Developed Countries

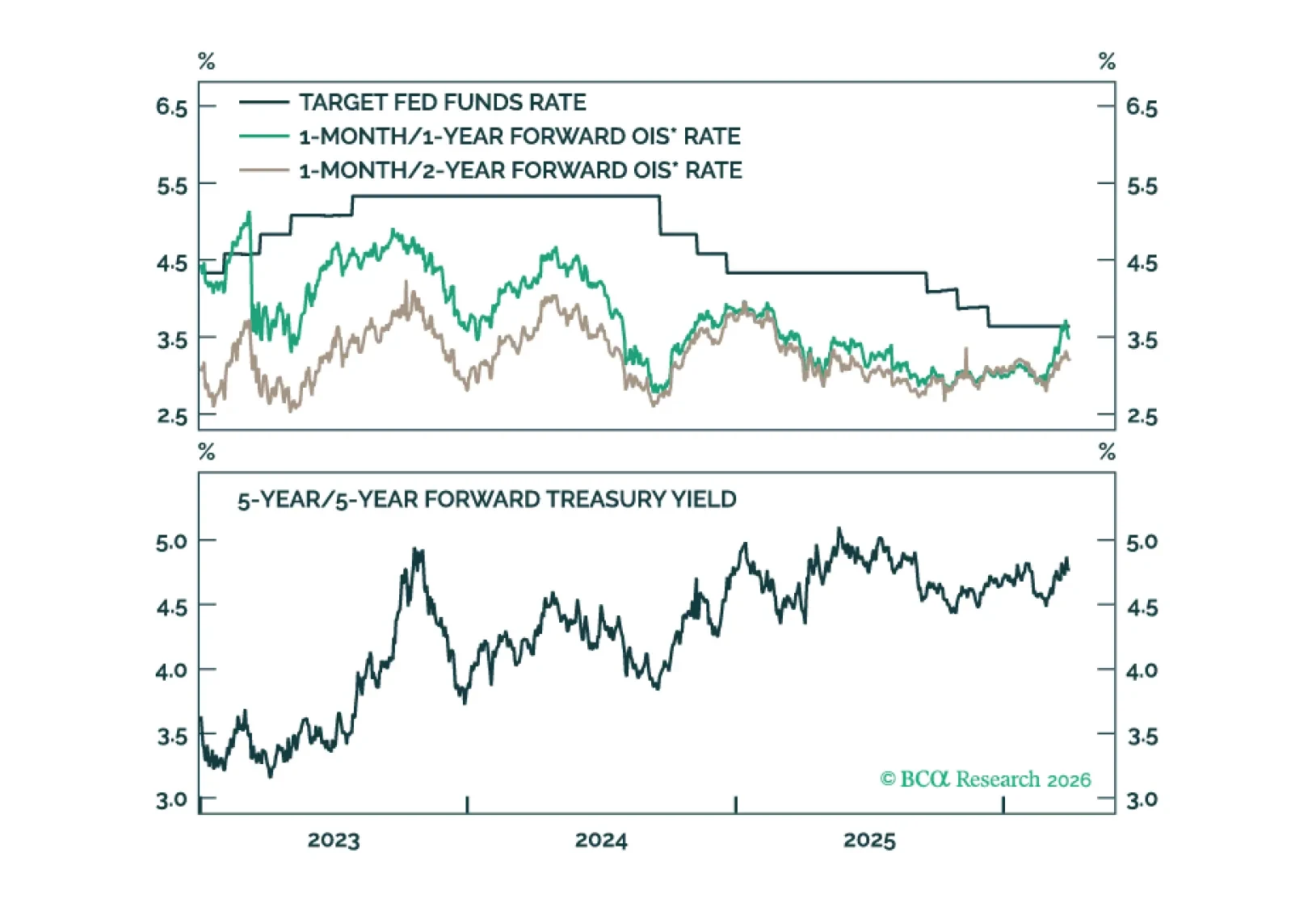

With central banks largely on hold, the return of a lower volatility environment is bringing carry trades back into focus. We outline the most attractive carry opportunities across global fixed income markets.

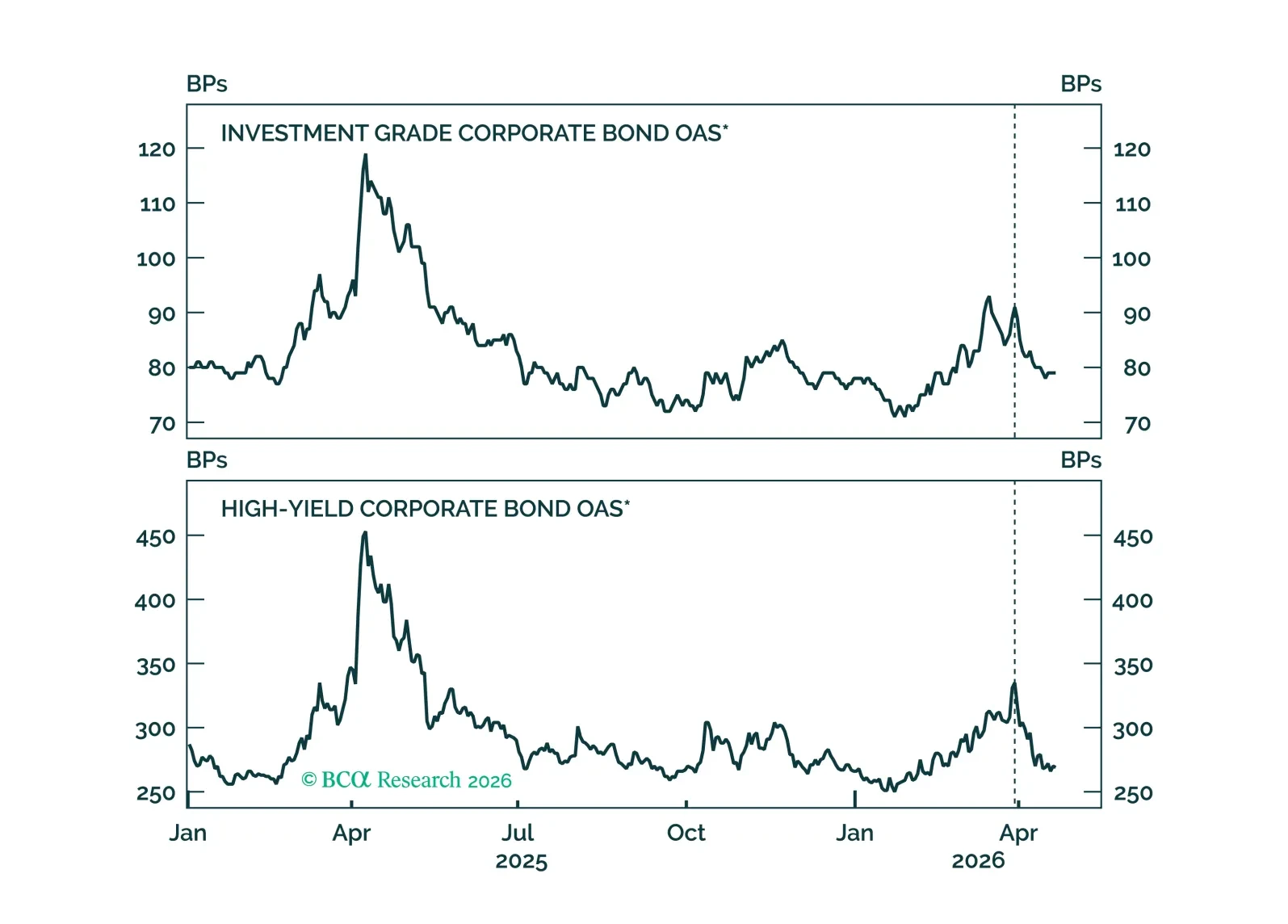

We recommend increasing exposure to spread product as the US economy transitions back into a low rate vol regime.

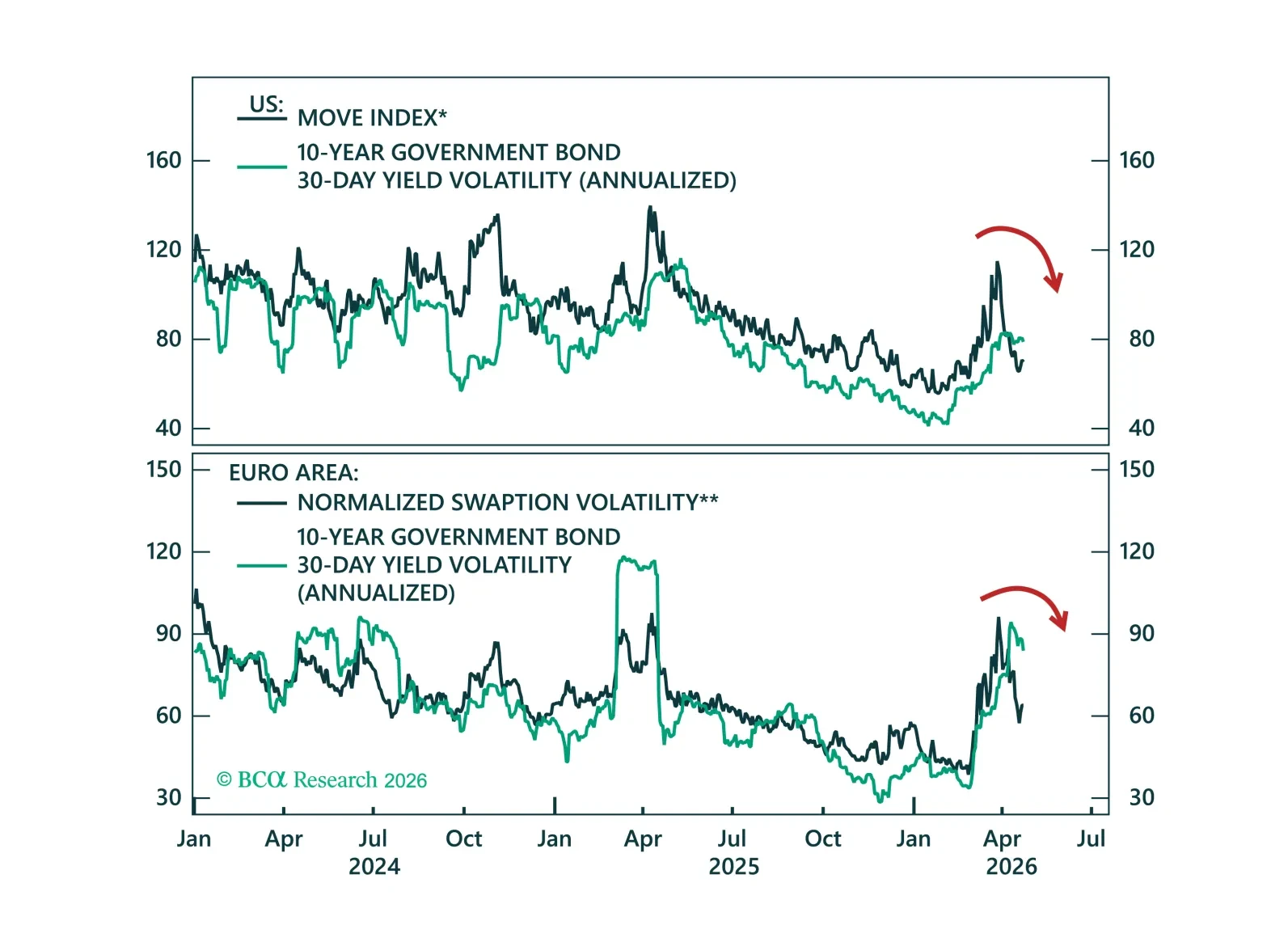

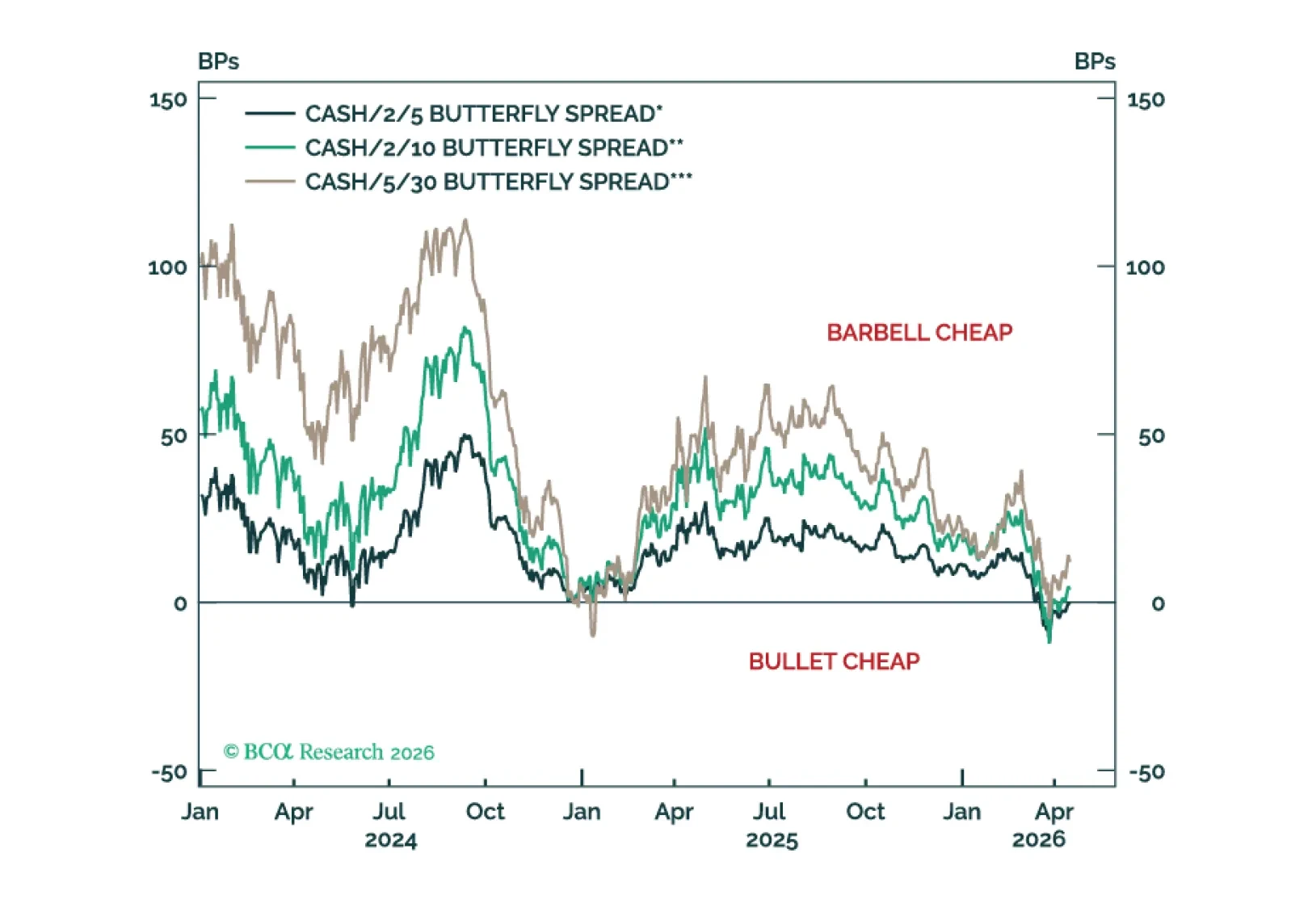

The rates market is moving back into a low vol regime, but with yields at a higher level. This argues for maximizing carry across the Treasury curve.

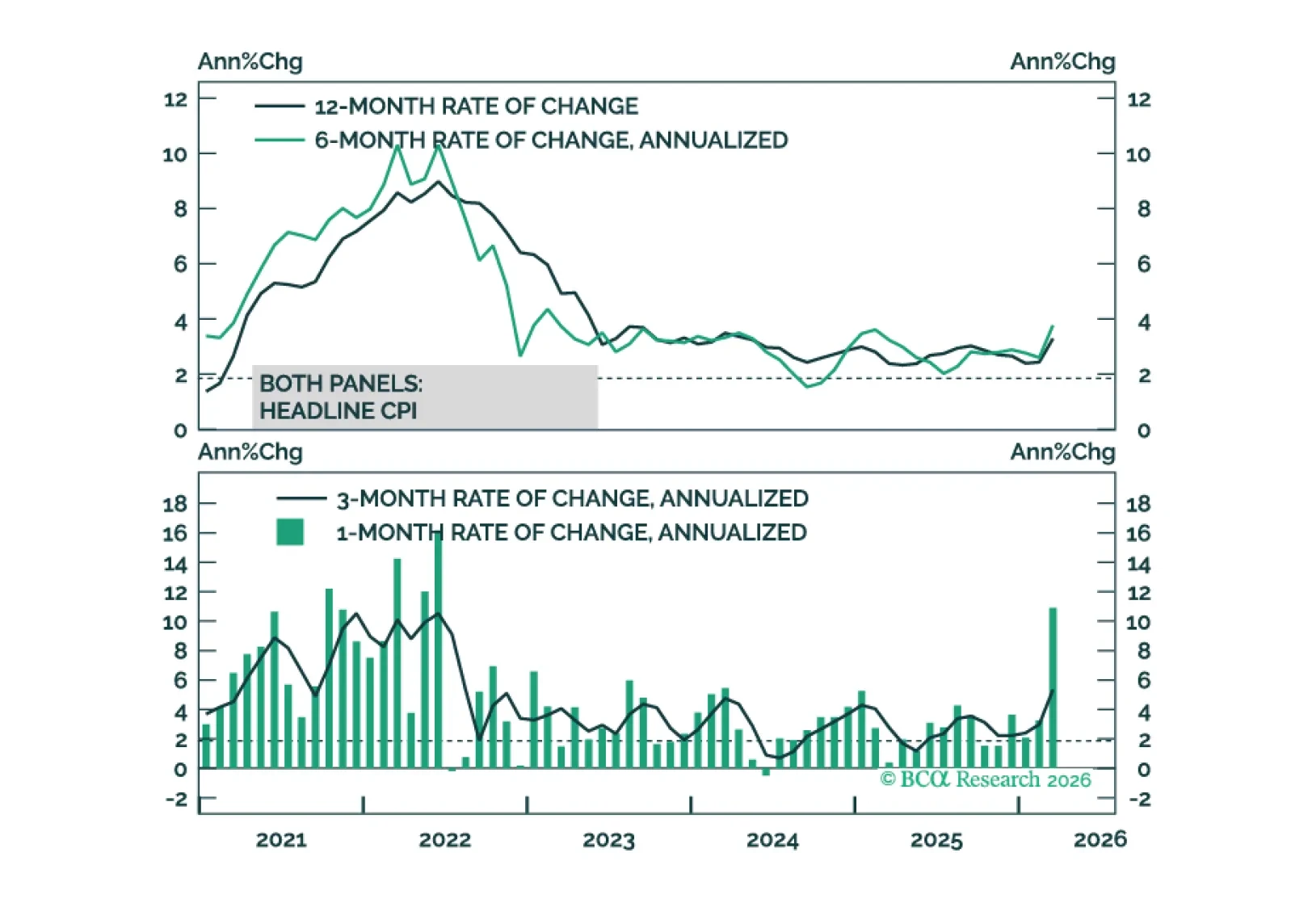

Inflation’s underlying trend was headed lower prior to the Iran war. This makes the recent back-up in bond yields look like an attractive buying opportunity.

The relief rally in stocks can continue a while longer. However, much can still go wrong. As such, we are retaining a 12-month underweight to stocks but are moving to neutral on a short-term tactical horizon.

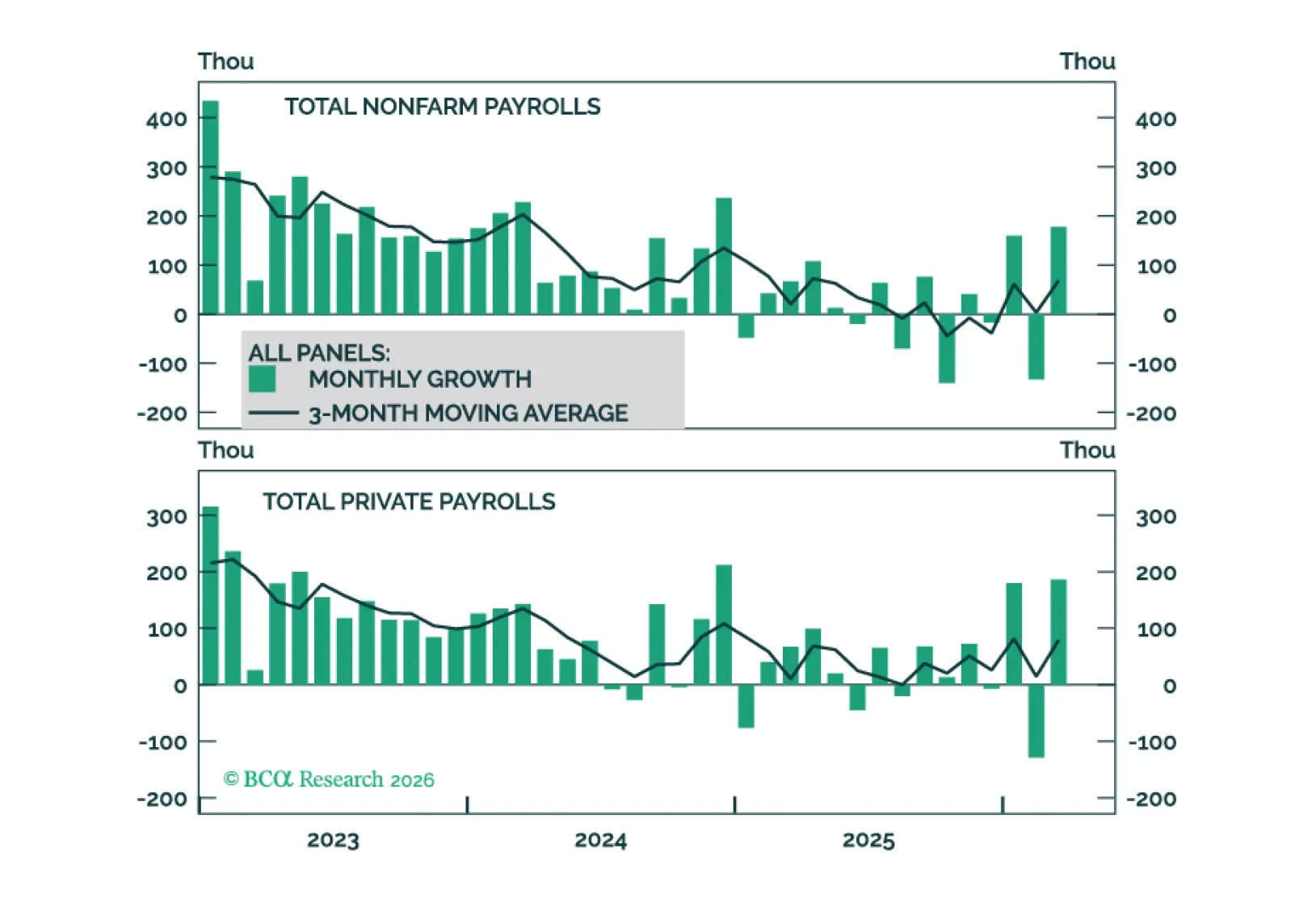

US employment data show some tentative signs of job growth acceleration and stable utilization. We see breakeven monthly job growth as closer to +30k per month than zero.

Our Portfolio Allocation Summary for April 2026.

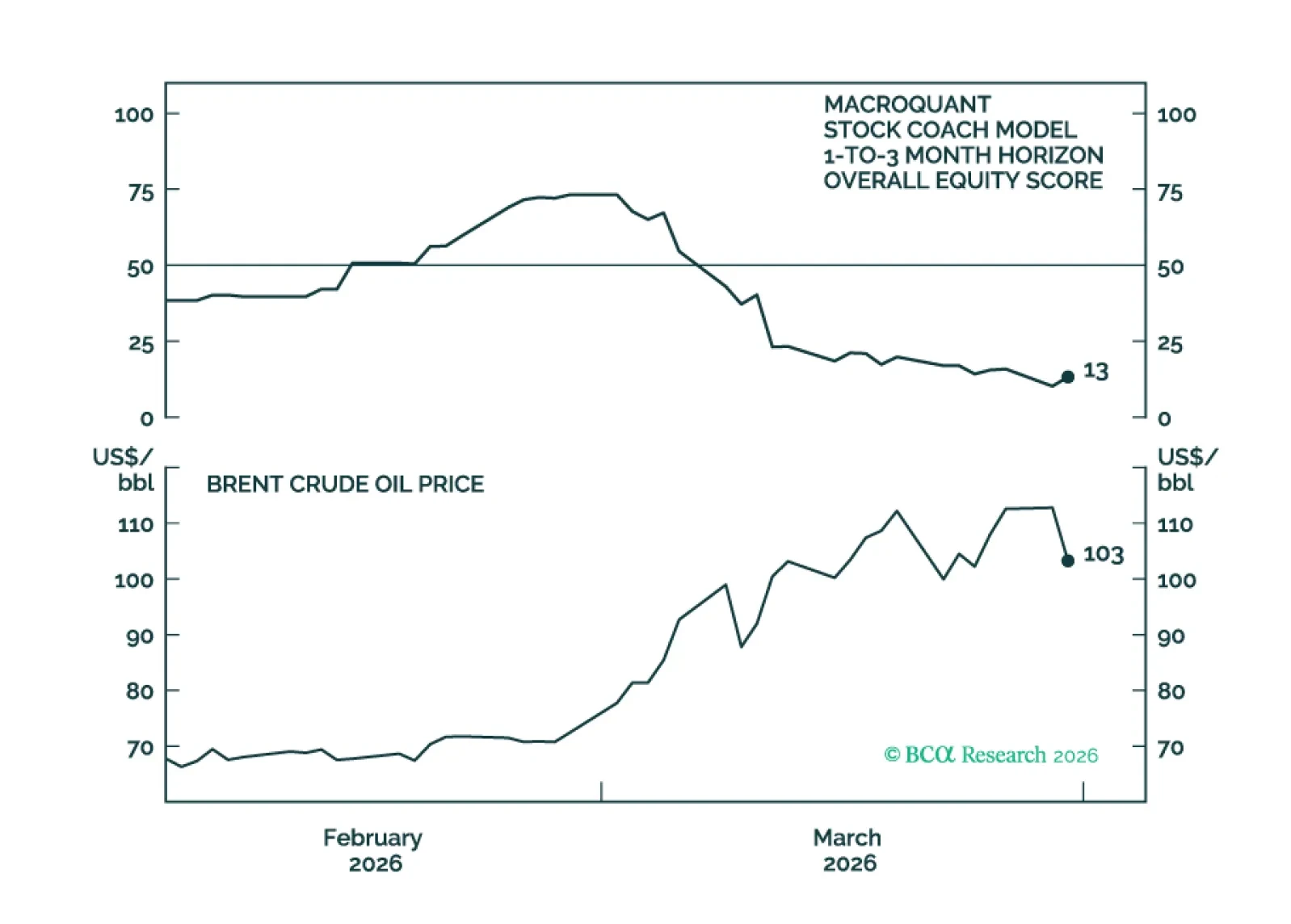

MacroQuant recommends a strong underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, has become neutral-to-slightly positive on the US dollar, has downgraded gold to neutral and copper to a strong underweight, and is bullish on oil.

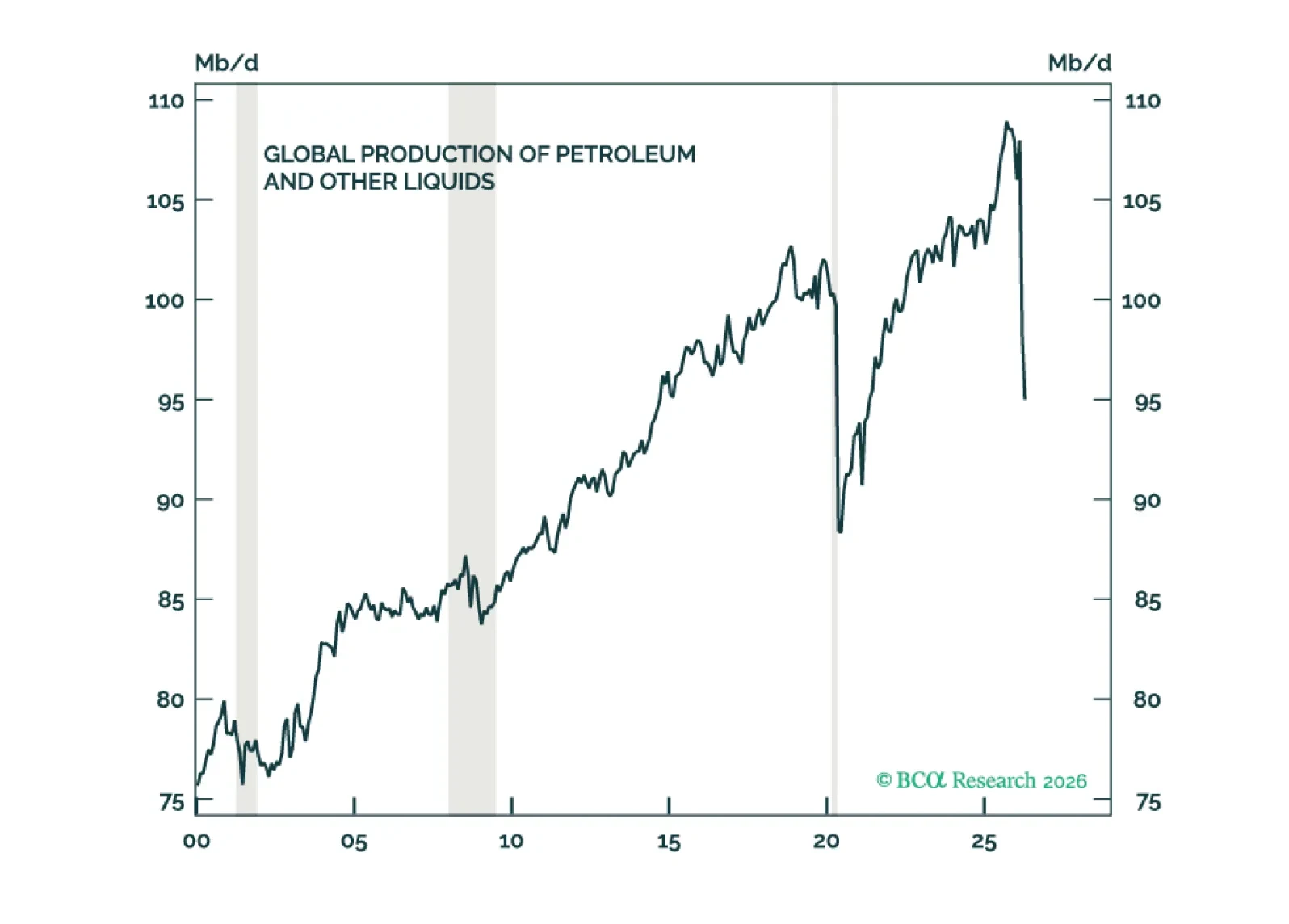

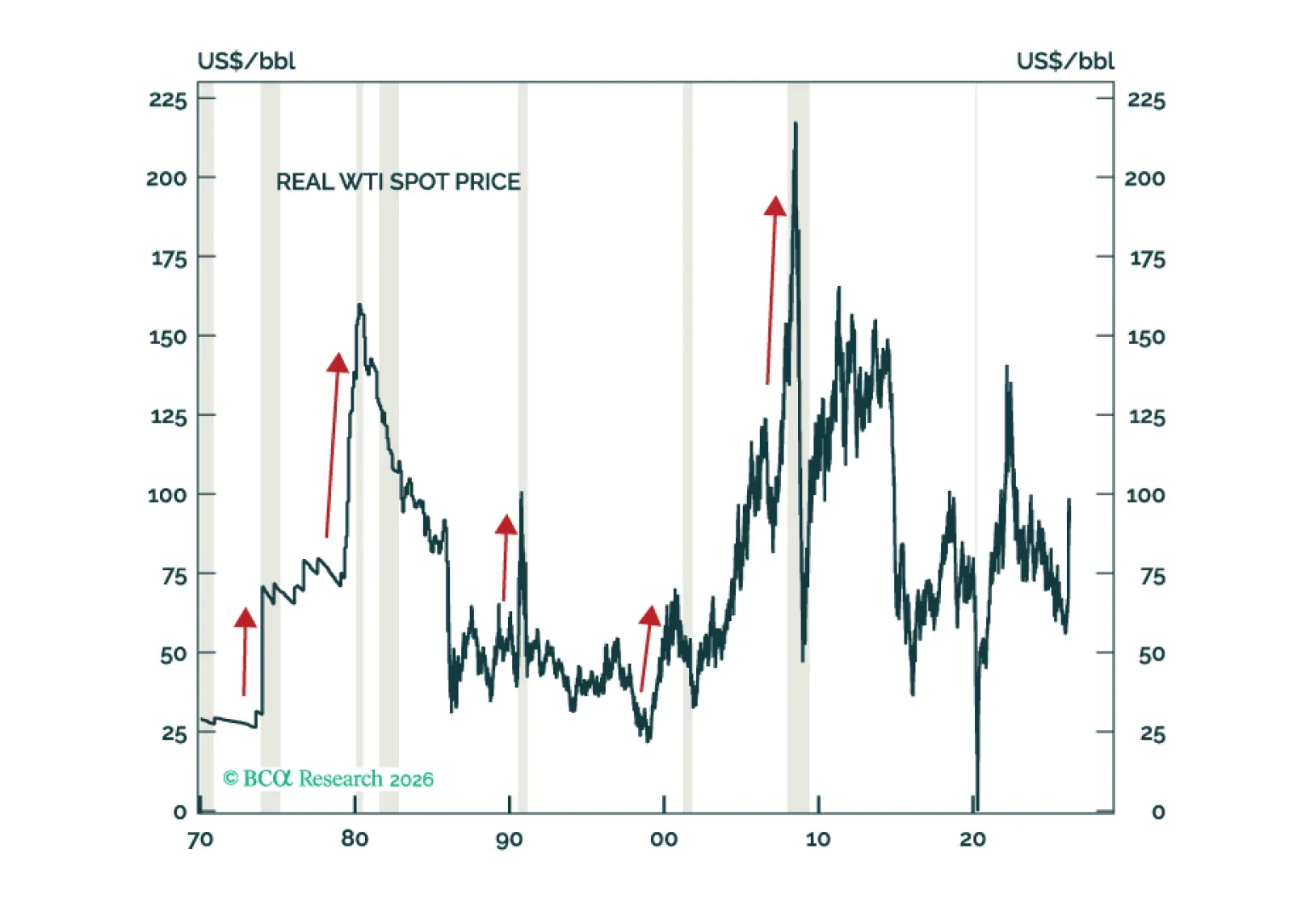

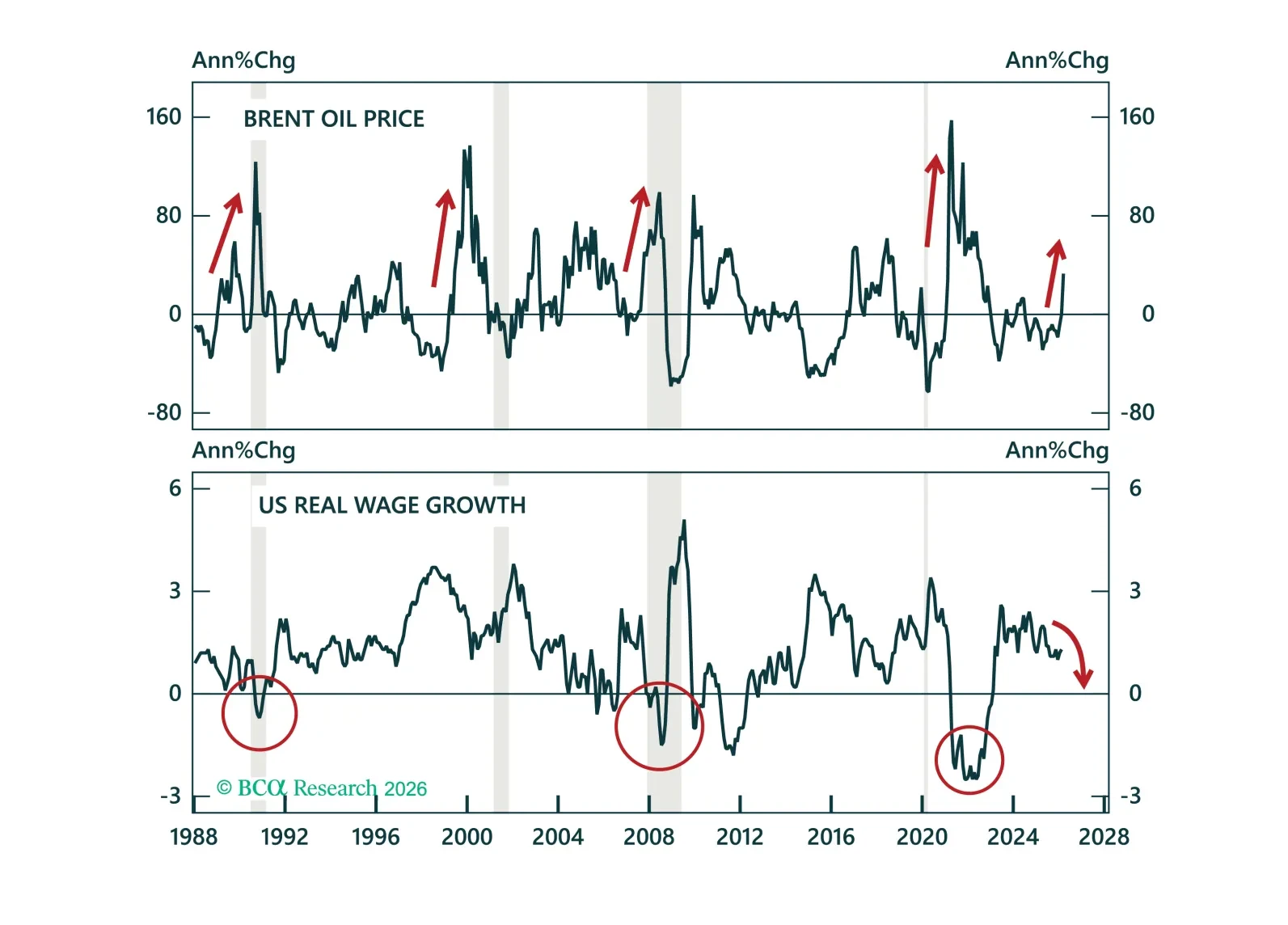

The current macro environment is a toxic brew of many of the same vulnerabilities that haunted the global economy in the lead-up to past recessions: Rising oil prices, an unsustainable tech capex boom, elevated equity valuations, excessively high homes prices, and brewing stresses in private credit and other parts of the financial system. While global equities look increasingly oversold in the very near term, they will still finish the year below current levels.

In today’s Strategy Insight, we show why both a quick resolution and a prolonged crisis ultimately point to lower yields.