Developed Countries

This week we present our Portfolio Allocation Summary for April 2023.

High rates have hurt real estate and, now, banks. The next shoes to drop: Loan growth, profits, and employment. Stay defensive. Recession is probable, but risk assets have not priced it in.

Is the European banking system hiding nasty surprises? How will the recent stress affect European growth and the ECB’s policy outlook?

We think the banking turmoil set off by Silicon Valley Bank’s failure will prove to be less than it’s been cracked up to be and that it will not derail the near-term equity we expect.

This week we are sending you a Style Chart Pack, which now includes a standalone macro section, as well as macro, fundamentals, valuations, technicals, and uses of cash charts for the S&P 500, Defensives vs. Cyclicals, Growth vs. Value, and Small vs. Large. In the front section of this publication, we will review recent equity performance, and attempt to answer real estate sector-related questions that are foremost in investors’ minds.

This US Bond Strategy Insight takes an in-depth look at core non-housing services inflation.

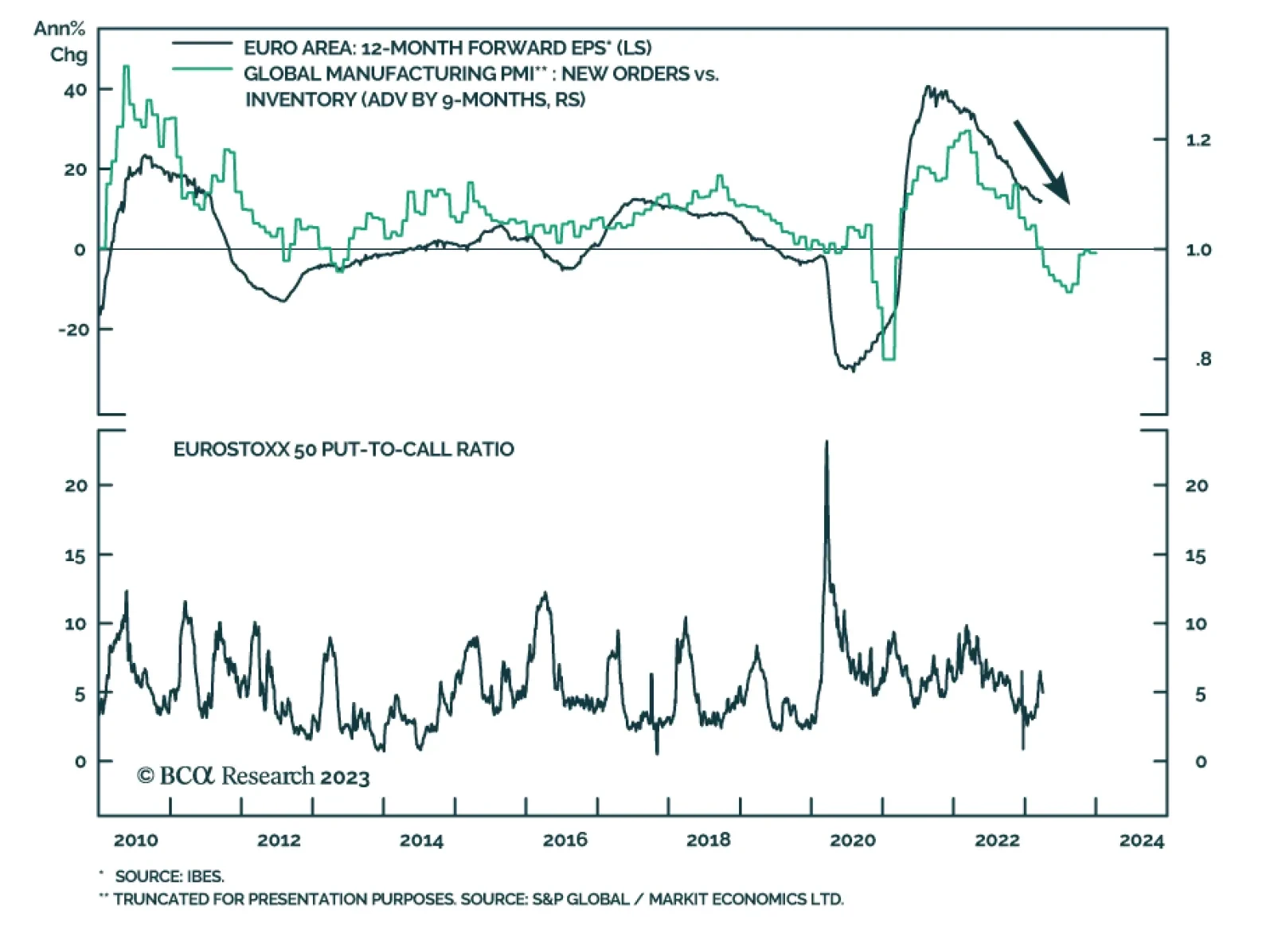

Stay defensive in the second quarter. We can see a narrow window for risky assets to outperform but we recommend investors stay wary amid high rates, supply risks, extreme uncertainty, peak polarization, and structurally rising geopolitical risk.

In this Special Report, we present our updated Central Bank Monitors for the US, Canada, Australia, New Zealand and Japan. We have improved the methodology used to calculate the monitors to make them more dynamic to structural changes over time. The main message from the Monitors is consistent across all five countries. The pressure to hike rates is diminishing, suggesting that the end of tightening cycles is approaching, but it is still too soon to expect rate cuts.

In this Strategy Outlook, we present the major investment themes and views we see playing out for the rest of 2023 and beyond.