Developed Countries

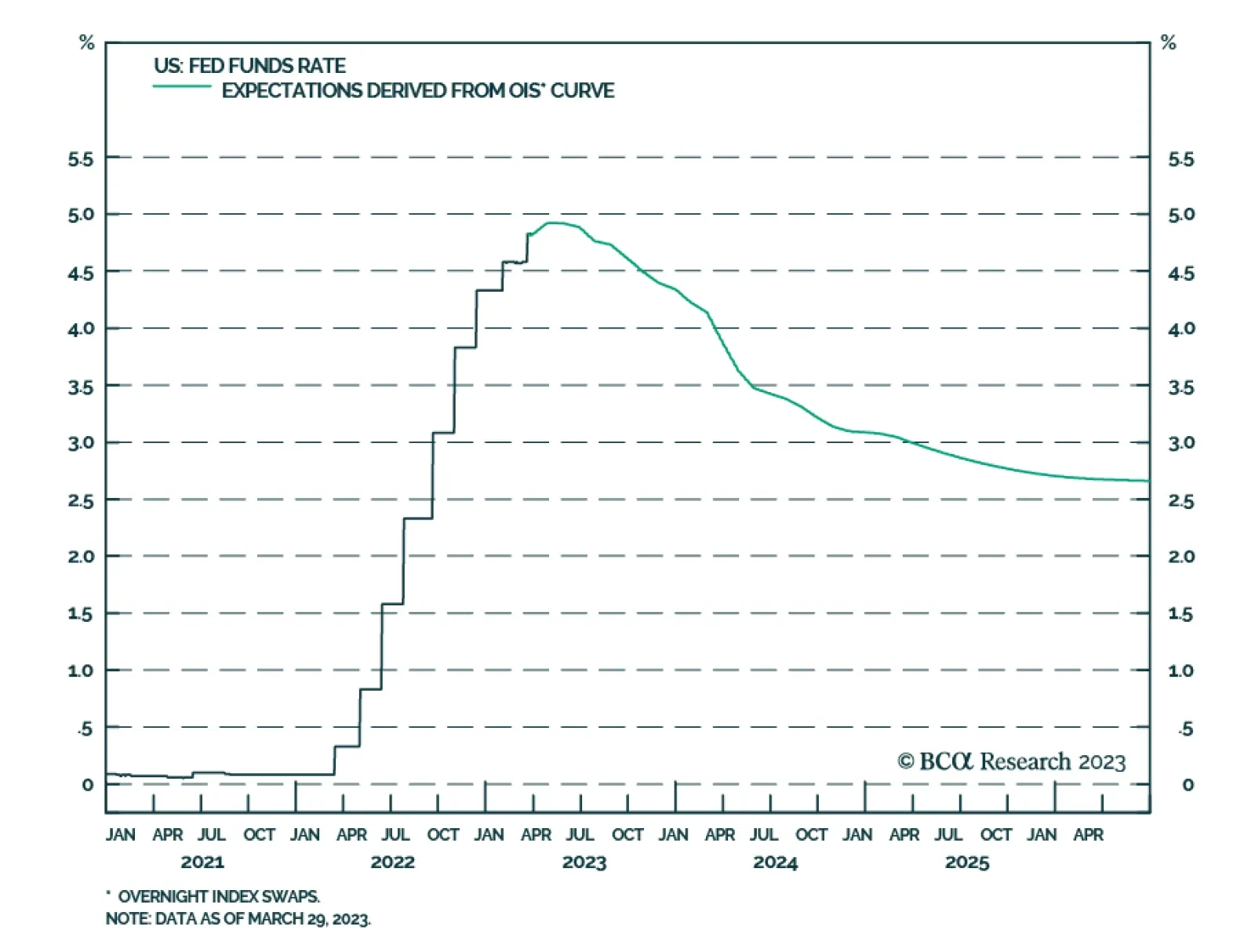

In Section I, we discuss the implications of the banking crisis that emerged in March. We do not expect what happened in the US or Europe to morph into a full-blown meltdown of the financial system, but this month’s events will likely lead to a further tightening in bank lending standards, raising further the odds of a US recession over the coming year. We continue to recommend an underweight stance toward risky assets versus government bonds over the coming 6-12 months, and defensive positioning within a global equity portfolio. In Section II, we estimate the impact of recently-passed US legislation on US business investment over the structural horizon and conclude that it will indeed boost capex growth over the coming several years. Assets poised to benefit from this trend will likely underperform over the coming year but should be bottom-fished following the next recession.

In Section I, we discuss the implications of the banking crisis that emerged in March. We do not expect what happened in the US or Europe to morph into a full-blown meltdown of the financial system, but this month’s events will likely lead to a further tightening in bank lending standards, raising further the odds of a US recession over the coming year. We continue to recommend an underweight stance toward risky assets versus government bonds over the coming 6-12 months, and defensive positioning within a global equity portfolio. In Section II, we estimate the impact of recently-passed US legislation on US business investment over the structural horizon and conclude that it will indeed boost capex growth over the coming several years. Assets poised to benefit from this trend will likely underperform over the coming year but should be bottom-fished following the next recession.

It is a big mistake to think that rate cuts or lower bond yields will ease credit conditions. Quite the contrary. After an aggressive tightening of monetary policy, the first rate cuts always coincide with much tighter credit conditions. We discuss the implications for credit, government bonds and equities. Plus, we find a startling anomaly in equity sector performance.