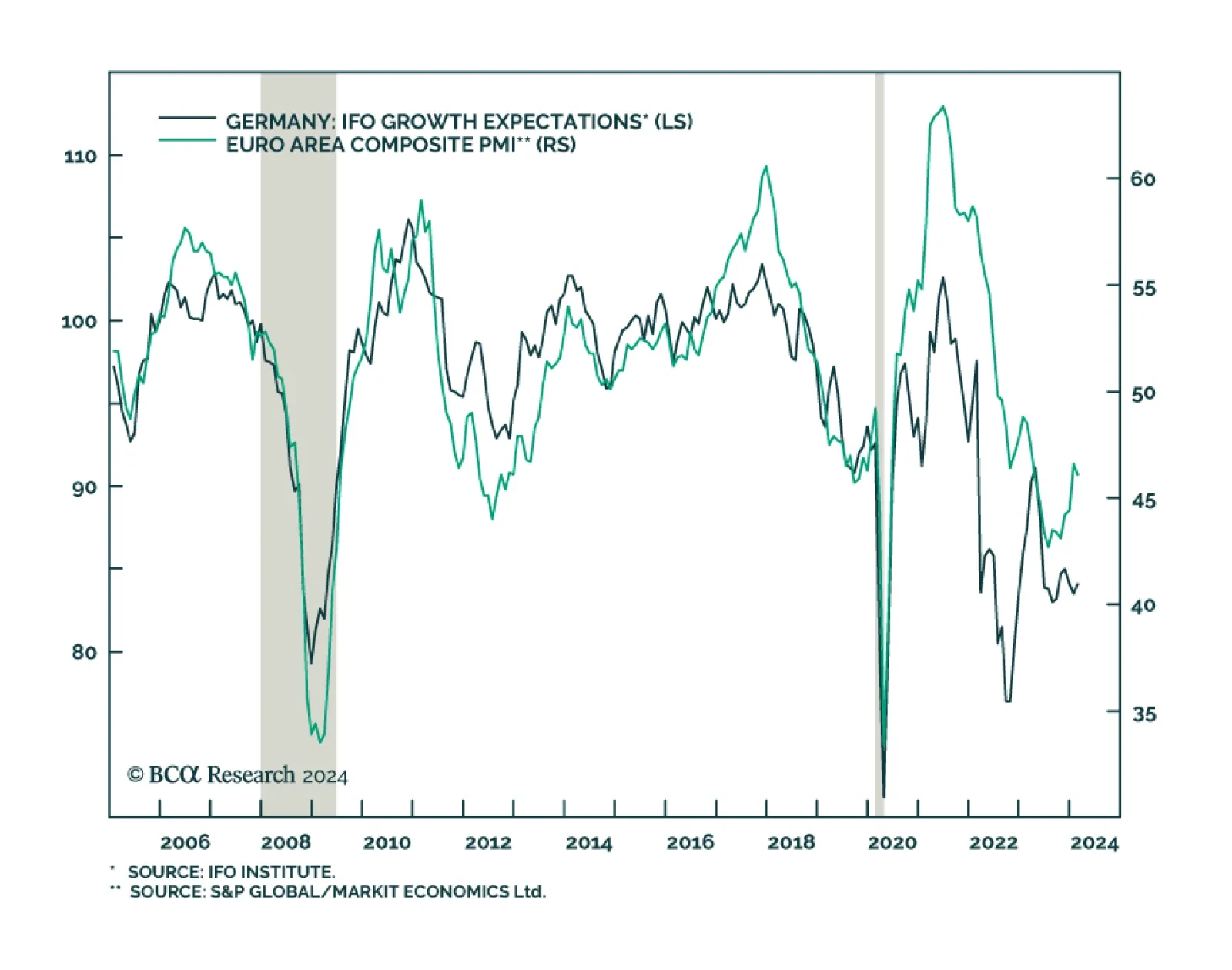

Outside of Germany, European growth fares better than many believe. Will this hidden resilience help the euro and push German yields higher?

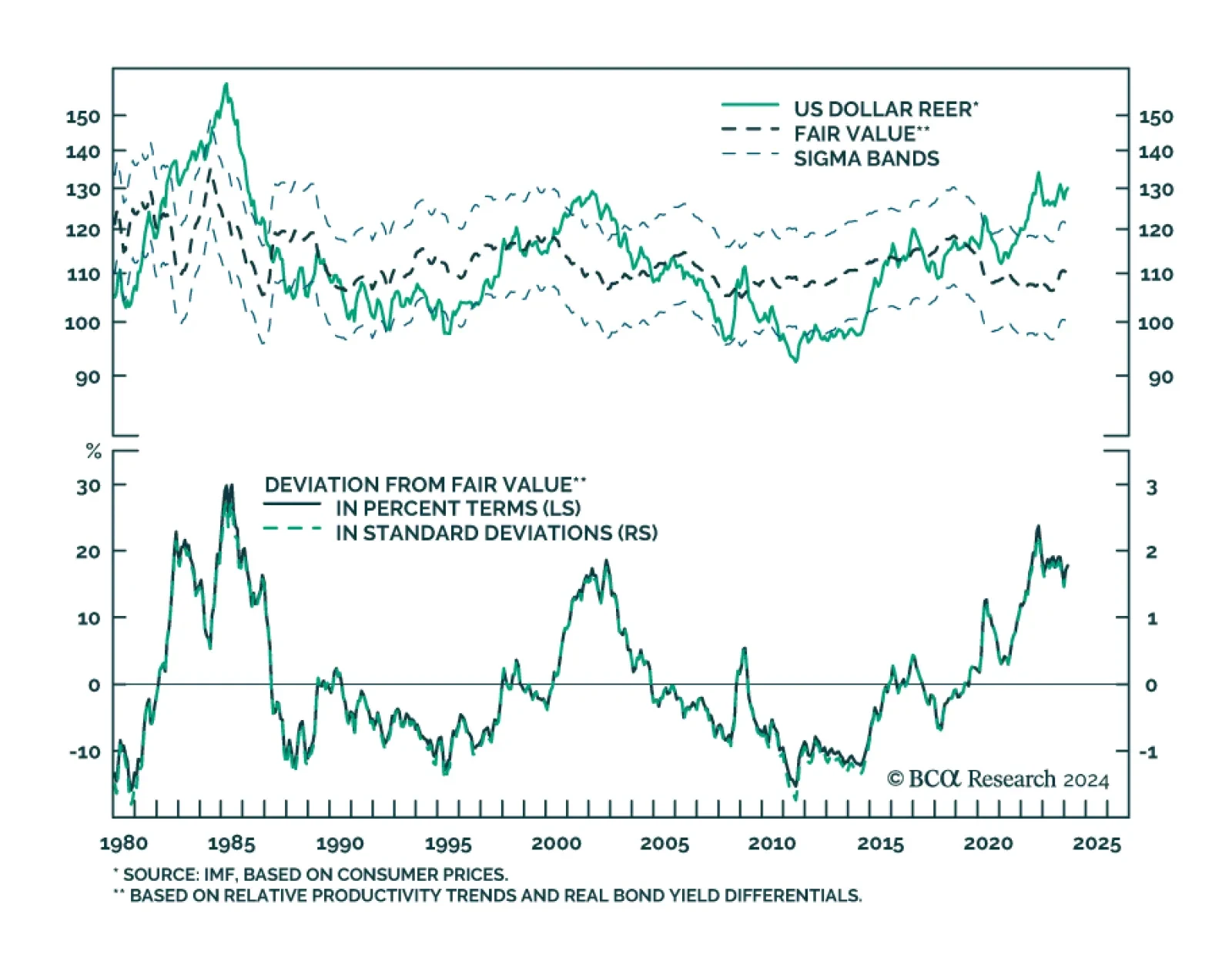

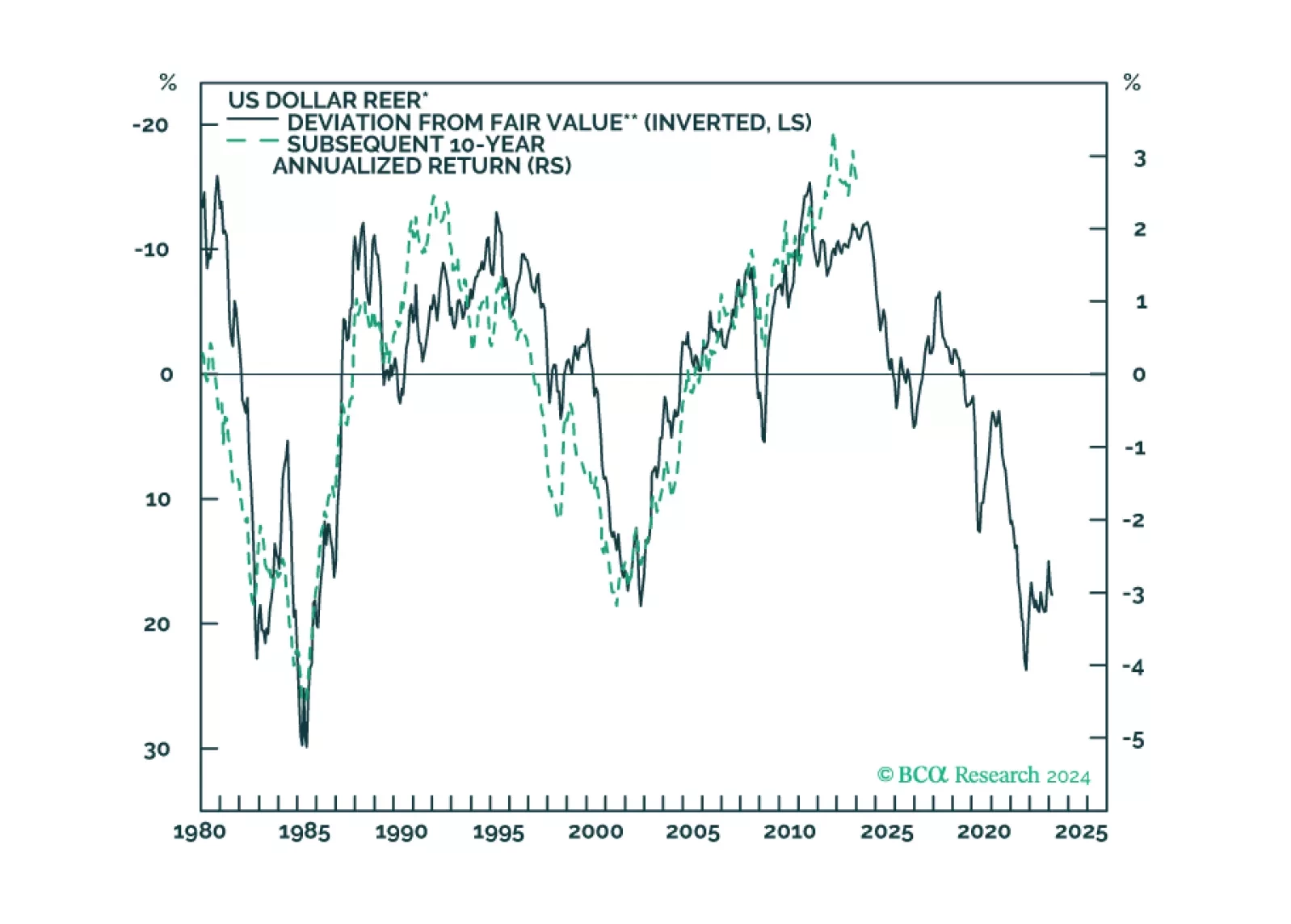

In this week’s report, we release an update to our long-term REER valuation model and expected future returns for major currencies.

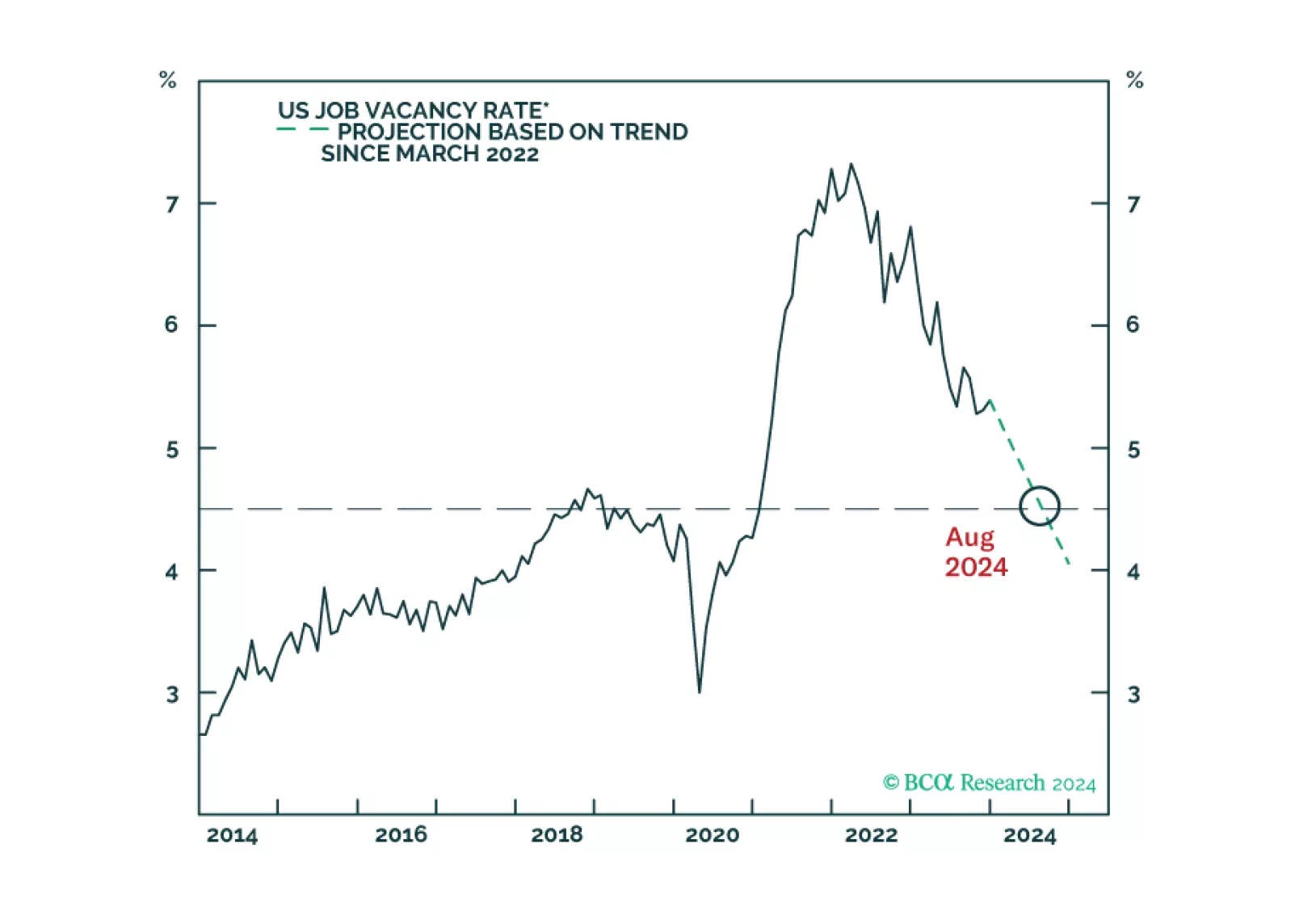

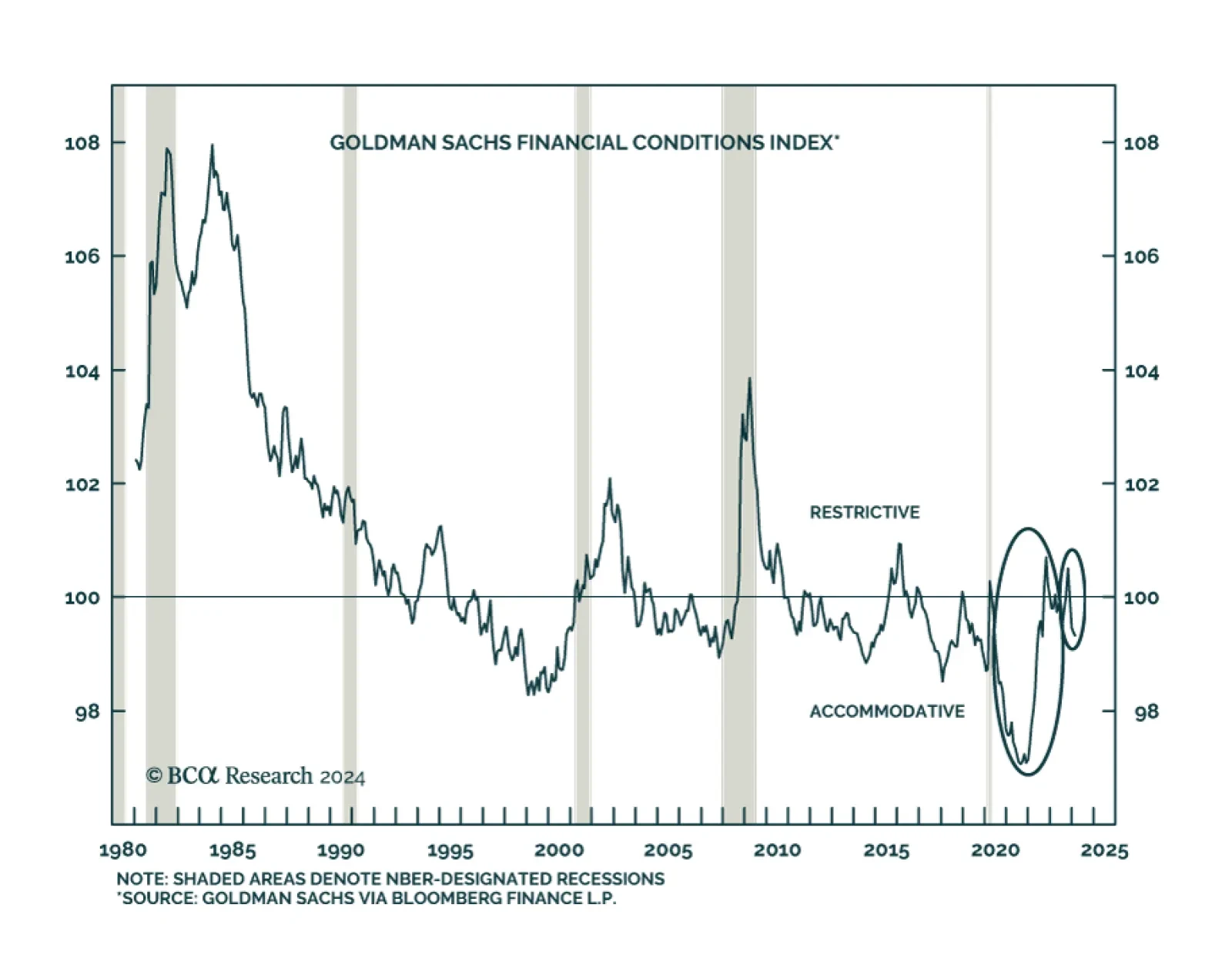

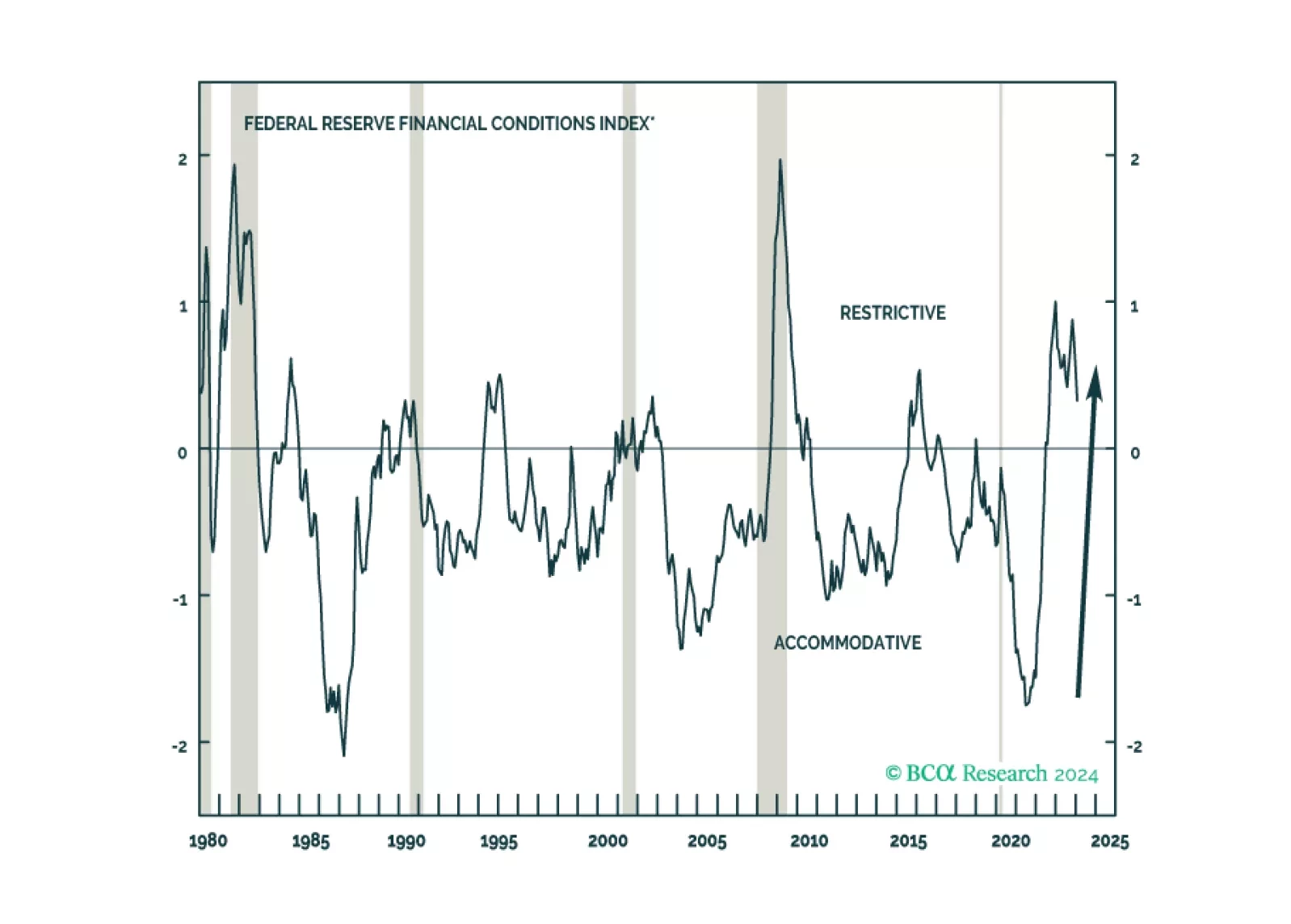

Clients have been pushing back on our recession call on the grounds that it is incompatible with the economy’s second-half acceleration and the more recent easing in financial conditions. We examine both of those points in the course of doing some pushing back of our own.