Developed Countries

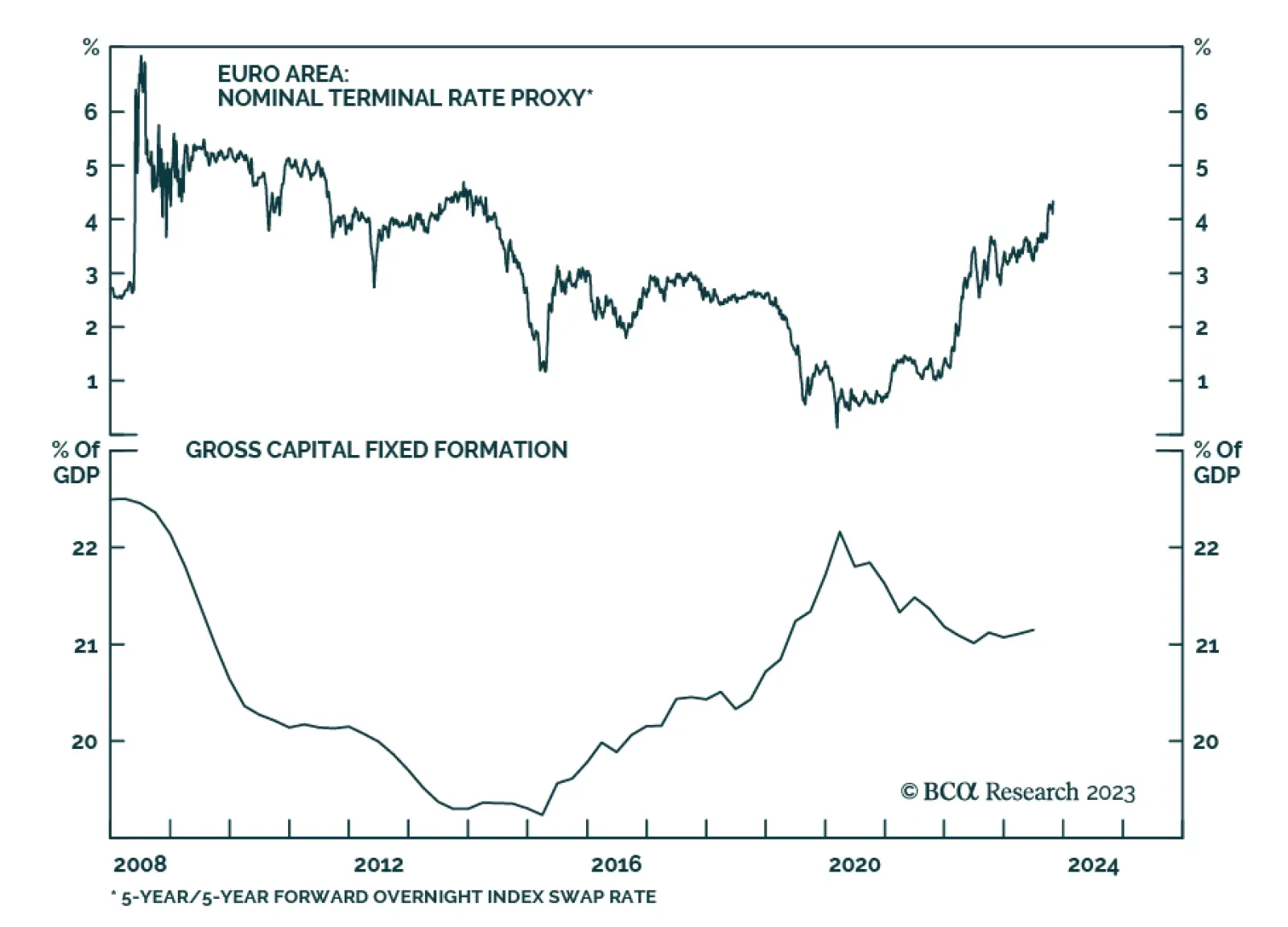

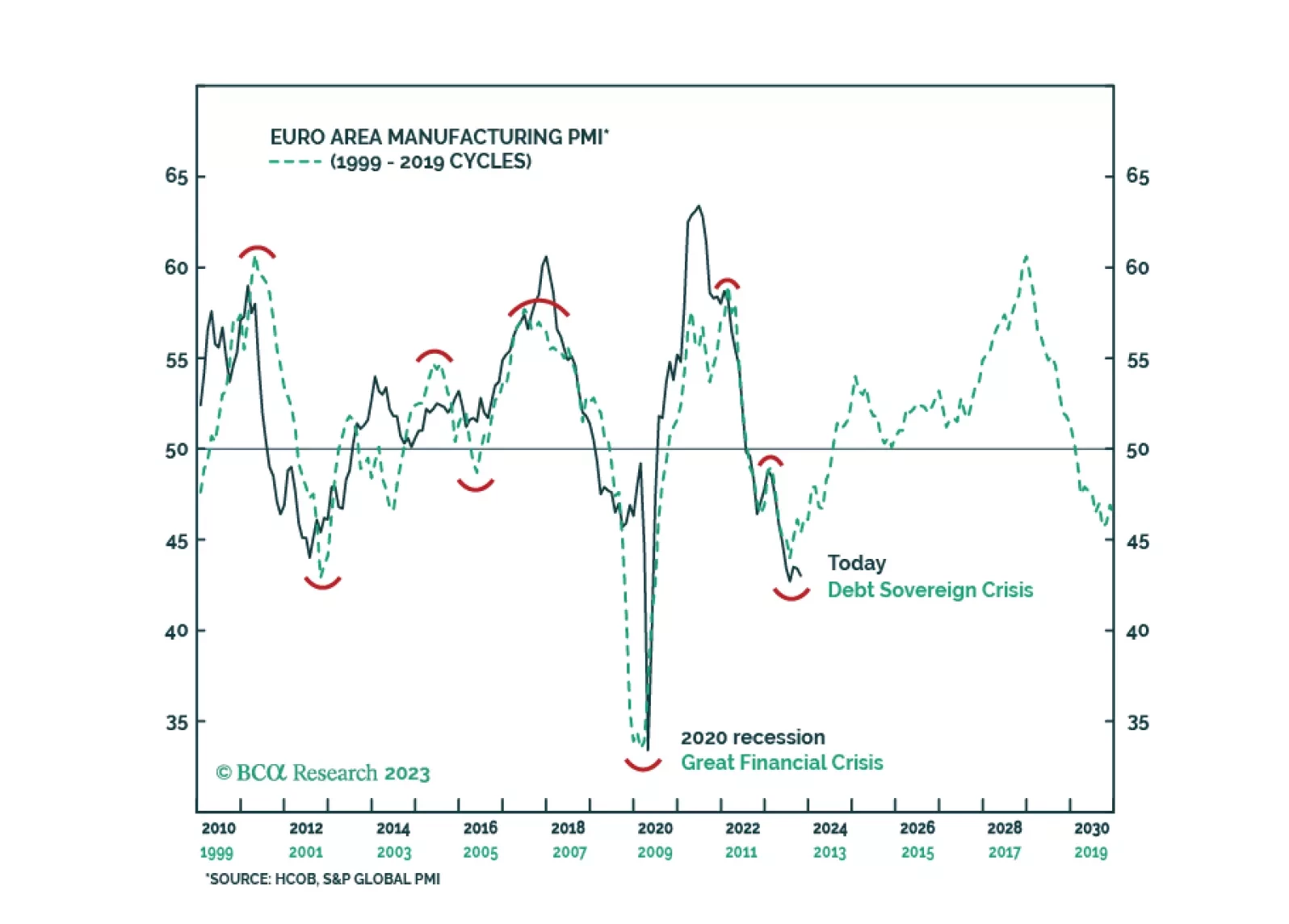

What will the next manufacturing cycle look like in Europe and how will risk assets perform? Lessons from the recent past.

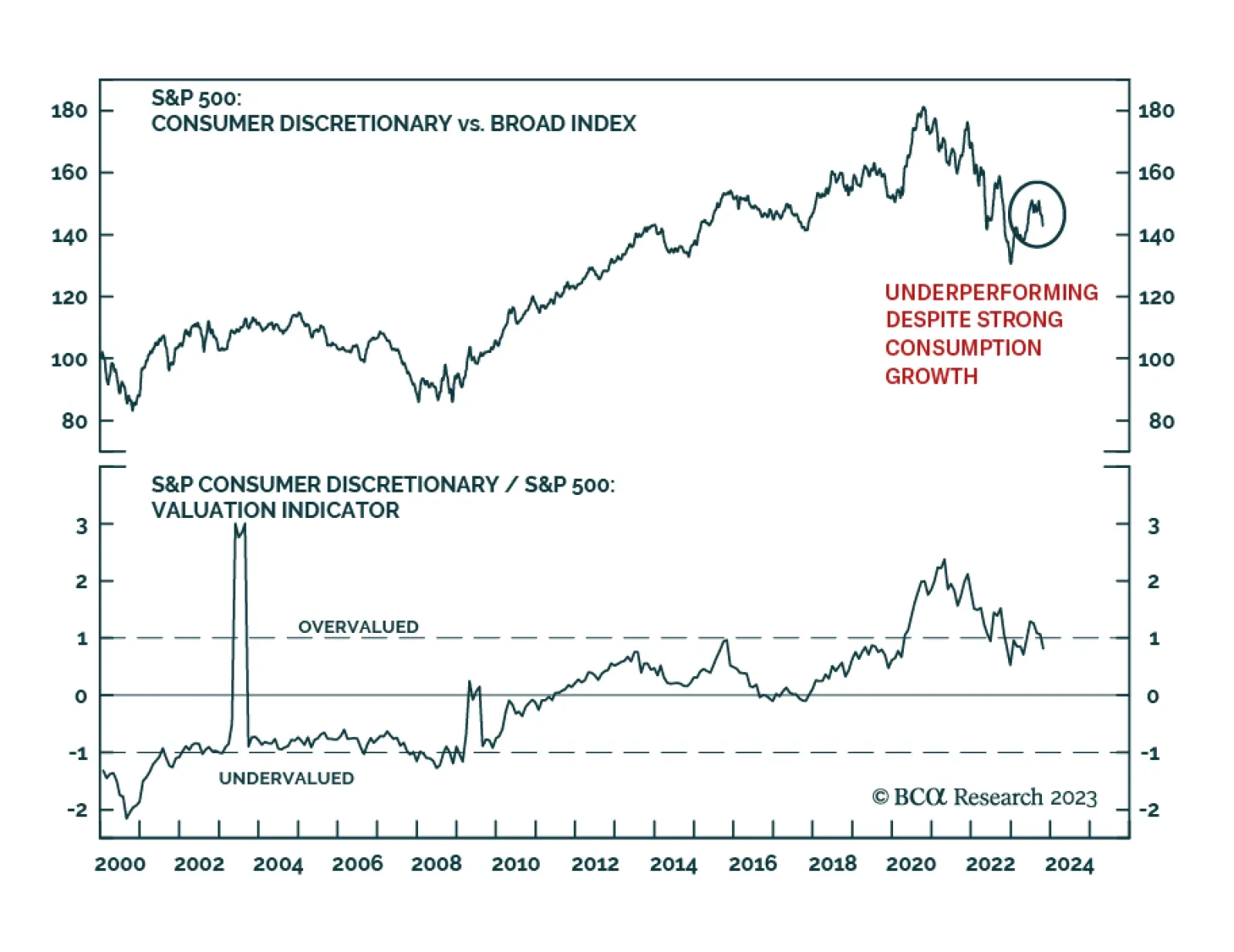

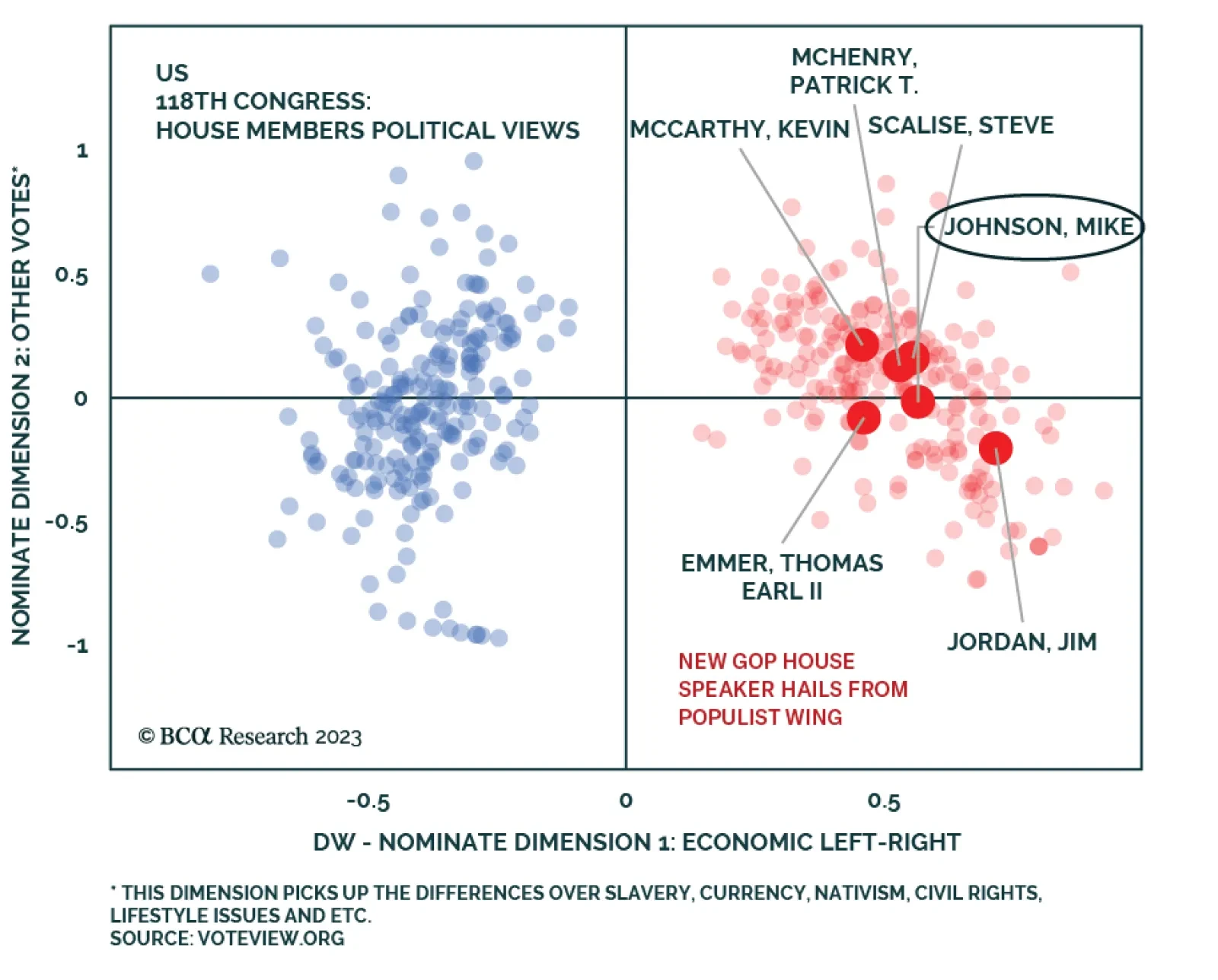

Stronger US growth elicits a response from the House Republicans. But a government shutdown is not devastating to the economy. What is more devastating would be a crisis in the Middle East, Europe, and Asia. Stay long US defense, energy, and large caps stocks.

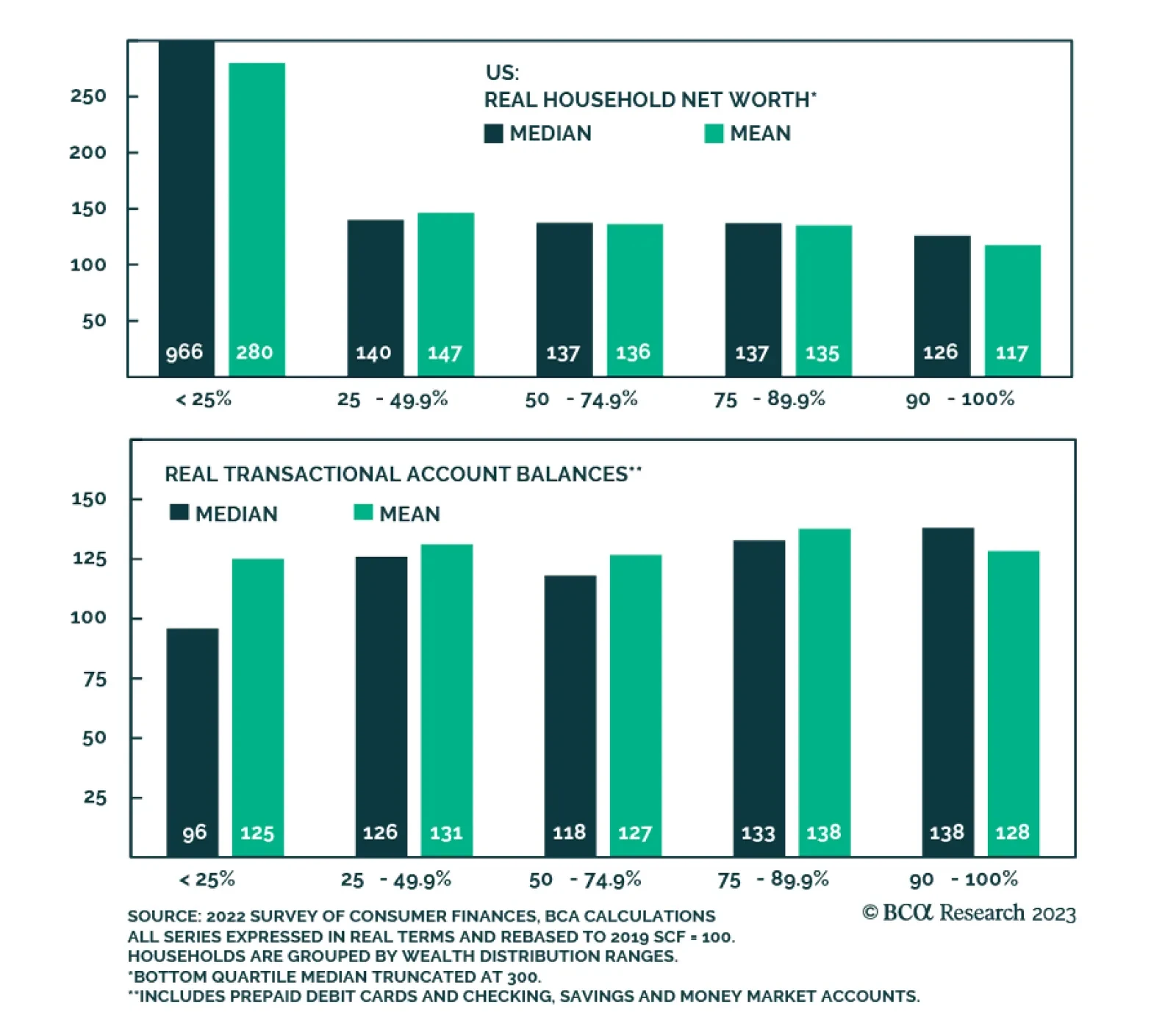

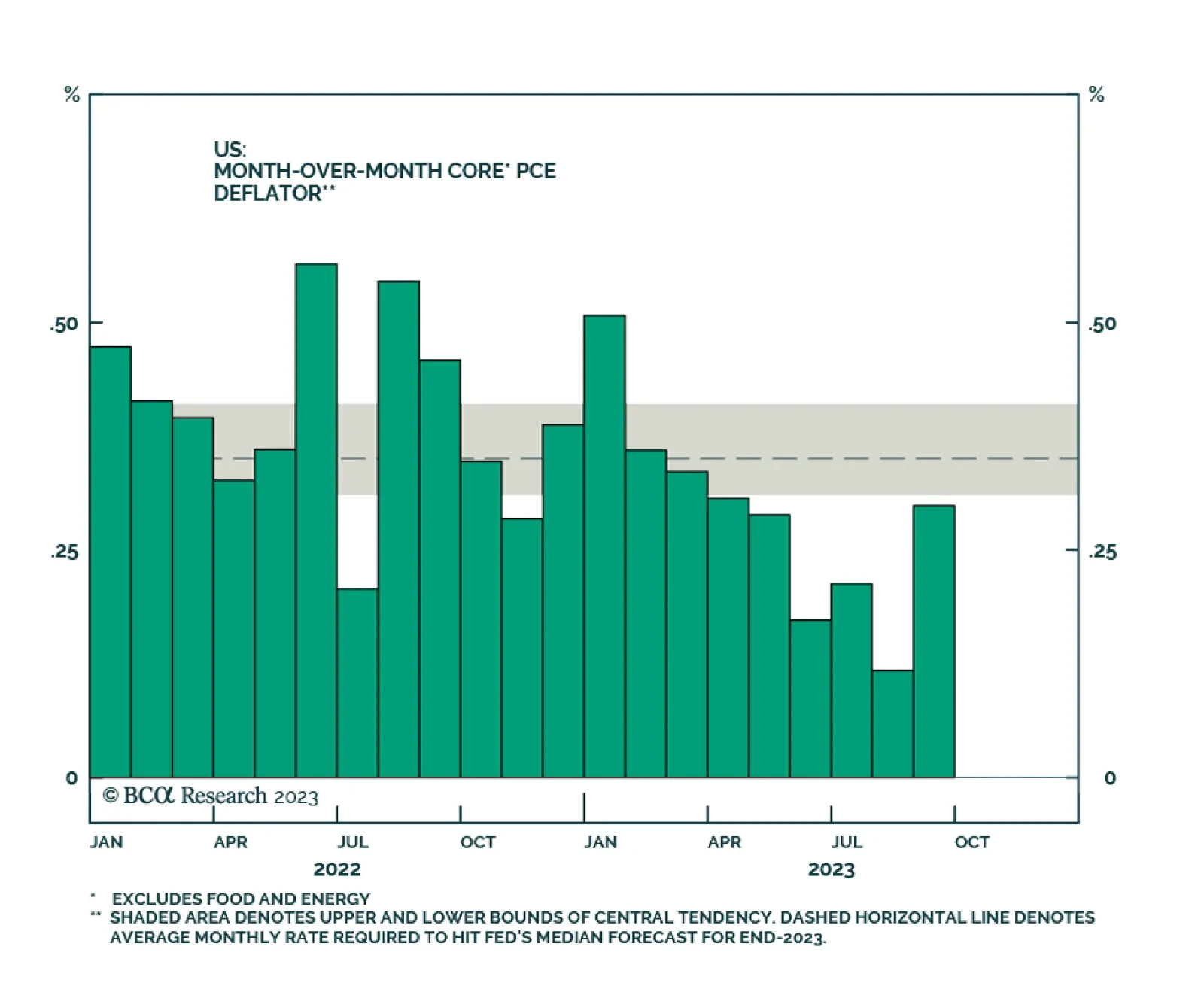

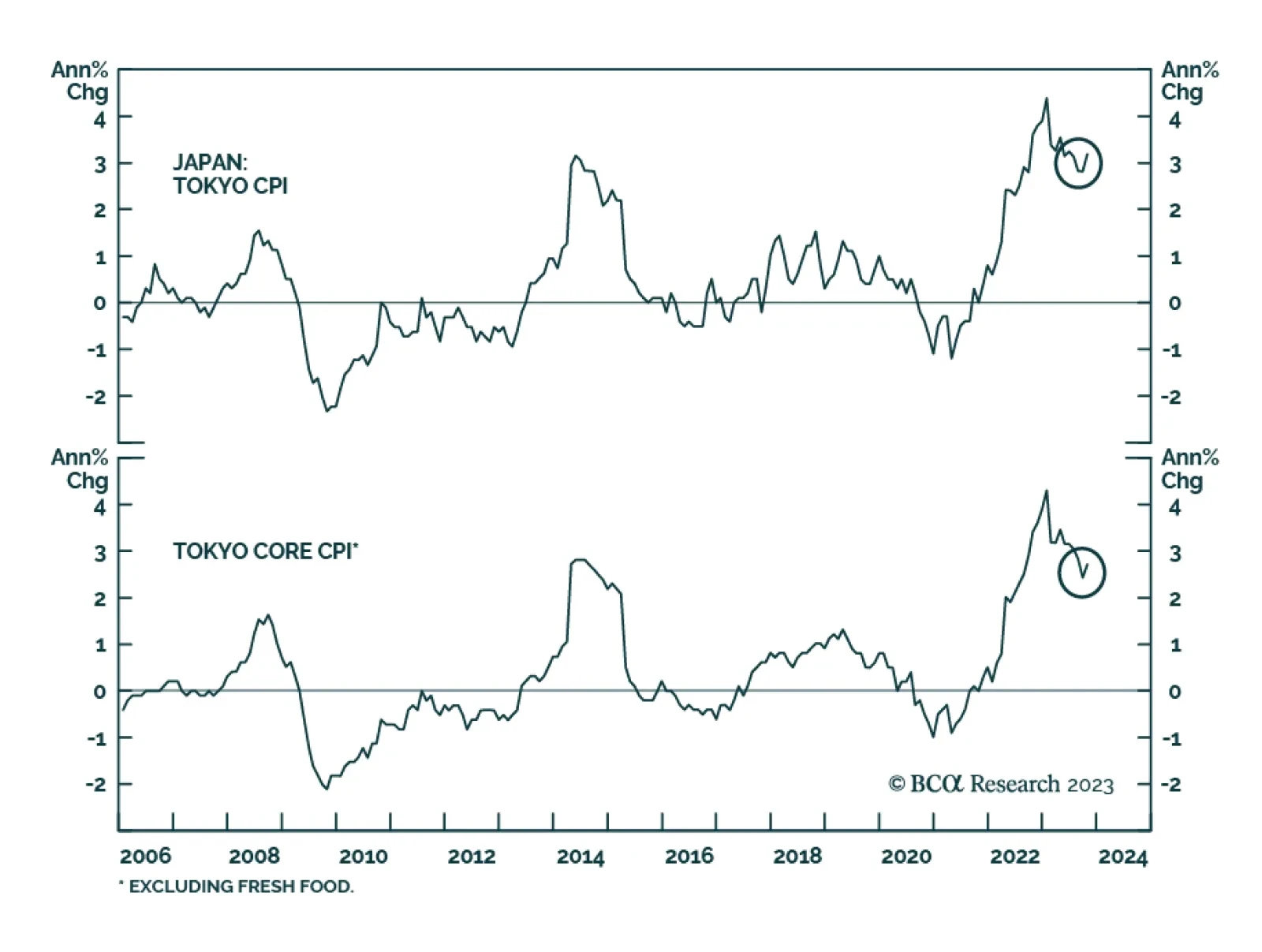

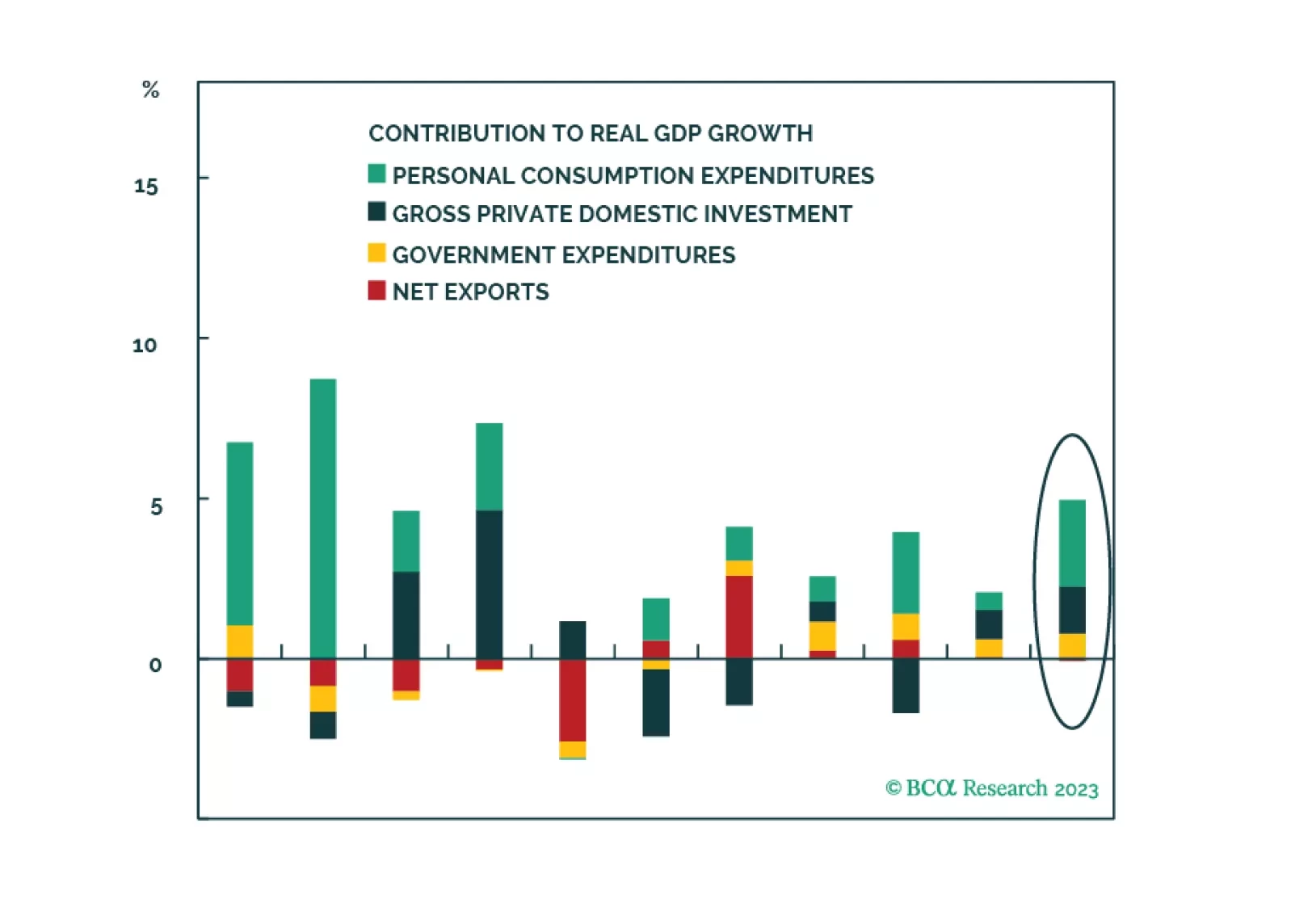

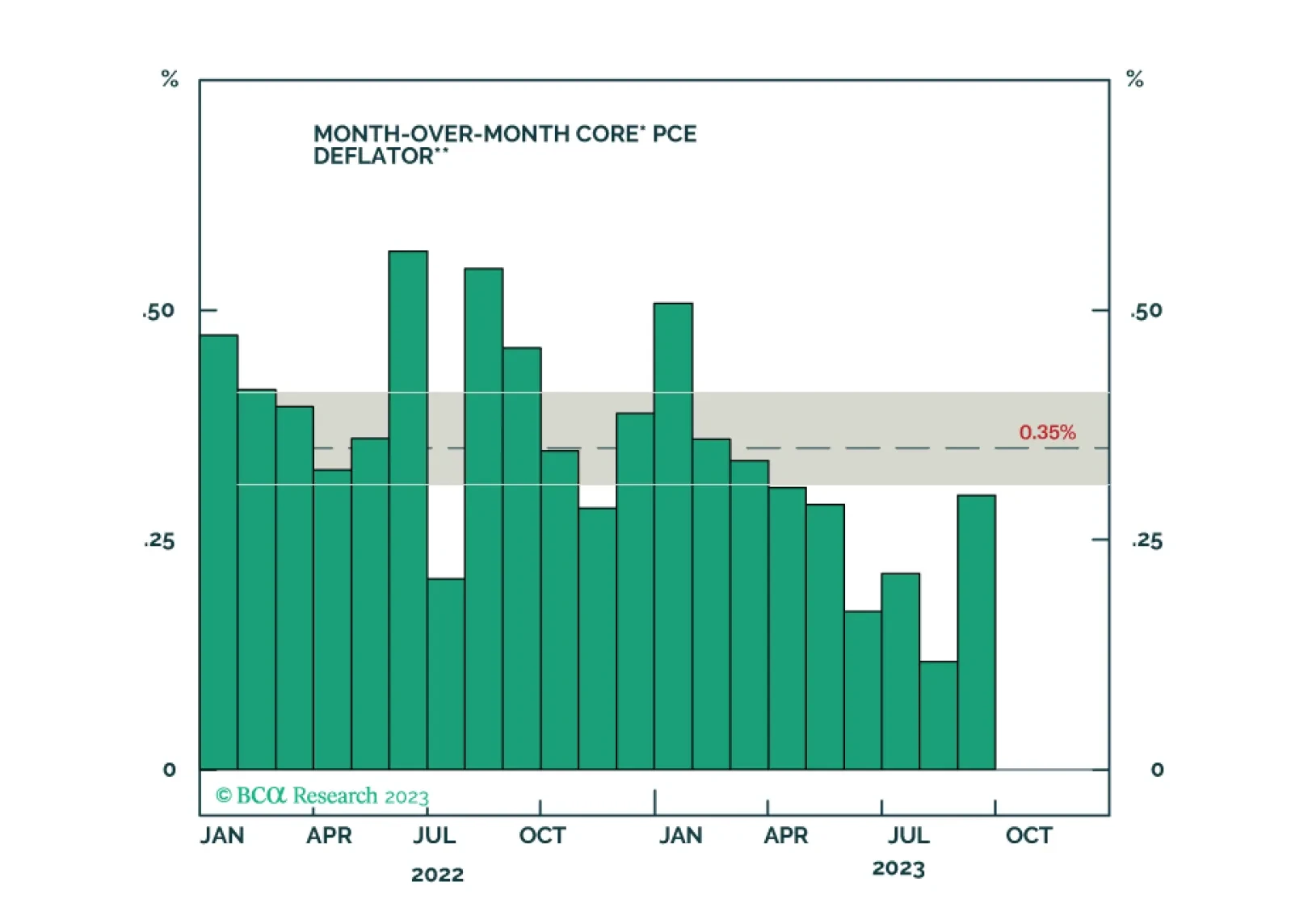

A look at recent data on economic growth, inflation and the labor market, and a discussion of the implications for Fed policy and bond strategy.

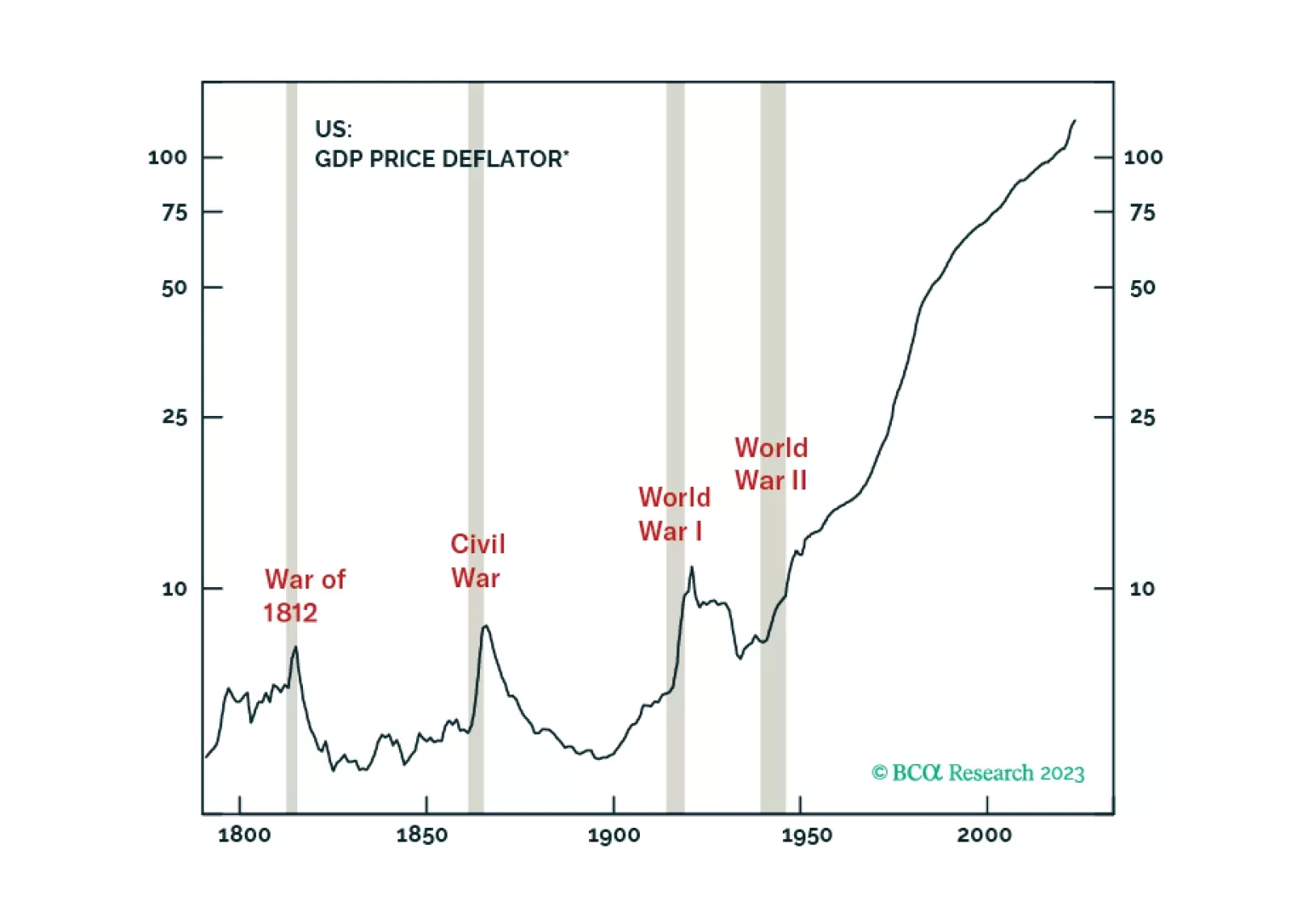

Section II of this month’s Bank Credit Analyst report is a guest piece written by Martin Barnes, which we are making available to all clients. Martin, who retired from BCA Research as Chief Economist in 2021 after a long and illustrious career, expresses his personal views about the long-run outlook for inflation. He argues that the multi-decade disinflationary era is over, which will bring significant challenges for both policymakers and investors.