Developed Countries

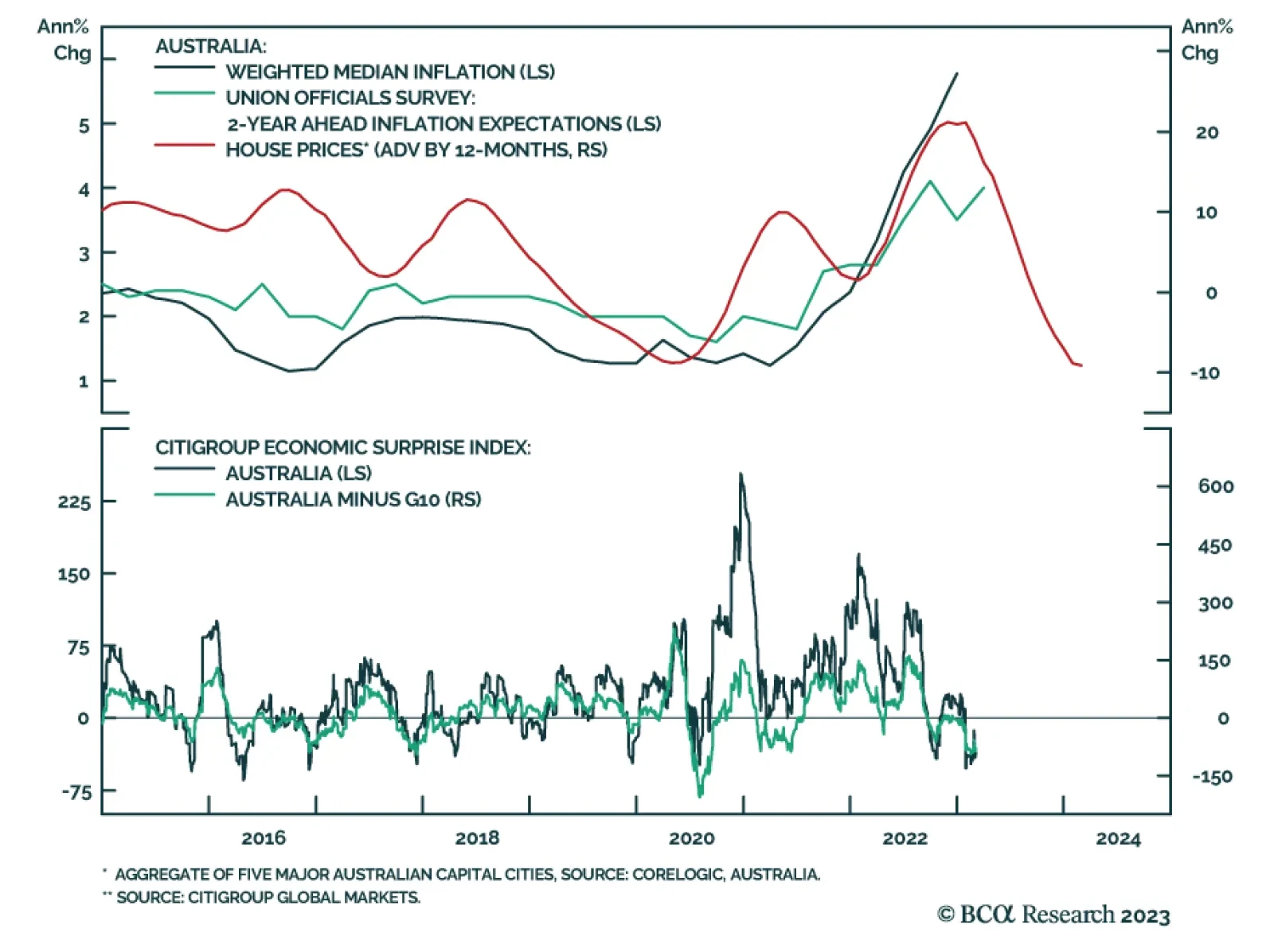

As expected, the Reserve Bank of Australia raised its Cash Rate by 25 basis points to 3.60%, delivering a 10th consecutive rate hike. However, the central bank’s dovish signal about the monetary policy outlook led to a decline in Aussie government bond yields…

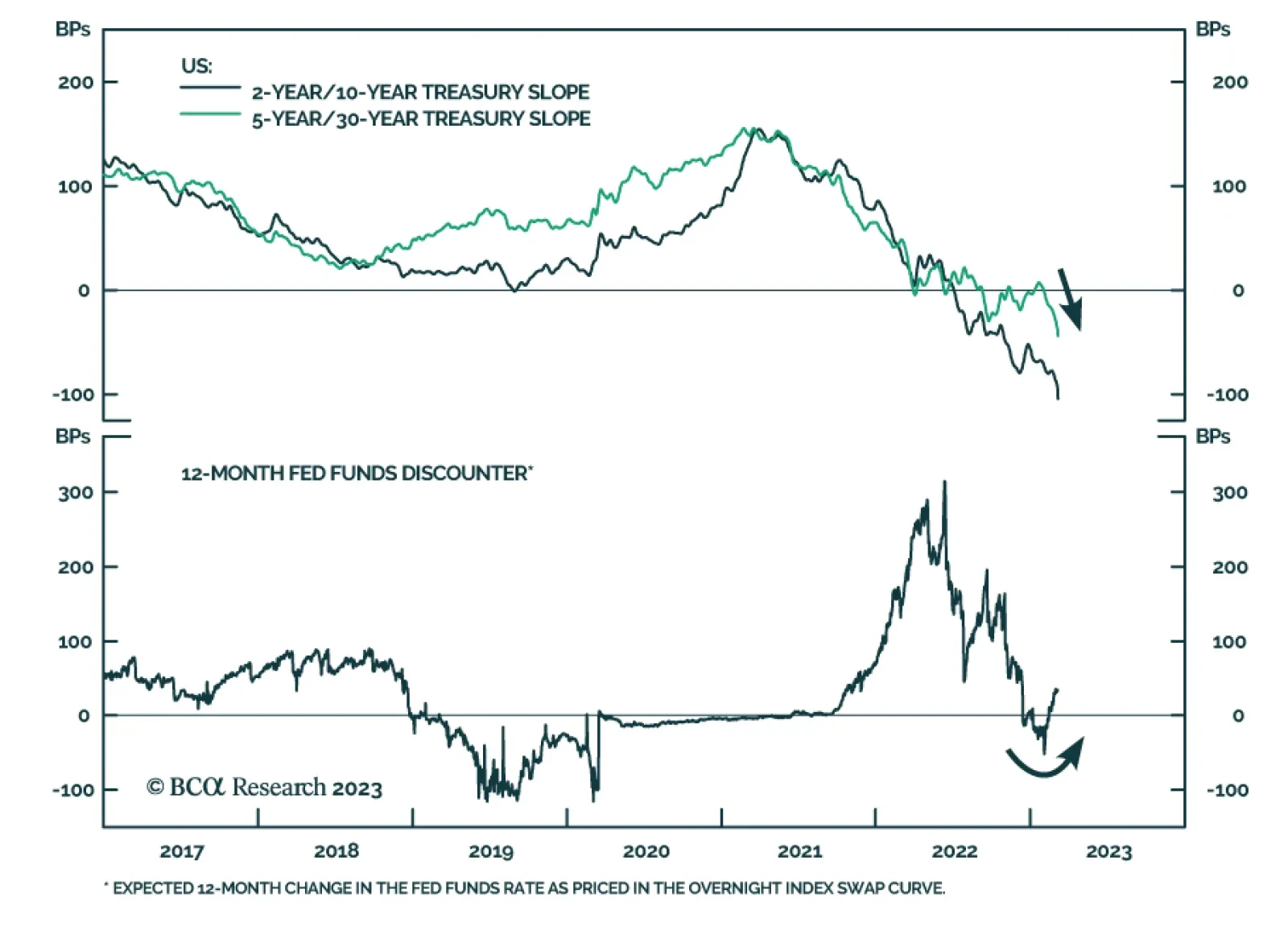

The US Treasury curve bear flattened sharply in response to Fed Chair Jay Powell’s testimony before the Senate banking committee on Tuesday. The 2-year yield’s 12 basis point jump and upward revision to futures markets’ expectations of the peak fed funds rate…

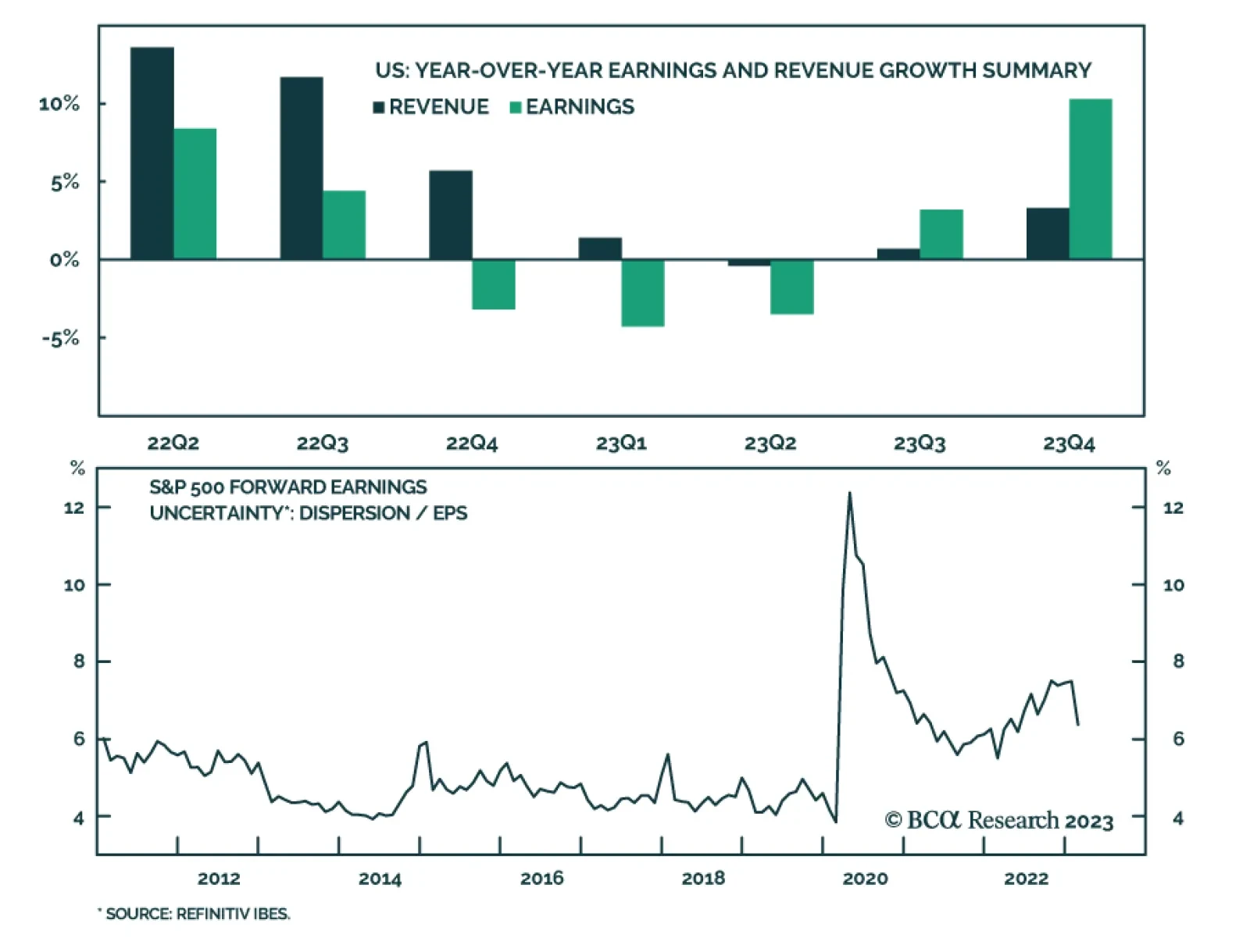

Lower earnings expectations: Analyst earnings growth expectations have moderated since the summer, downshifting from a sugar-high 10% in July to the most recent target of 2% for the next twelve months. This is a positive for equities as it indicates…

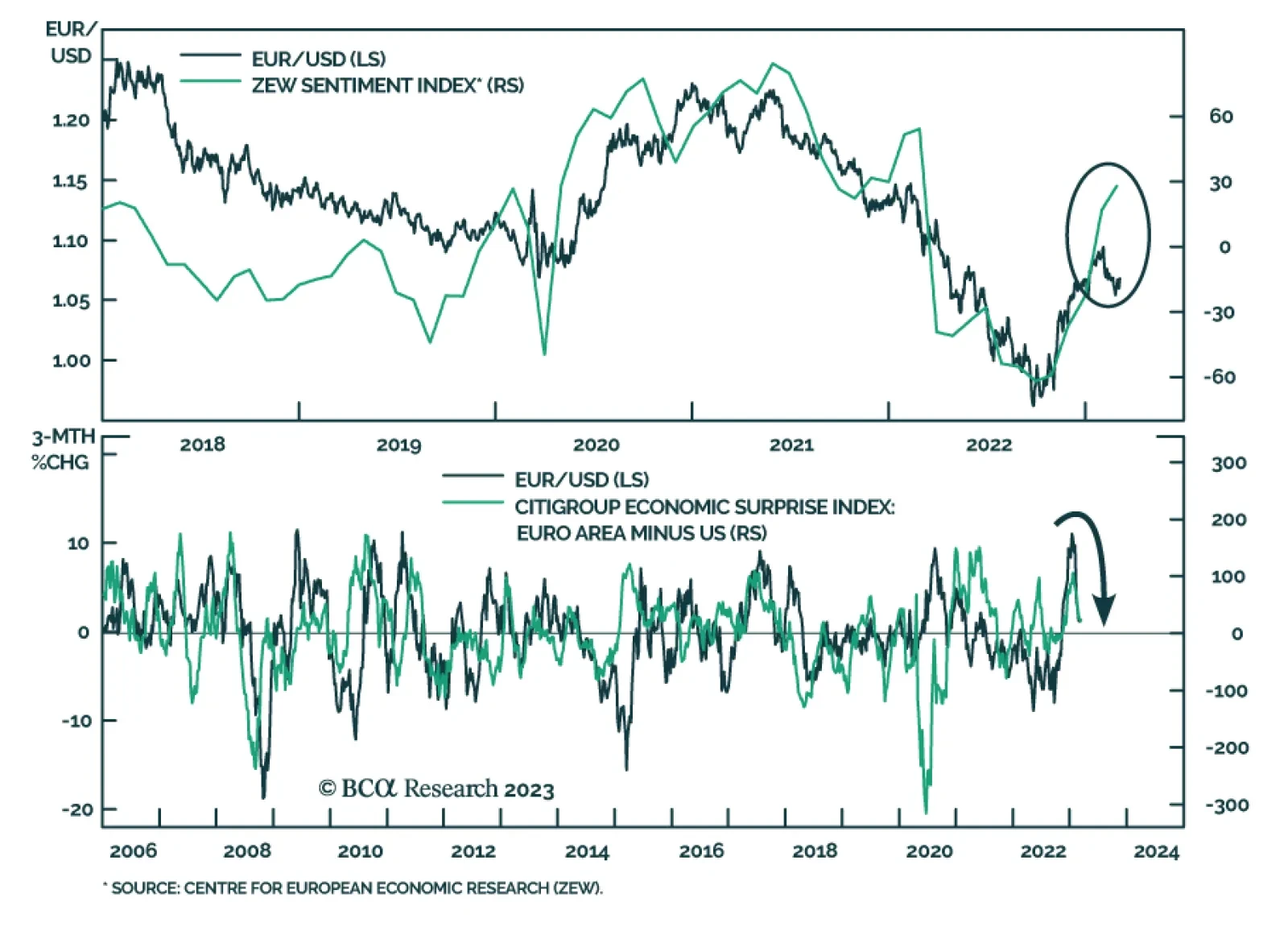

BCA Research’s European Investment Strategy & Foreign Exchange Strategy services conclude that for the next one-to-three months, European data could continue to underwhelm US variables, which will weigh on the euro. The euro has been giving back recent…

The equity market is back to the 2019 level on an inflation-adjusted basis. However, it is still not cheap as it is not pricing in the possibility of a prolonged and deep earnings recession or a higher interest rates regime. Many areas of the market that appear cheap, are cheap for a reason. The only industries that are cheap because they are growing into their valuations are Energy and Airlines. We are upgrading Airlines to equal weight.

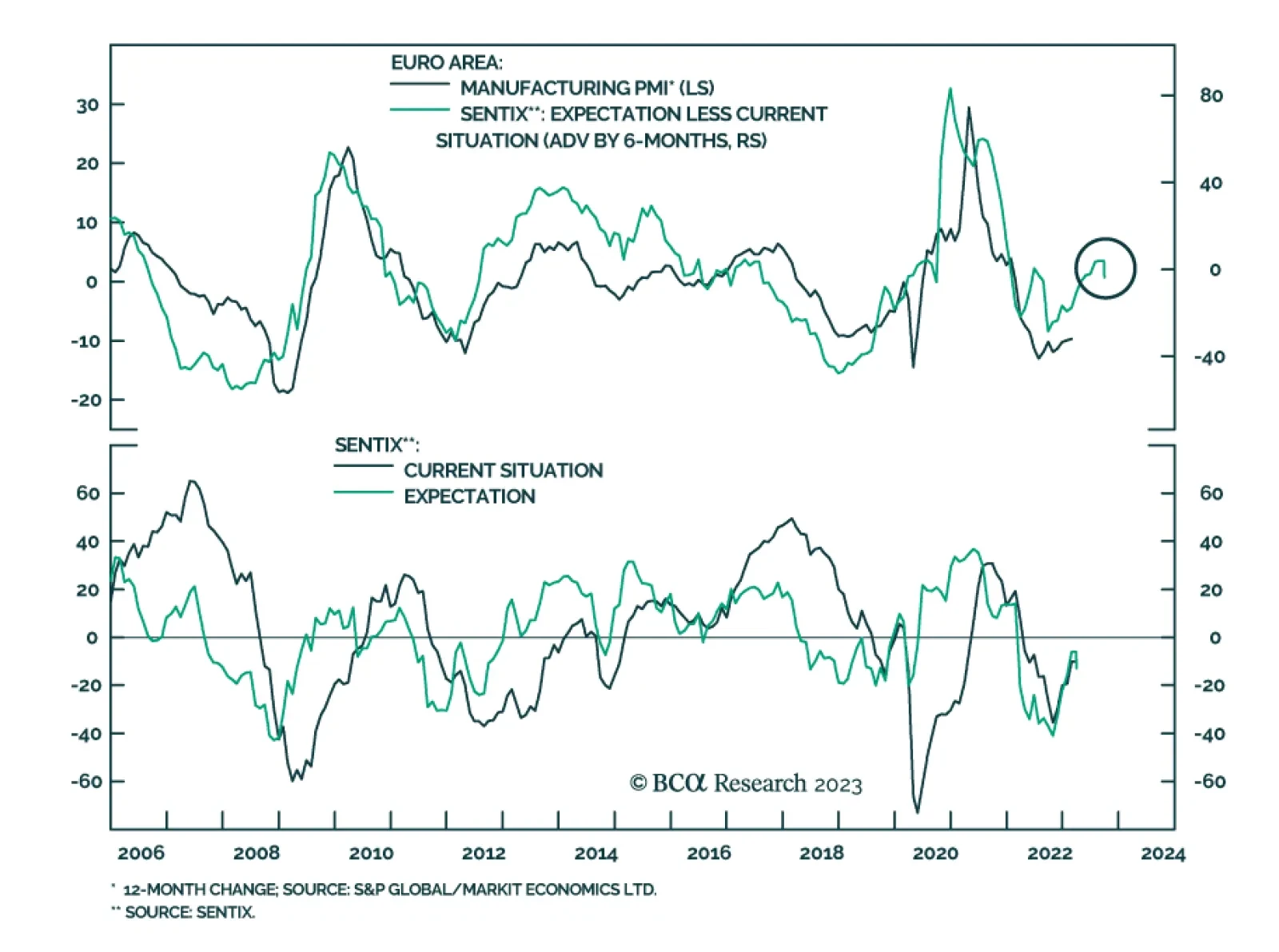

The March Sentix Economic Index sent a cautionary signal about investor morale. The overall index for the Eurozone declined from -8.0 to -11.1 – marking the first monthly decrease since the index bottomed at -38.3 in October and missing expectations of a…

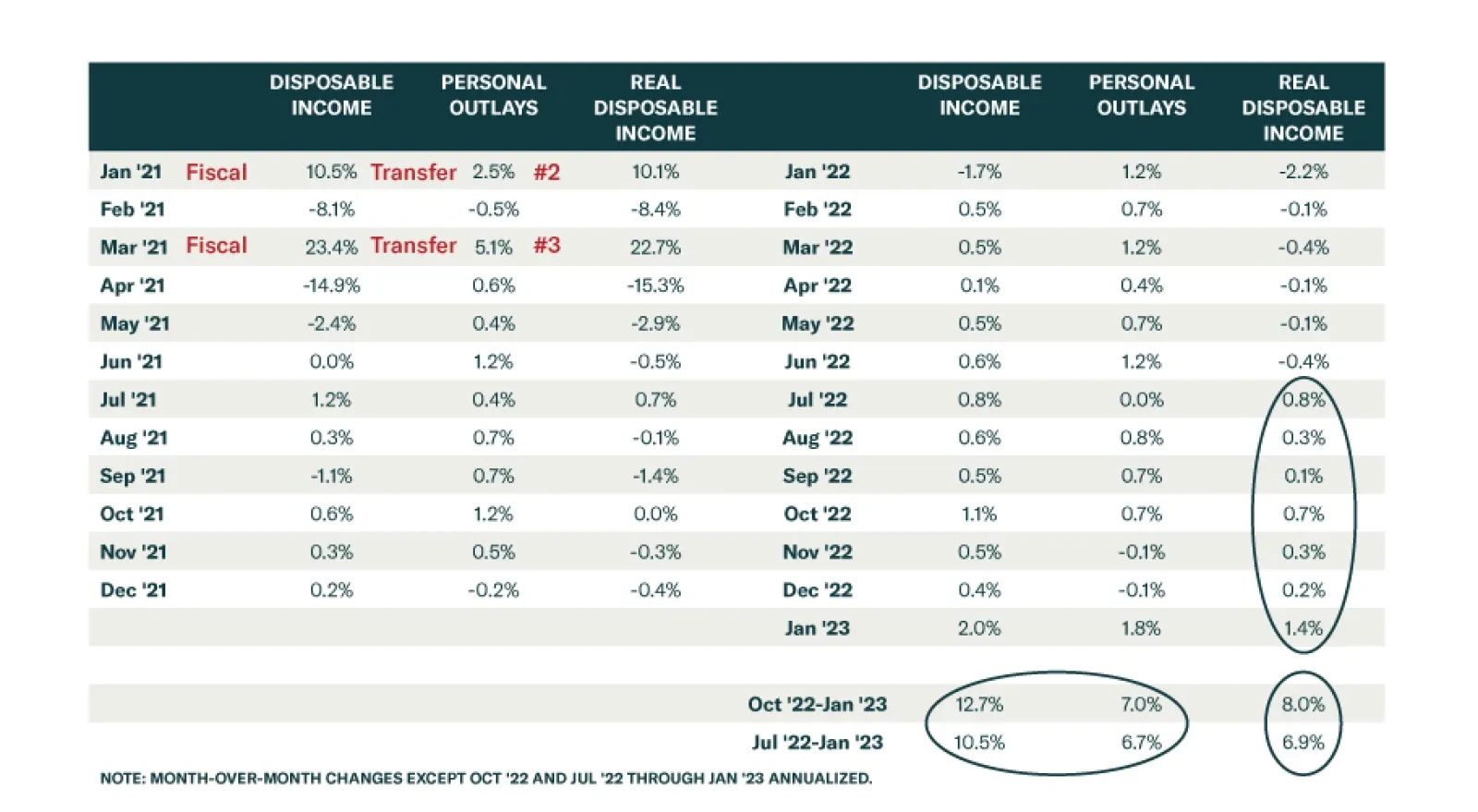

According to BCA Research’s US Investment Strategy service excess pandemic savings are far more evenly spread than most investors realize, and all but the households at the bottom of the distribution are swimming in cash. The team has used the savings rate…

This week we present our Portfolio Allocation Summary for March 2023.

A run of hot January data shook up financial markets, but we think they overreacted. We remain constructive on equities and the economy in the near term.

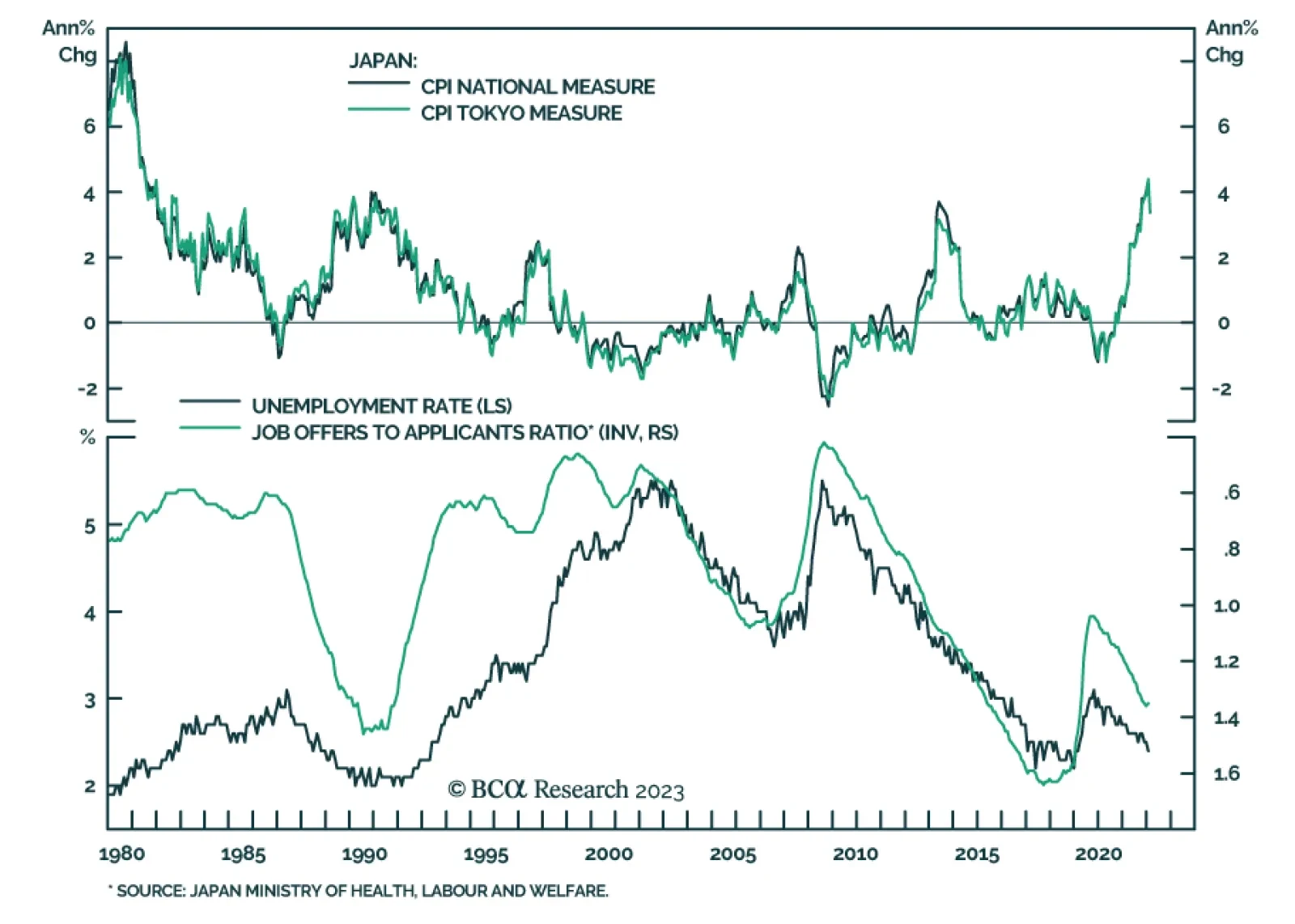

Last week’s Tokyo CPI release showed the first signs of modest disinflationary pressures in the Japanese economy. Headline inflation fell from 4.4% to 3.4%, in February. The ex-fresh food component also fell. That said, the core measure, that strips out both…