Developed Countries

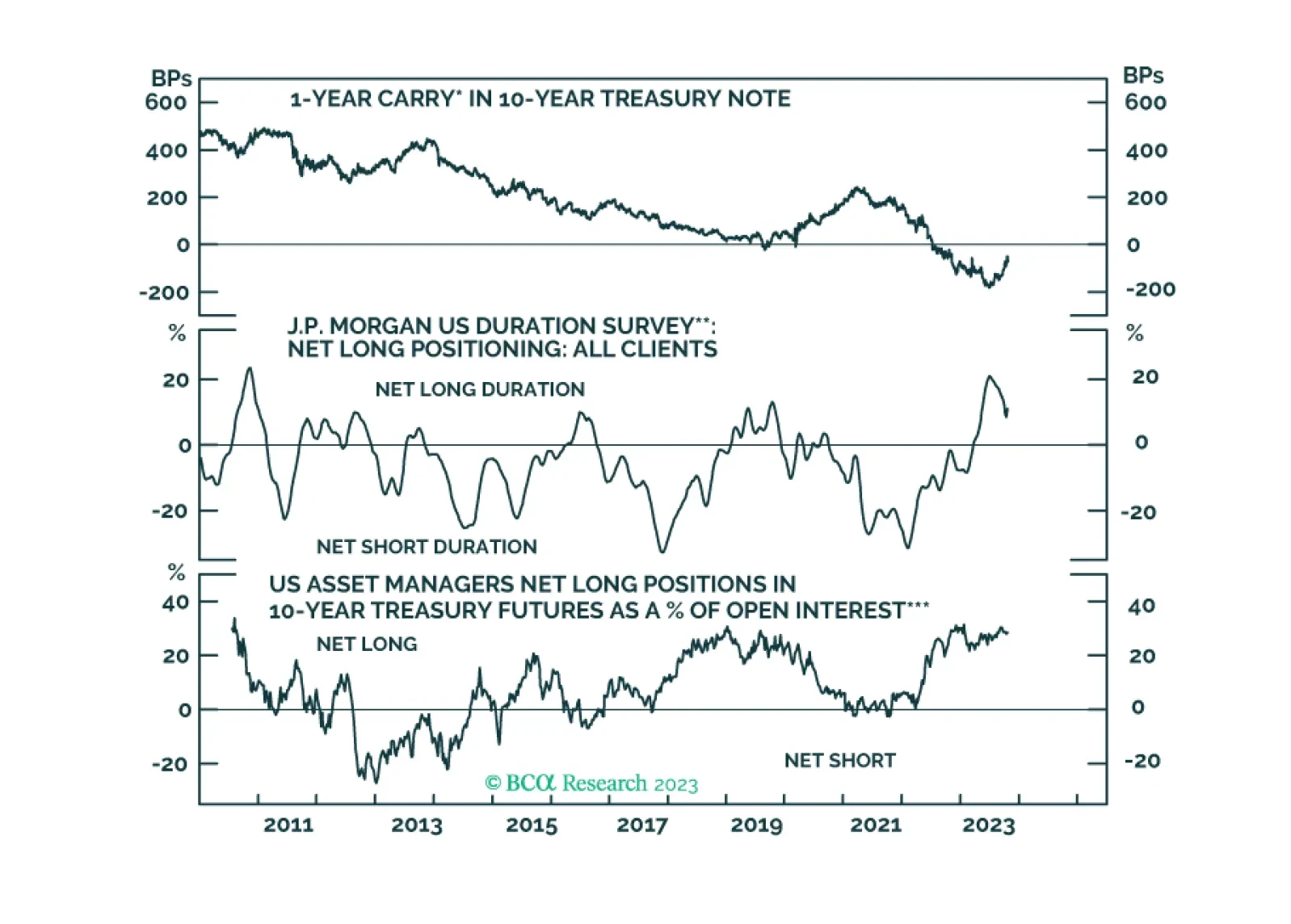

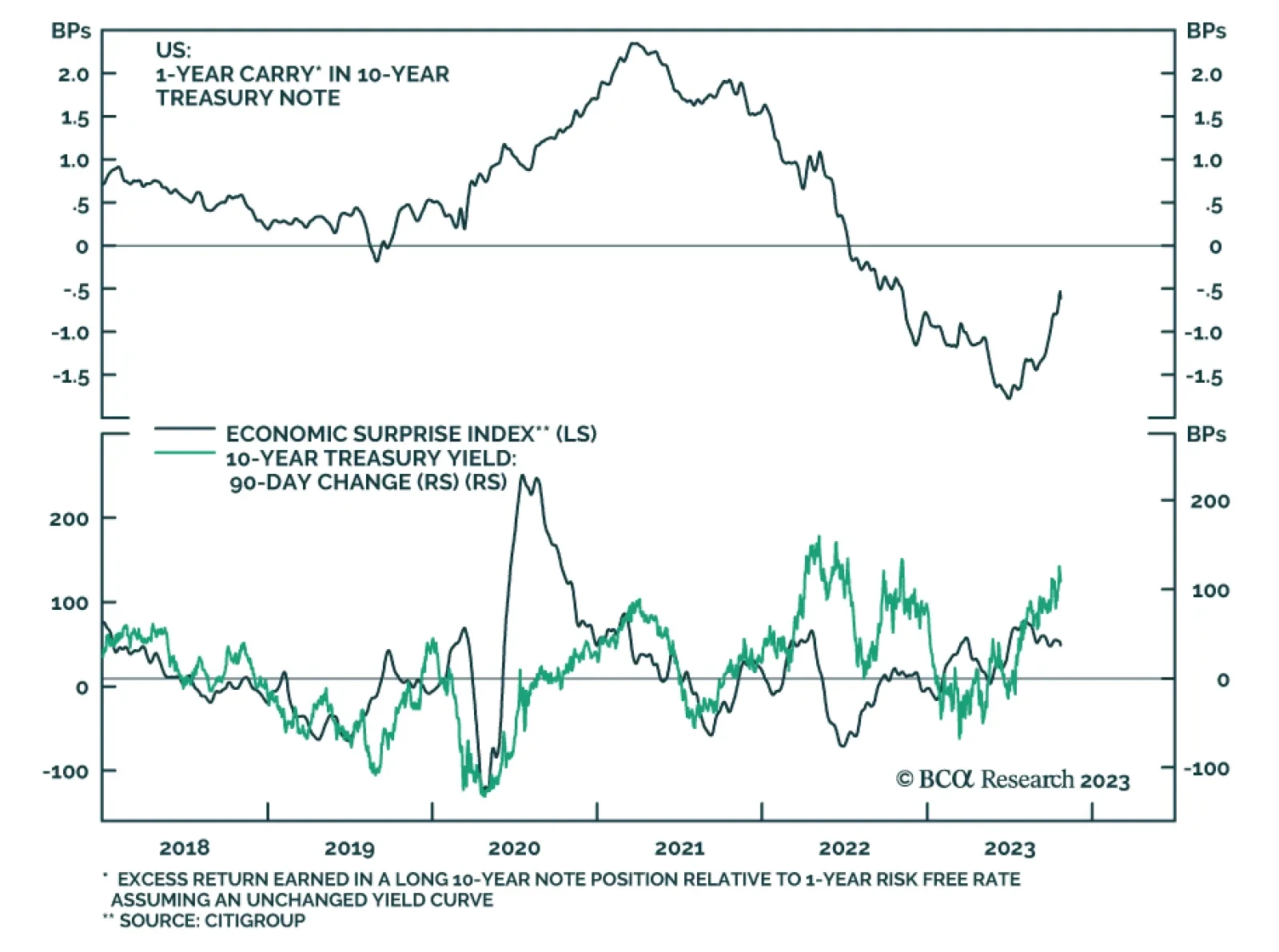

This week’s report contains an update on the Treasury curve’s recent bear-steepening trend and a look at different measures of long-maturity Treasury valuation.

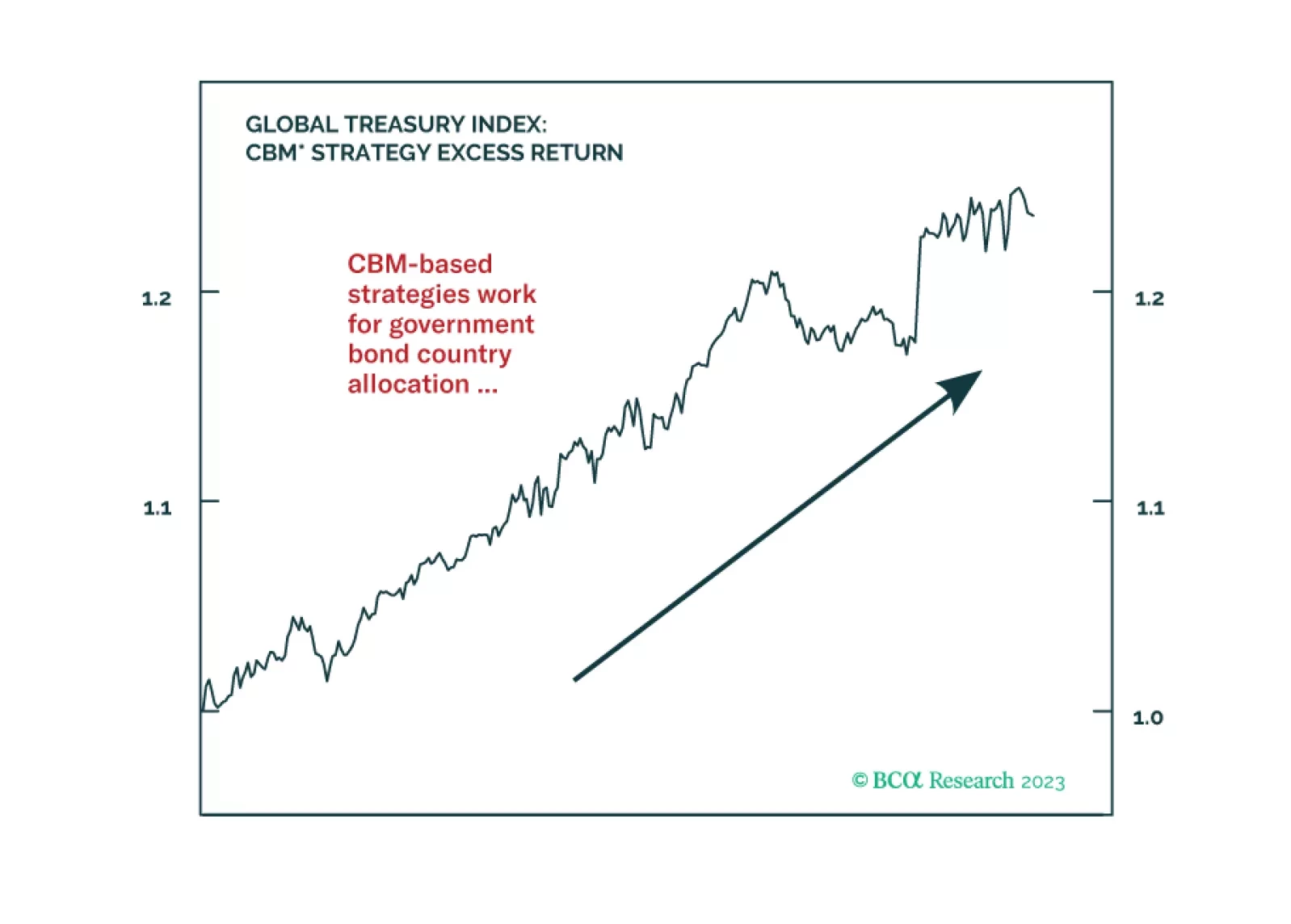

In this Special Report, we introduce two strategies that use our Central Bank Monitors for global fixed income country allocations and currency trades. We find that using the Monitors in country selection helps improve the performance of a developed markets government bond portfolio. The CBMs can also help substantially minimize the drawdowns on a standard FX carry strategy.

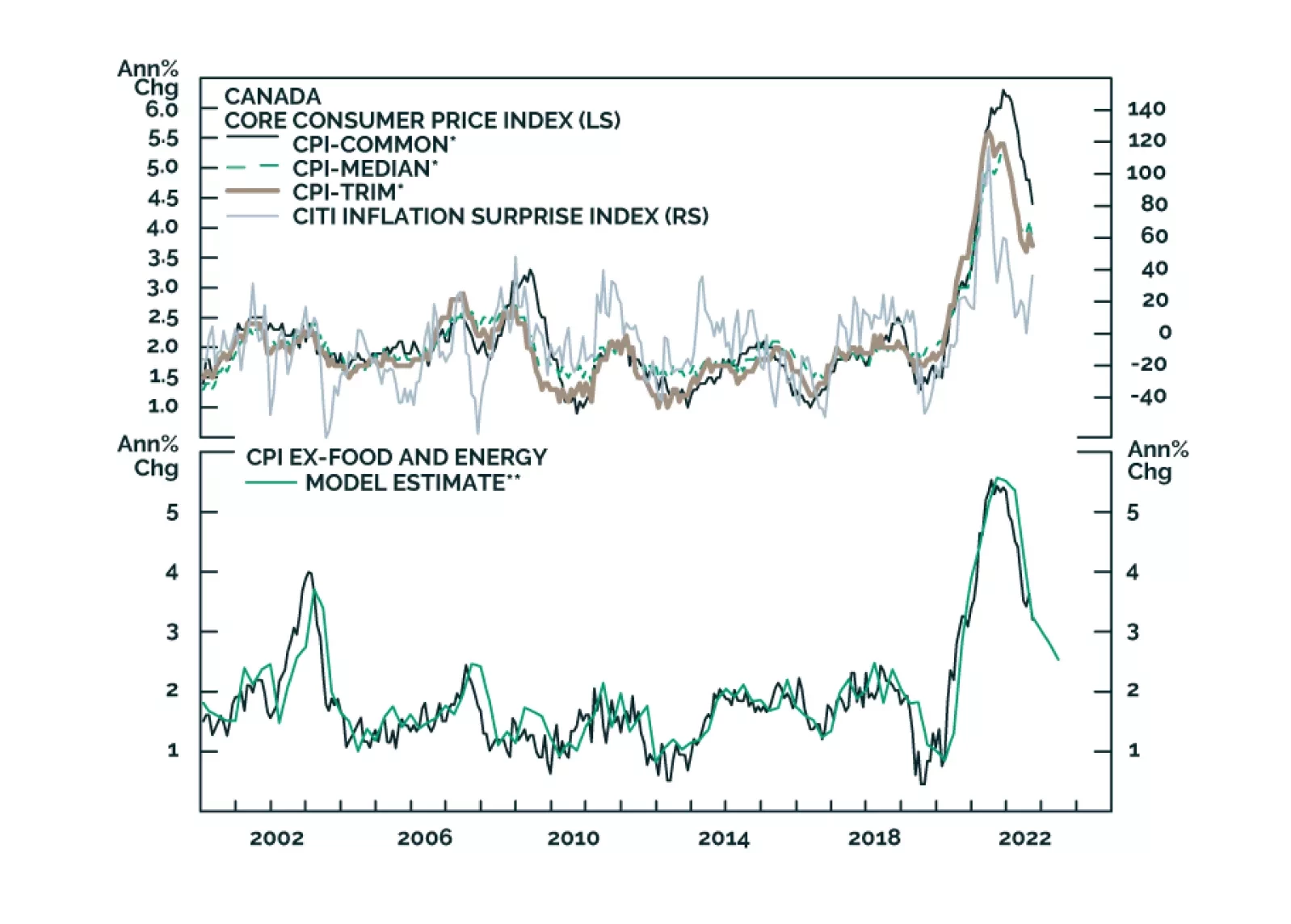

In this insight, we look at whether the recent data justifies a shift by the BoC, and some potential trades.

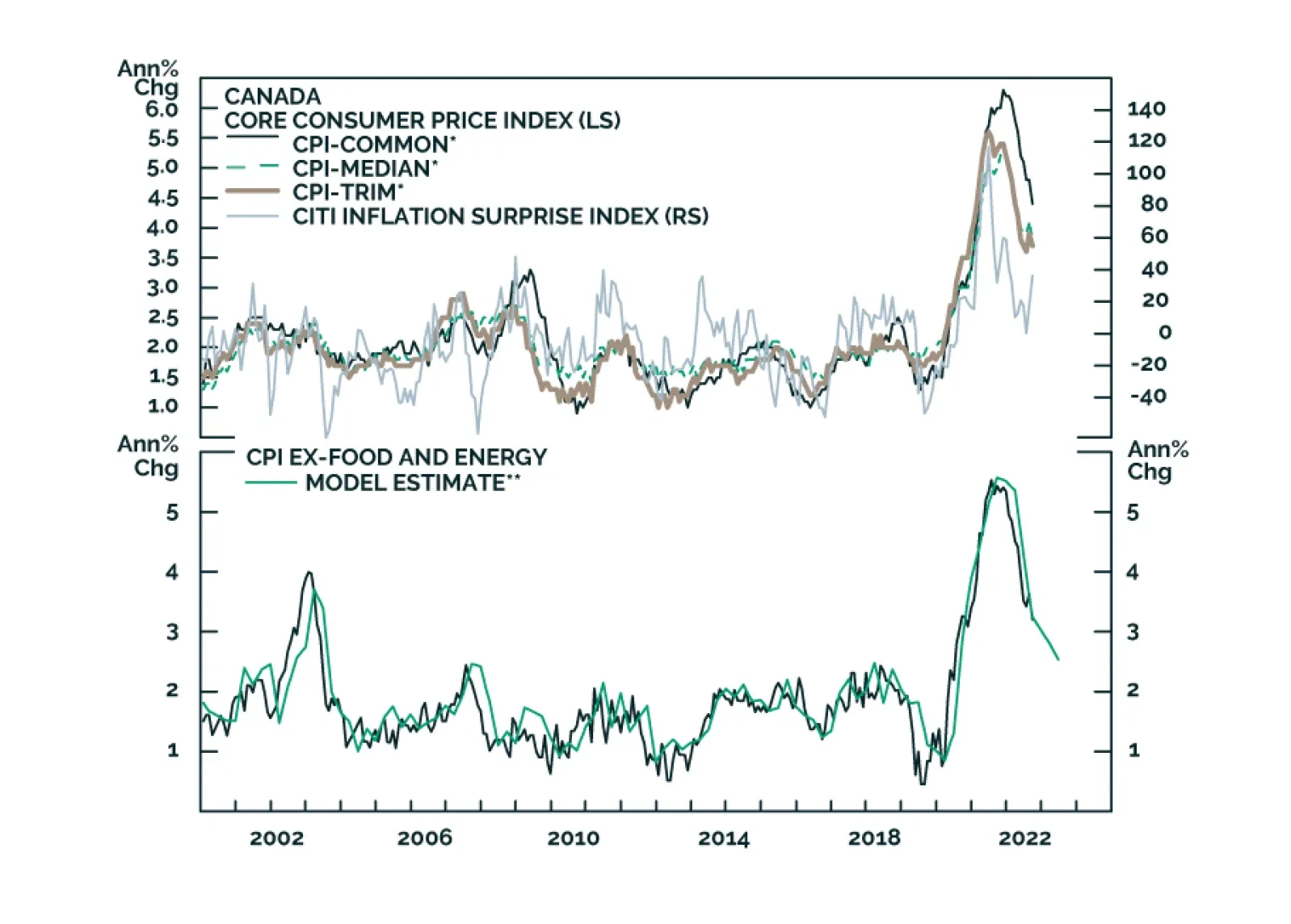

In this insight, we look at whether the recent data justifies a shift by the BoC, and some potential trades.