Developed Countries

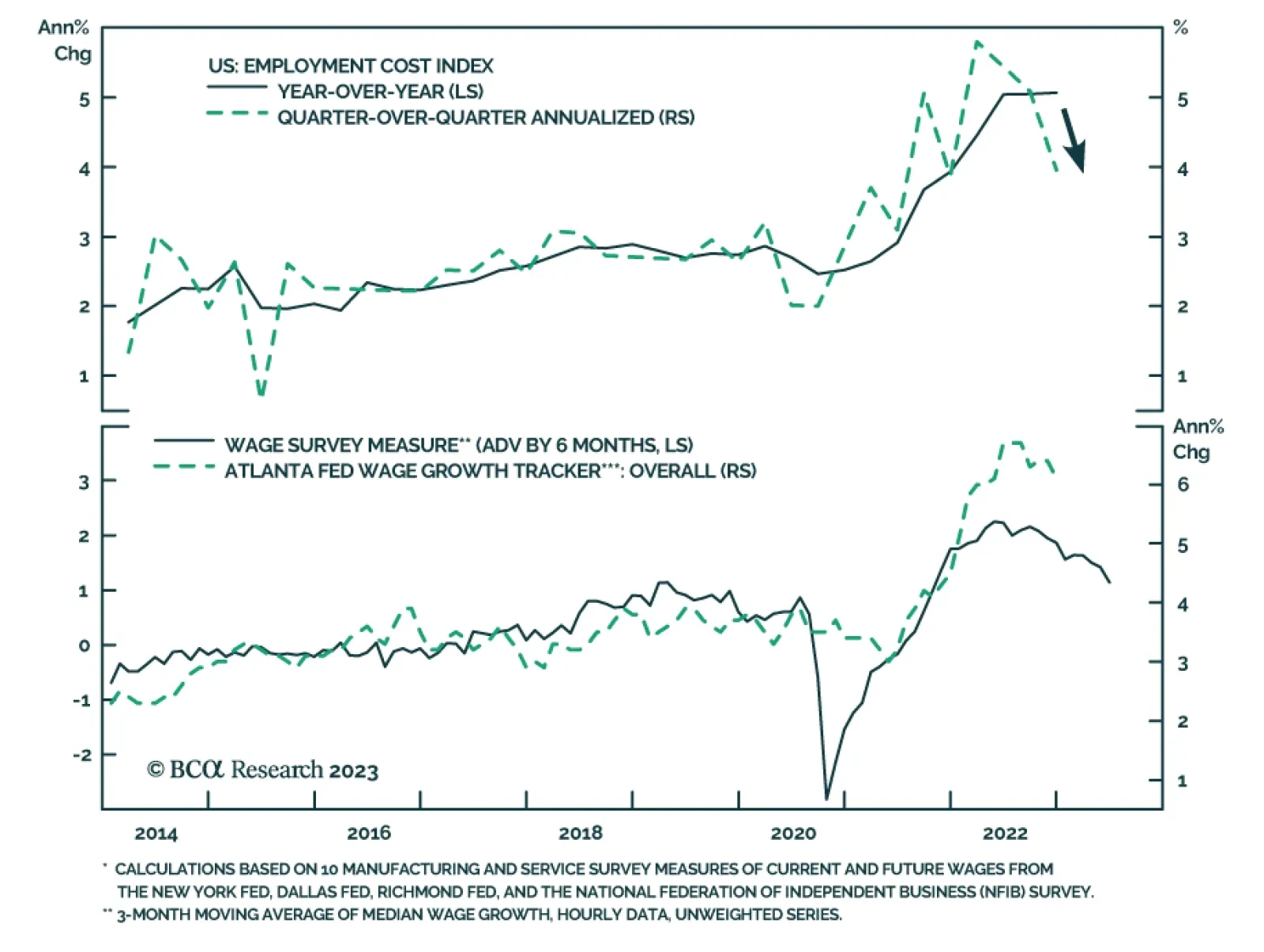

The Employment Cost Index decelerated to a lower-than-expected 1.0% q/q in Q4 following 1.2%, corroborating several other indicators suggesting that wage growth is moderating in the US. Compensation within goods-producing industries grew at a constant 0.9%…

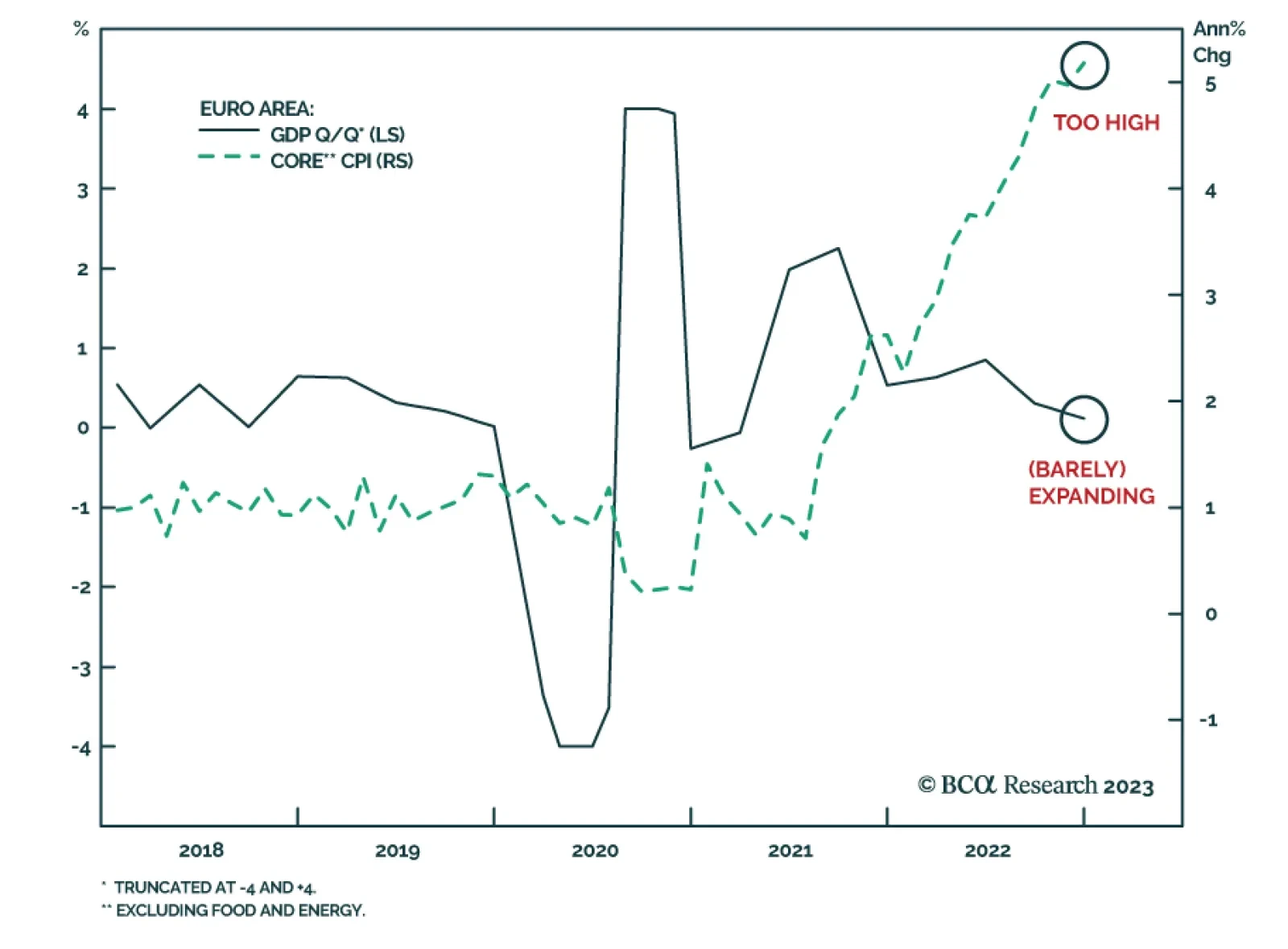

The preliminary GDP estimate suggests that the Euro Area economy expanded by 0.1% q/q in Q4 2022, beating expectations of a 0.1% q/q contraction. The improving energy situation due to milder-than-anticipated weather, as well as generous fiscal support…

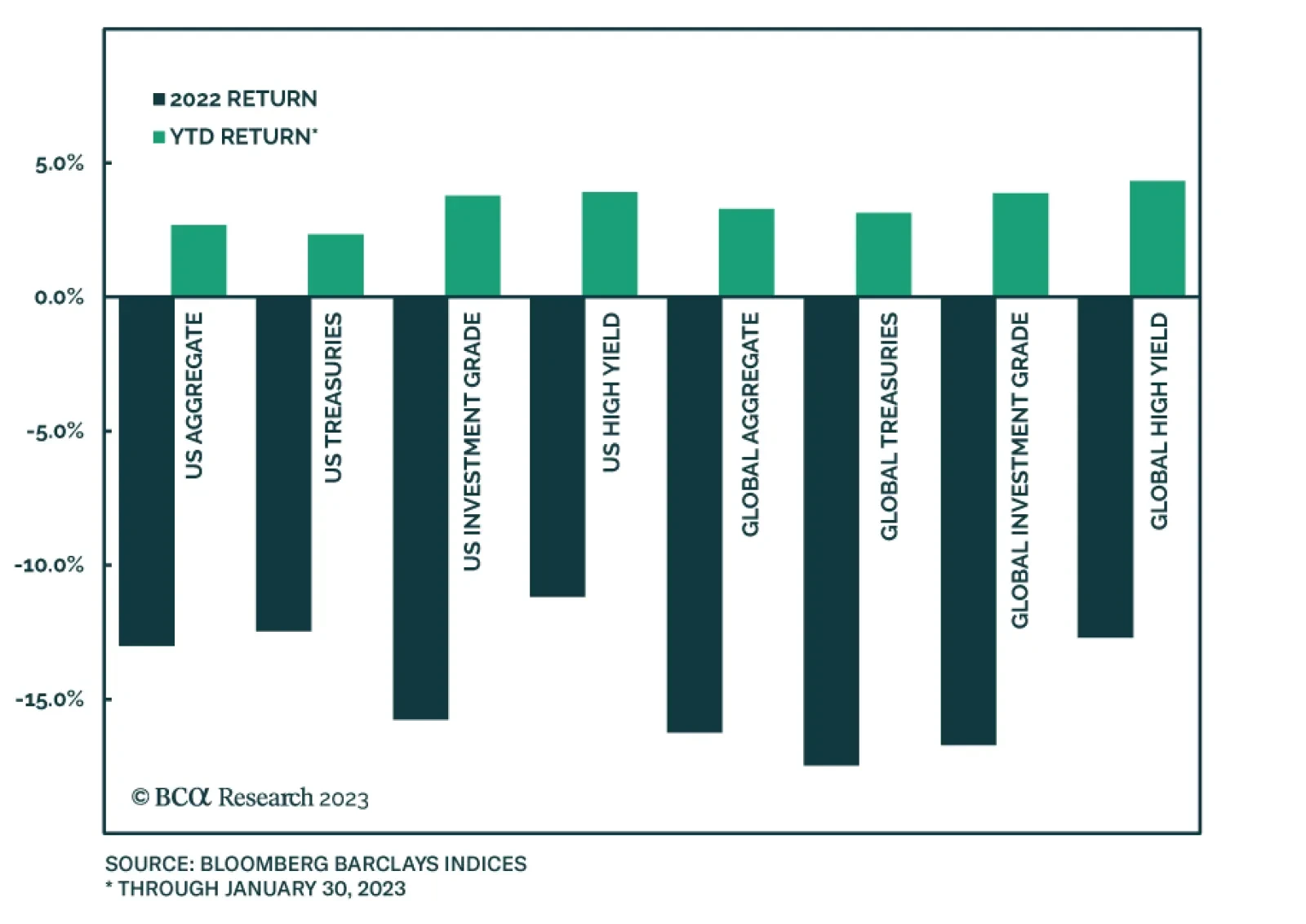

Bonds started off the new year with a bang. So far in 2023, the Barclays US and Global Aggregate indices have returned 2.7% and 3.3%, respectively. These gains come after last year’s historic broad-based bond market selloff when the global monetary policy…

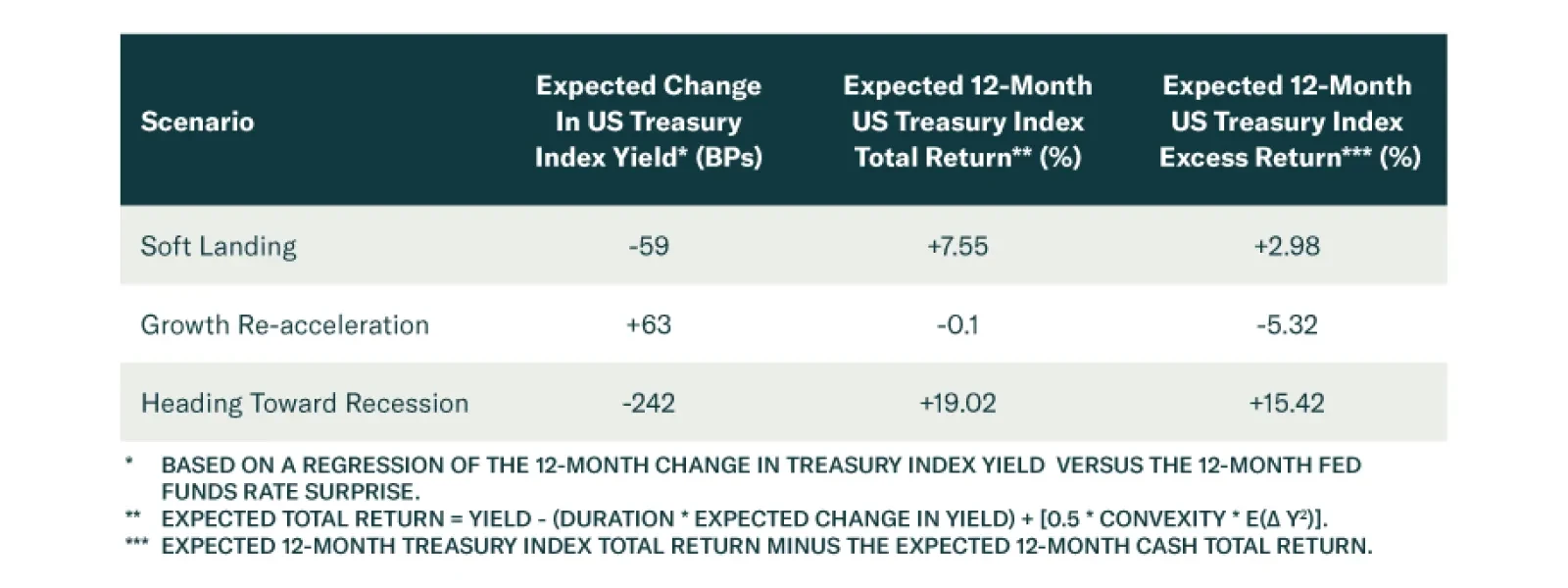

According to BCA Research’s US Bond Strategy service, US Treasuries have limited downside, even in relatively optimistic economic scenarios, but considerable upside in a recessionary scenario. They devise three plausible scenarios for how the US economy…

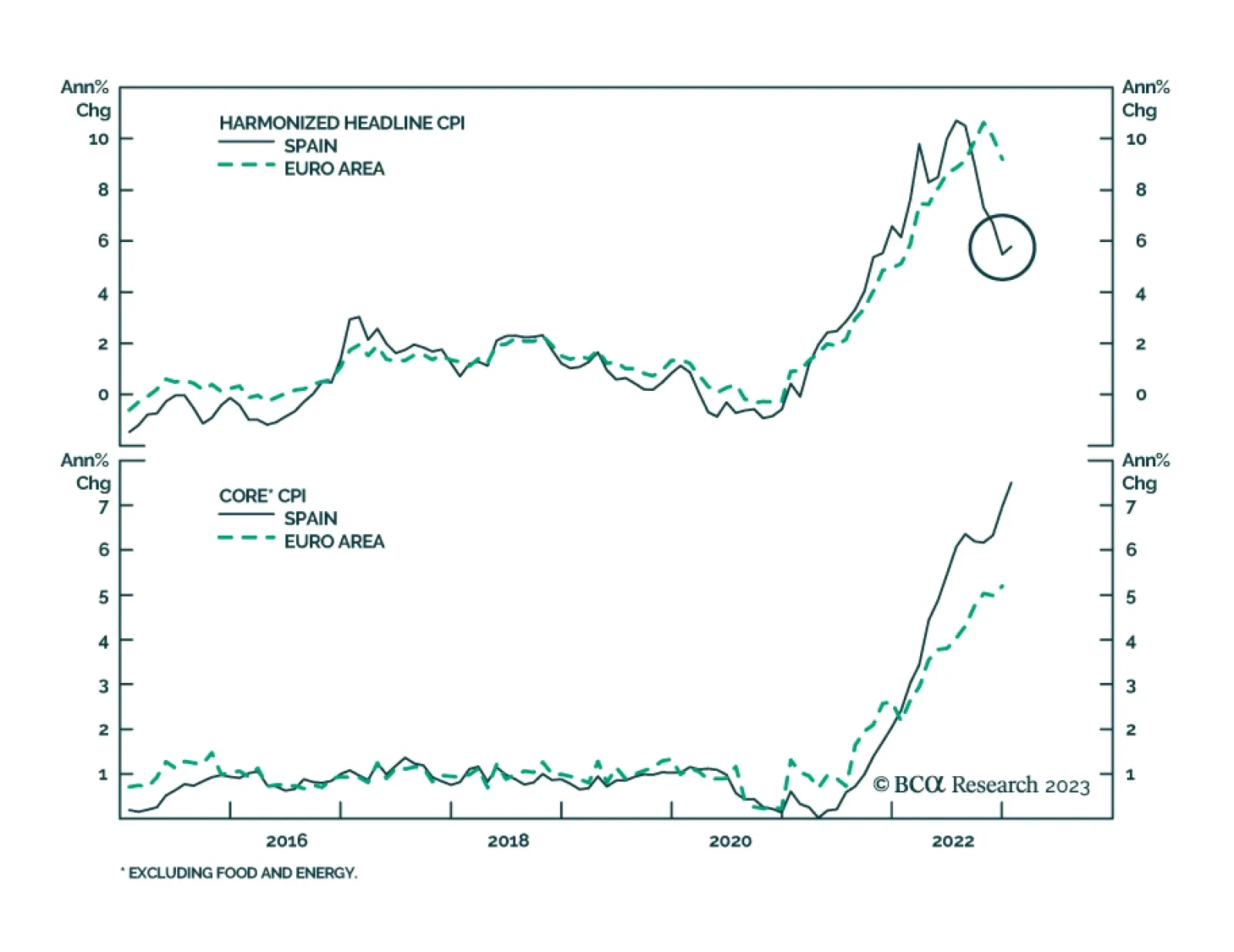

Preliminary estimates suggest that Spanish headline harmonized CPI inflation (HICP) accelerated to 5.8% y/y in January, from 5.5% y/y, largely surpassing expectations for a moderation to 4.8% y/y. A reacceleration of fuel prices compared to January 2022, as…

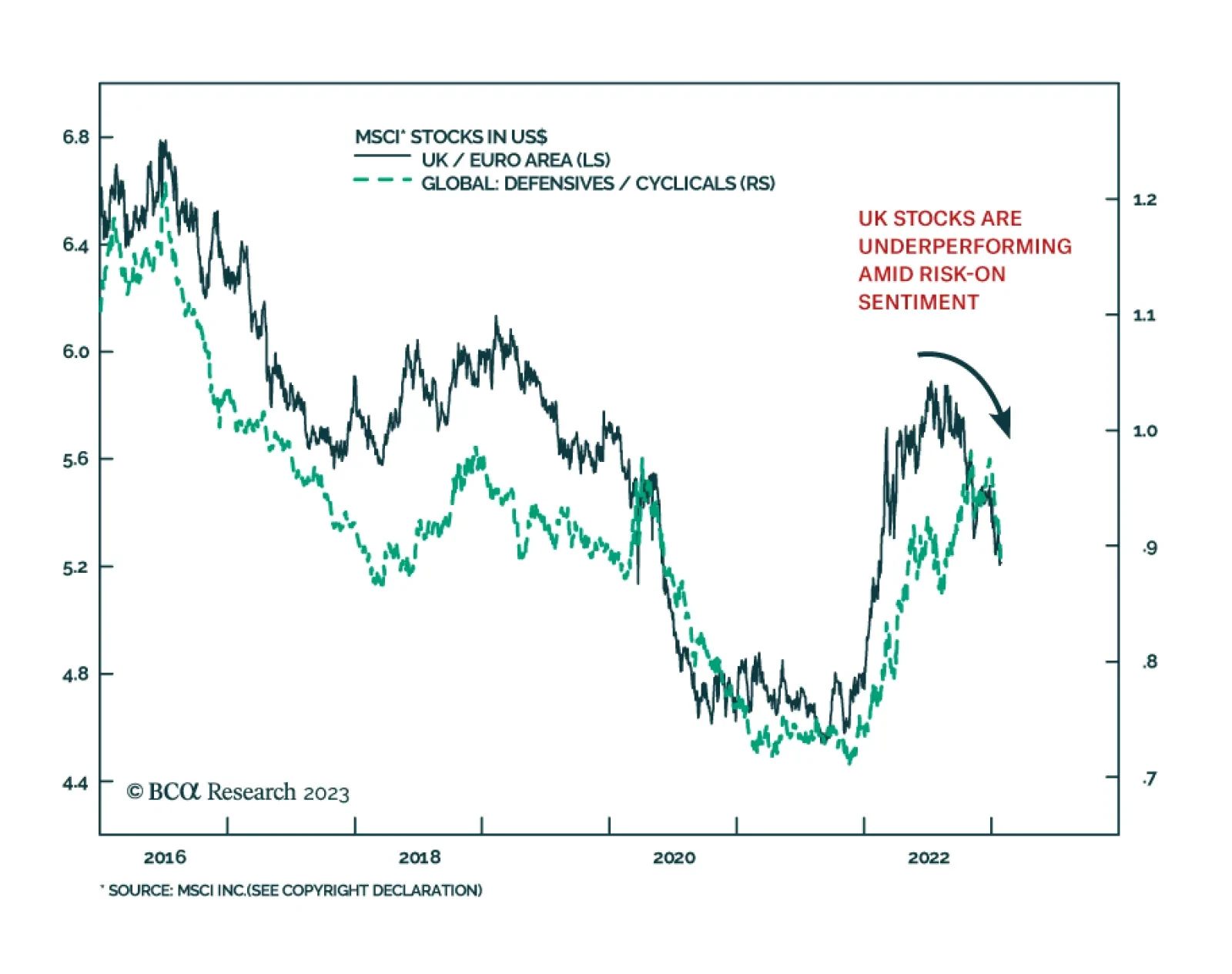

UK stocks have been underperforming their Eurozone peers recently. The MSCI Euro Area index’s 39% gain in the four months since its trough dwarfs the UK benchmark’s 27% increase since its September 27 bottom. Notably, this comes after a period of comparative…

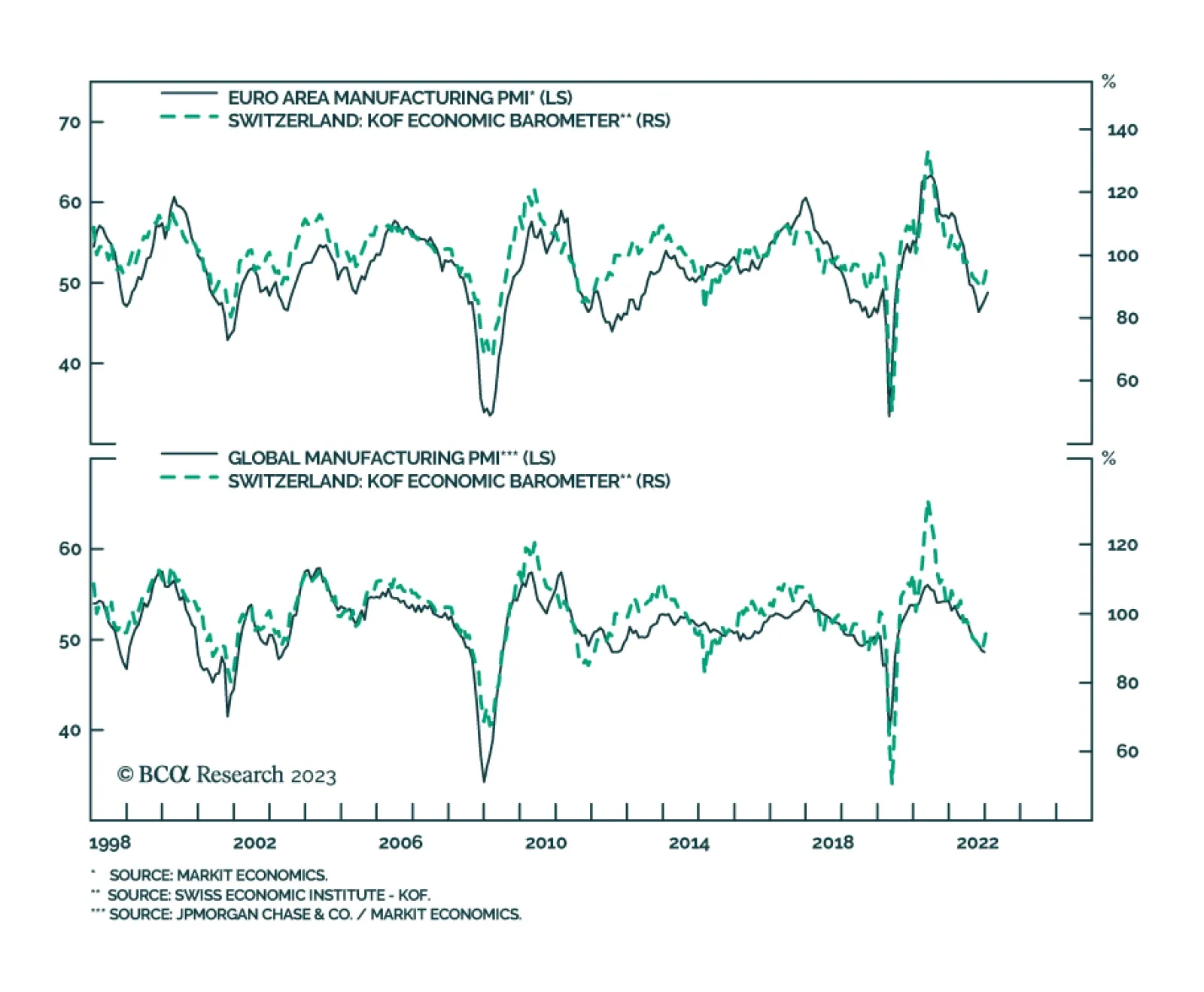

The Swiss KOF Barometer jumped 5.7 points to 97.2 in January, marking the second consecutive monthly increase, pushing the index to the highest level since June 2022. Importantly, the January increase reflects improvements across all of the KOF barometer’s…

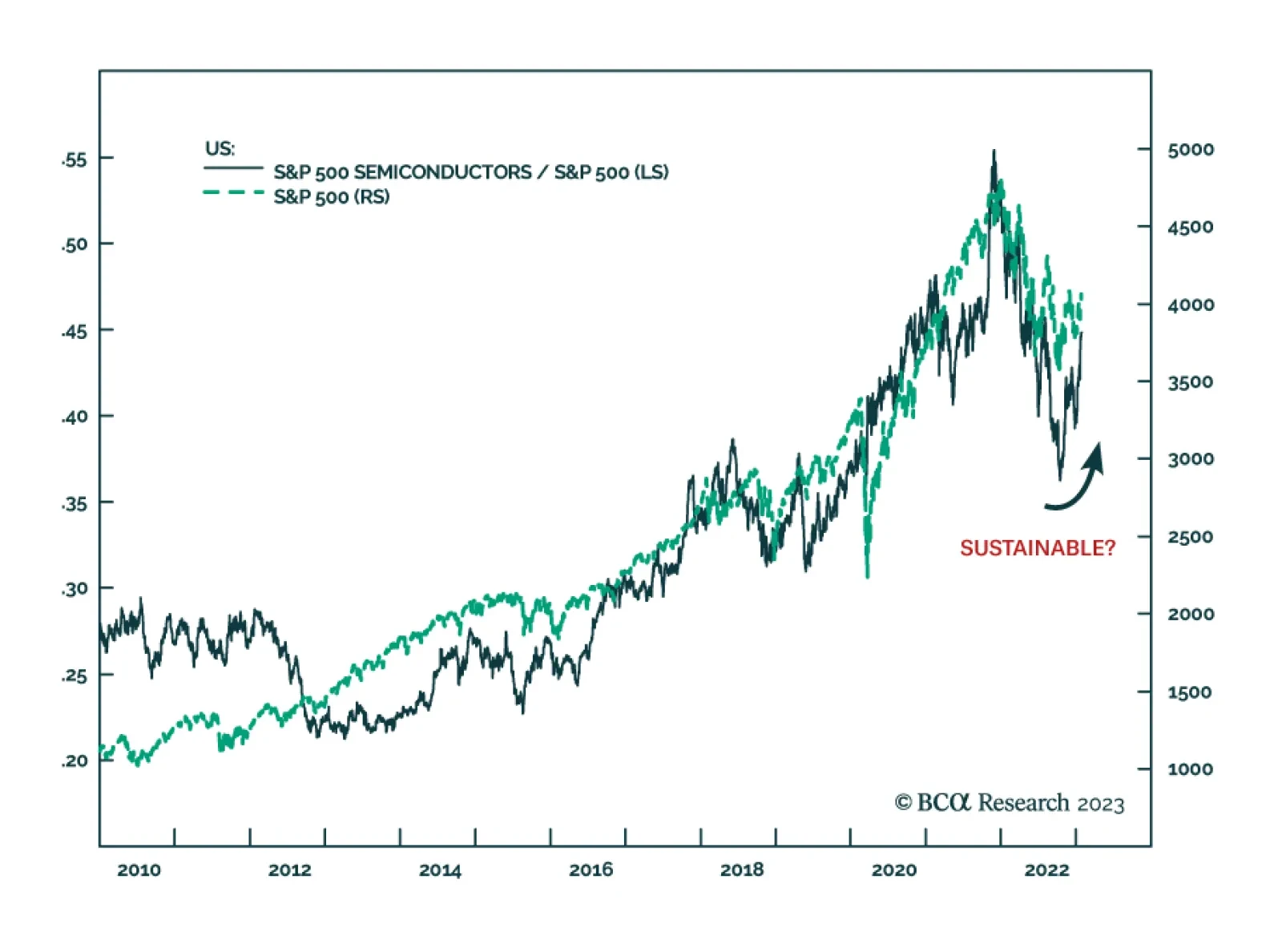

In recent months, US and global semiconductor companies have participated in financial markets’ “risk-on” phase. The semiconductor subsector of the S&P tech sector is up 39.4% since mid-October, outperforming the broad index by 25.8% during this period…

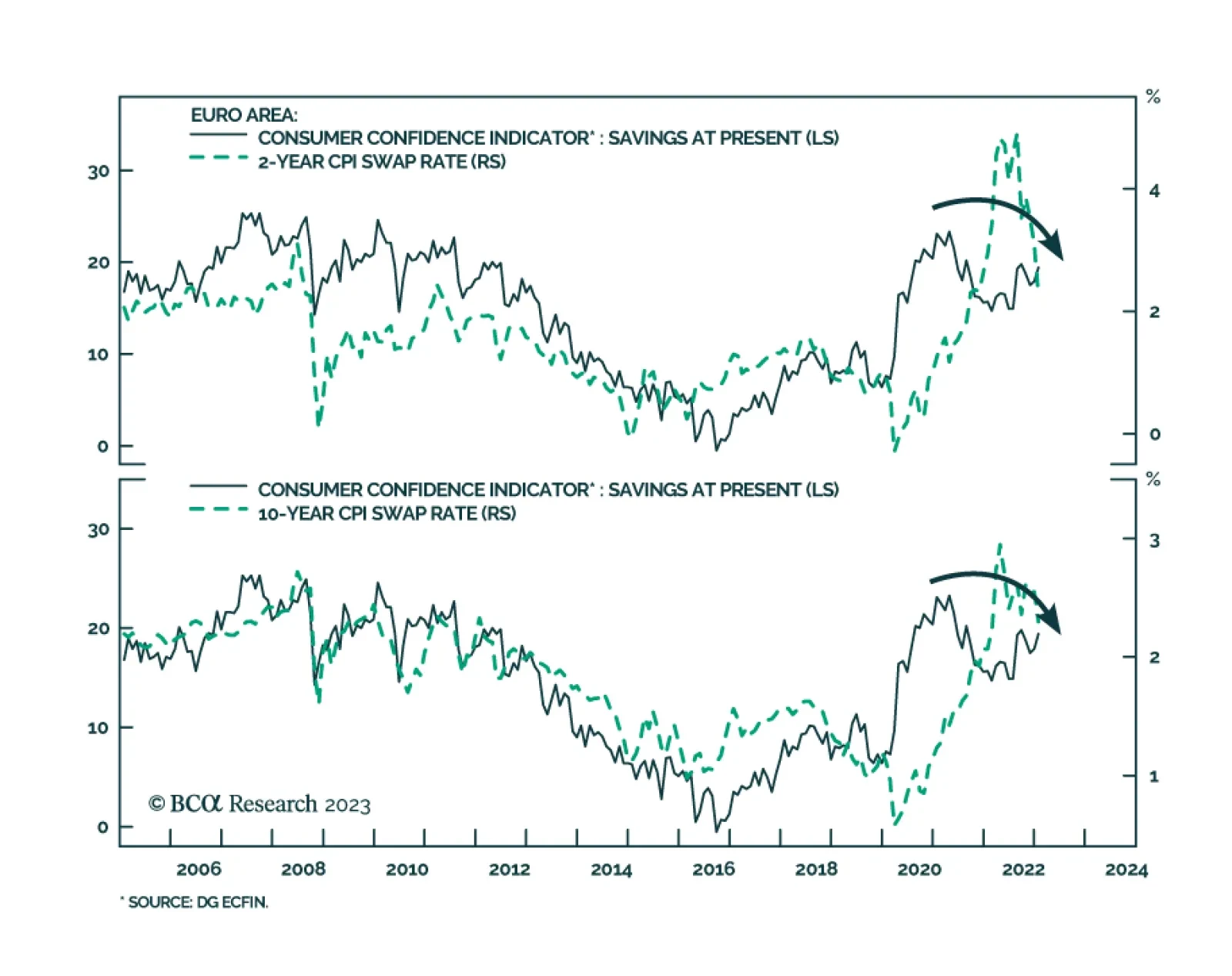

According to BCA Research’s European Investment Strategy service, Eurozone domestic demand is likely to be firm in 2023. Declining inflation will have a positive impact on consumption because it will lift real wages, which are currently contracting at 7%…

The most important question investors need to answer is whether this is the right time to shift the portfolio to a more aggressive and cyclical stance now that the end of the hiking cycle is in sight. To answer this question, we review the most recent macroeconomic, geopolitical, and equity market developments, and do our best to separate facts and data from sentiment and conjecture. We conclude that there are many challenges ahead and equities are not in a clear yet. We recommend investors add small positions in areas of the market that benefit from rate stabilization while maintaining an overall defensive stance.