Developed Countries

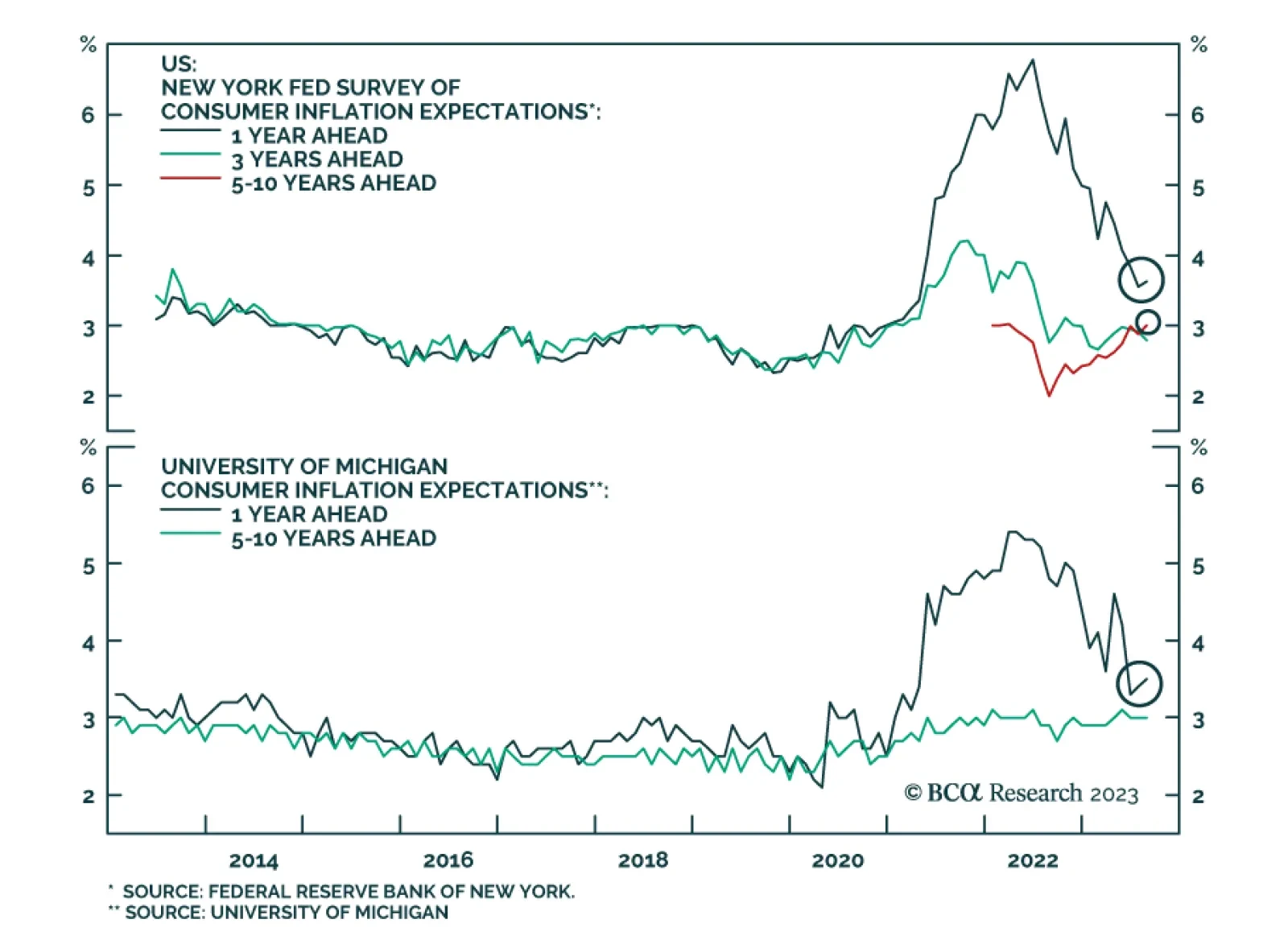

The New York Fed’s latest consumer expectations survey shows household sentiment deteriorated in August. Job loss expectations jumped, with the average perceived likelihood of losing one’s job over the coming year increasing by 2.0 percentage points to a…

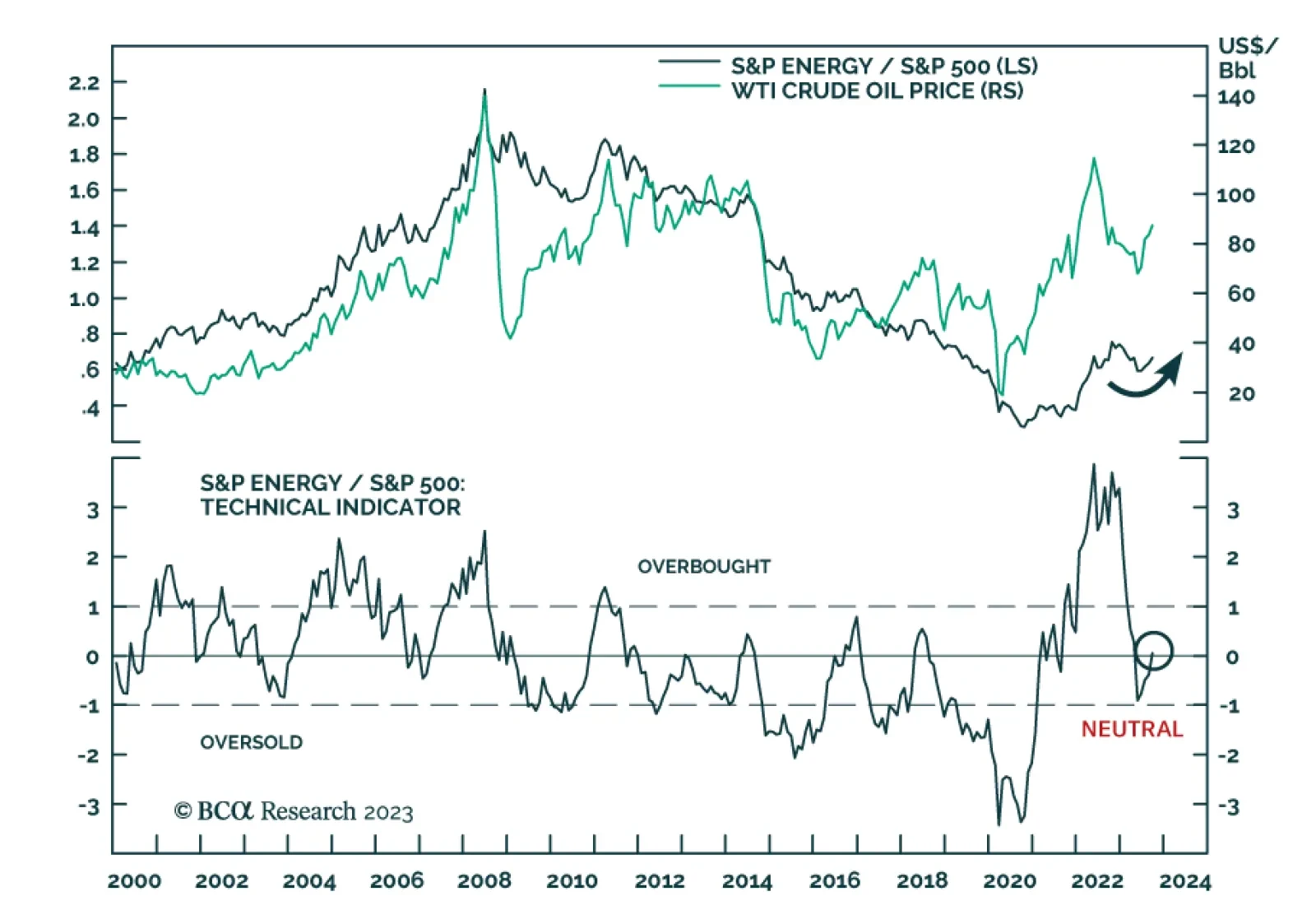

The S&P 500 Energy sector’s fortunes have recently reversed. After having been the worst performing sector in the first half of the year — losing 7.3% versus the S&P 500’s 15.9% gain — Energy is now leading all other US equity sectors. Energy stocks…

Our colleagues at BCA’s US Investment Strategy service have been excess savings bulls since cash began silting up on household balance sheets as transfer payments flowed from the Capitol to Main Street while High Street businesses were shuttered. Excess…

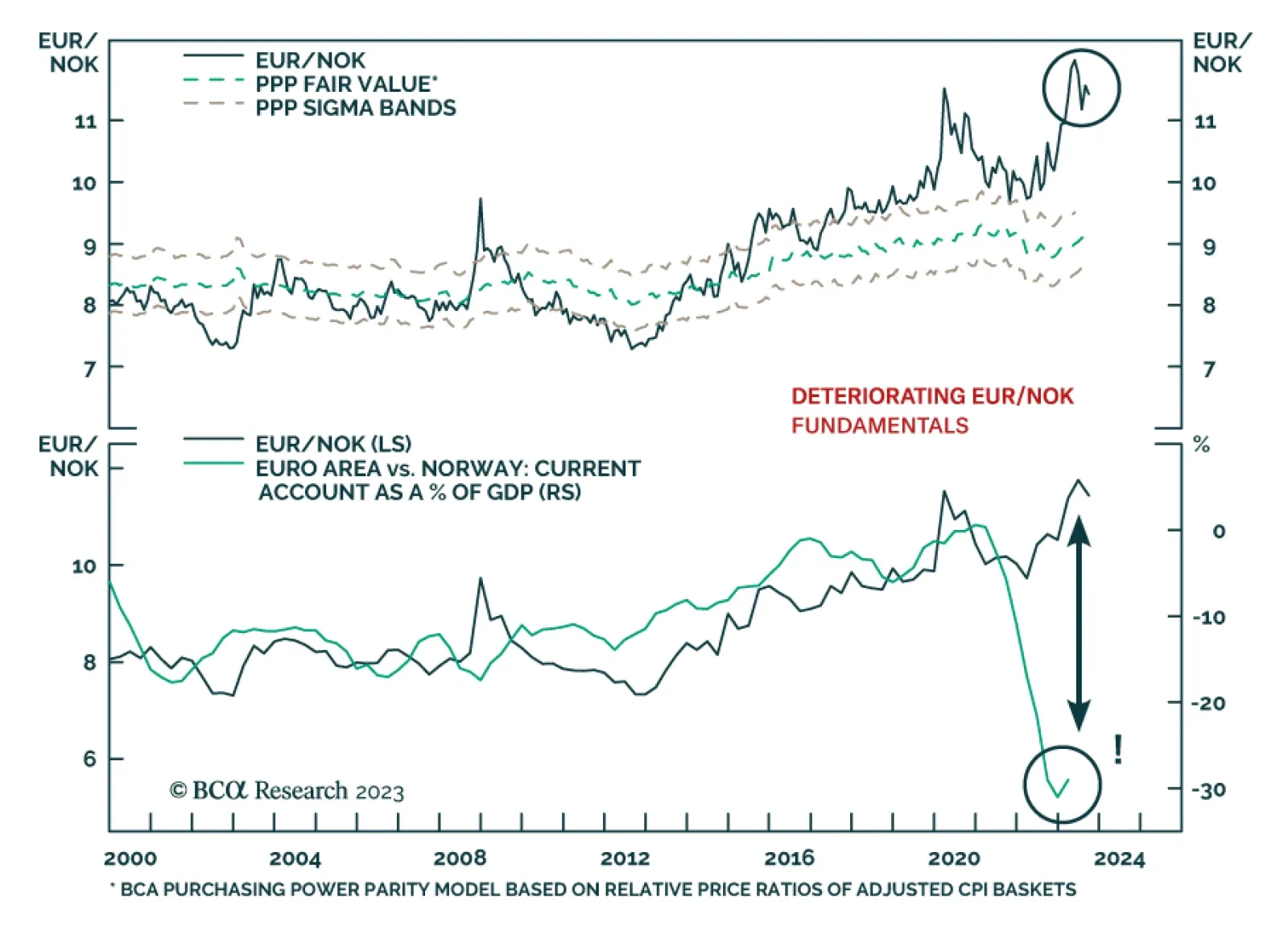

According to BCA Research’s European Investment Strategy service, valuations, interest rate differentials, and higher oil prices favor the NOK over the EUR. Higher oil prices, especially when they reflect tightening supply, act as a risk to the euro. This…

Stocks perform worse in presidential election years than average years, especially in the first half of the year, and especially if the ruling party ends up falling from power. Investors should take risk off the table until the unemployment rate peaks.

The euro has weakened sharply since mid-July as US growth continues to outperform that of the Eurozone. Is a new bear market afoot for the common currency?

Magnificent Seven leadership is neither a new nor an unnatural phenomenon. There is no shortage of reasons why equities might have already made a top, but investors should not be tricked into thinking that the rally was somehow specious.

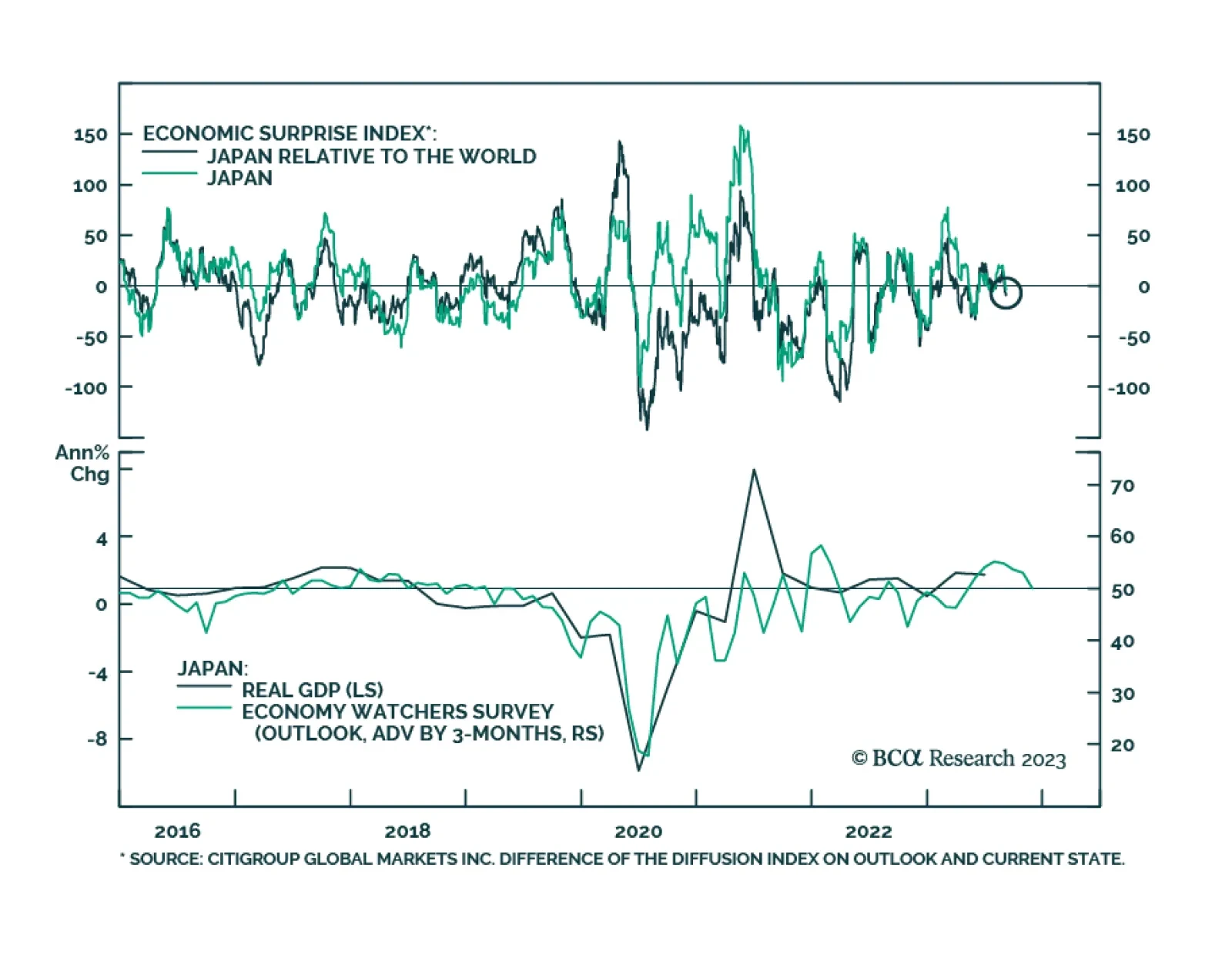

Japanese economic data delivered a negative surprise on Friday. Q2 GDP growth was revised down from 1.5% q/q to 1.2% q/q, below expectations of 1.4% q/q. The downwards revision reflects a 1% q/q decline in business spending (down from the preliminary…

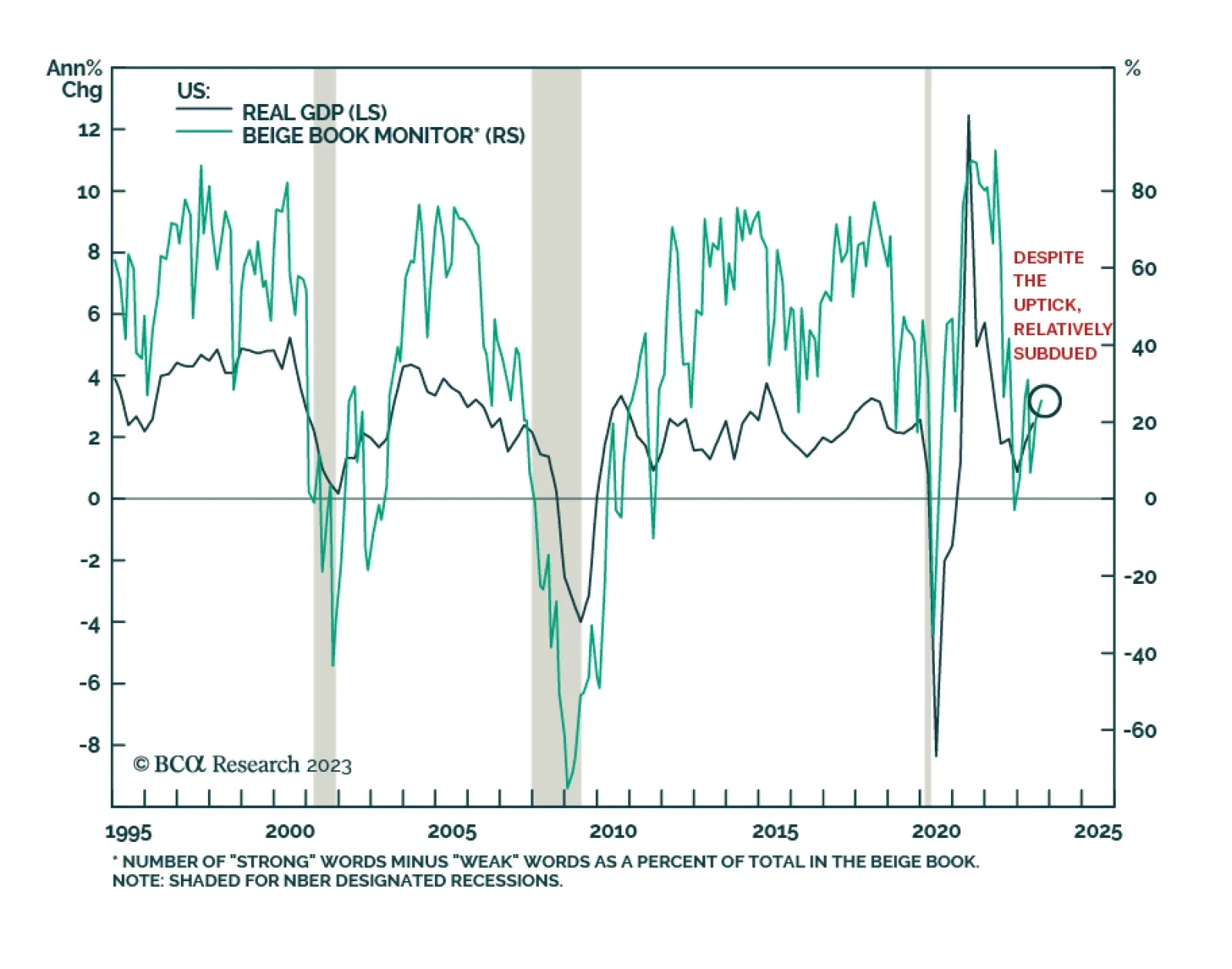

Overall, the Fed’s latest Beige Book provided a pessimistic assessment of the US economy. Although the report characterized tourism spending as “stronger than expected,” it also noted that pent-up demand for leisure travel has now likely been satisfied and…

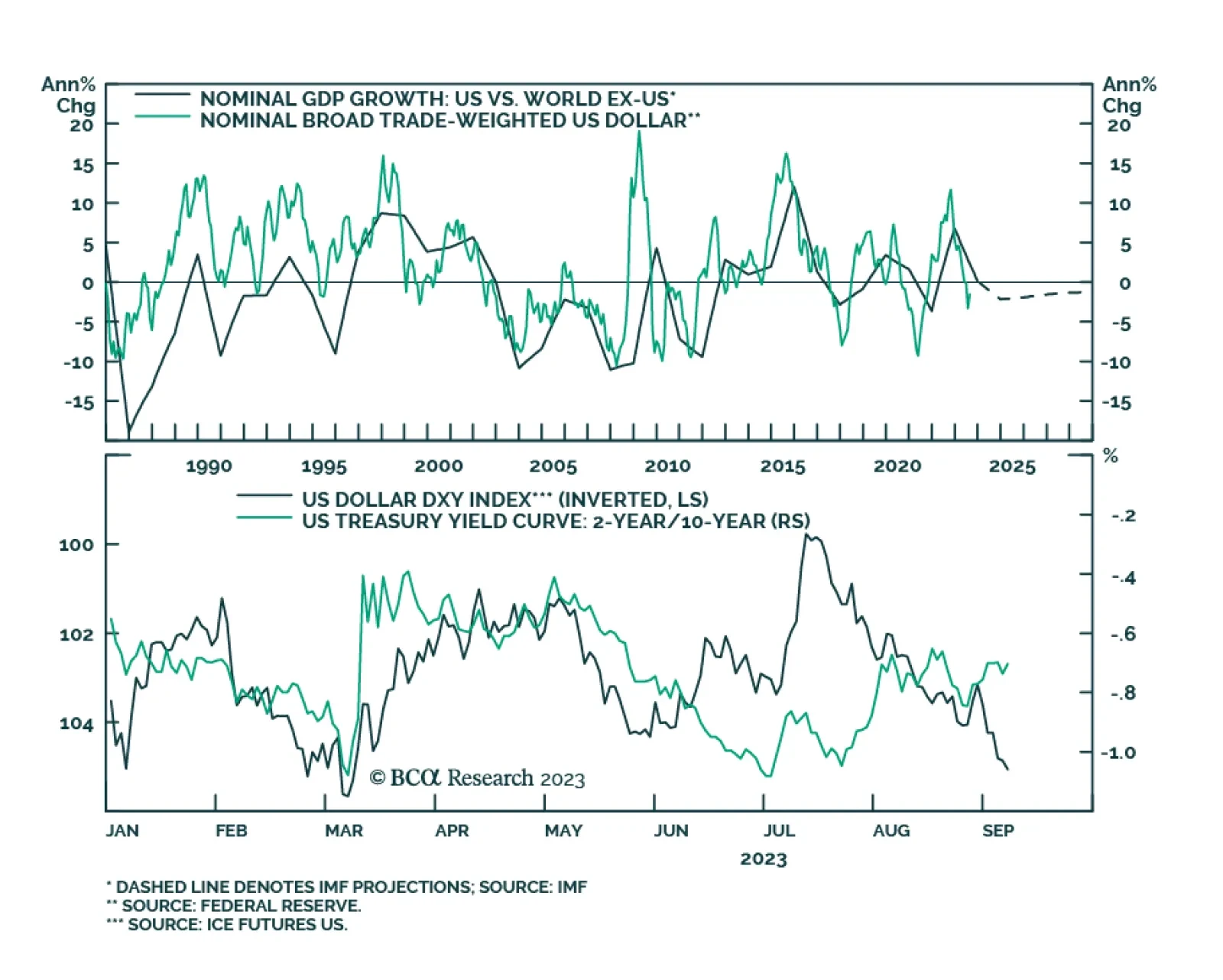

According to BCA Research’s Foreign Exchange Strategy service, the counter-trend bounce in the dollar will continue. Factually, the trend in the dollar has depended on both global growth dynamics and the relative health of the US economy. From higher…