Developed Countries

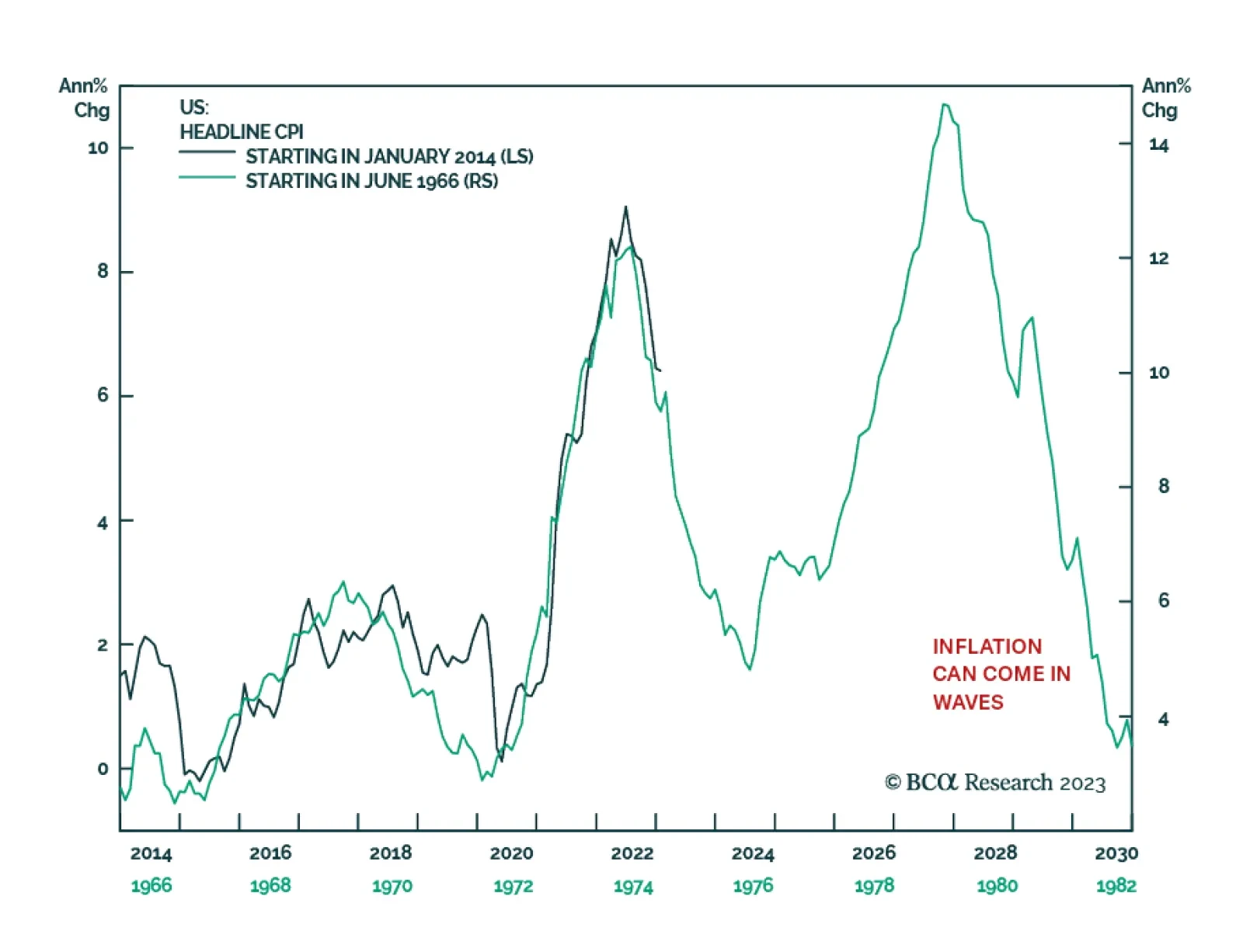

This week’s report considers the risk that inflation will be stickier than we anticipate, and looks at what a fair value for the 10-year Treasury yield might be in a scenario where the Fed keeps the policy rate on hold for a prolonged period.

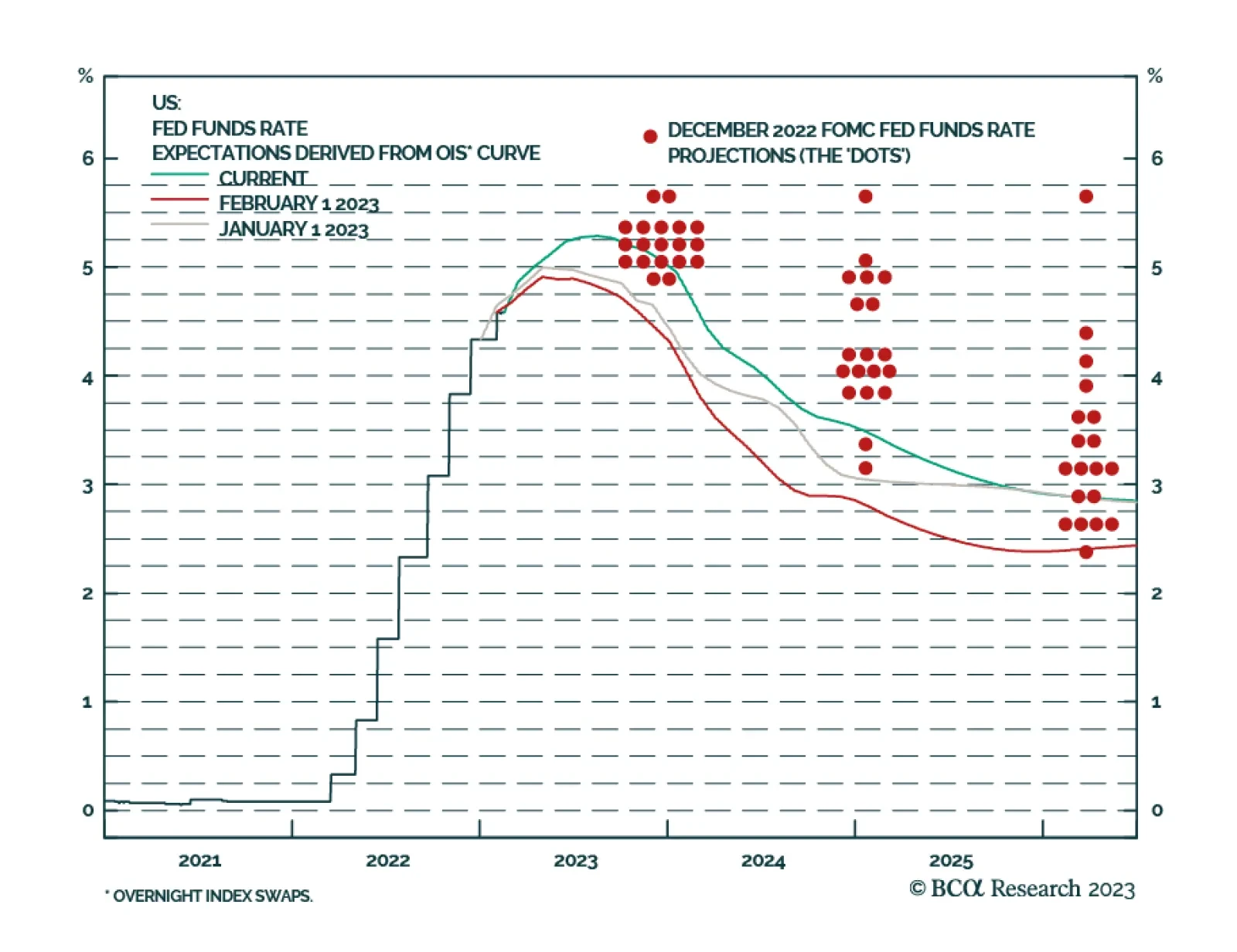

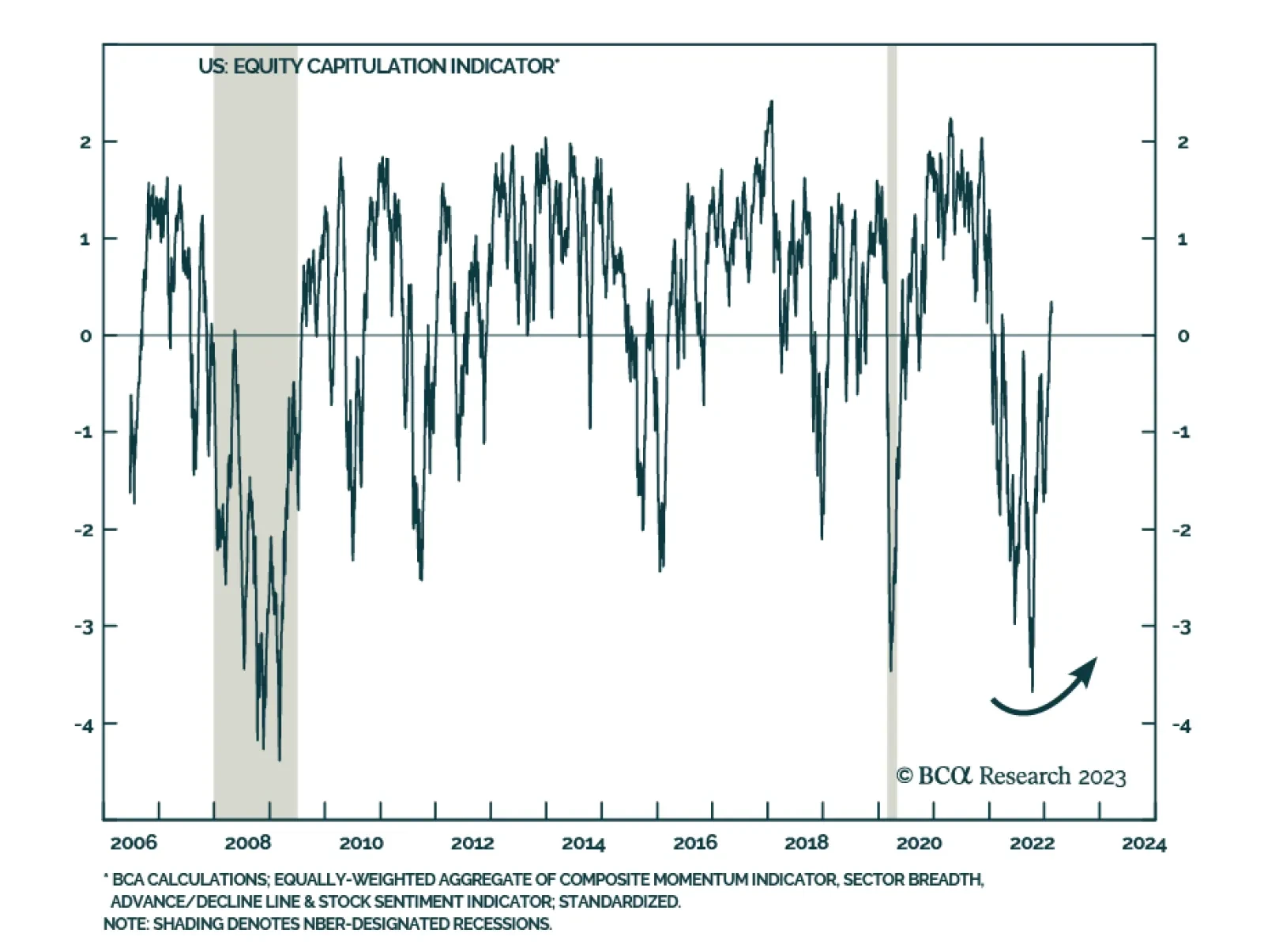

We refresh our 2023 plan of attack to reflect the latest data and several rounds of discussions with clients in virtual and face-to-face meetings. We continue to expect a meaningful first-half rally in the S&P 500, despite revising our expected terminal fed funds rate 25 basis points higher.

The US equity market is in the midst of an earnings contraction driven by slowing sales growth – a manifestation of the weakening economic demand and loss of corporate pricing power that accompany disinflation. The telecommunications industry is a defensive industry that faces many challenges: Low growth, cut-throat competition, and incessant demands for capital investment.

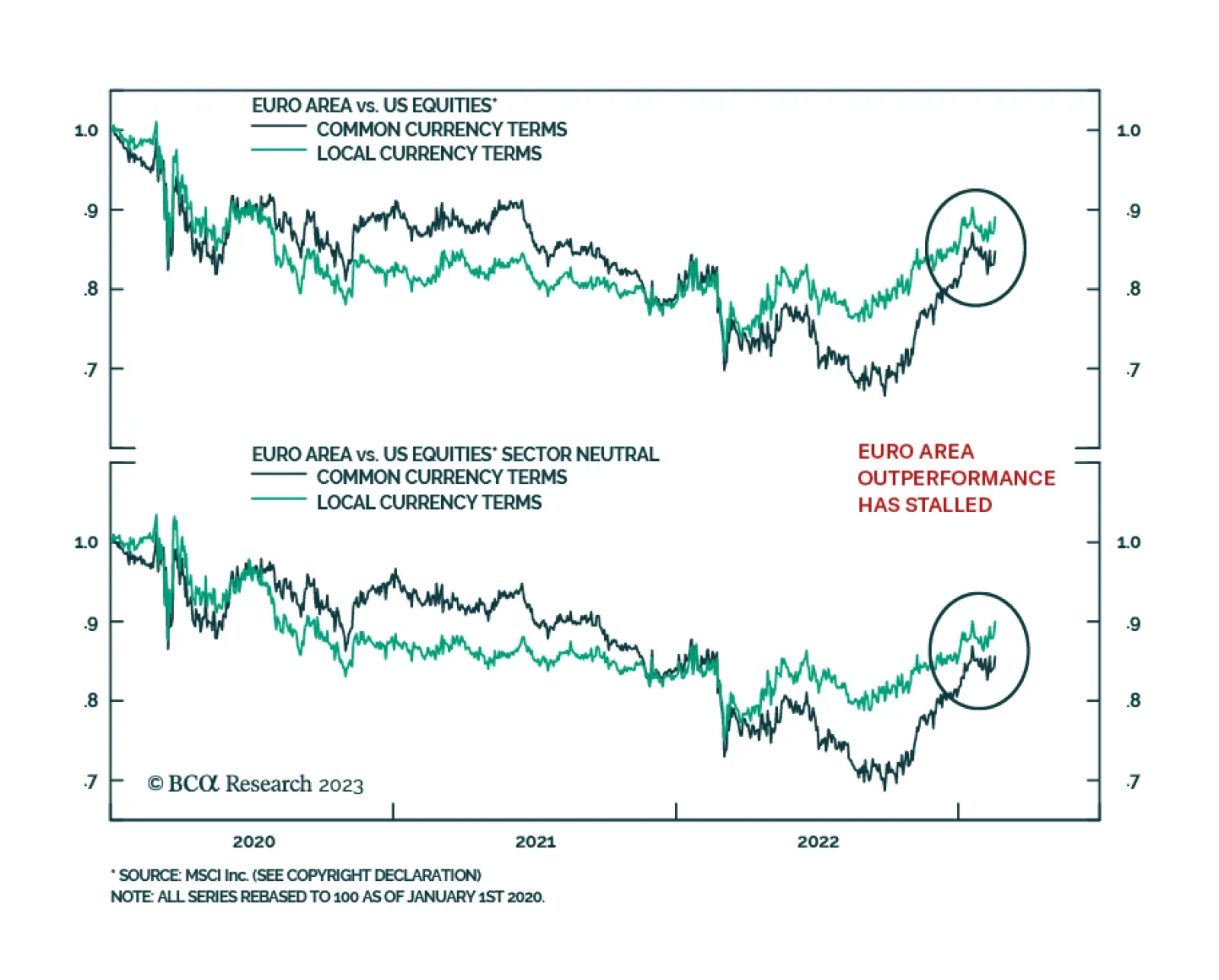

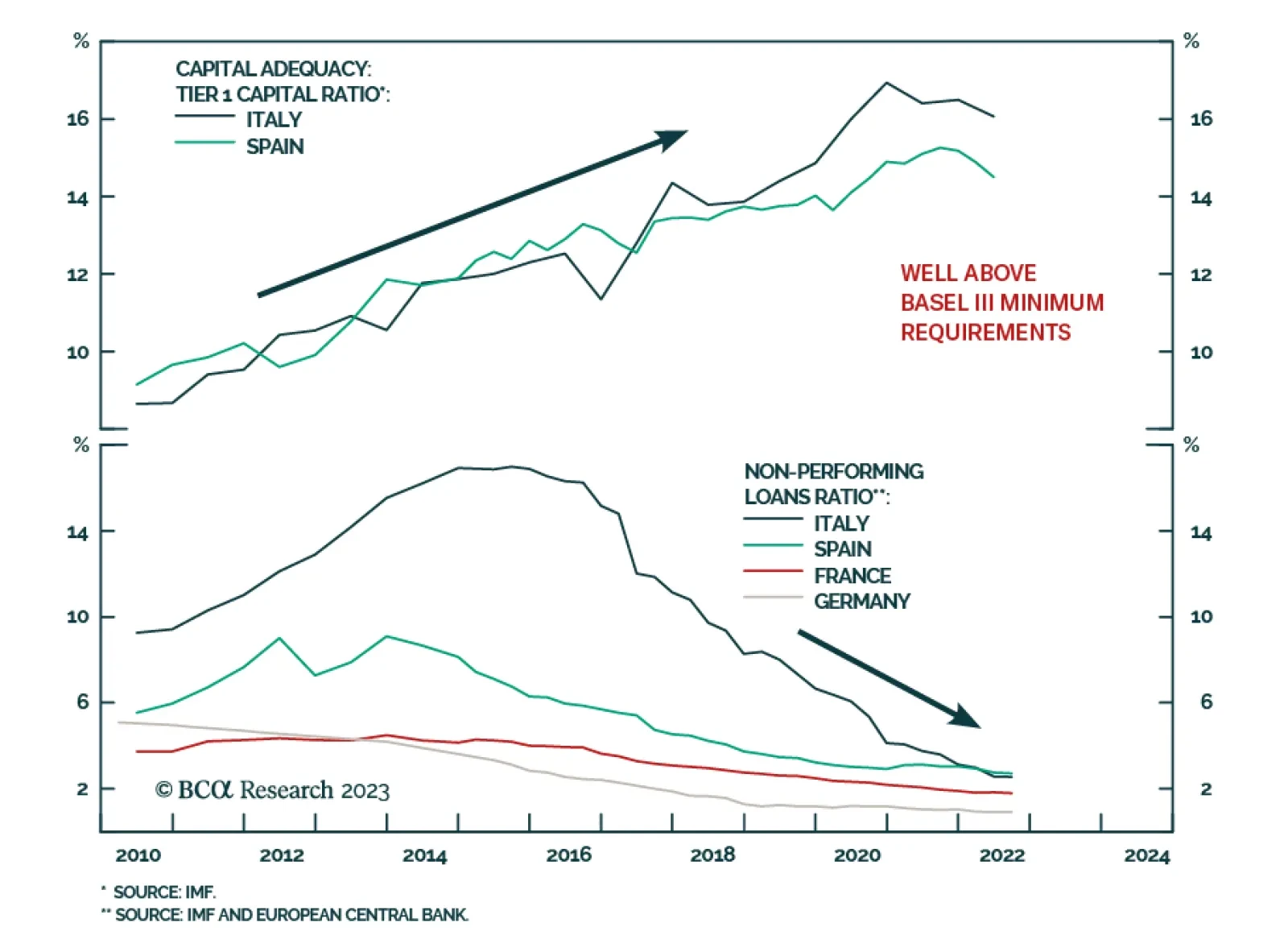

Long-term drivers, including the growing ability of banks to returns cash to shareholders, point toward a strong structural performance for European financials. However, the ECB’s aggressive tightening campaign could still spoil the party.