Developed Countries

The Russia-Ukraine war has prompted Europe to ramp up its defense spending. This will greatly benefit its defense industry, especially if defense coordination across the EU increases.

The Bank of Japan is about to get new leadership when Kazuo Ueda takes over as governor in April. Will there be a new monetary policy to go along with the new governor? We attempt to answer that question, and what that means for global bond markets and the yen, in this Special Report.

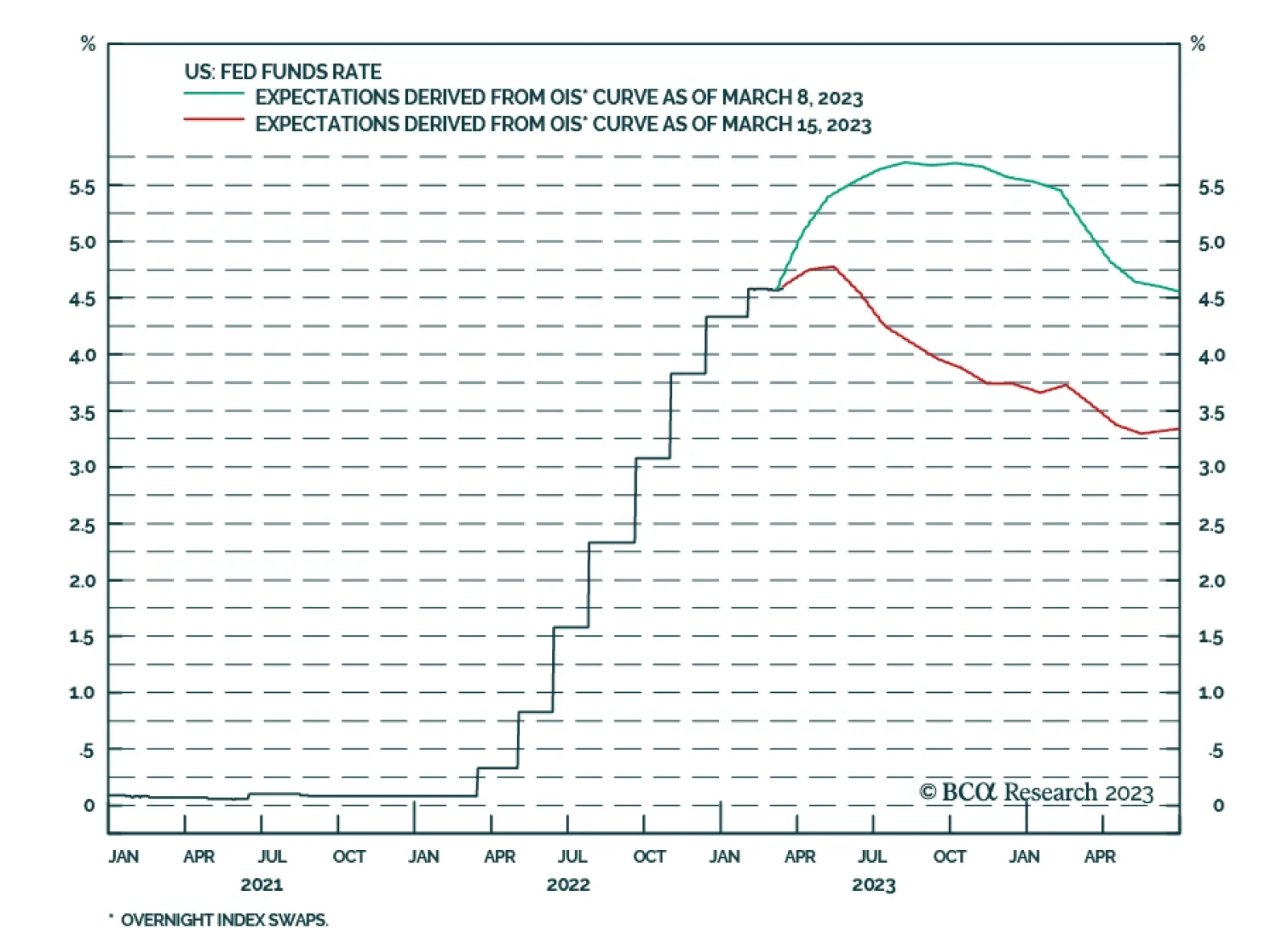

Depending on market volatility during the next few trading days, the Fed will either lift rates by 25 bps next week or pause its tightening cycle. Either way, the Fed’s hiking cycle is close to its peak but rate cuts won’t be coming anytime soon.

China’s victory in getting KSA and Iran to restore diplomatic relations is of far greater consequence to commodity markets than the past weeks’ bank failures in the US. For China, further success in sorting long-standing security issues in the Middle East could incentivize oil and gas capex and affect oil flows. With short- to medium-term fundamentals largely unchanged, we are keeping our 2023 and 2024 Brent forecasts similar to last month, at $95/bbl and $110/bbl, respectively.