Developed Countries

Several signs have emerged that the “bad news is good news” rally has run its course. Despite deteriorating economic data, the Fed is expected to maintain its “higher for longer” stance, disappointing the market. A rate cut is likely is only in case of a severe downturn, but that will not offer support to equities, until earnings growth bottoms. We recommend shifting a portfolio toward a defensive stance, and away from cyclicals at this juncture. We downgrade Auto to an underweight, and Capital Goods and Energy Equipment and Services to an equal weight.

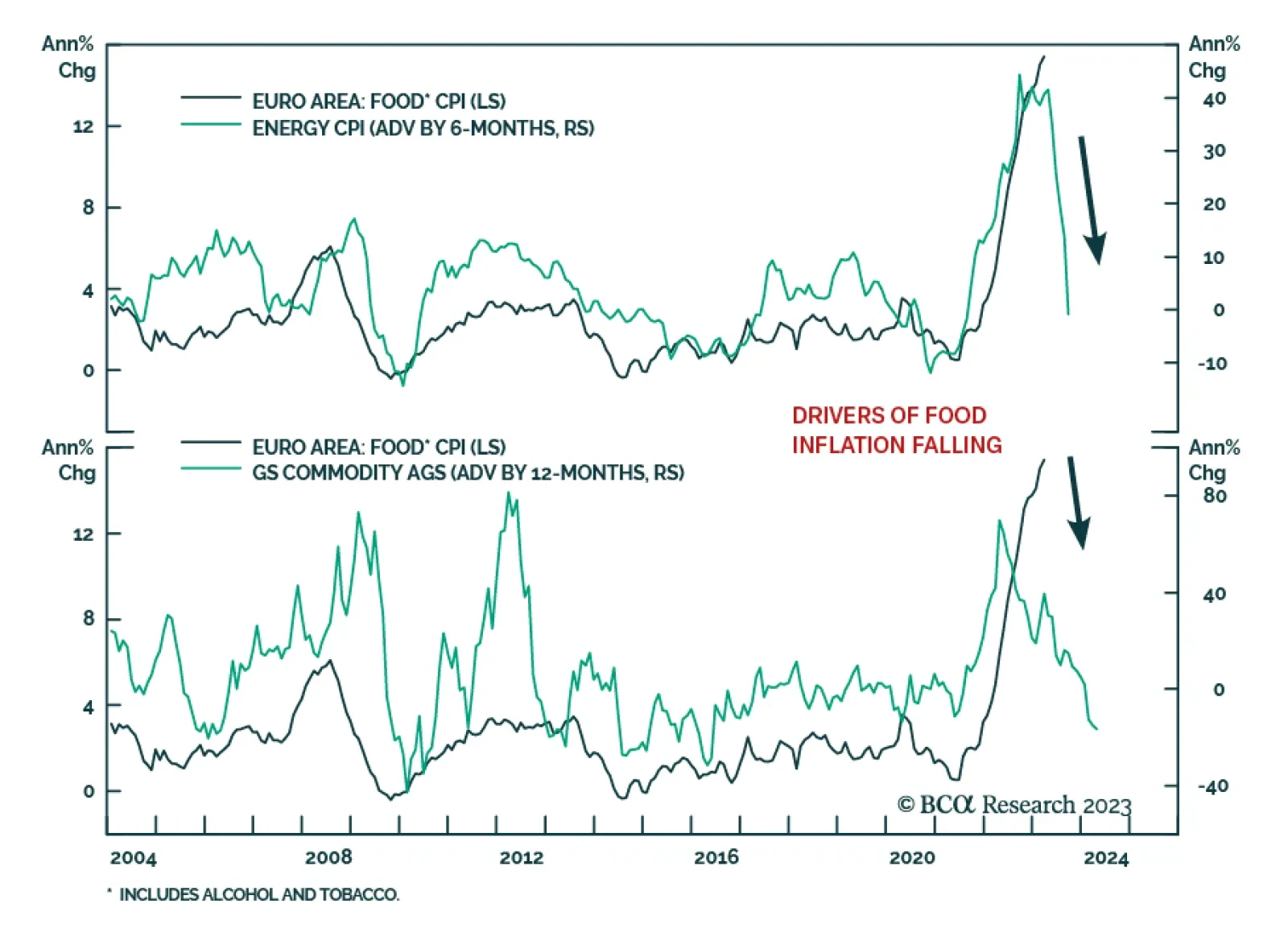

European inflation has further downside and core CPI will soon begin to fall too. However, European growth will remain soggy in Q2. What does this environment mean for investors?

In this week’s review, we look at recent data and its impact on currency markets.

In this <i>Special Report</i>, BCA Strategist Ritika Mankar highlights that Japanese savers own foreign assets to the tune of a staggering $6.5 trillion today. As implausible as it may seem today, the rate cycle in Japan will turn later this decade. Once it does, Japanese savers will sell down their global assets – a dynamic that is likely to kick up a storm.