Developed Countries

US fiscal, monetary, and foreign policies are unlikely to deliver any dovish surprises for investors in Q4, due to the impending government shutdown, persistent inflation, and instability among OPEC+ and China.

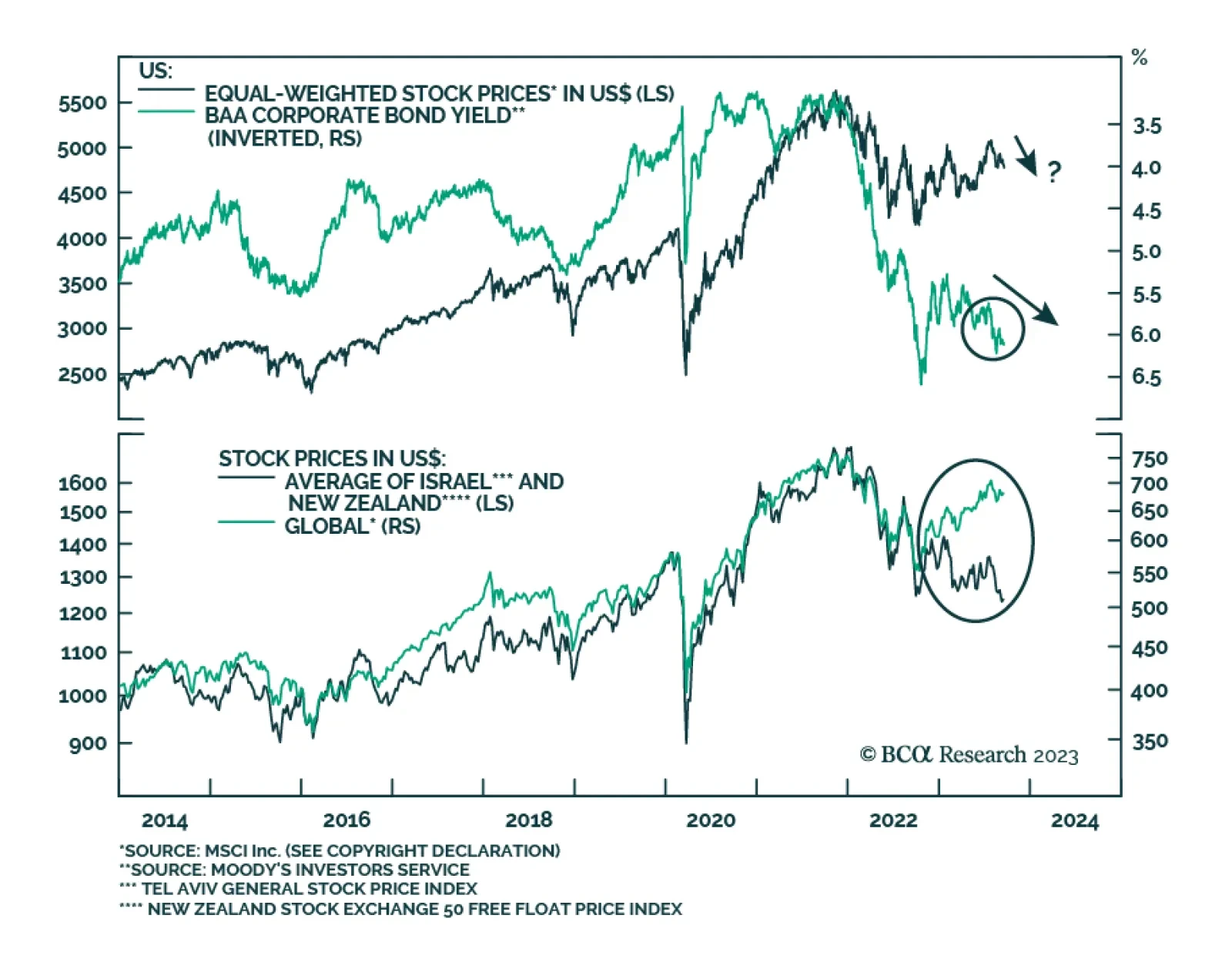

Emergency pandemic fiscal and monetary policy measures buffered households and nonfinancial corporate businesses in ways that have acted to lengthen the lags between monetary policy changes and their effect on the economy. We believe, however, the extended lags are merely delaying the recession, not cancelling it. We expect to downgrade equities on a tactical basis from equal weight to underweight soon.

The global downturn will be shallower than it was in 2008 and in 2020 but will last for longer. The primary reason for a more prolonged downturn is that policymakers in the US, Europe, and China will be reluctant to proactively and aggressively stimulate. The combination of rising oil prices, an appreciating US dollar, and mounting US bond yields constitutes a triple whammy for US share prices.

We continue to expect Brent crude to trade just above $101/bbl in 4Q23, and to average $118/bbl in 2024. Higher volatility looms. We expect Russia will cut oil production next year as part of a concerted effort to undermine Biden’s re-election. Oil-demand volatility is set to rise in response to divergent policy imperatives. We continue to favor equity exposure to oil and gas via the XOP ETF; direct exposure via the COMT ETF, and long Dec23 $100/bbl Brent calls. We are getting long Jan-Feb-Mar 2024 Brent futures vs. short the same months in 2025 expecting steeper backwardation as inventories draw and markets tighten.