Developed Countries

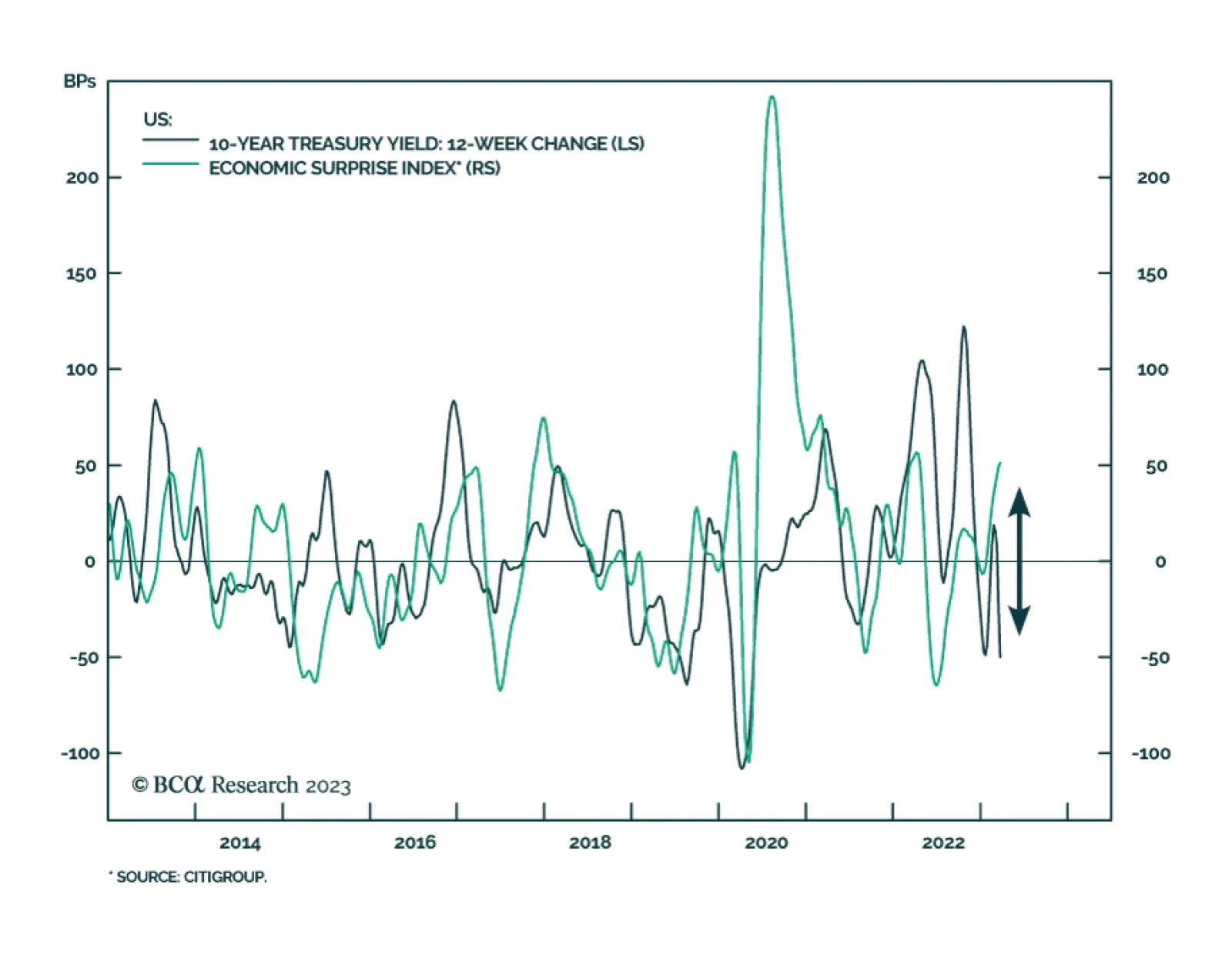

To the extent that Treasury yields typically rise when US economic data is strong, and decline when growth momentum disappoints, changes in bond yields have historically moved in tandem with the level of economic data surprises. However, the two series…

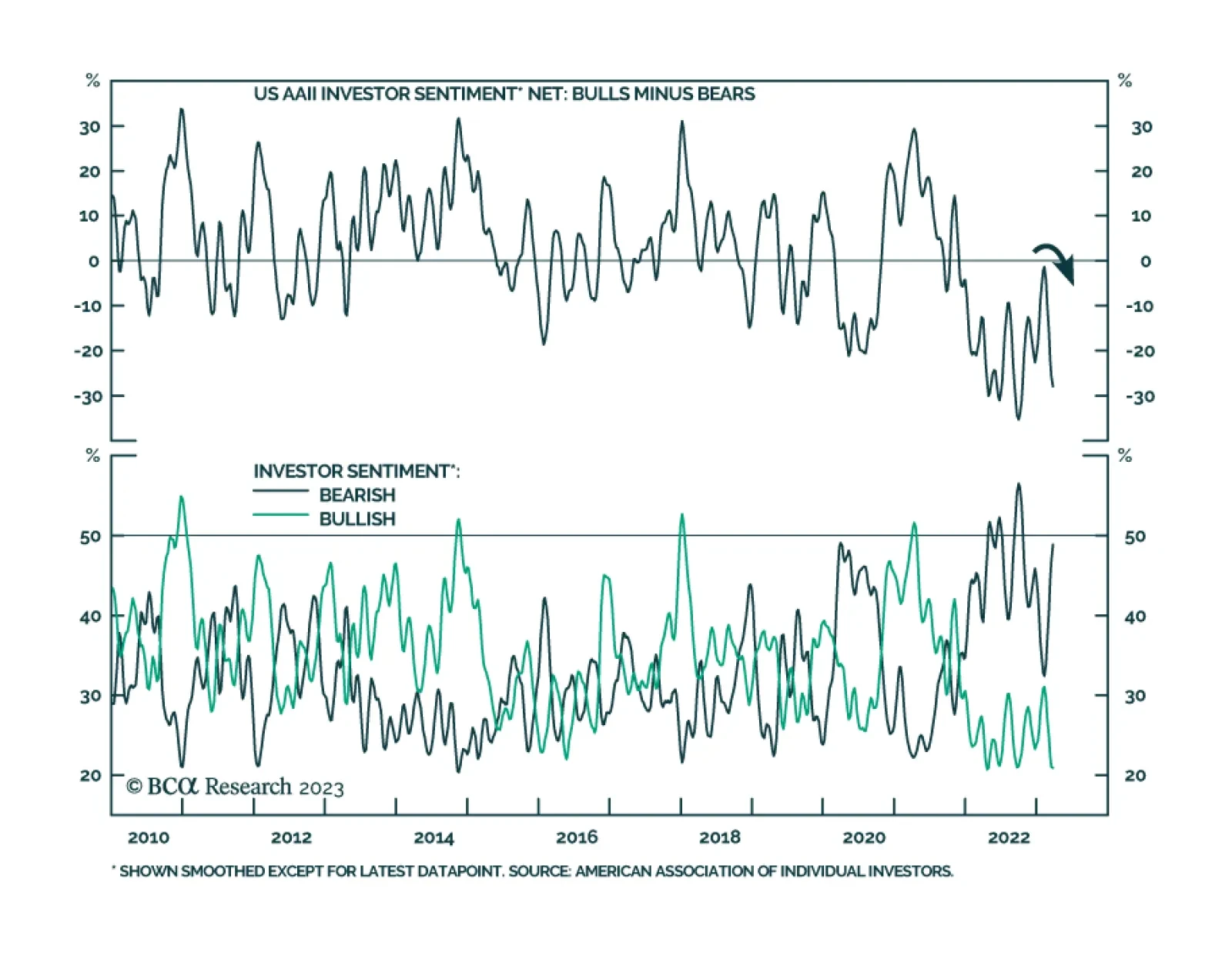

The American Association of Individual Investors (AAII) bull-bear survey shows a deterioration in investor sentiment following the flare up of bank tensions earlier this month. The latest results show that a net 28% of investors are downbeat on the stock…

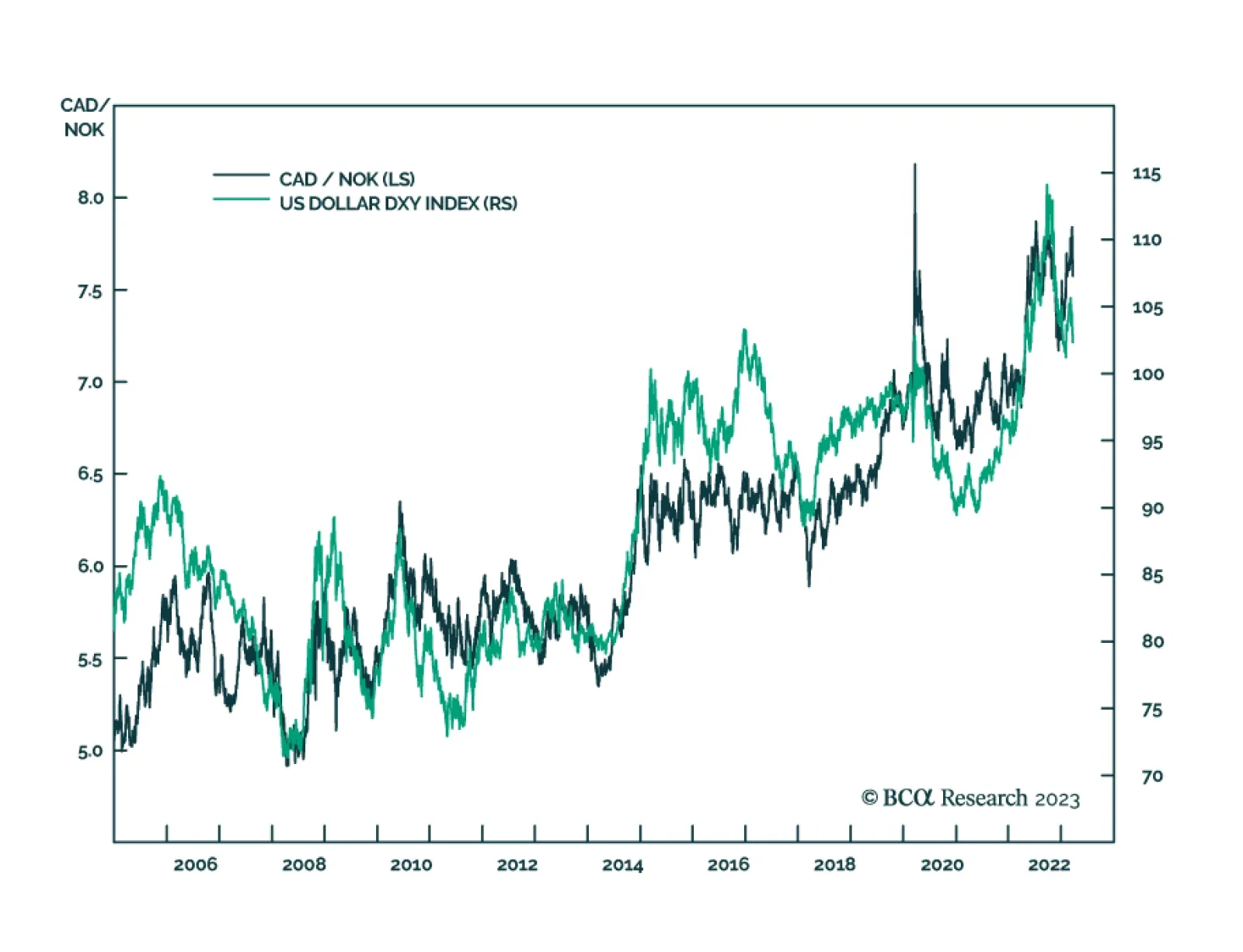

CAD/NOK tends to trade in perfect harmony with the DXY, but a divergence has emerged of late. For one, the selloff in the Norwegian krone versus the Canadian dollar has not been associated with a similar rise in the DXY. The culprit has been both falling…

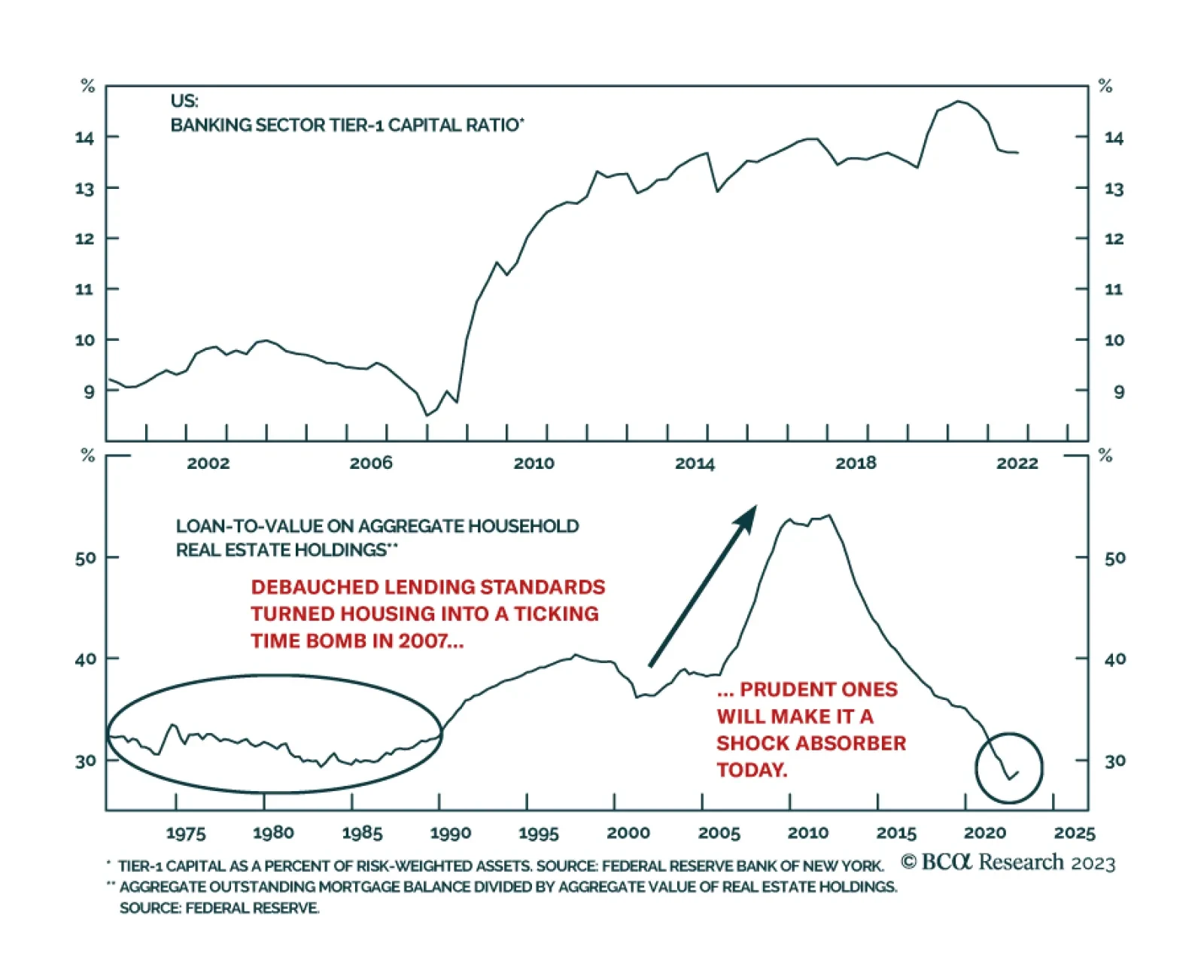

According to BCA Research’s Global Investment Strategy service, recent banking stresses will have a moderate but not severe impact on economic activity. On the positive side, banks are much better capitalized than they were in 2008. The quality of their…

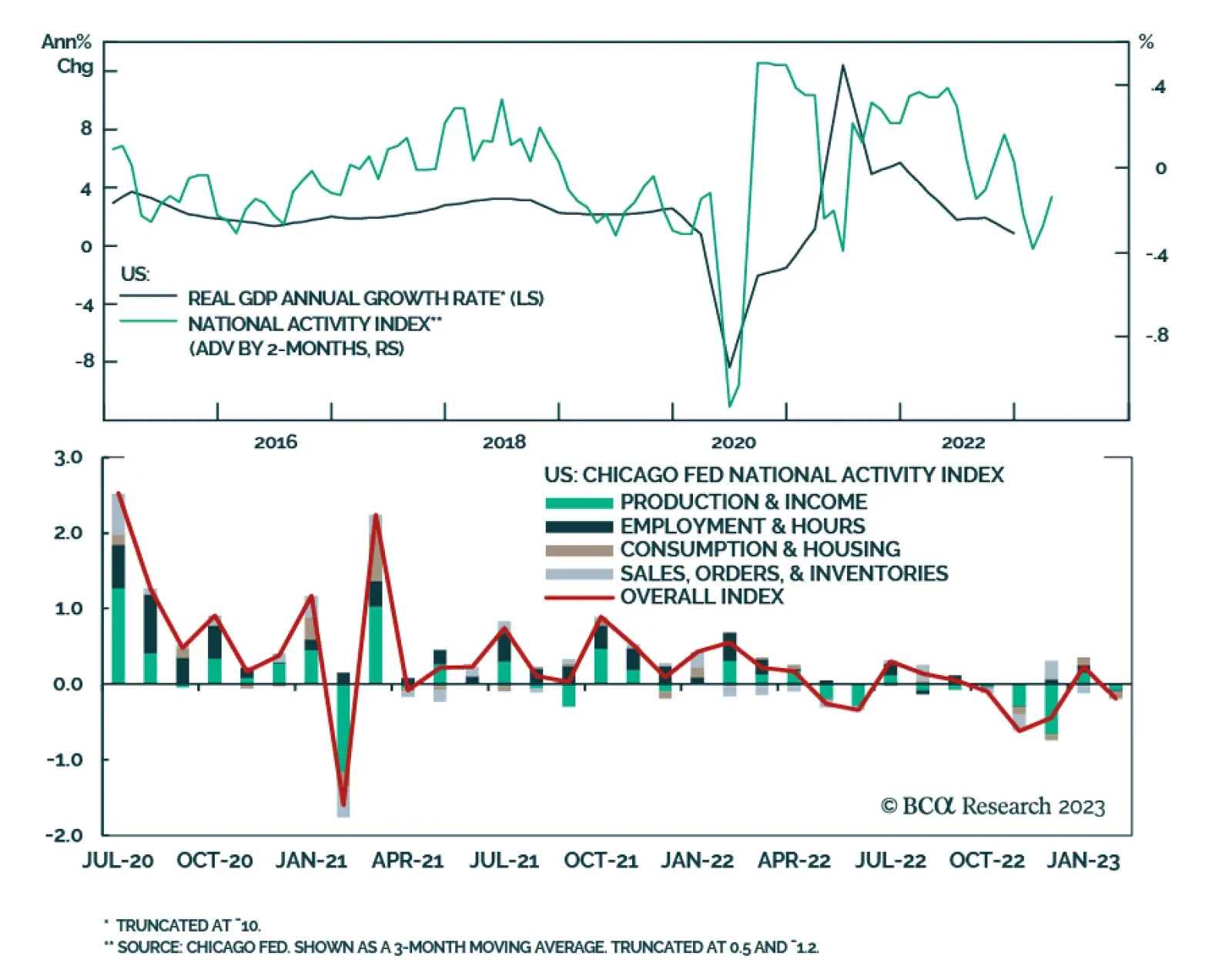

The Chicago Fed National Activity Index (CFNAI) – a summary statistic of all the important US economic data releases over the month – disappointed on Thursday. It fell from 0.23 to -0.19 in February, below expectations of a more muted decline to 0.10.…

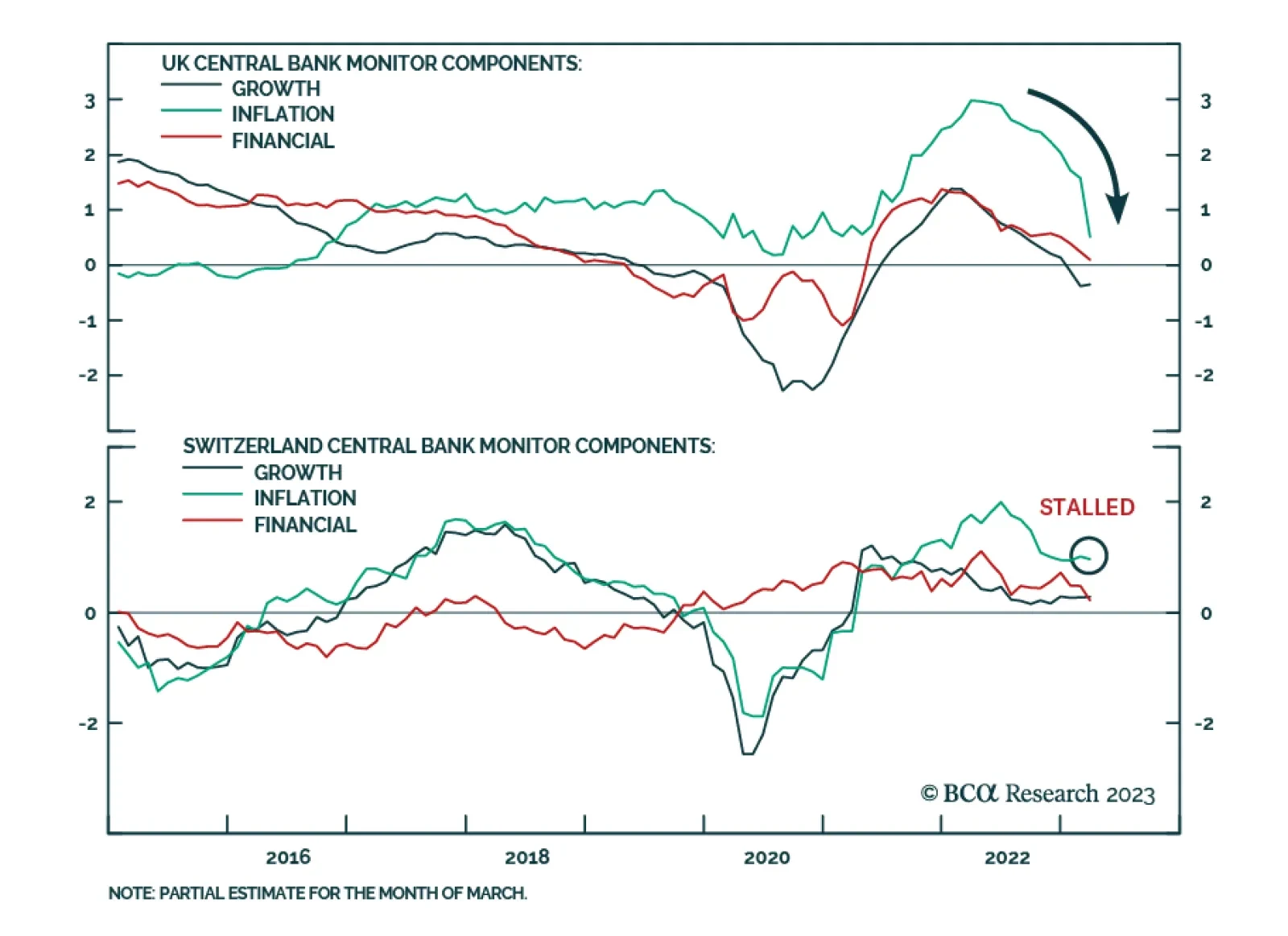

As expected, the Bank of England, Swiss National Bank, and Norges Bank all delivered rate hikes at their Thursday meetings, lifting interest rates by 25bps, 50bps, and 25bps respectively. In the case of the BoE, the Financial Policy Committee’s assessment…

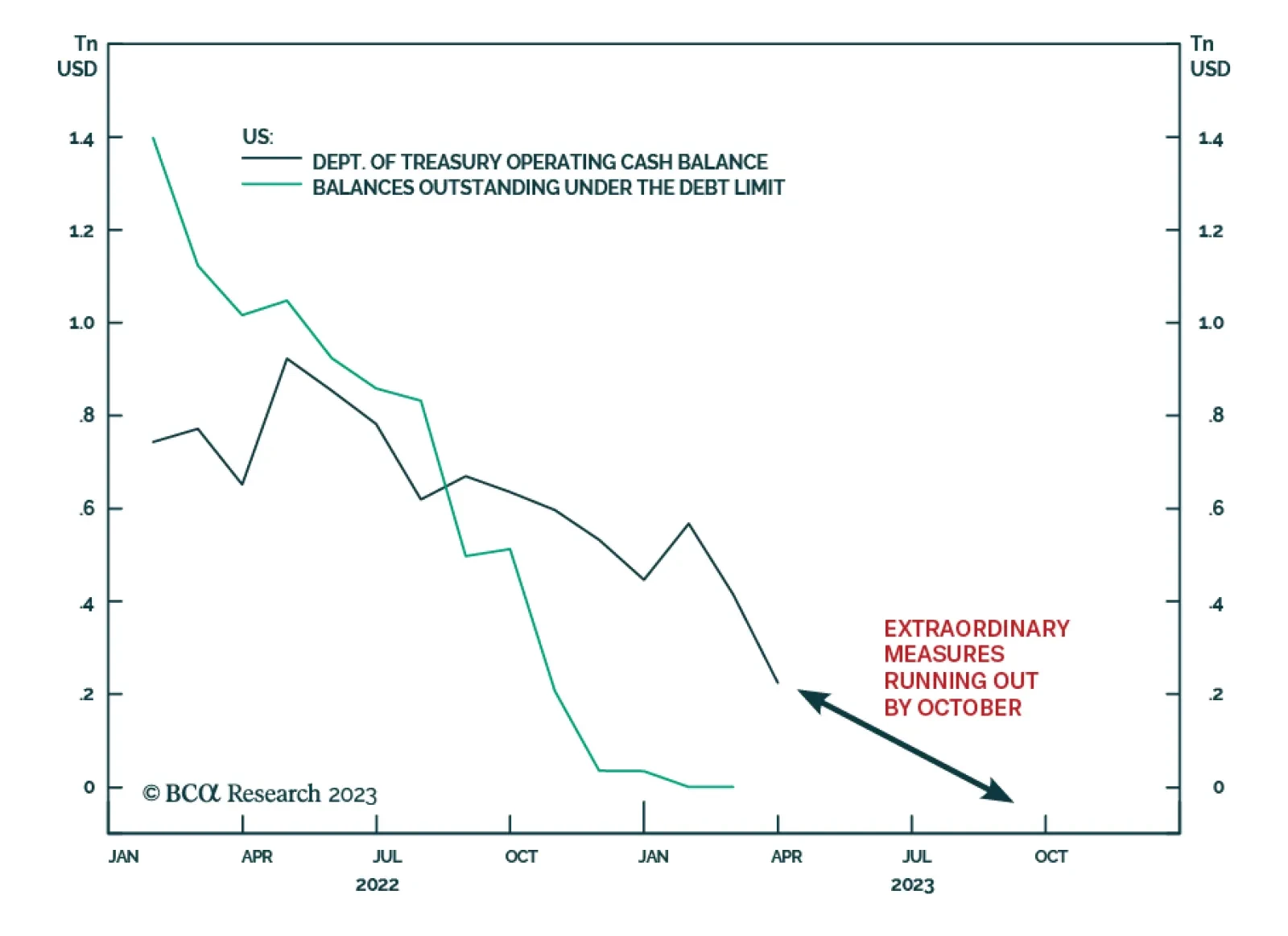

According to BCA Research’s US Political Strategy service emergency executive actions to stabilize the financial system will conversely lead to higher political risk and more dangerous brinksmanship in Congress, The Republican Party and Republican…

The Fed lifted rates 25 bps yesterday while also signaling that the tightening cycle is near its peak. We discuss the short-run and long-run implications for Treasury yields.

US financial instability reinforces our bearish investment outlook by weighing on economic growth and corporate earnings while also increasing US policy uncertainty and geopolitical risk.

Have global equity markets reached a riot point? Is the Fed going on hold a sufficient condition for stocks to stage a cyclical rally? If not, what would be needed to produce such a rally? Does the Fed’s recent balance sheet expansion foreshadow a rise in the US money supply? This report provides answers to all these questions.