Developed Countries

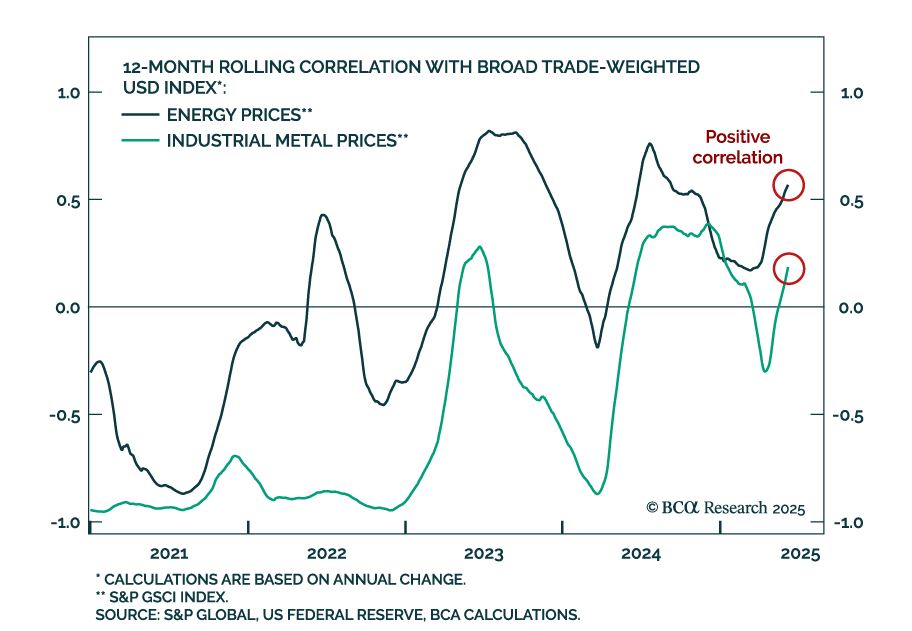

Our Commodity strategists see a breakdown of historical commodity correlations. The US dollar now shows a positive correlation with commodities, particularly energy, and a weaker dollar will no longer guarantee upside for commodity prices. Softening global…

While we anticipate higher inflation in June, it looks increasingly likely that the price impact from tariffs will be less aggressive and long-lasting than many feared.

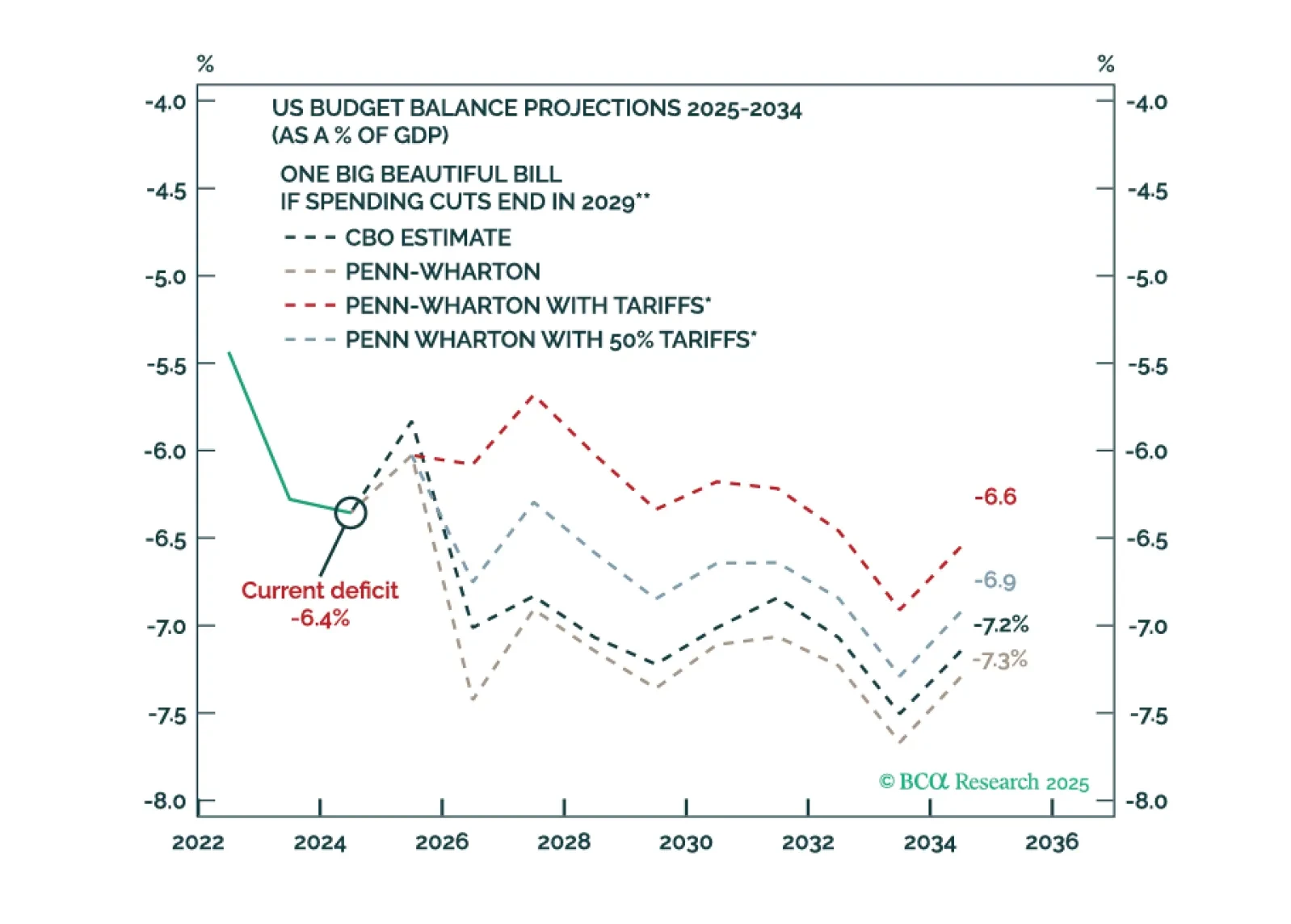

Bond market volatility will spike again in the near term. The Fed is committed to an easing cycle yet the Trump administration’s signature fiscal policy action will stimulate the economy. Tariffs are supposed to keep the budget deficit contained but they are inflationary.

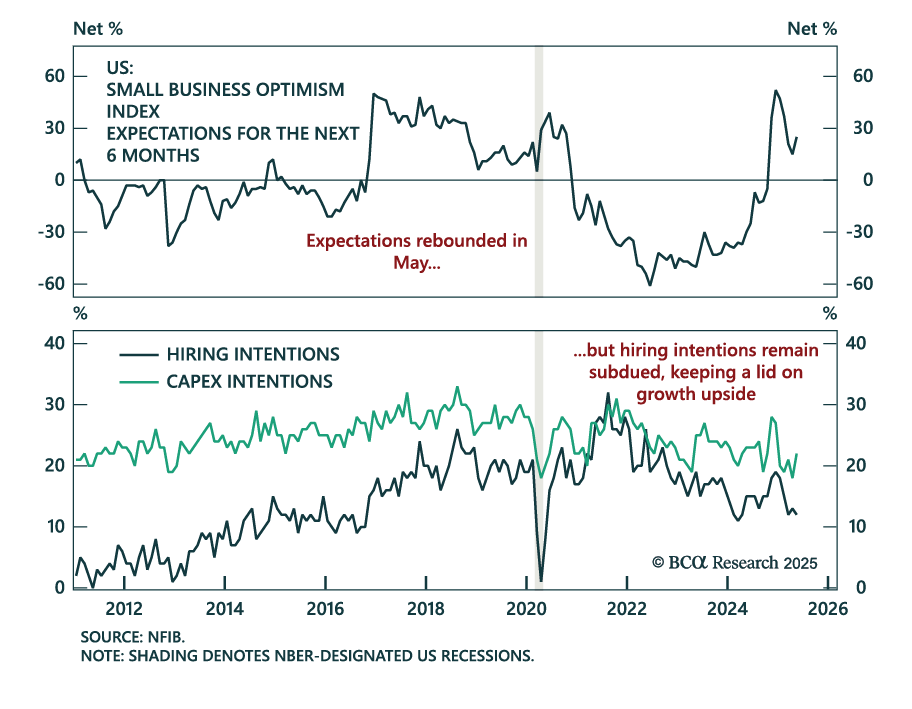

Small business confidence improved in May, but hiring intentions fell and activity remains sluggish, reinforcing our cautious equity stance. The NFIB Small Business Optimism Index rose to 98.8, beating expectations. However, most of the improvement came from…

UK labor market deterioration reinforces our overweight on Gilts and dovish BoE policy trades. Payrolls fell by 109k in May, an acceleration from the 55k revised decline for April (originally reported as -33k), and job vacancies continued to slide. Slower…

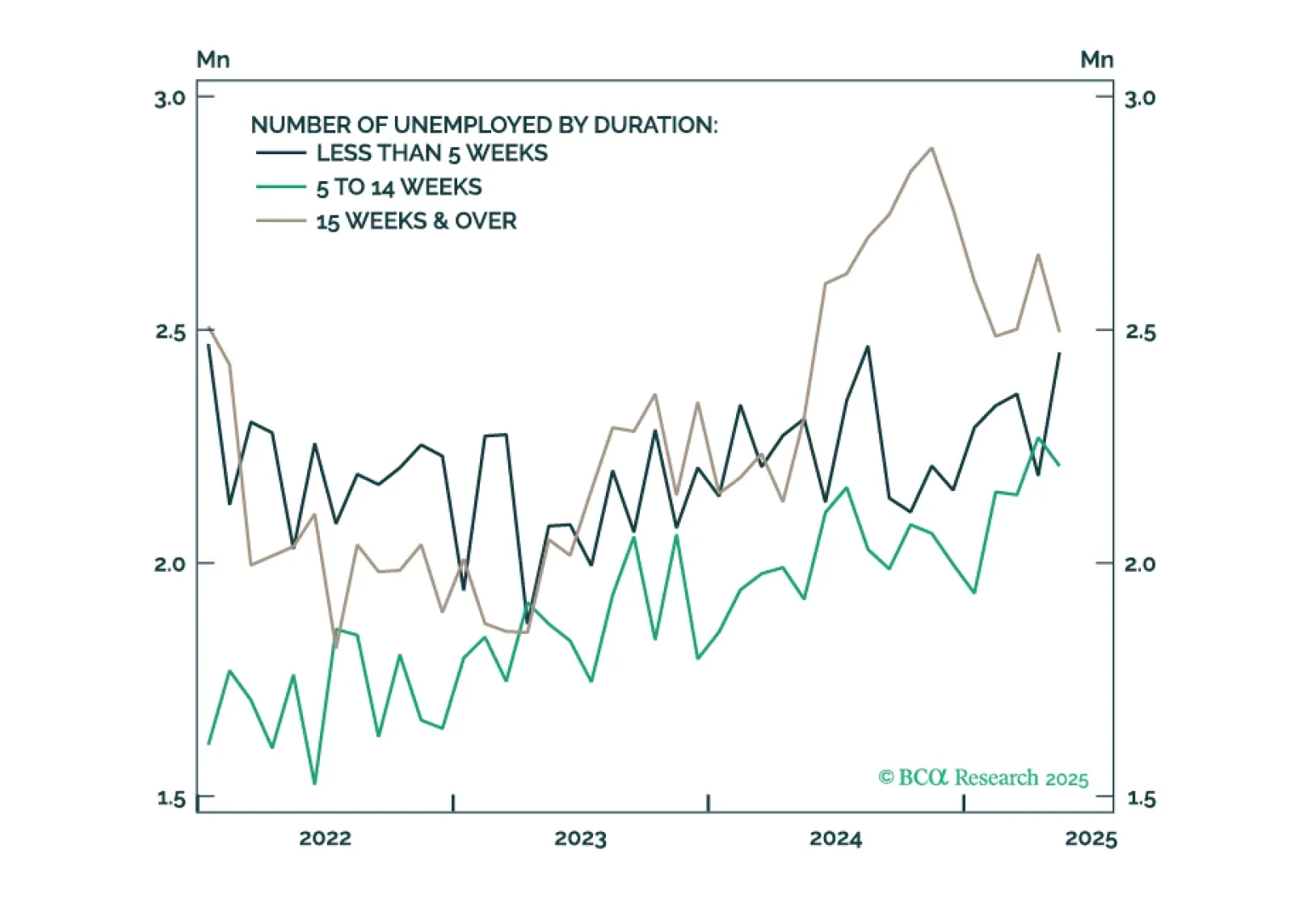

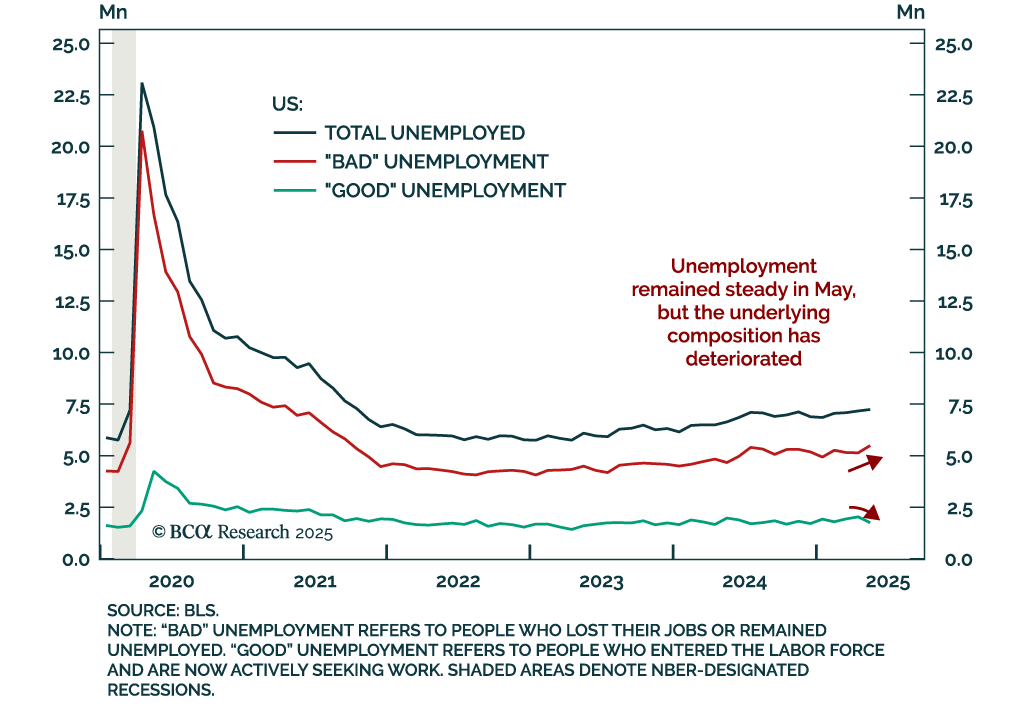

For now, measures of labor market utilization (like the unemployment rate) are only gradually weakening. But we know from history that these trends have a habit of quickly accelerating in advance of recession.

Our Counterpoint Strategists see no signs of recession or market fragility but remain skeptical of US superstar stocks. Winners of past tech cycles rarely lead the next, making Web 2.0 firms unlikely beneficiaries of the AI-driven rally. BCA’s Counterpoint…

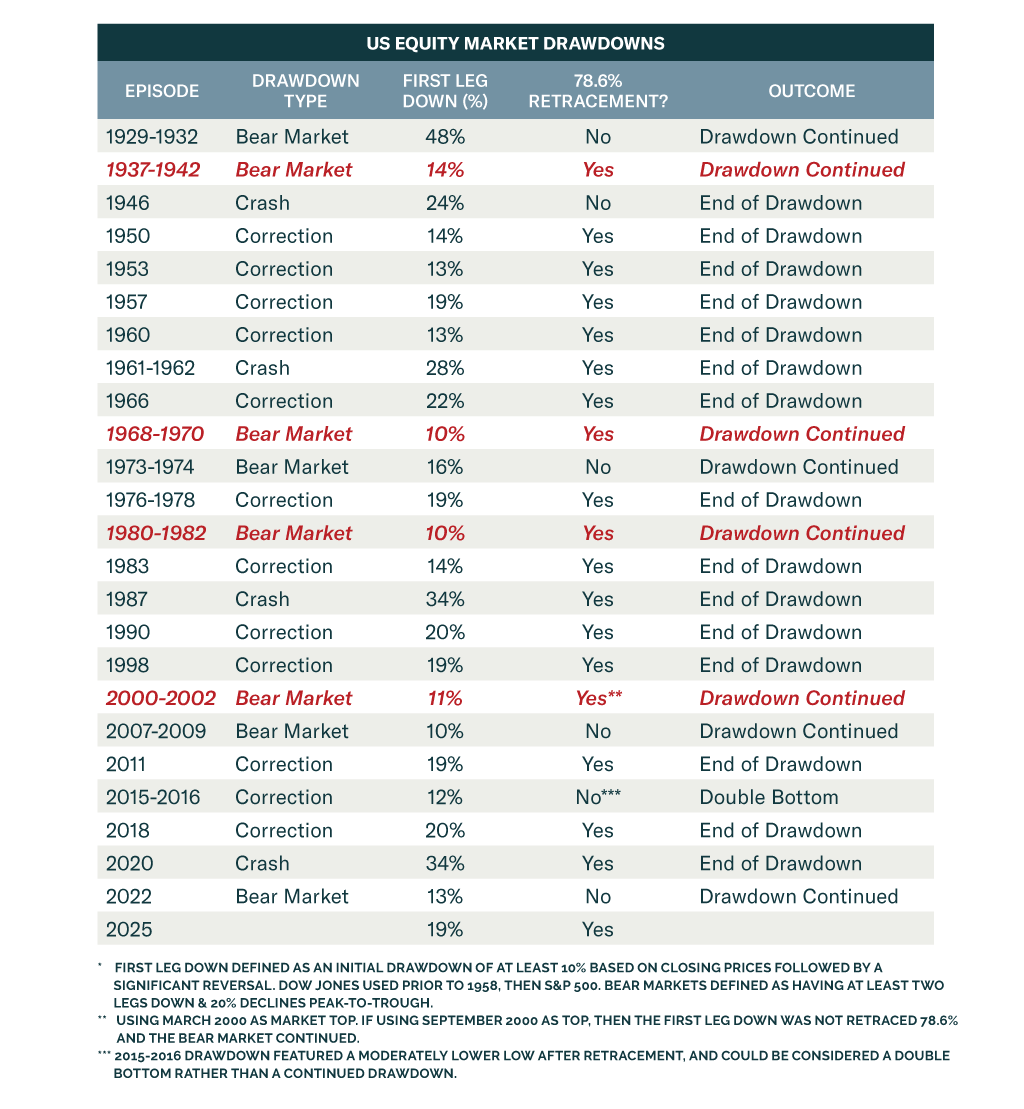

Despite a strong rebound in equities, we remain defensively positioned as recession risks persist and market history warns against premature optimism. The S&P 500 has retraced 78.6% of its initial drawdown, a level that typically signals the end of a…

The May US jobs report reinforces our defensive stance as labor momentum is slowing even if not collapsing. Payrolls rose 139k, beating estimates, but decelerating from a downwardly revised 147k. Two-month revisions cut 95k jobs, again signaling that initial…

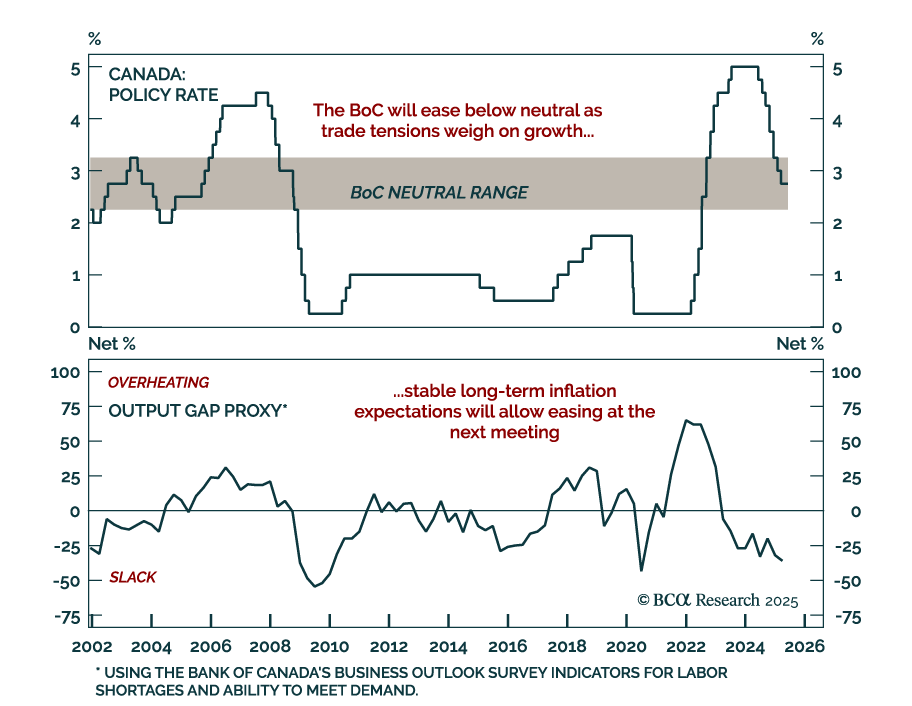

The Bank of Canada held rates at 2.75% but signaled a dovish shift, pushing us to overweight Canadian government bonds and go long CORRA futures. The policy rate remains within the BoC’s neutral range, allowing the Bank to wait for more clarity on trade…