Developed Countries

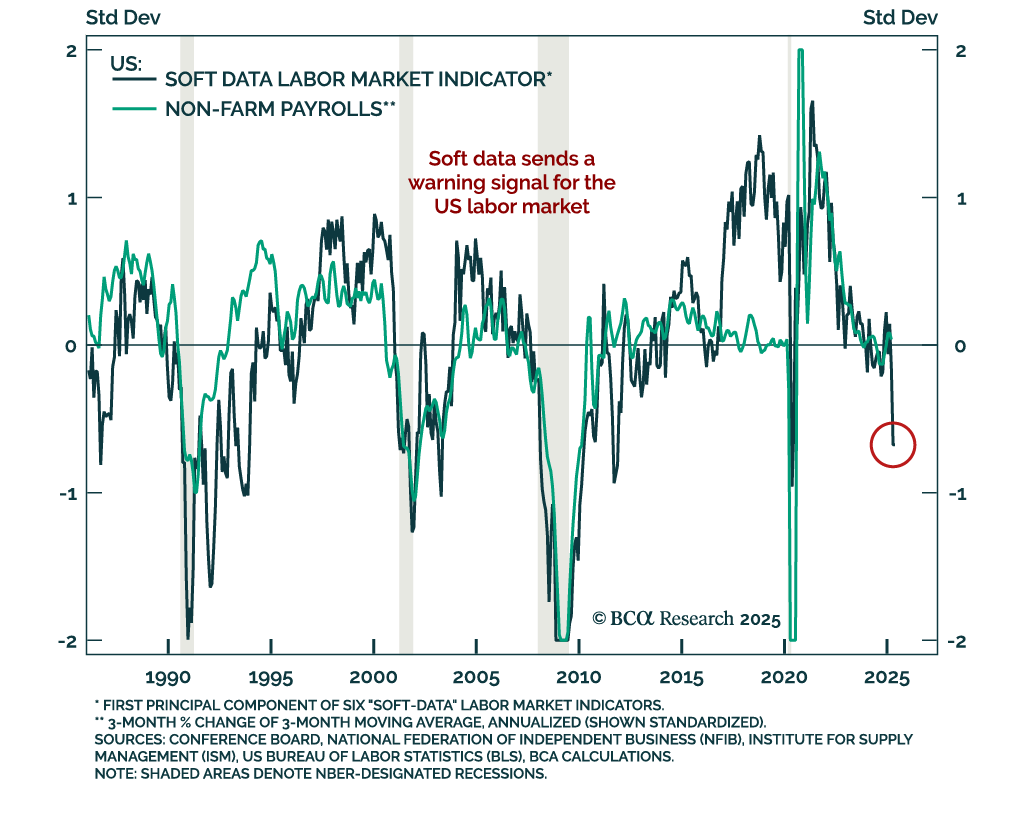

Soft data for the US labor market has turned sharply lower, reinforcing the case for a defensive asset allocation. Our Chart Of The Week comes from Miroslav Aradski from our Global Investment Strategy team. While it may take months for the tariff shock and…

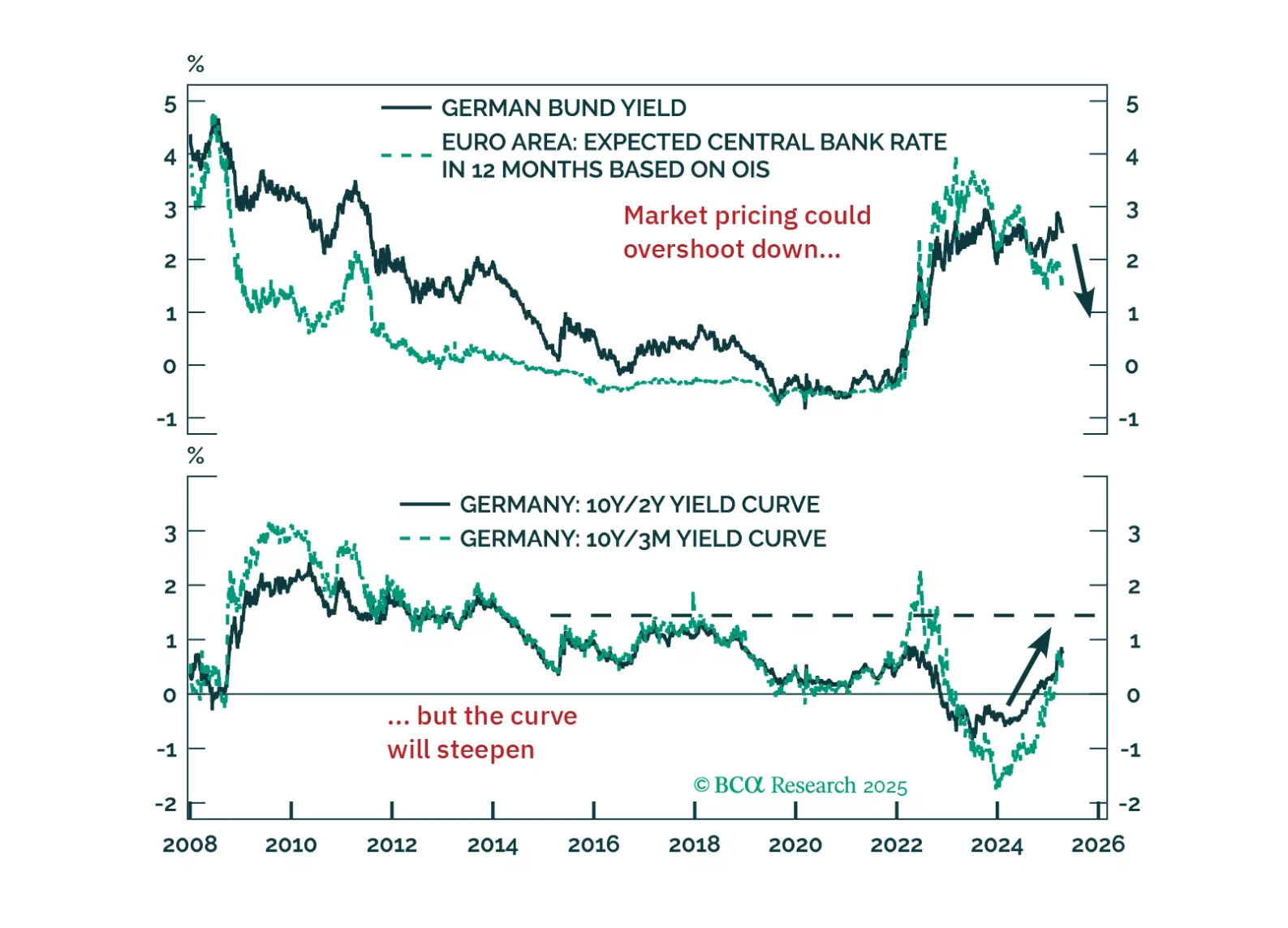

Europe’s deflation problem is getting harder to ignore. This week’s ECB cut is just the beginning — tariffs, the euro’s rally, and softening demand all point to more easing ahead. We explain what it means for yields, equities, and EUR/USD.

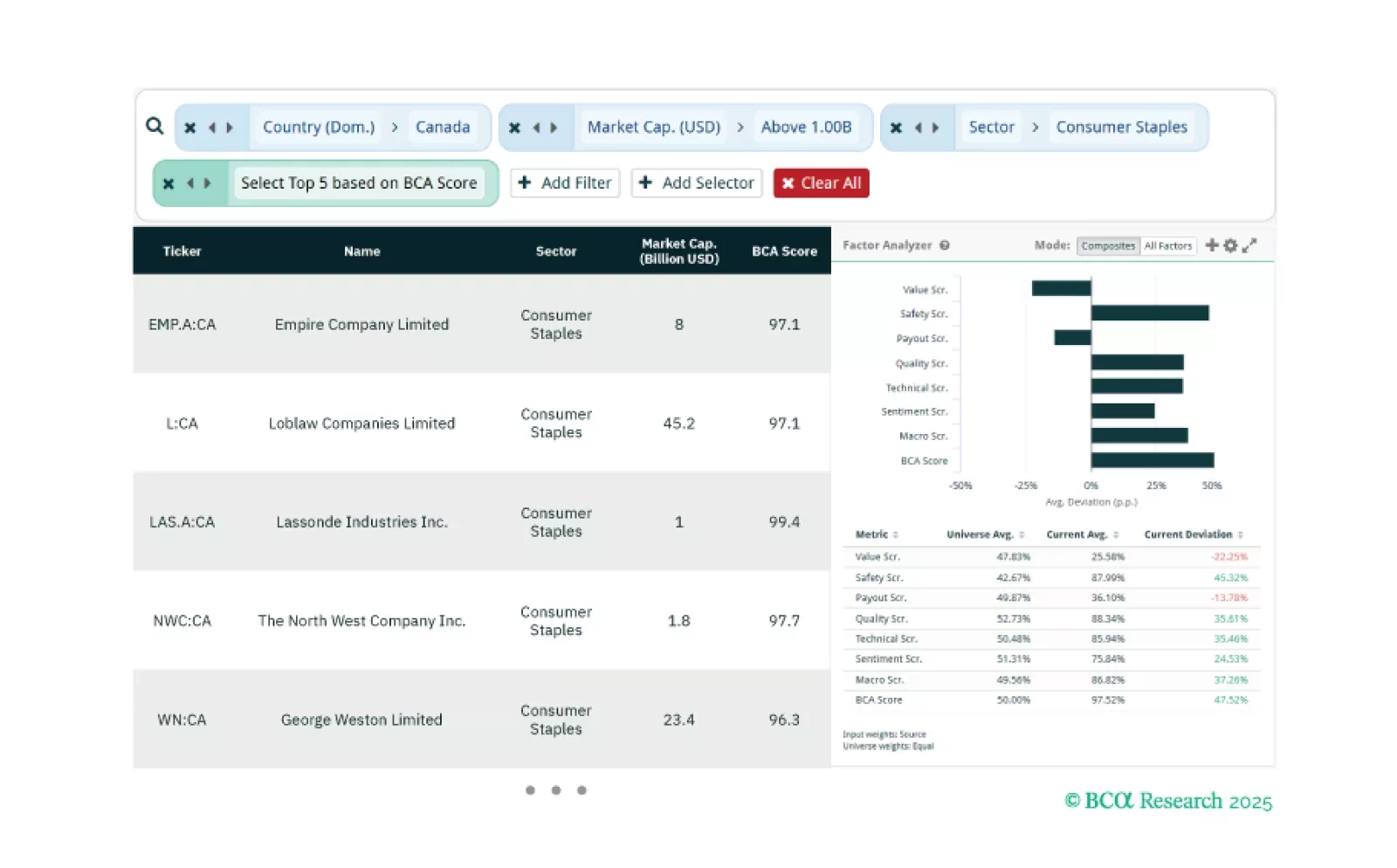

This week, our three screeners cover equity plays in: Canadian Consumer Staples, high-beta Swedish equities, and factor plays across global equities.

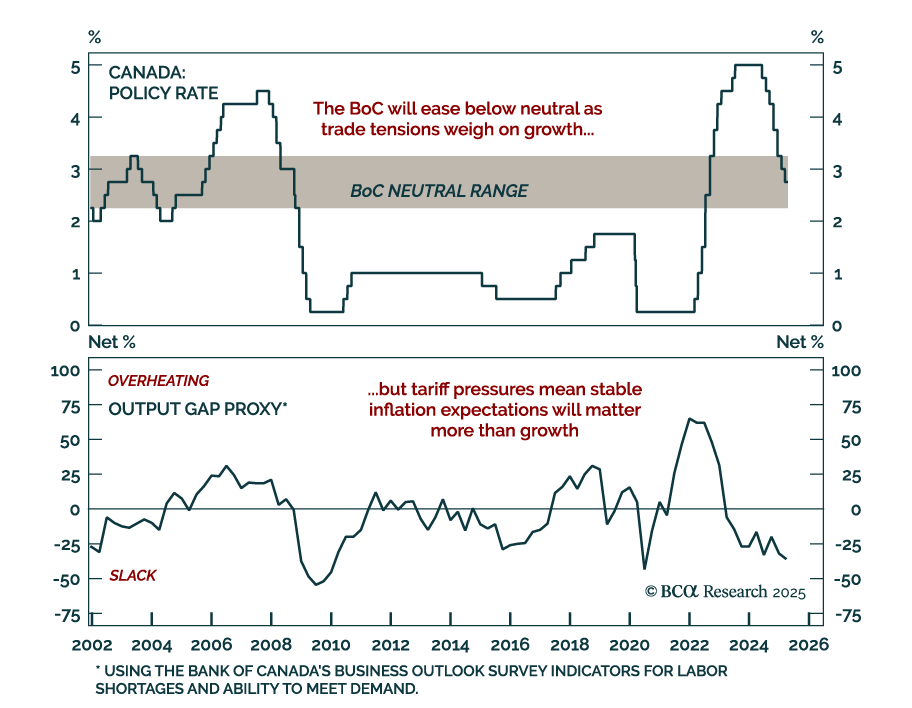

After seven consecutive cuts brought policy into neutral territory, the BoC held its deposit rate at 2.75% reinforcing our neutral-to-negative stance on Canadian government bonds. With policy now within the 2.25%-3.25% neutral range, the Bank comfortably…

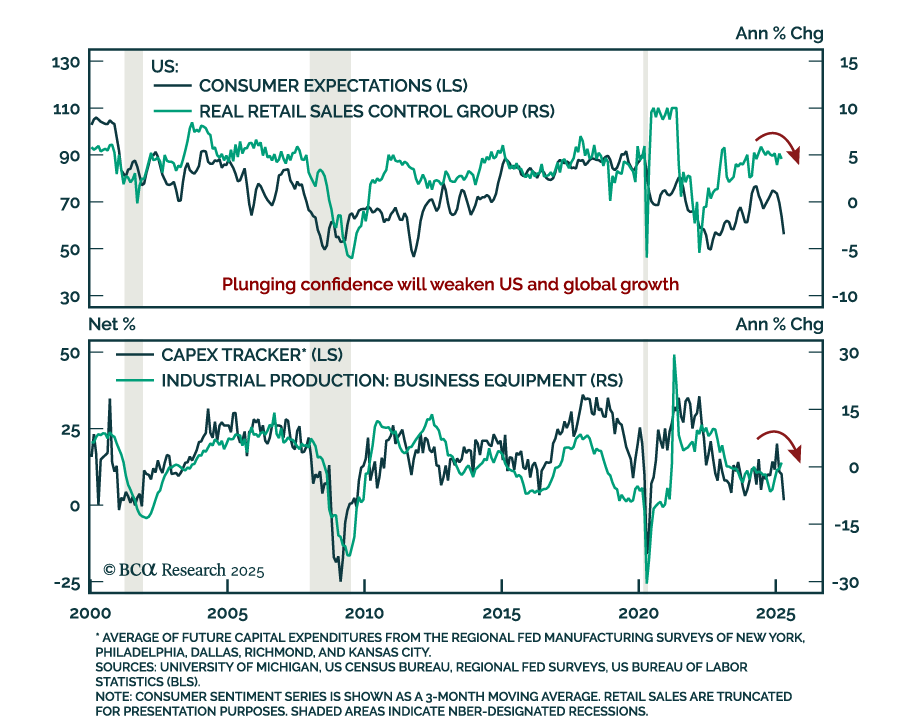

Soft data continues to deteriorate and hard data will soon follow, reinforcing our defensive asset allocation. Consumer and business confidence have plunged as policy uncertainty and inflation expectations rise, with spending, hiring and capex plans…

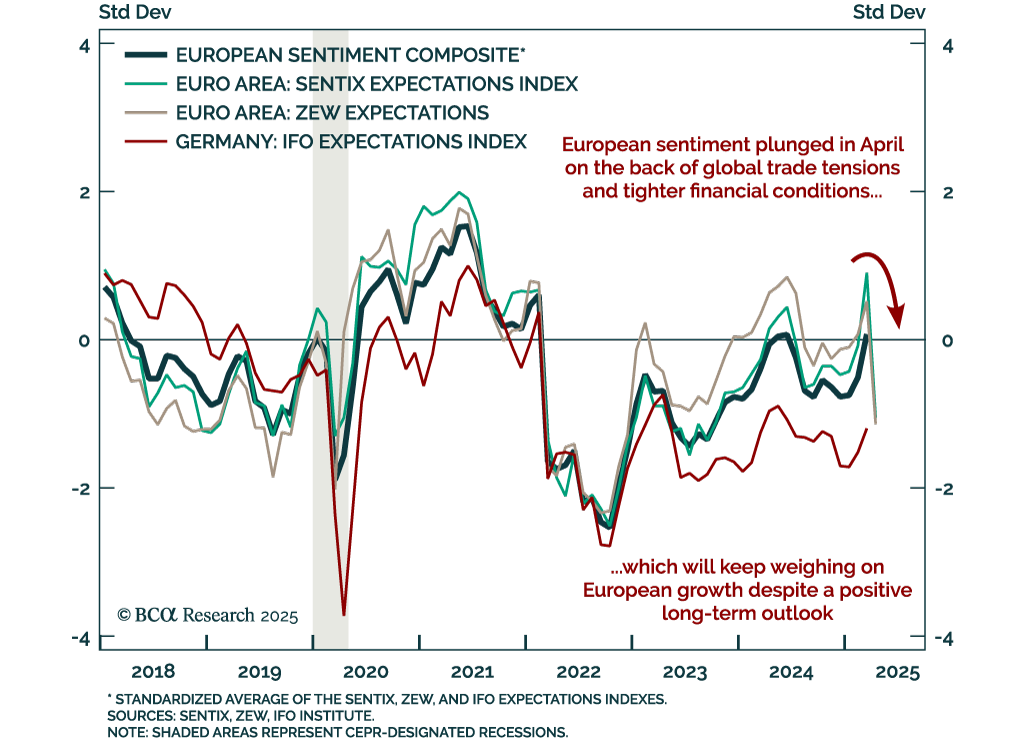

Eurozone sentiment has sharply deteriorated, reinforcing a cautious stance on European assets over the next 6 to 12 months. The April ZEW expectations index for the eurozone collapsed to -18.5 from 39.8, while Germany’s gauge also plunged and missed…

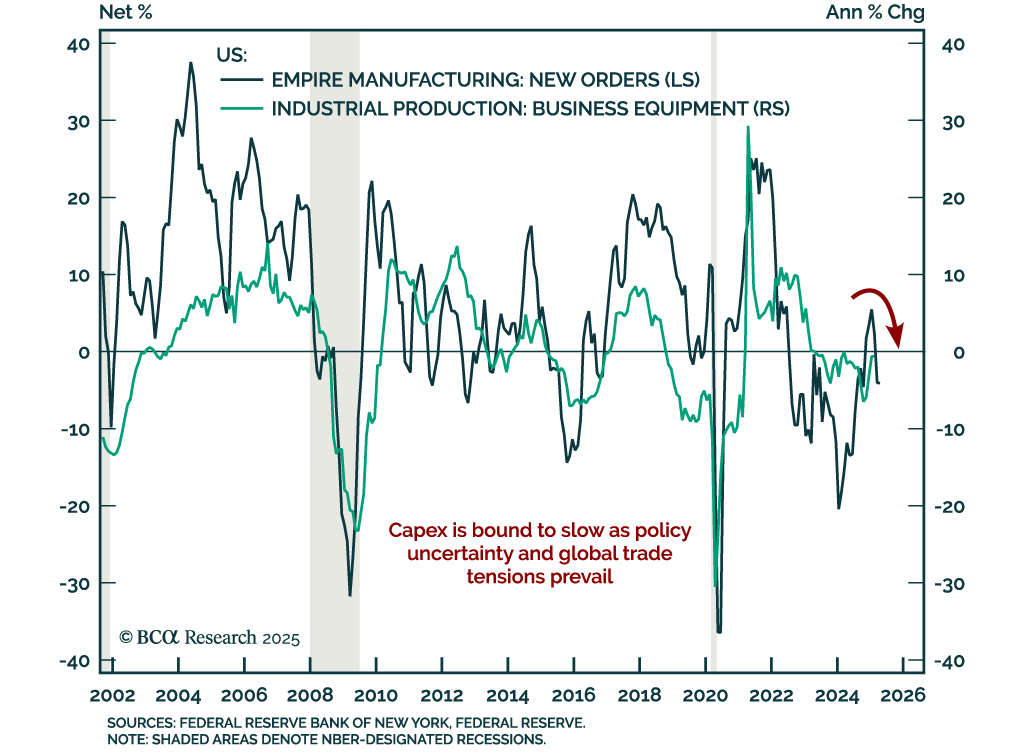

The NY Fed Empire Manufacturing survey adds to recent stagflationary worries, reinforcing our underweight in risk assets and overweight in government bonds. The general business conditions index rose slightly to -8.1 but remains in contraction, while the…

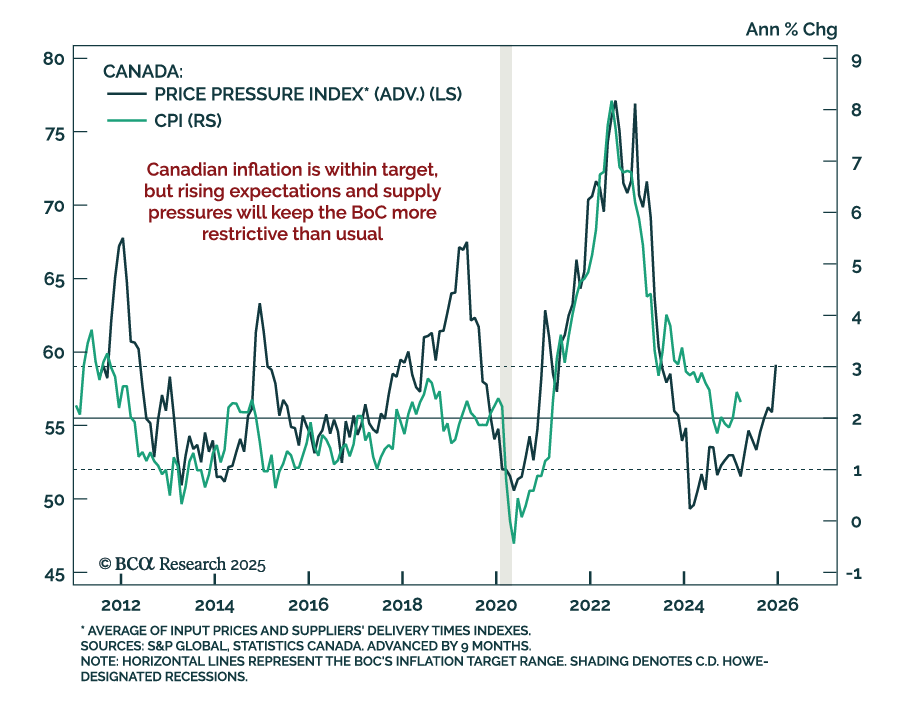

Cooler inflation will not shift the BoC’s stance, as stagflation limits potential easing, keeping us neutral on Canadian bonds. In March, headline CPI slowed more than expected to 2.3% y/y from 2.6%. However, lower energy prices drove much of the downside…

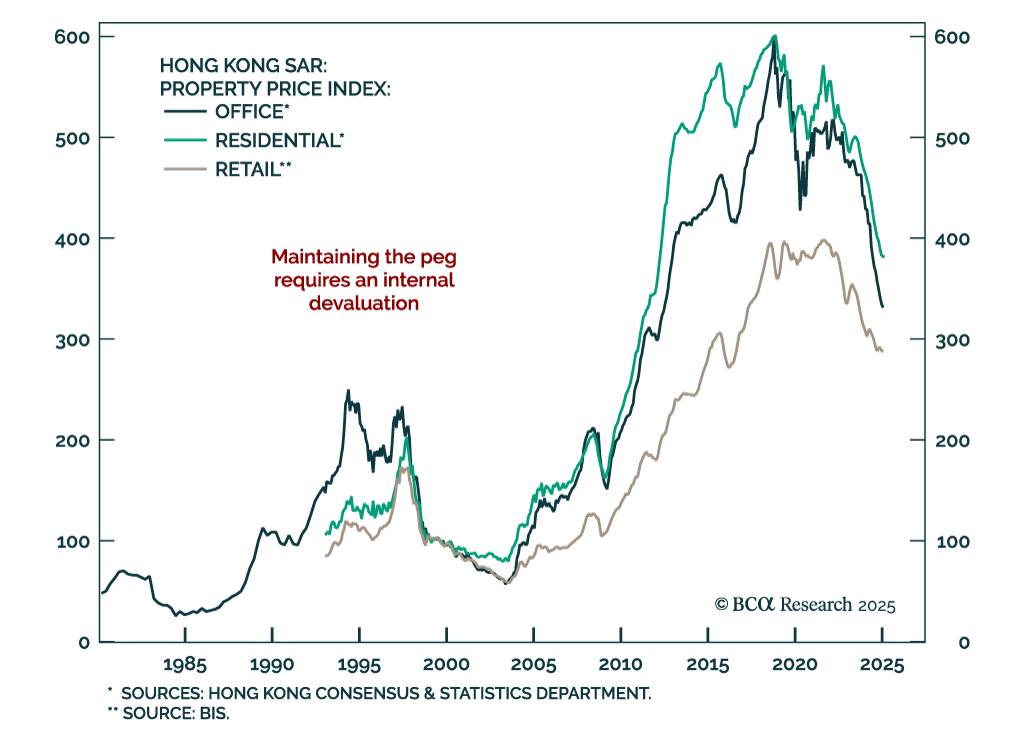

Our FX strategists expect the HKD peg to hold, but at the cost of prolonged economic weakness and debt deflation in Hong Kong. Interest rates remain too high for the local economy, yet monetary easing is off-limits due to the peg.The currency’s…

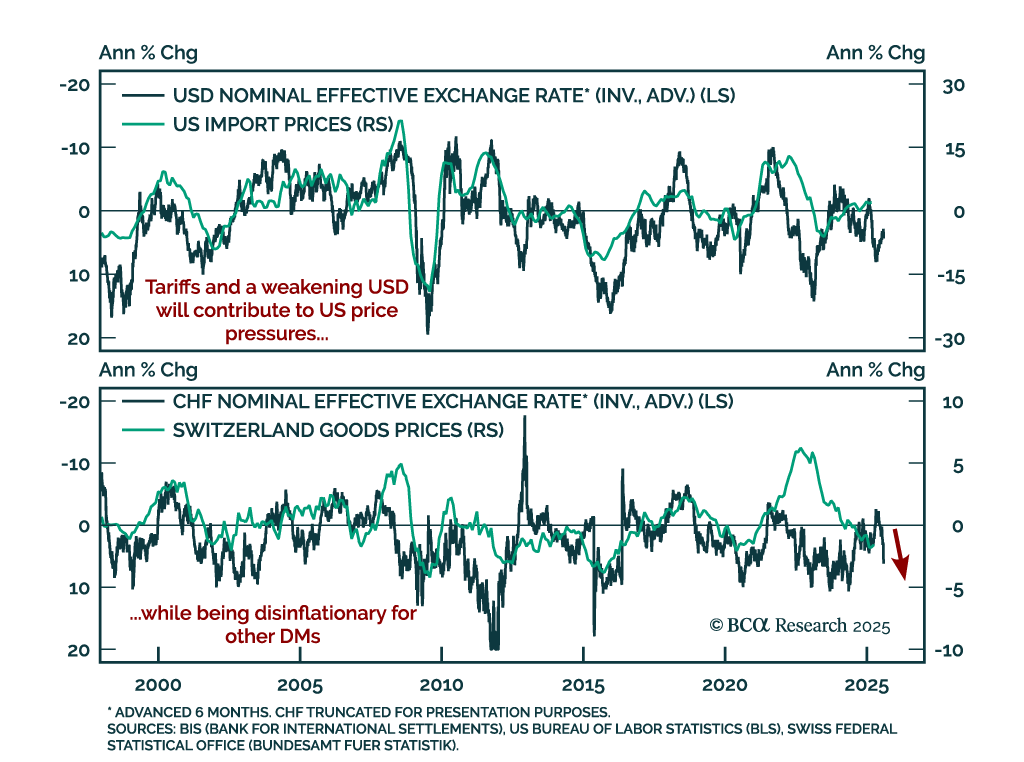

Tariff-driven inflation is diverging across economies, with the US facing mounting pressures while disinflation persists elsewhere. In theory, US tariffs should strengthen the dollar and weaken targeted currencies. In practice, the opposite has occurred: The…