Developed Countries

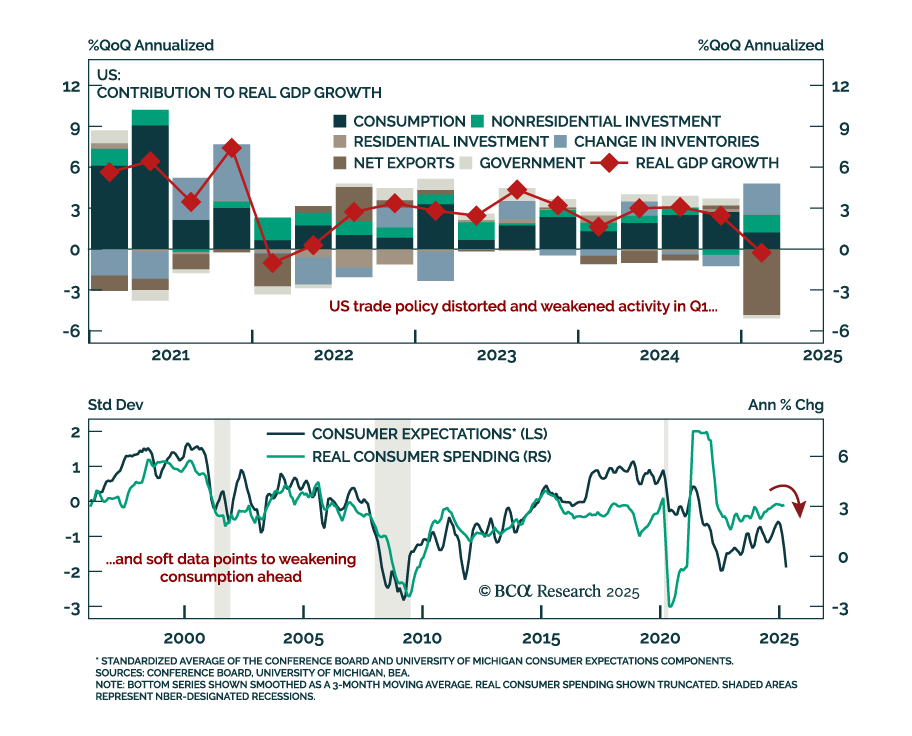

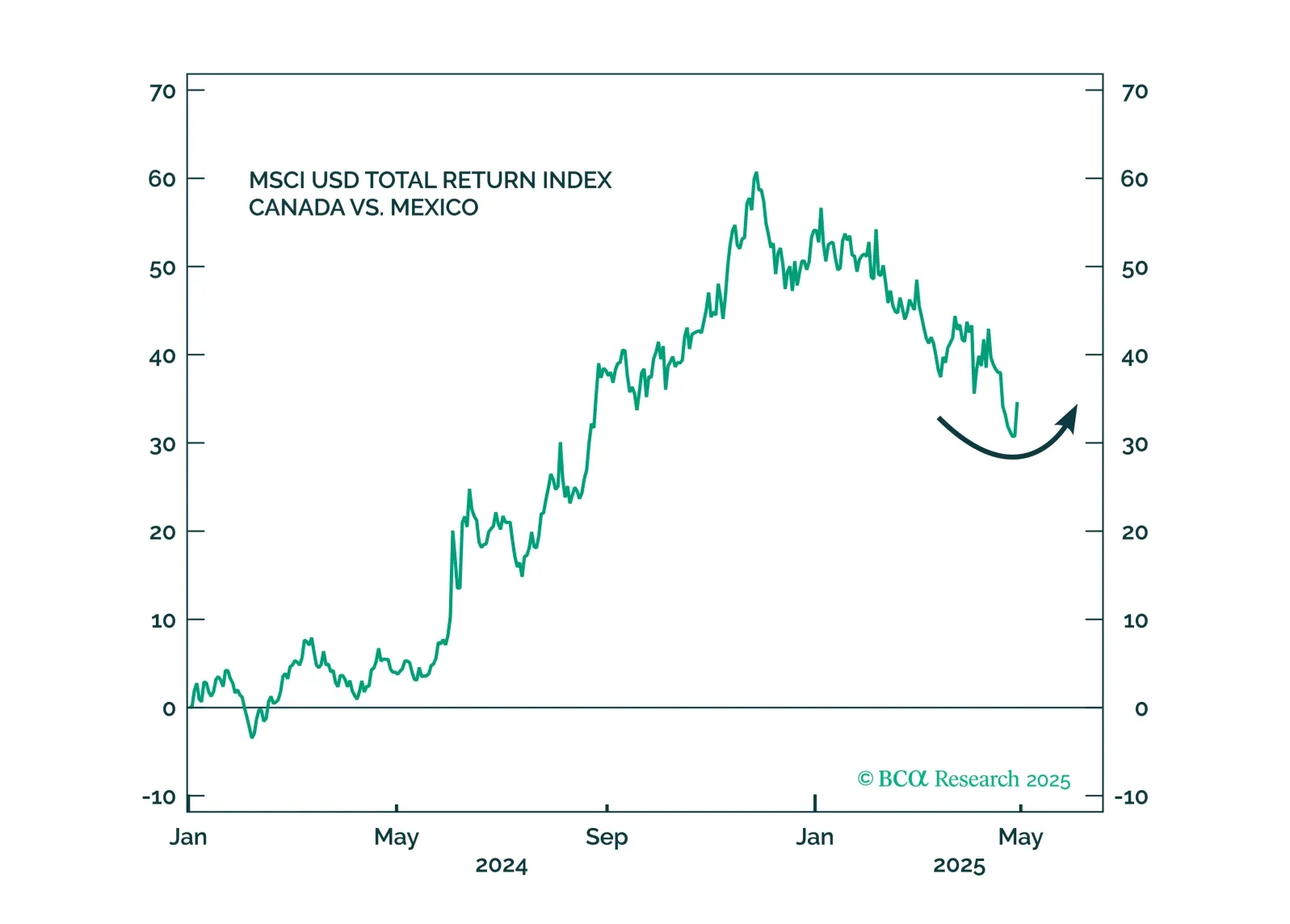

The US and Canada will resolve their trade dispute quickly, leading to a North American deal and better prospects for future relations, as well as for other US trade deals around the world. But even as tariff threats decline, the US economy will slow, weighing on its neighbors. Canada will fare better than Mexico.

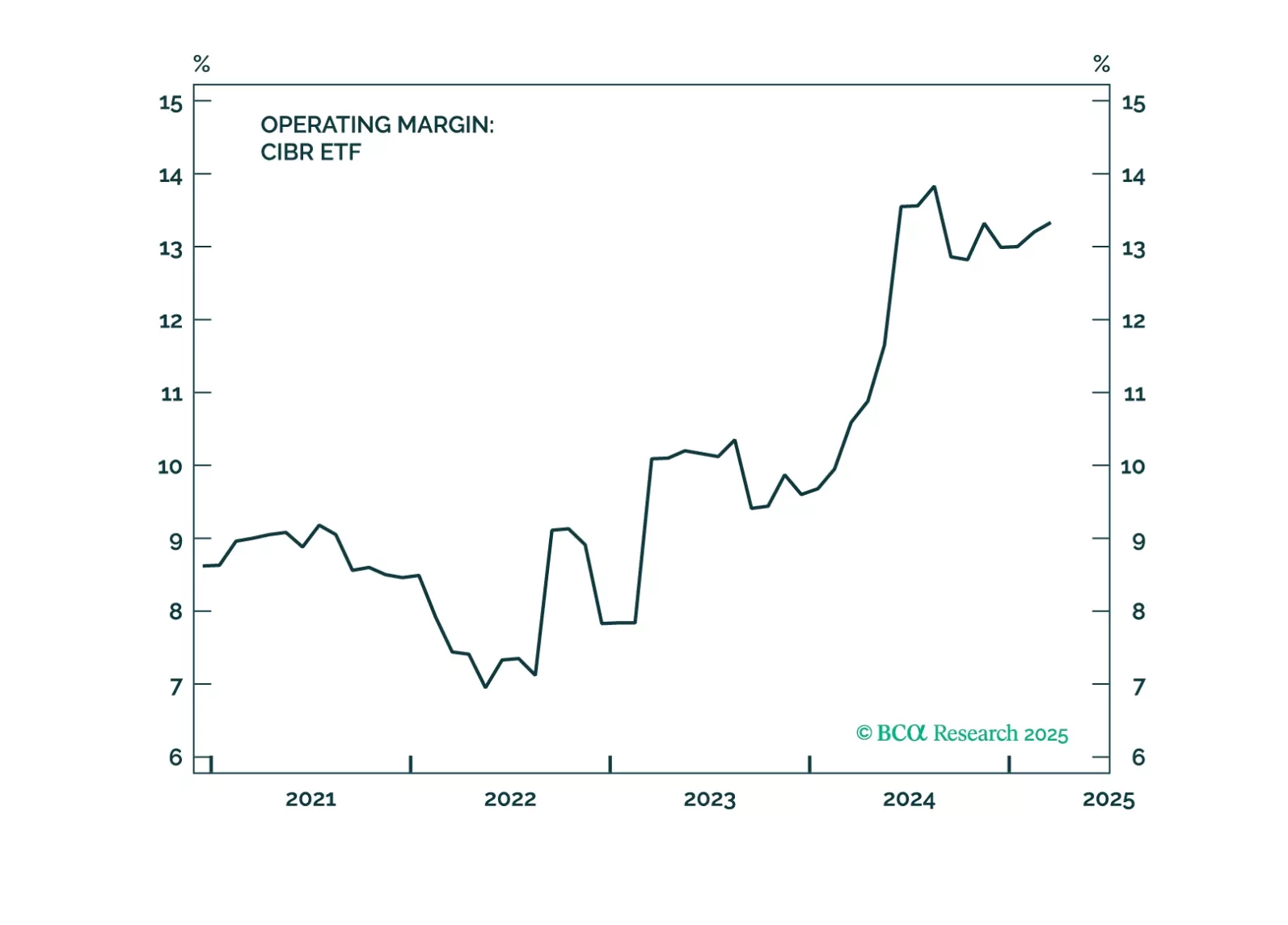

Cybersecurity is a strategic investment theme, which looks particularly interesting in light of the trade war and heightened geopolitical tensions. It is less exposed to tariffs than other industries and, if anything, benefits from geopolitical tensions as customers seek protection from international cyberattacks and cybercrime. The industry’s fundamentals are improving, while valuations are moderating. A recent pullback presents an attractive entry point into the theme.

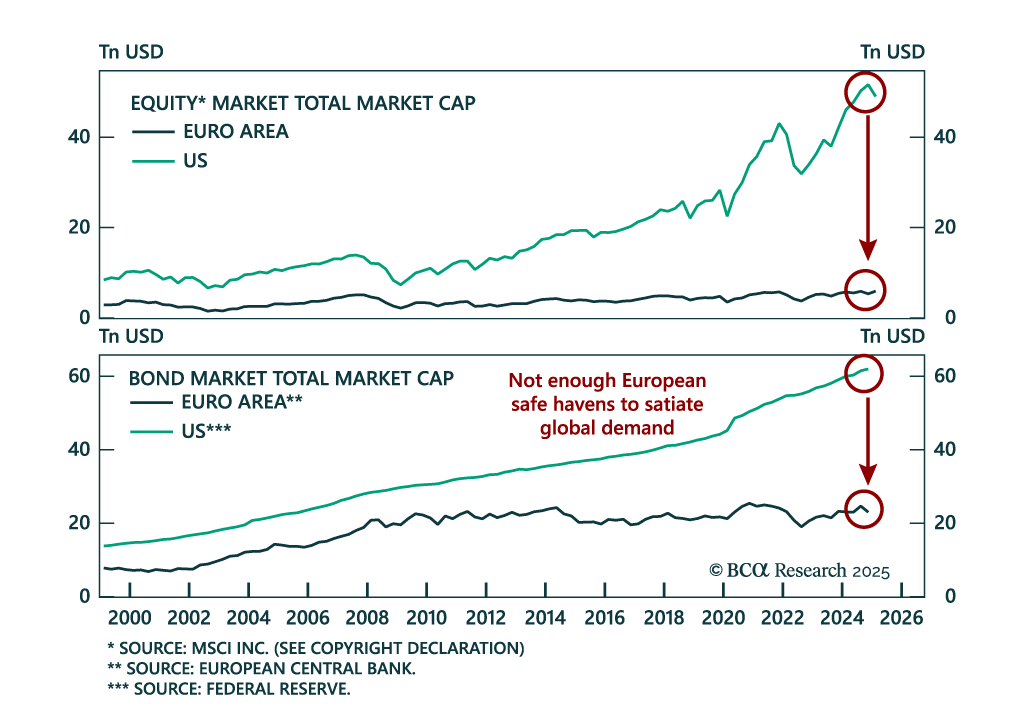

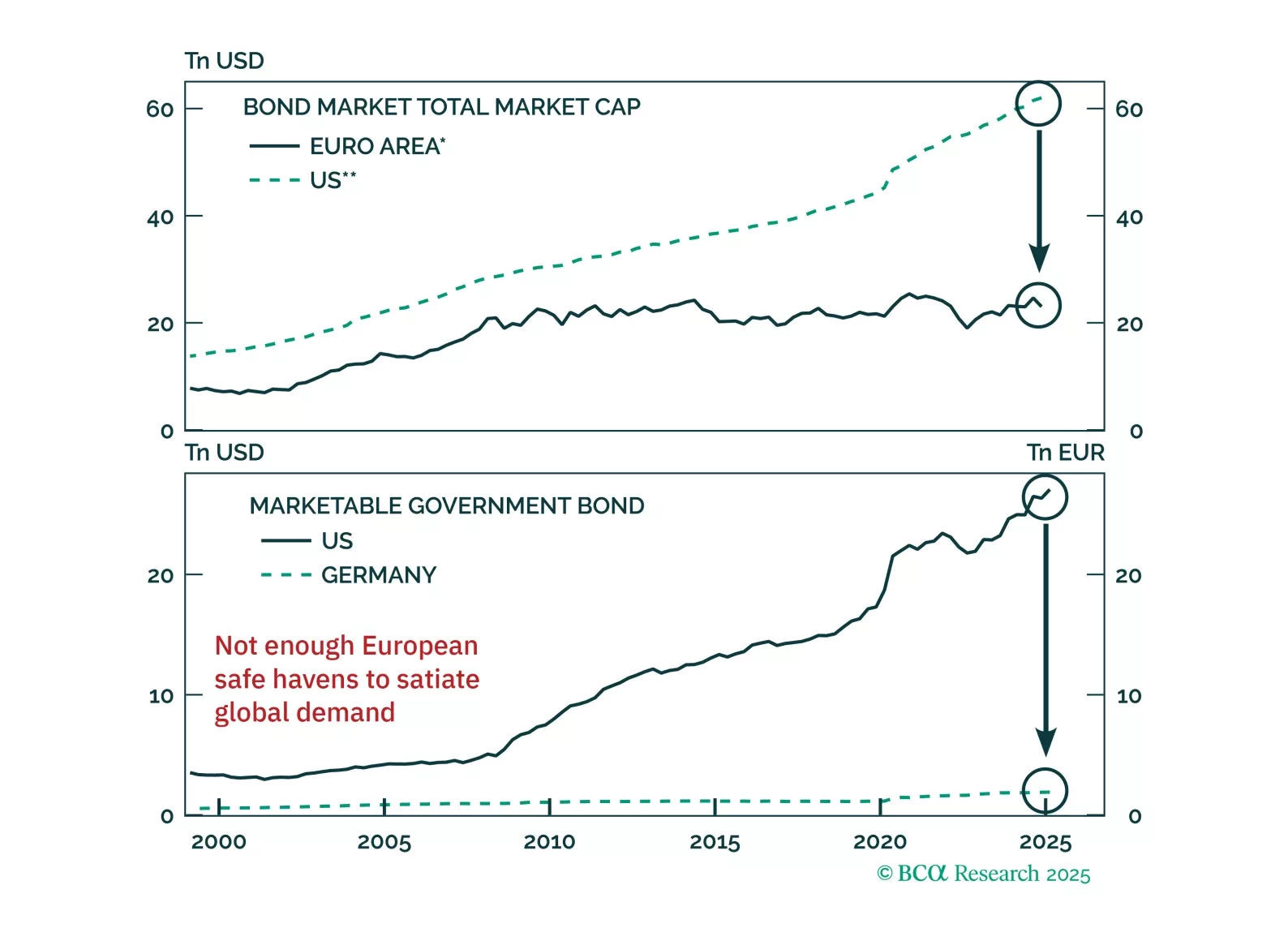

Are bunds the new Treasurys? The euro and German debt are gaining favor as safe havens, but markets may be overplaying the shift. Our latest report dissects what's durable, what's not, and how to trade the dislocation.