Developed Countries

A recent slew of macroeconomic data has reassured us that the runway to a recession is longer than many thought. However, that positive realization comes with two caveats. First, the Fed pivot is not imminent, and the magnitude of rate cuts may disappoint. Second, the recession has been delayed but not avoided. Further, geopolitical risk is elevated. We will overweight Tech on the next dip and upgrade Retail to an overweight.

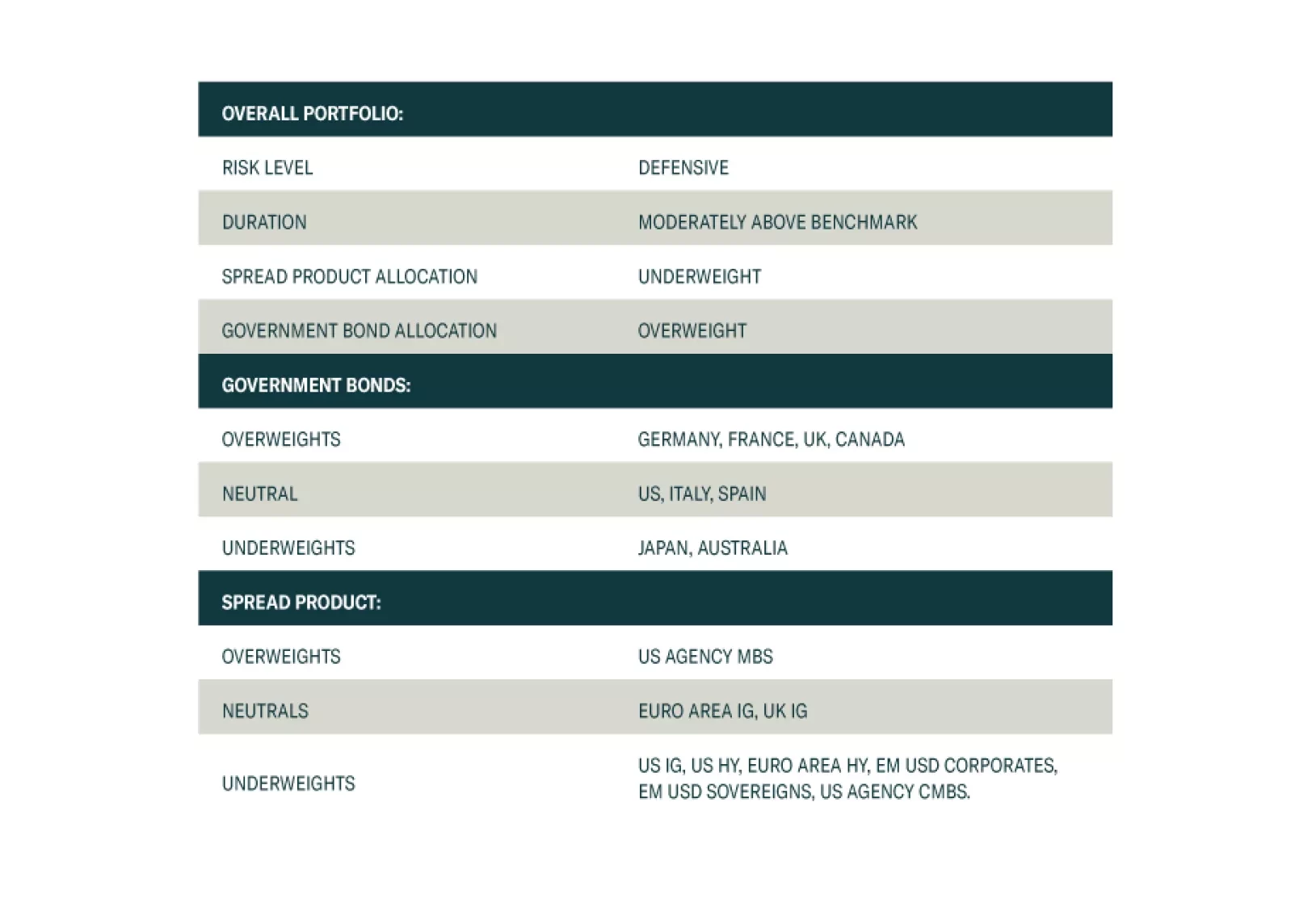

We present the performance review of the Global Fixed Income Strategy Model Bond Portfolio for 2023. We also discuss the outlook for 2024 performance based on our Key Views for the year. The portfolio is positioned to benefit from a year where the global backdrop will be one of weak growth and further declines in inflation, leading central bank to begin cutting interest rates.

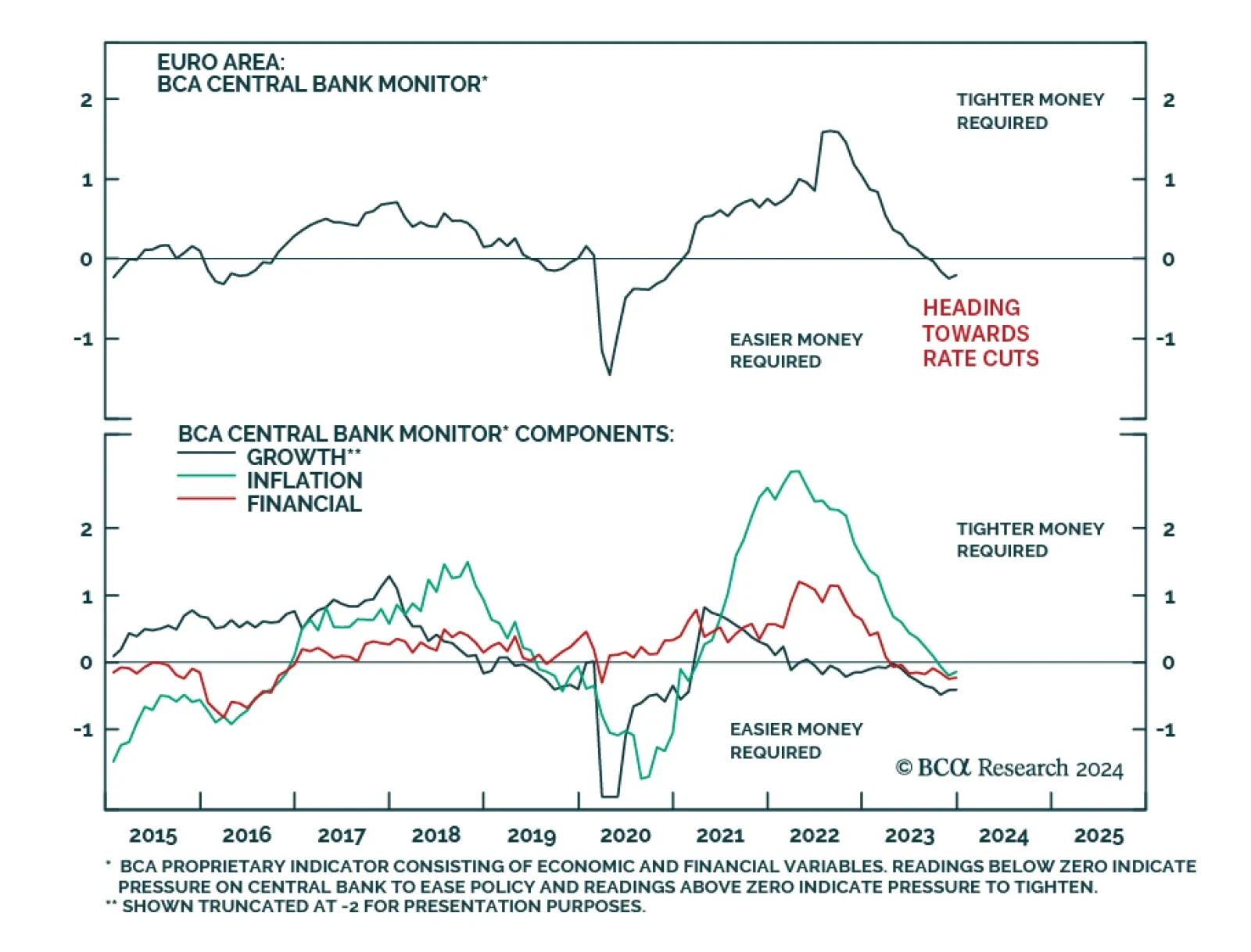

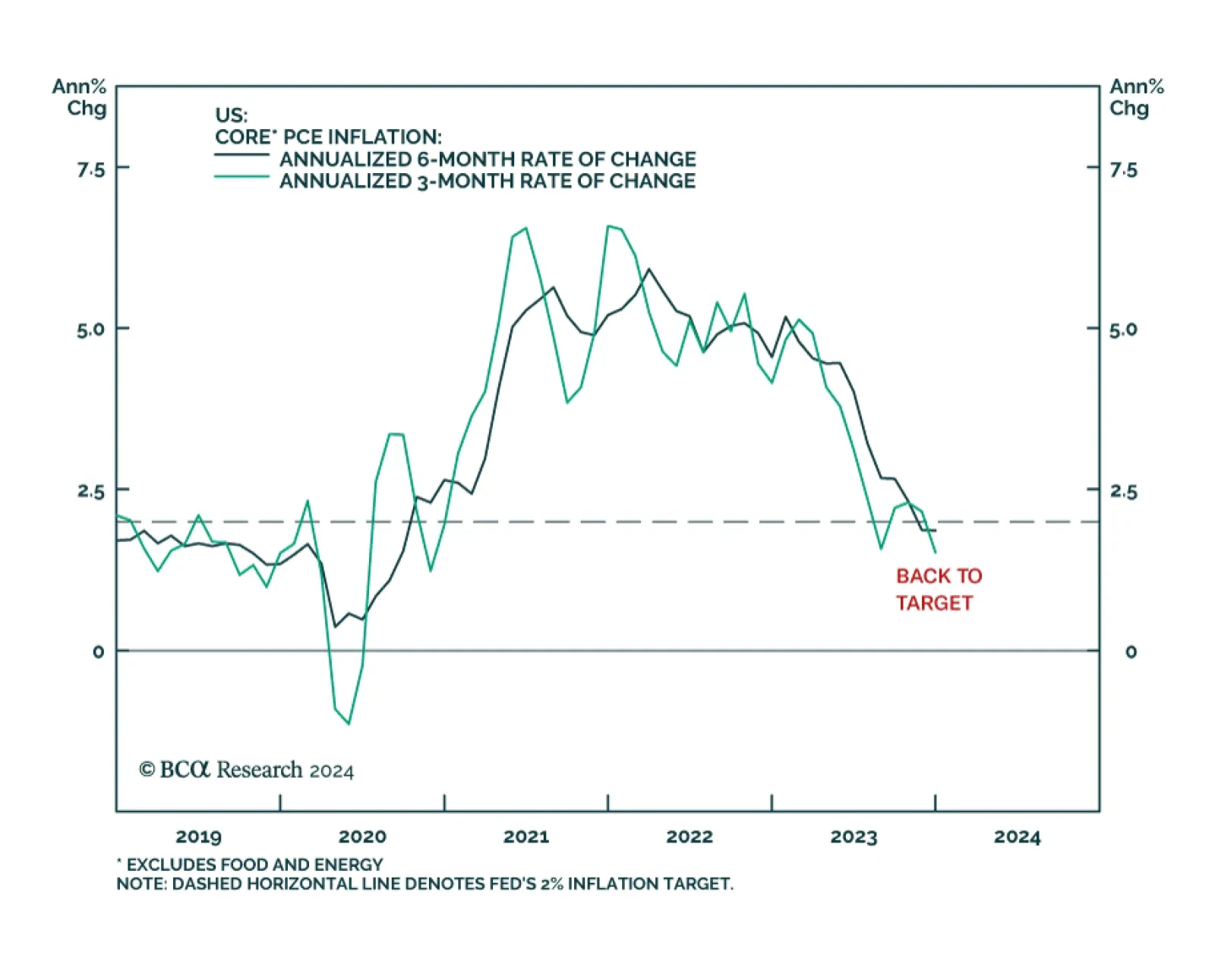

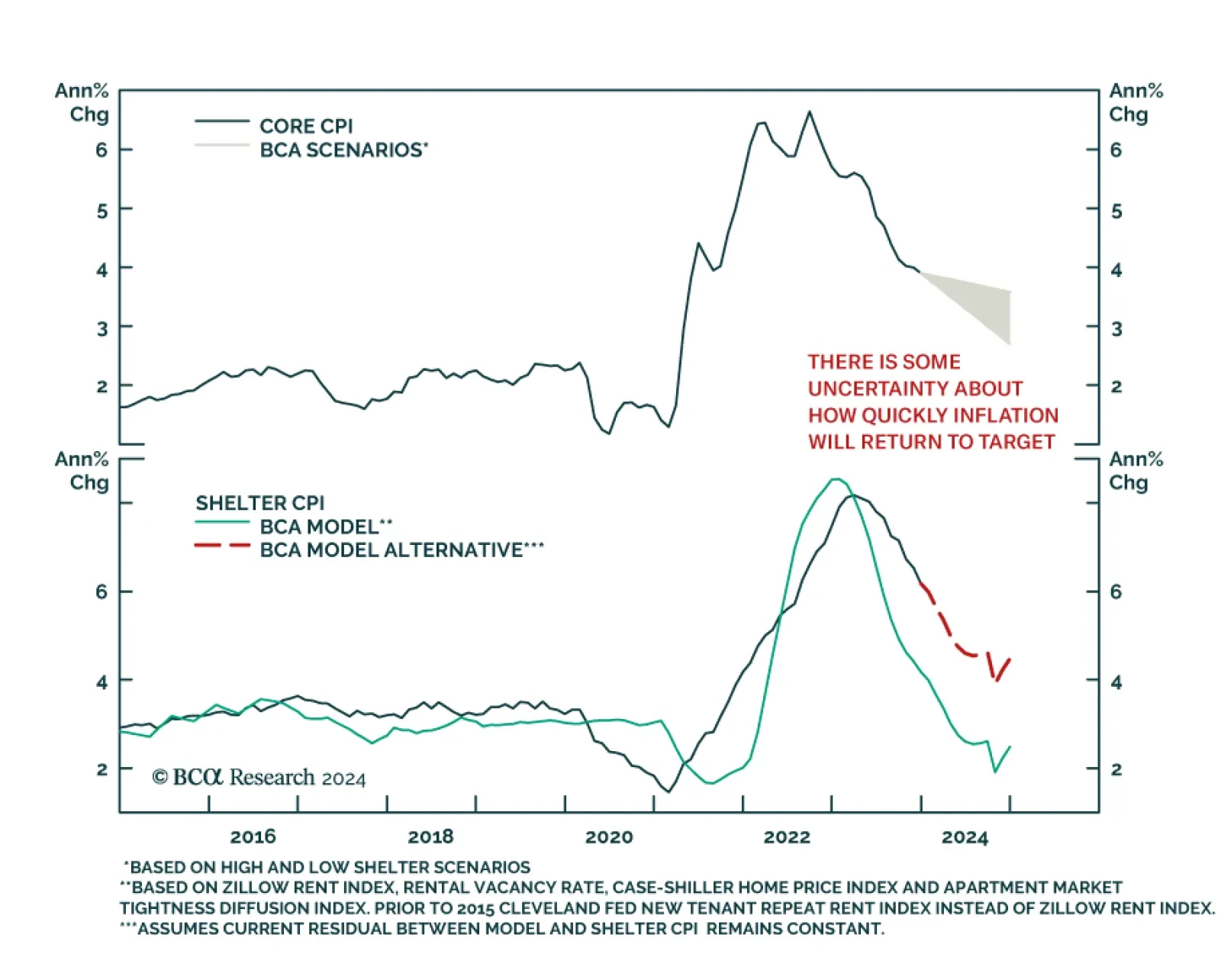

Low inflation argues for the Fed to move relatively quickly toward rate cuts. Continued above-trend GDP growth poses a risk to this view, but leading indicators point to slower growth in the coming quarters.

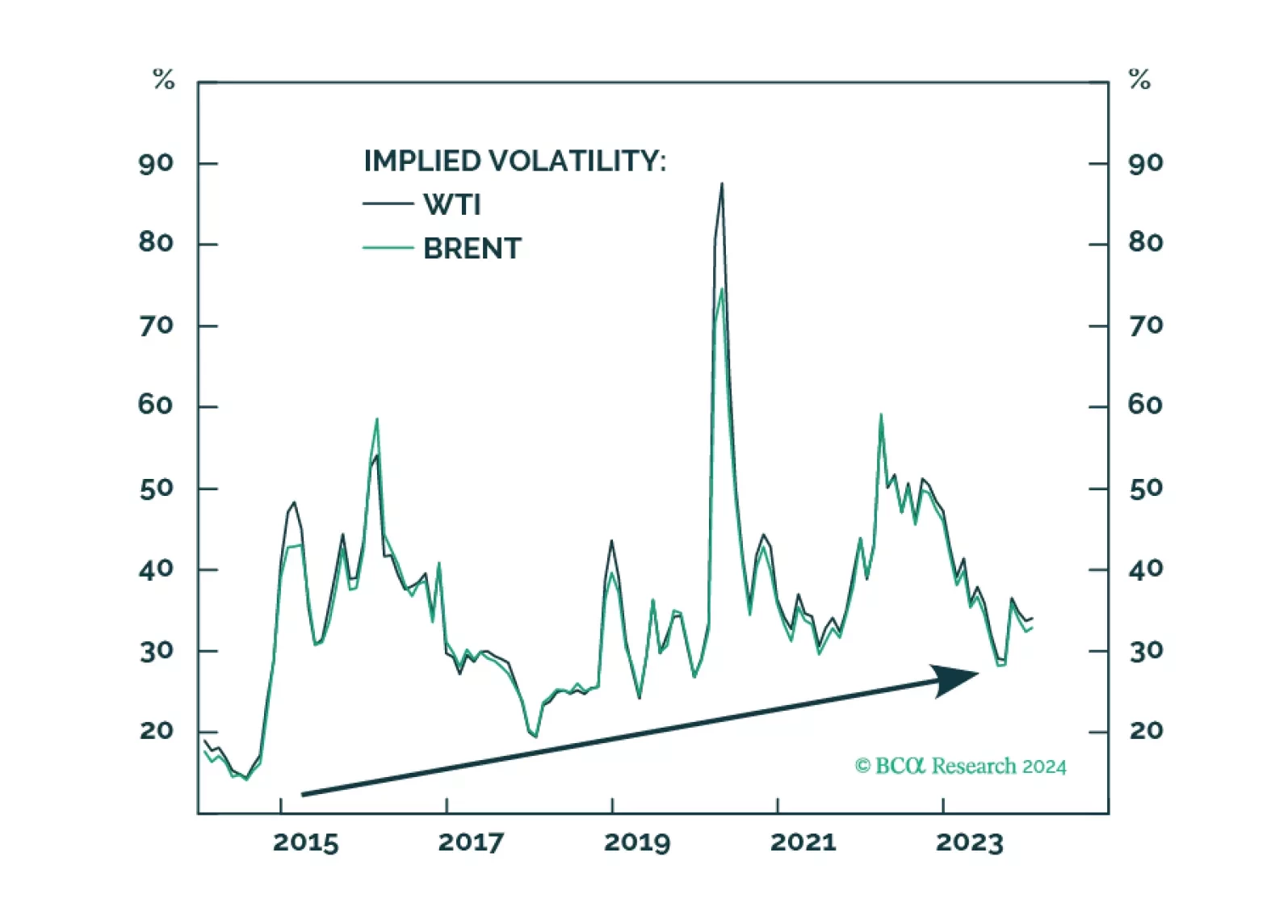

Commodity volatility will continue its rising trend since 2014. The US is on the brink of a major election, the outcome of which could reduce its willingness to engage with the outside world. So, states seeking to carve out their own spheres of influence are incentivized to raise the economic costs to the US and discourage its influence in their regions. These states can do this by interfering in key trading routes in their regions. As a result, geopolitical threats to maritime chokepoints are a structural as well as cyclical problem and will persist due to the revival of superpower competition.