Developed Countries

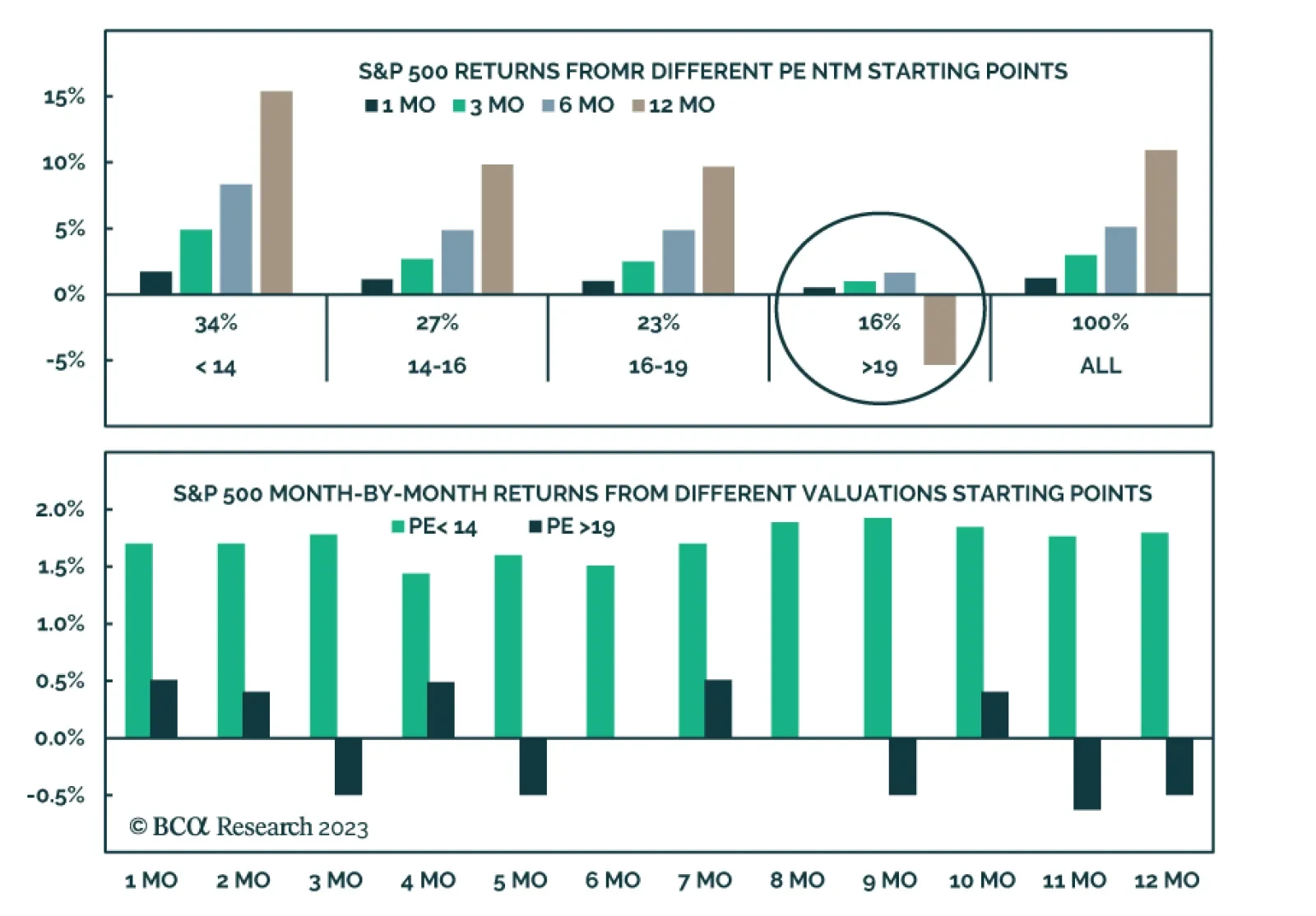

Investors should prepare for an equity market pullback this fall, prefer Treasuries over stocks, and US defensives over cyclicals. A pullback could also morph into another bear market given that monetary policy is tight, policy uncertainty will spike, global growth is slowing, and geopolitical risks are still high.

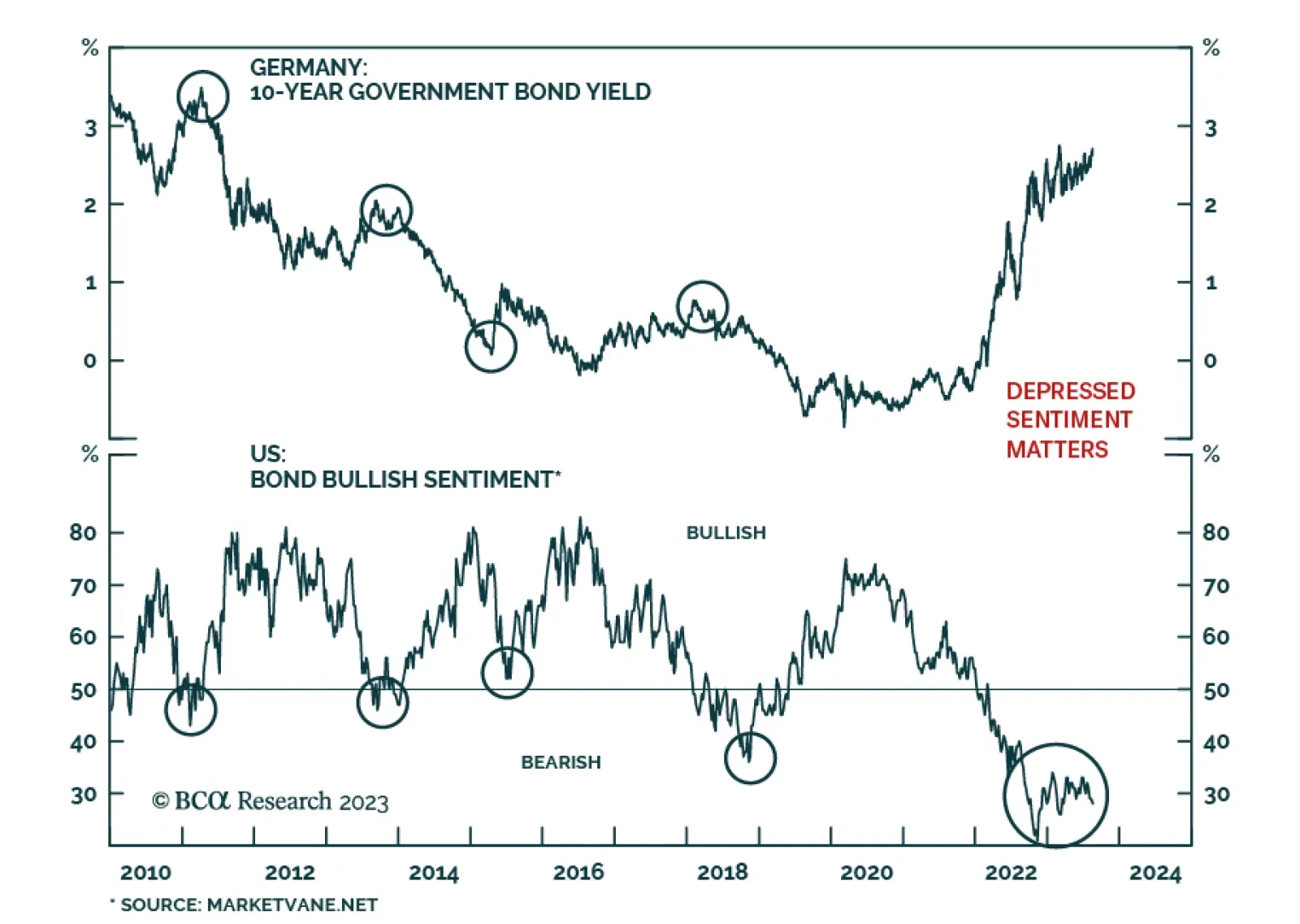

European yields are testing the upper end of their recent trading range. Is the European economic outlook consistent with an imminent breakout?

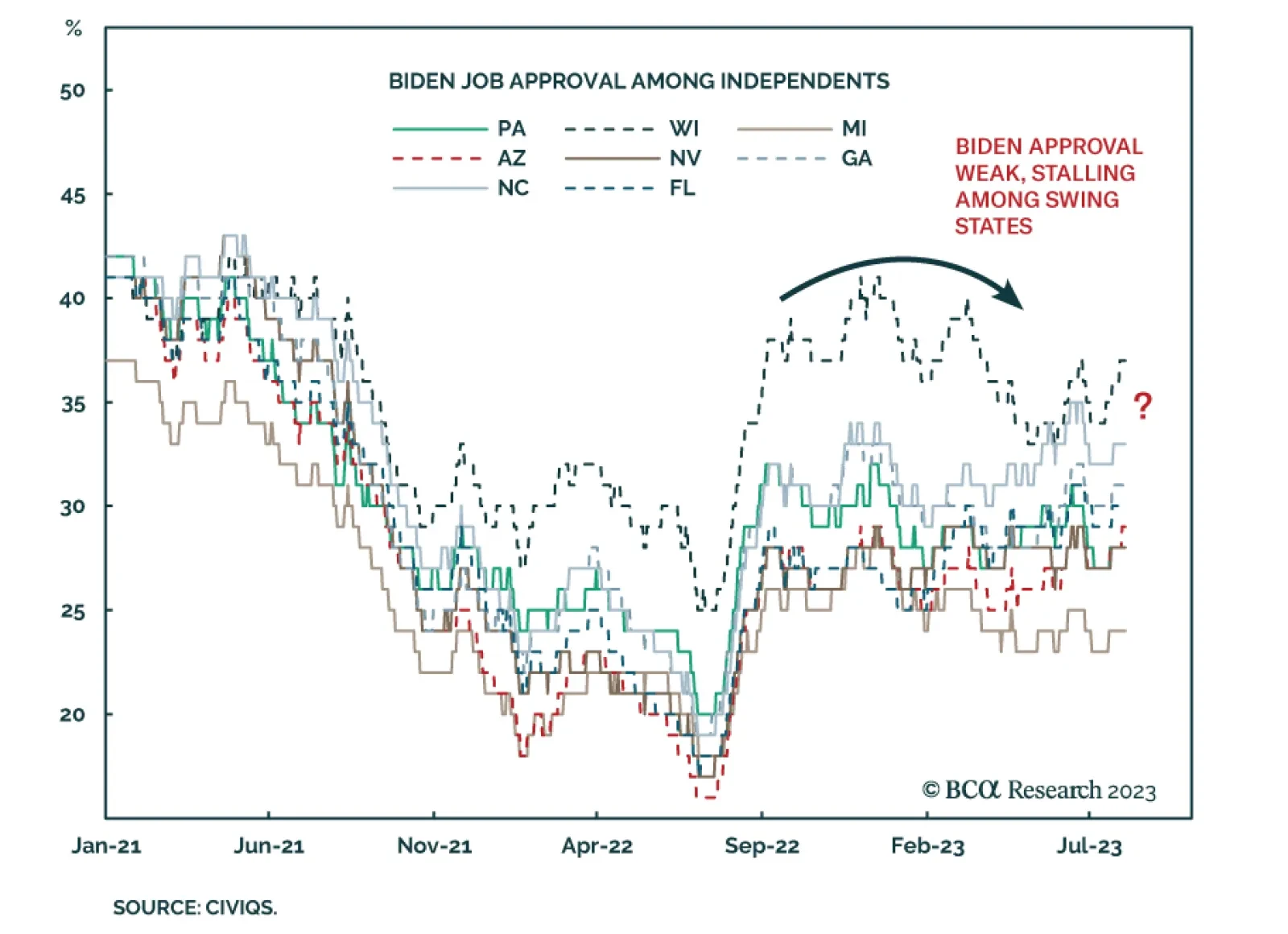

The next six-to-nine months hold a crucial test of whether the equity market will ratify the soft landing and the Biden administration or not. If so, then markets will rally on policy continuity and likely gridlock. If not, then markets will struggle until the election is over and again in 2025-26.