Developed Countries

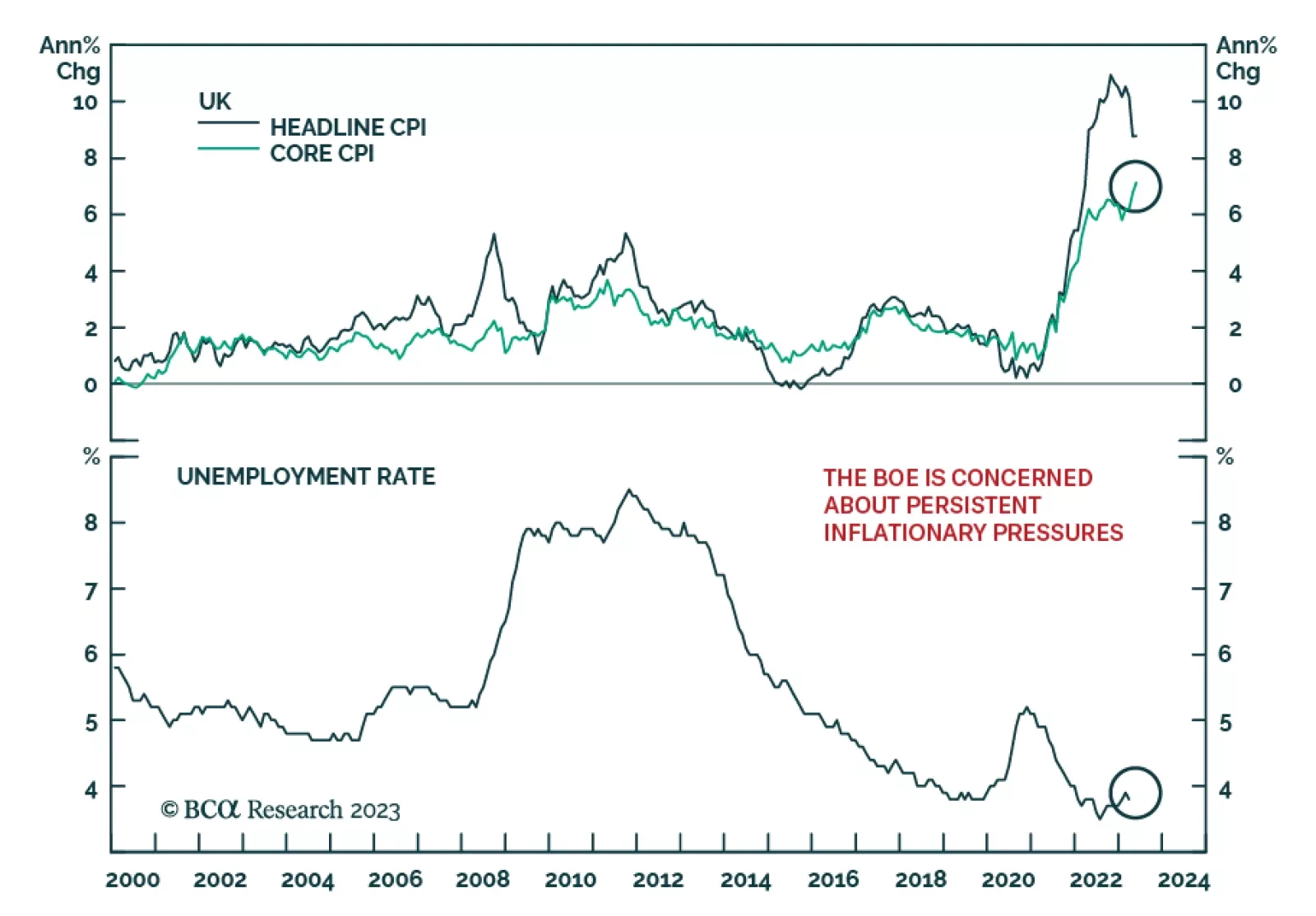

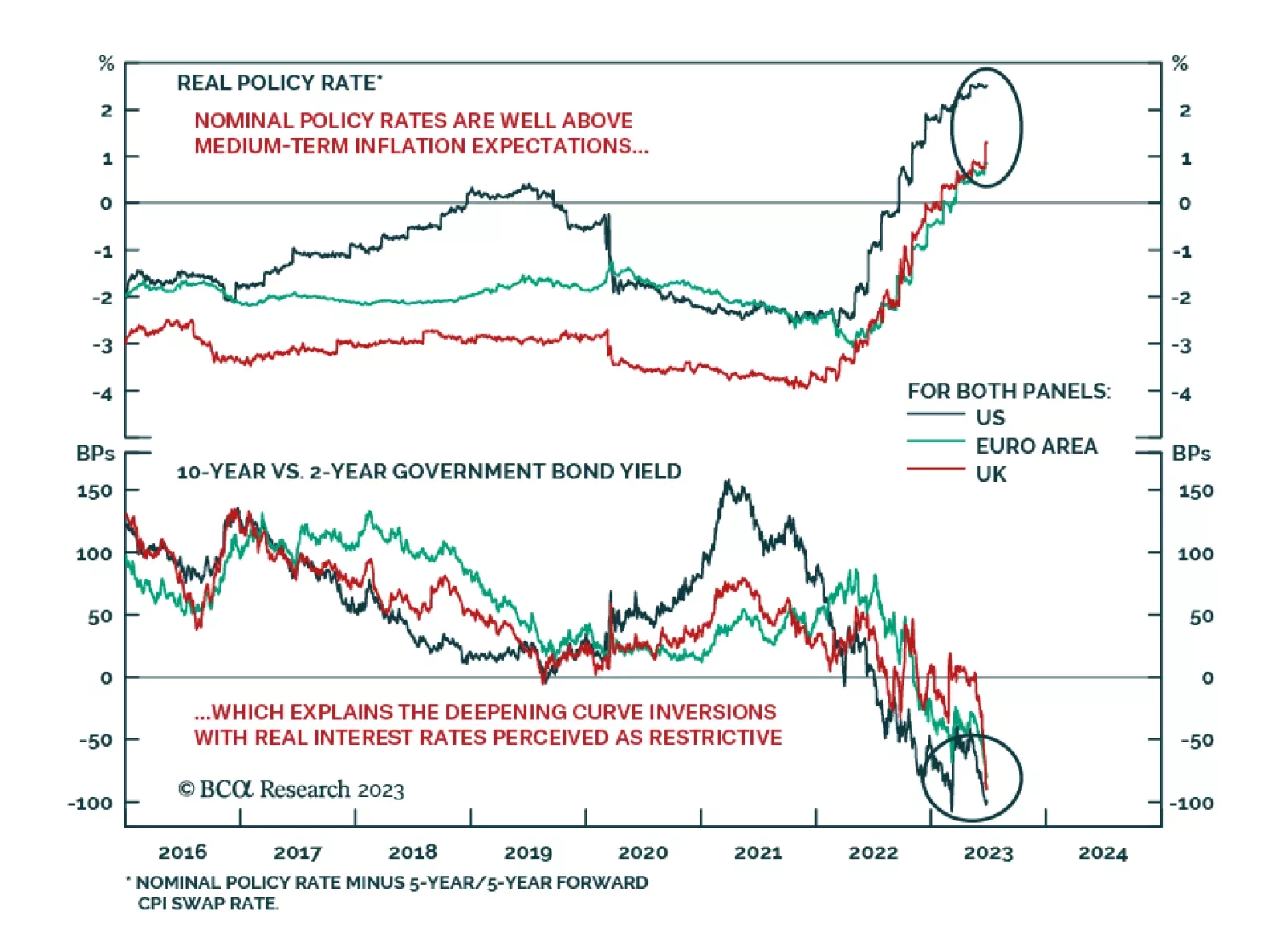

The market does not grasp the implied depths of recessions that will be needed to prevent inflation expectations from un-anchoring. Among the major economies, the most vulnerable to a deep recession is the UK. We explain why, and some investment implications. Plus: the yen is a rebound candidate, while Japanese equities are a reversal candidate.

This week’s Special Report updates our US default rate forecast and considers whether corporate bond spreads offer value given the trend in credit fundamentals. We also consider the relative value proposition between investment grade and high-yield credit and between European and US corporate bonds.

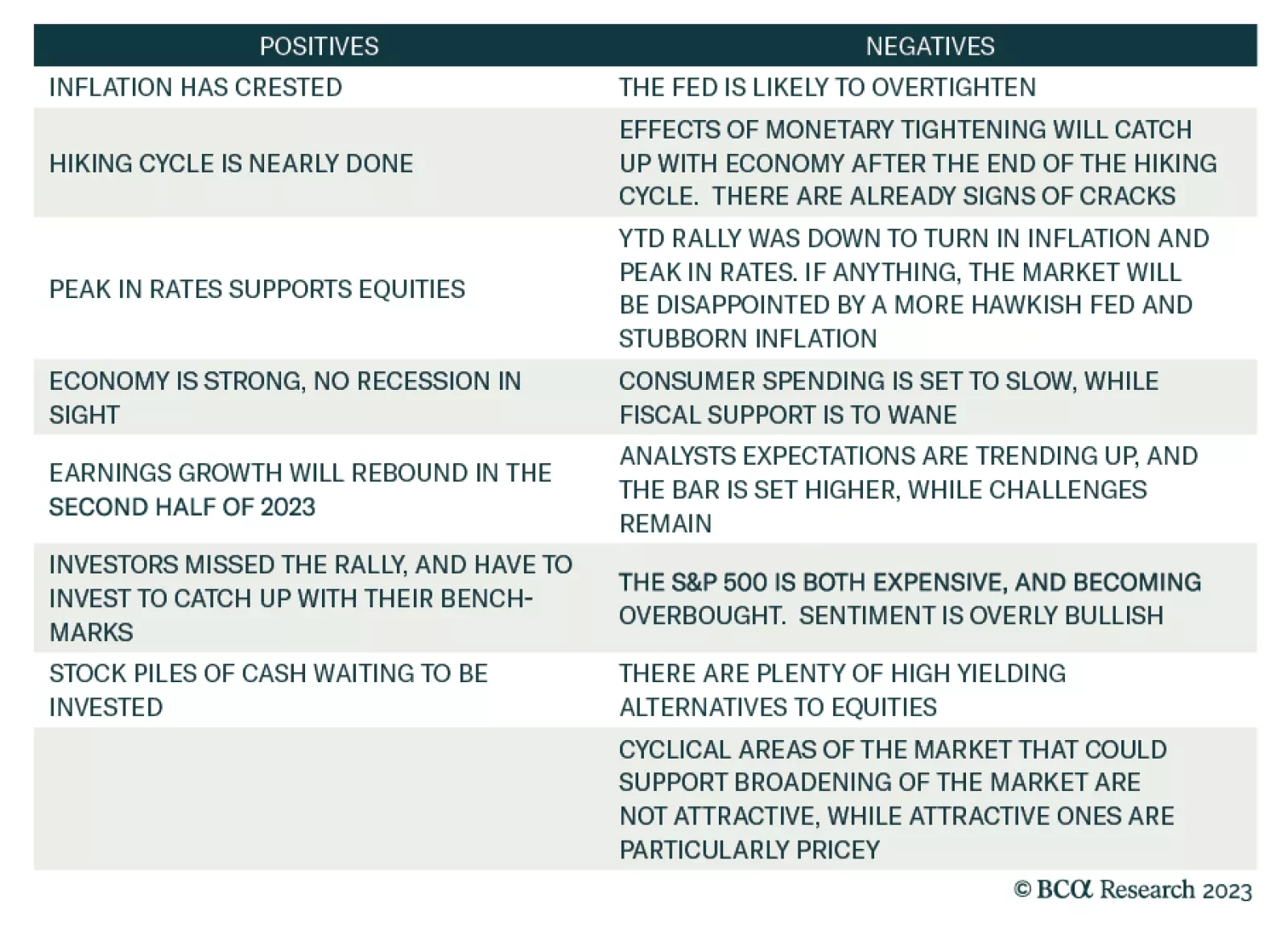

Momentum, high cash balances, FOMO, and expectations of soft landing drive the market higher. This rally may continue for a while, but macroeconomic headwinds are intensifying and will eventually derail the rally. It is too early to celebrate victory.

Talks of a détente are premature and there is no domestic political basis in China or the US to support a true détente. Investors should not underappreciate global risk, on the basis of a détente, and should avoid Greater China equities in the next 18 months.