Developed Countries

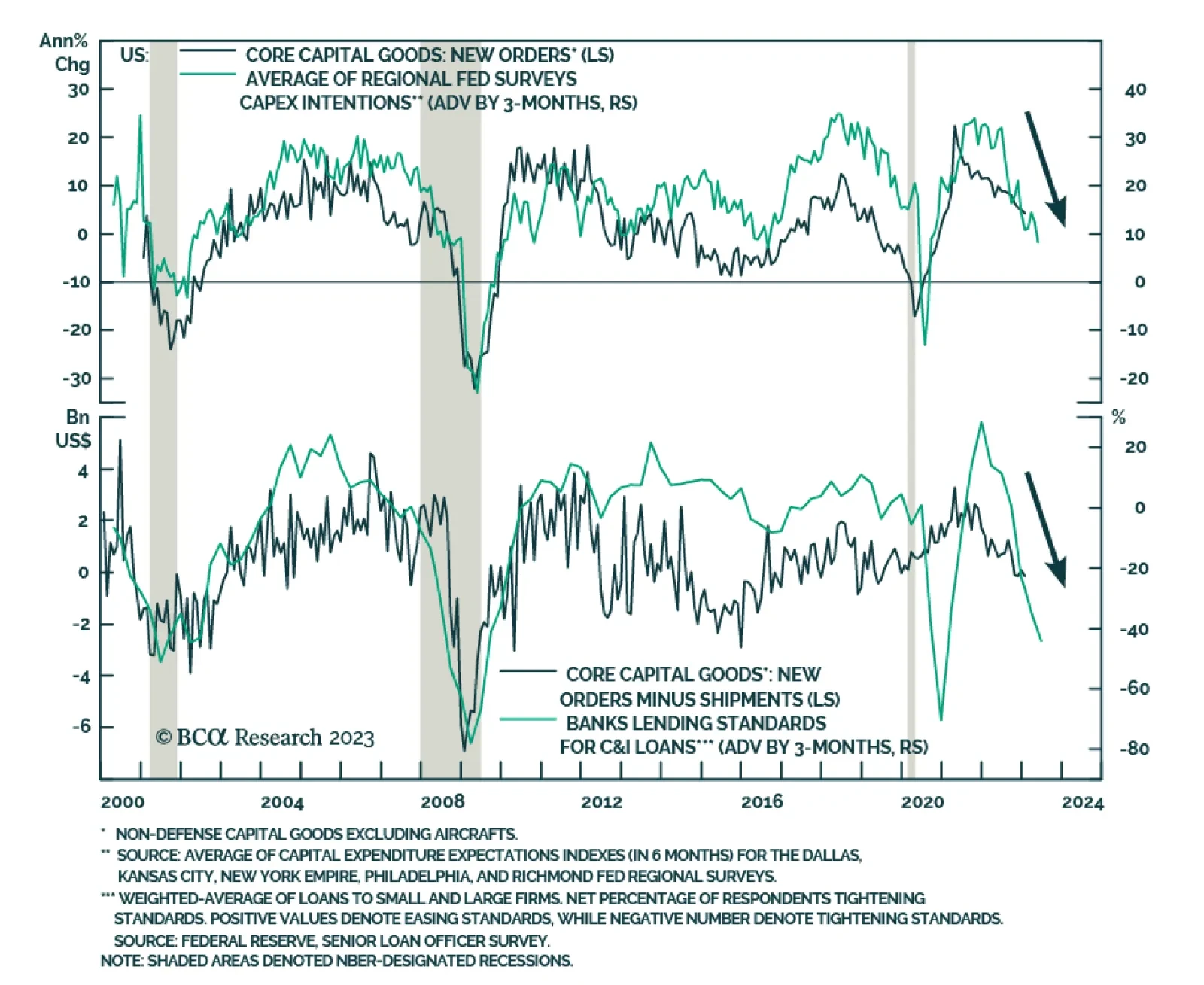

Although the 4.5% m/m drop in US durable goods orders in January (below expectations of a 4% m/m decline) painted a bleak picture of businesses’ willingness to invest, the contents of the report were significantly more positive. Specifically, a 13.3% m/m…

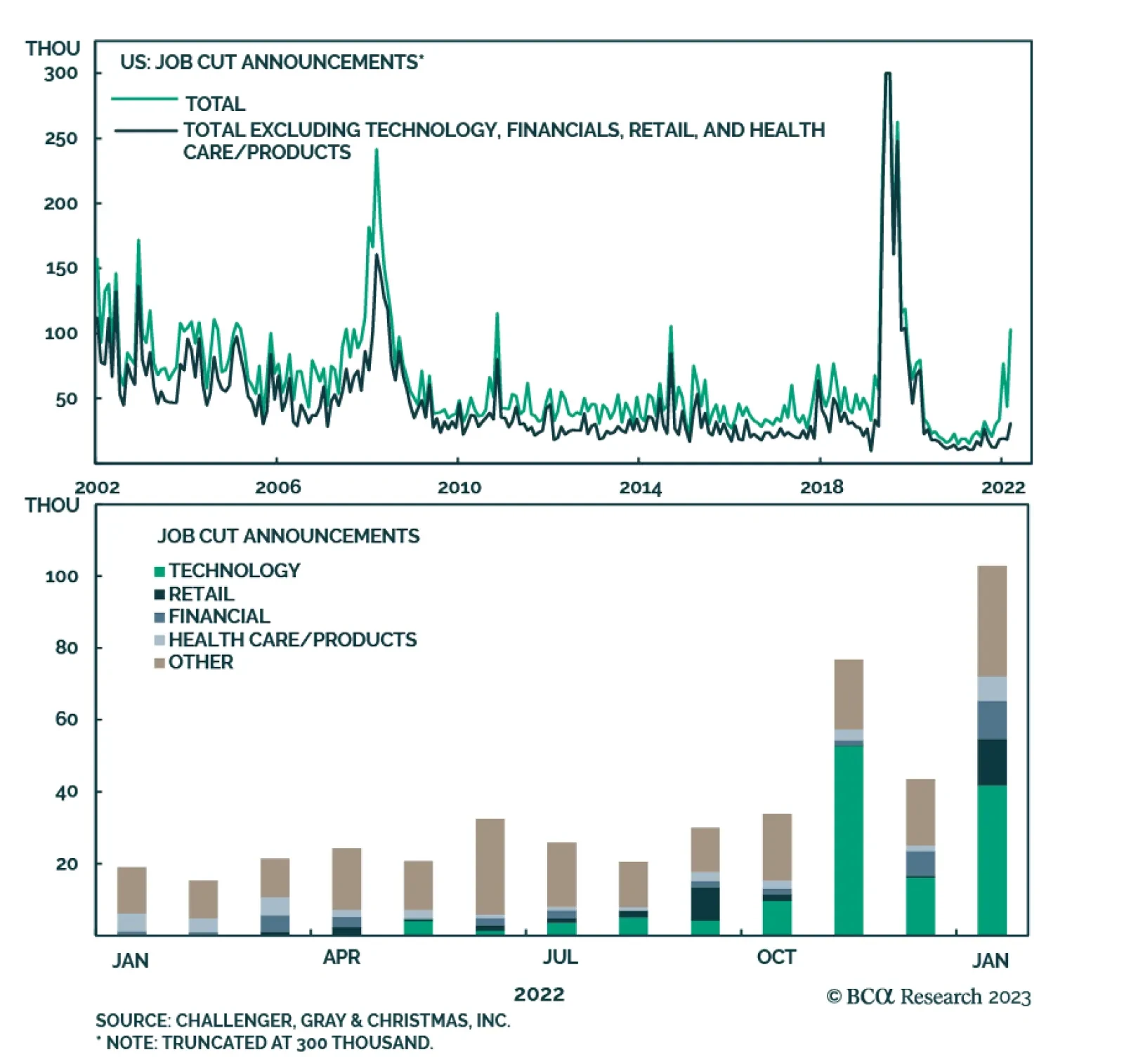

The number of job cut announcements as measured by Challenger, Gray, and Christmas has been trending higher in recent months. The 103 thousand cuts announced in January were the highest since September 2020 – marking a 136% m/m increase and a 440% y/y rise. …

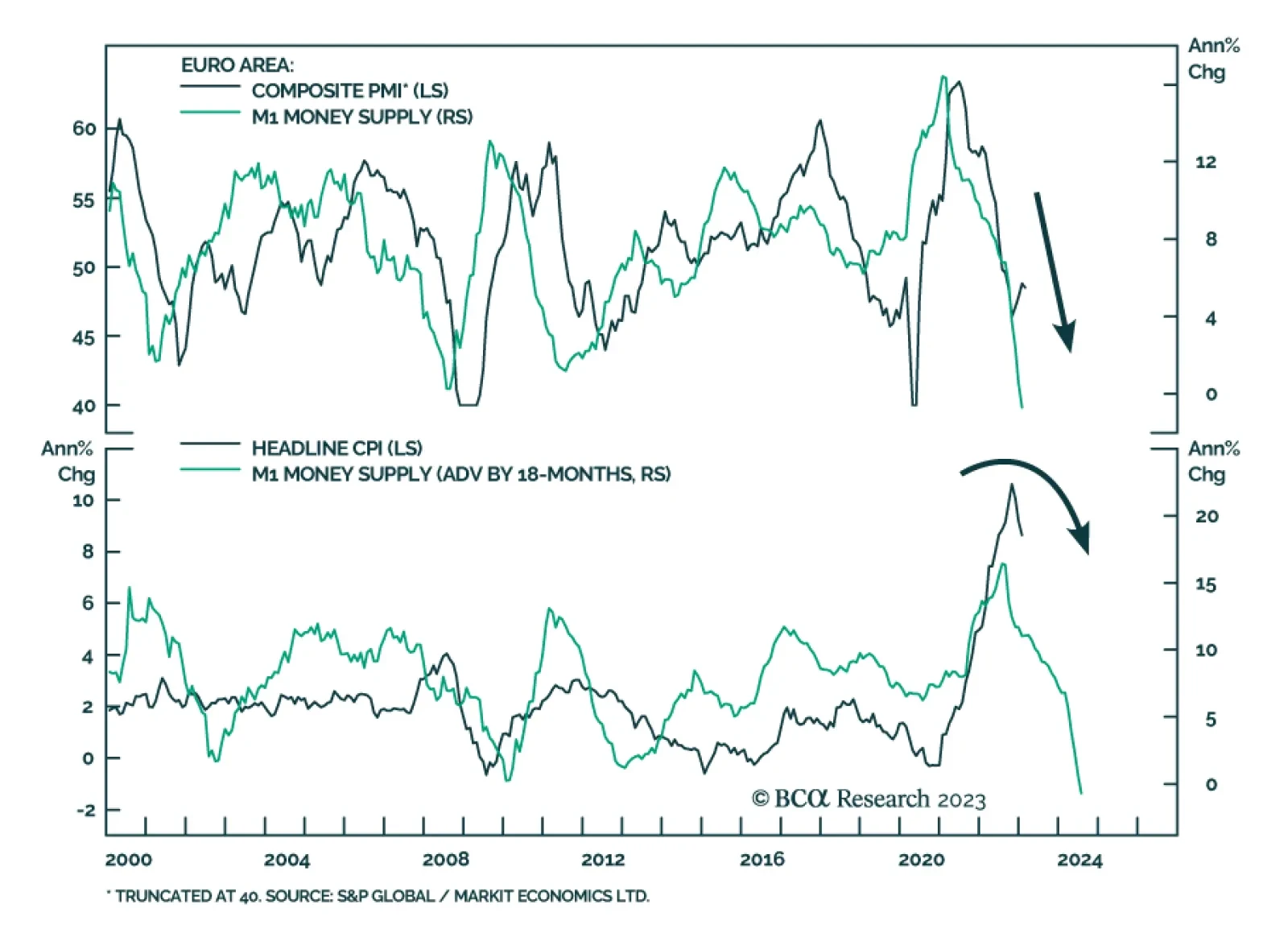

Euro Area monetary aggregates are showing the impact of tight ECB policy. M1 money supply – which includes currency in circulation and overnight deposits – declined by 0.7% y/y in January. The broader M3 measure of money supply growth continued to…

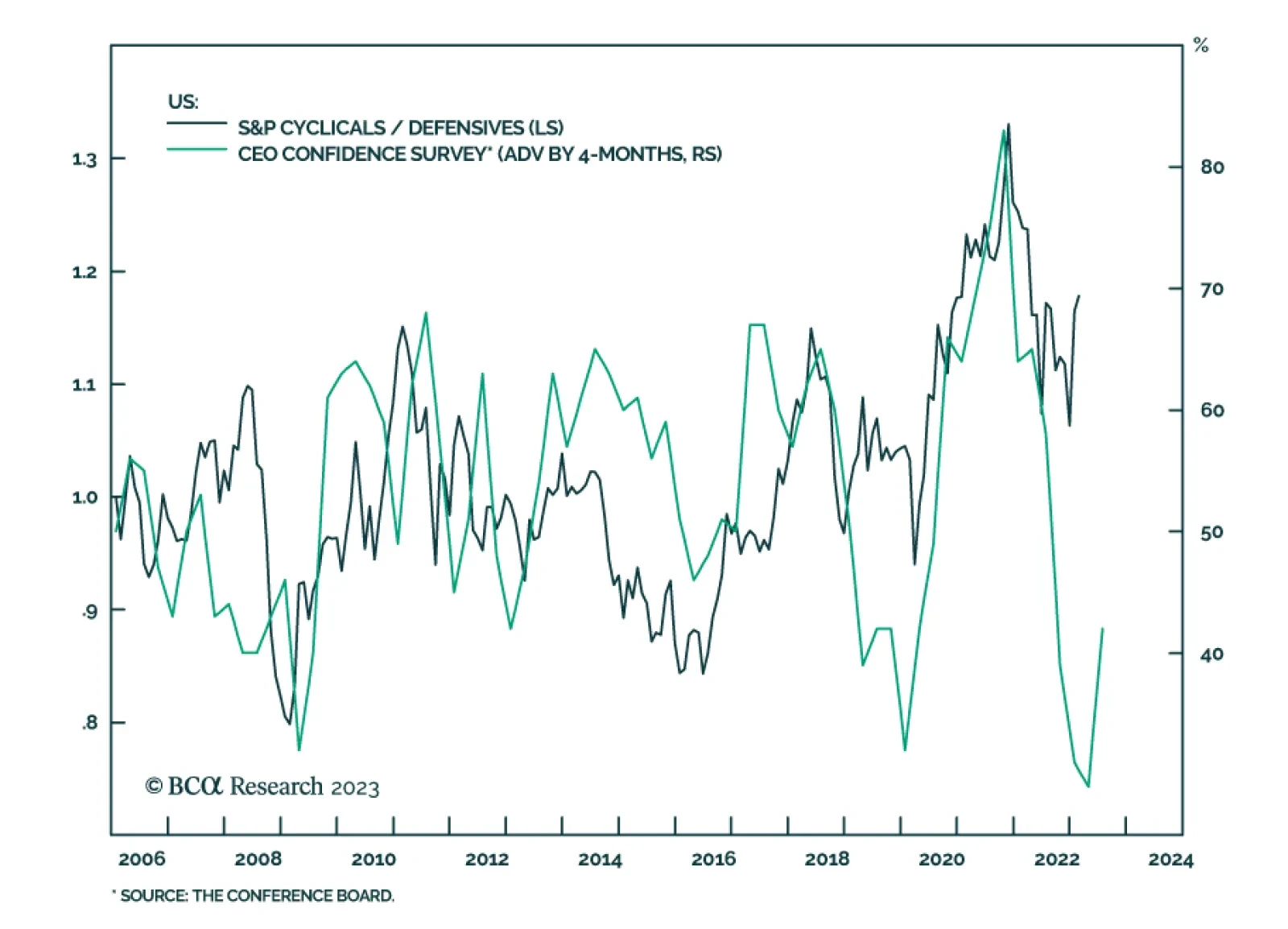

Results of the US Conference Board’s latest quarterly survey show an improvement in CEO Confidence in Q1. The share of CEOs reporting better economic conditions versus six months ago increased by 11 percentage points to 16% while the share of those indicating…

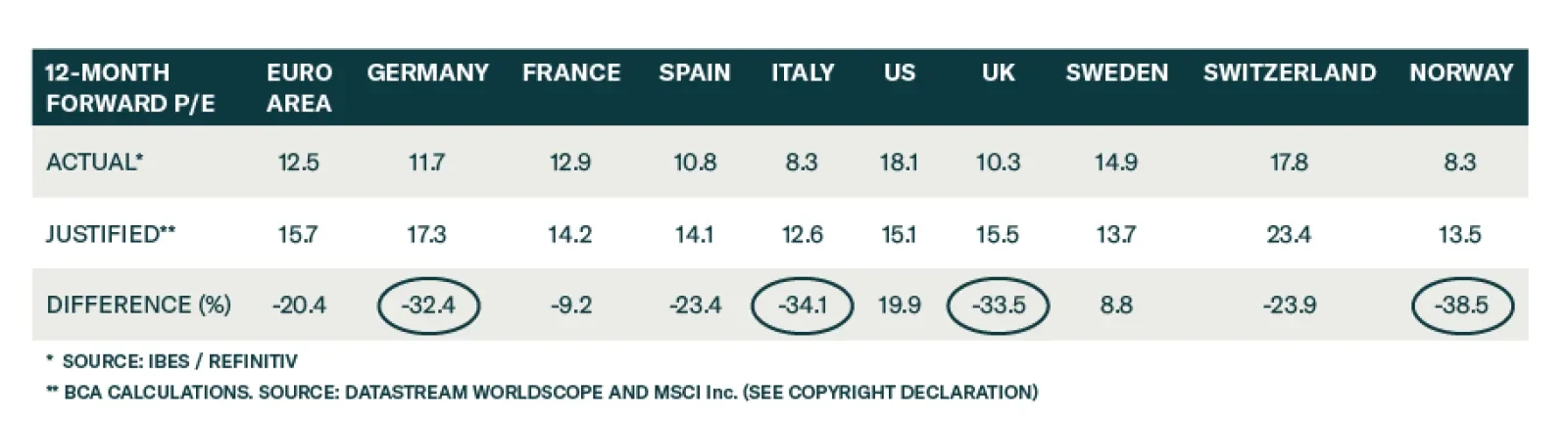

According to BCA Research’s European Investment Strategy service investors worried about the impact of higher yields on their equity portfolios should favor German, Norwegian, British, and Italian stocks in their portfolios compared to US, French, and Swedish…

This report considers the outlook for the US corporate credit cycle based on a suite of economic, monetary and corporate health indicators. We conclude that both the default rate and US corporate bond spreads will grind higher during the next 6-12 months.

It is easy to conclude that European equities are attractively valued by looking at multiples; however, a method rooted in fundamentals is essential to find out which bourses are genuinely cheap.

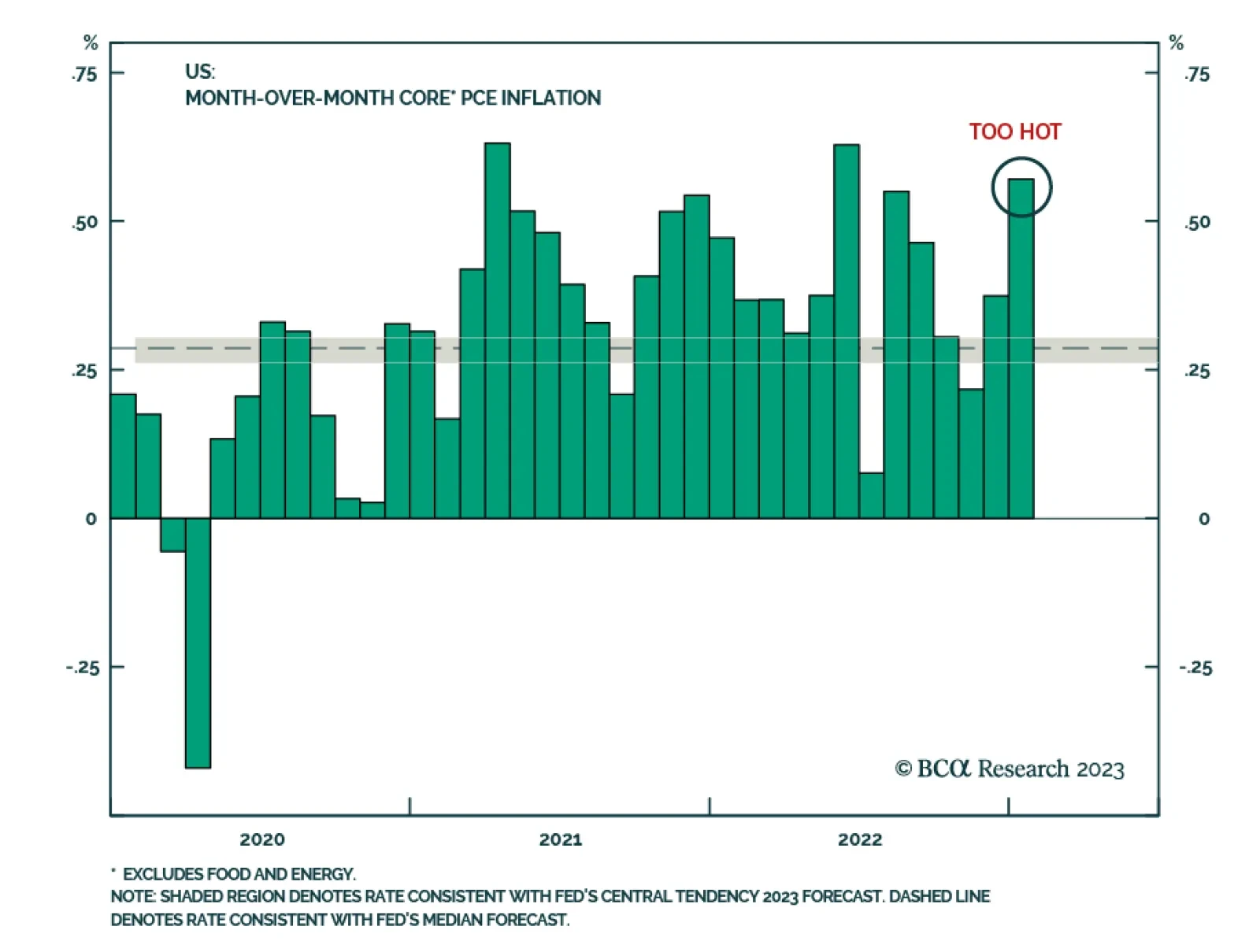

The January Personal Income and Outlays report delivered a positive signal about consumption, corroborating the signal from the CPI, employment and retail sales reports released earlier this month. The 0.6% m/m increase in personal income is an acceleration…

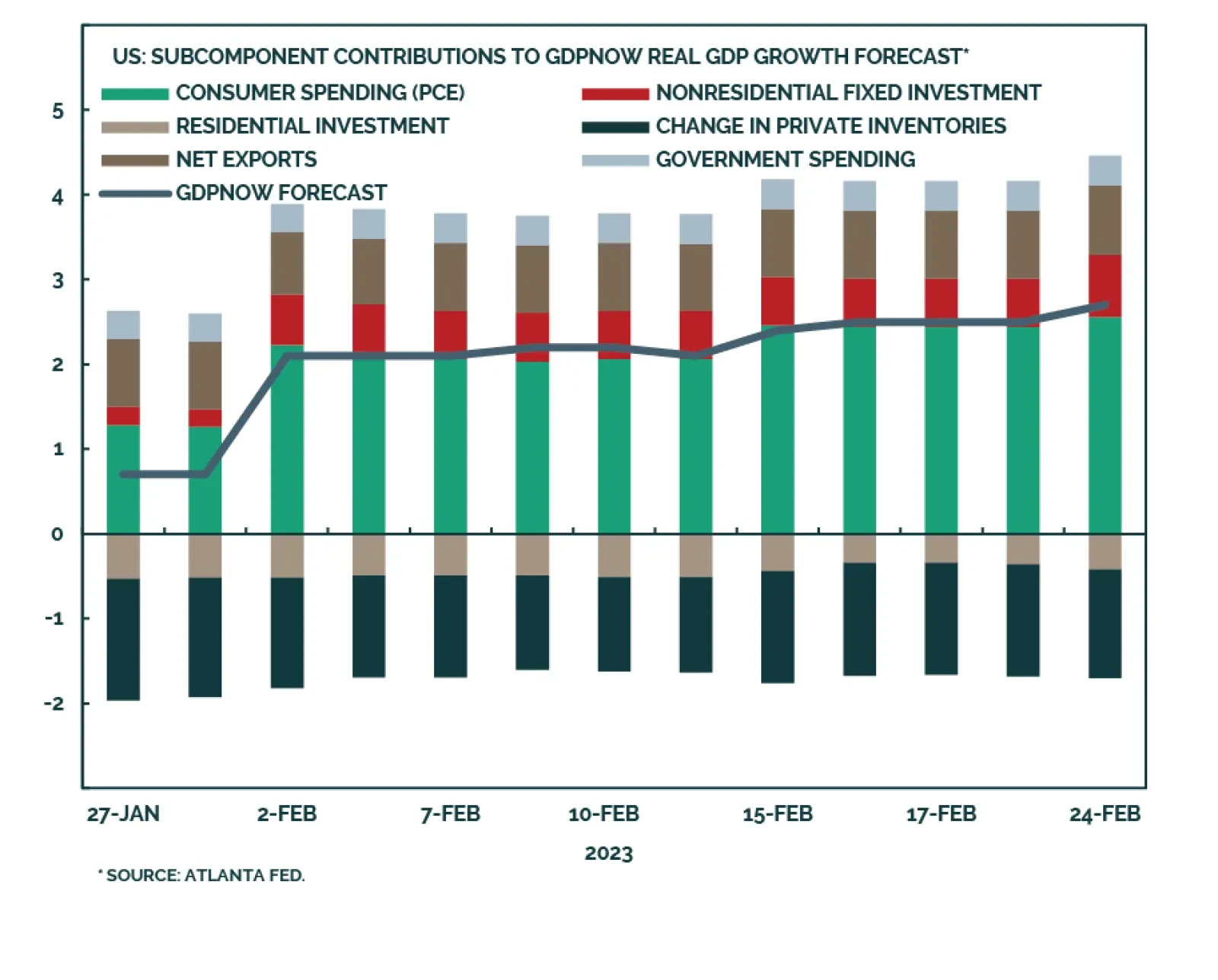

The latest reading from the Atlanta Fed’s GDPNow model estimates annualized US real GDP growth of 2.7% in Q1 2023. This is a significant improvement from its initial 0.7% estimate at the end of January. The latest upbeat reading reflects the consistent flow…

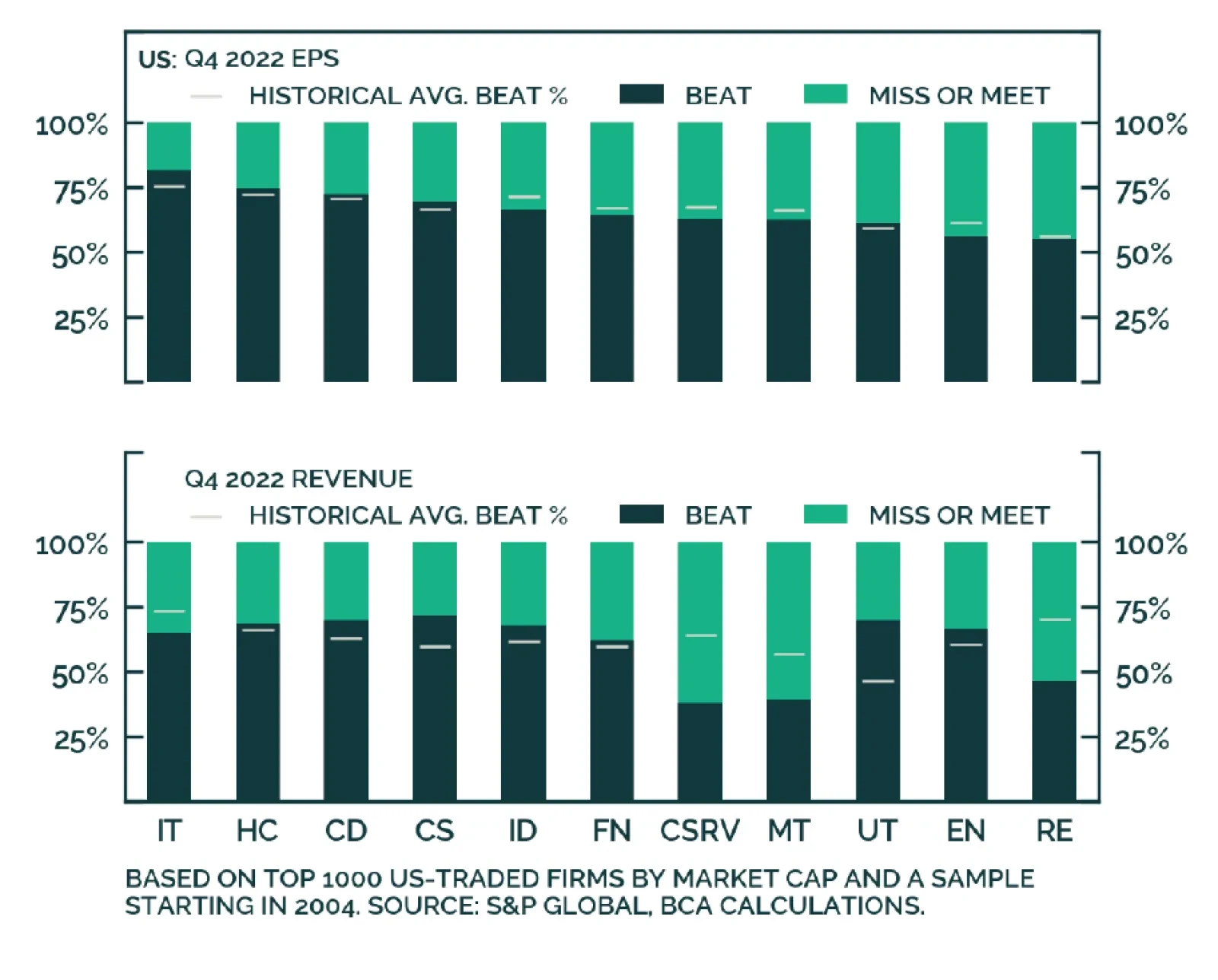

In a summer 2022 report, our colleagues in BCA Research’s Equity Analyzer service examined the one-day forward returns of stocks after an earnings release and found that firms that beat on both earnings and revenue tended to outperform their peers, while…