Developed Countries

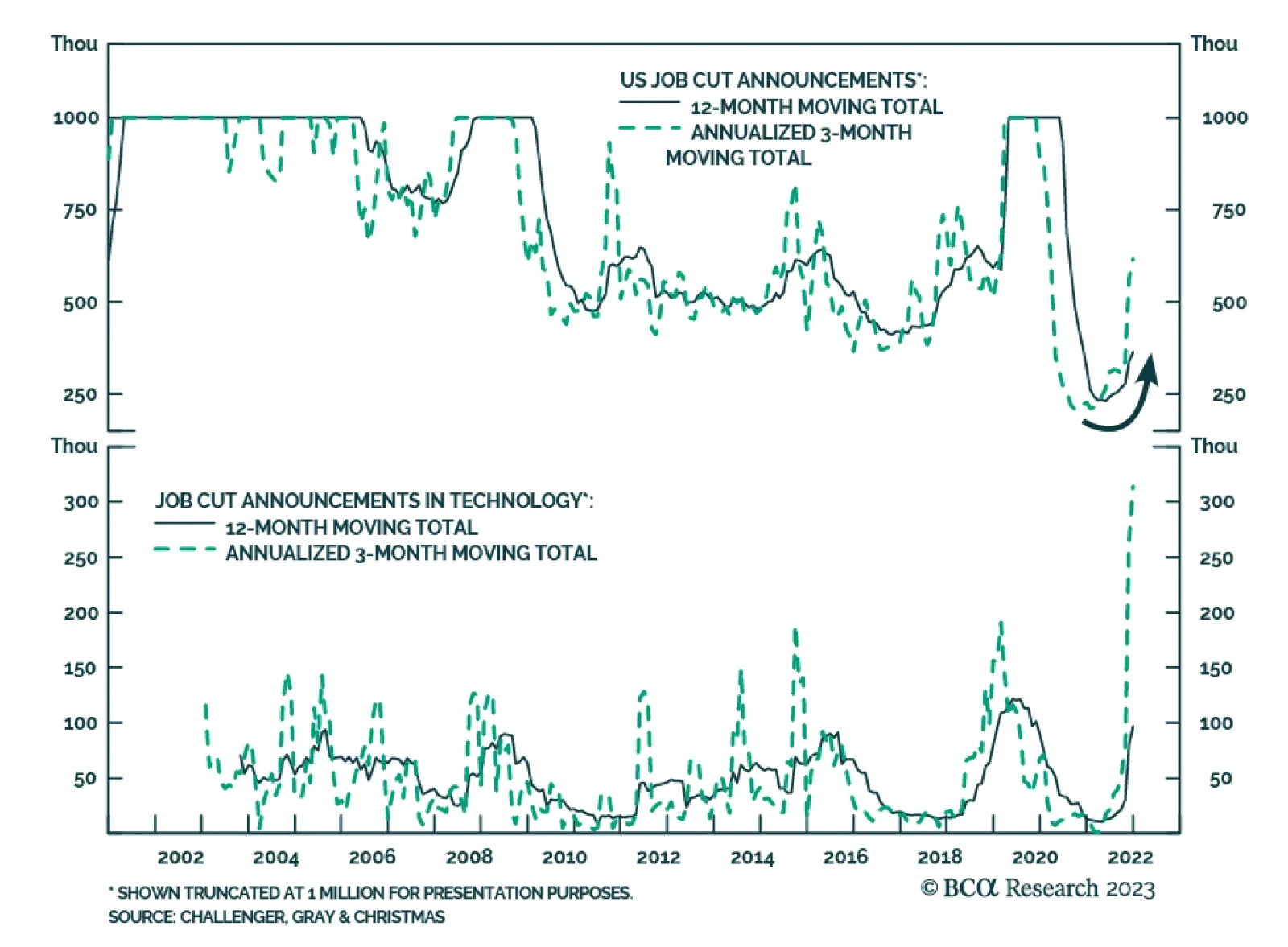

Last week, 190 thousand initial unemployment claims (IUC) were filed in the US, below expectations they would increase from the prior week’s 205 thousand. On a 4-week moving average basis, initial unemployment claims have now reached an 8-month low,…

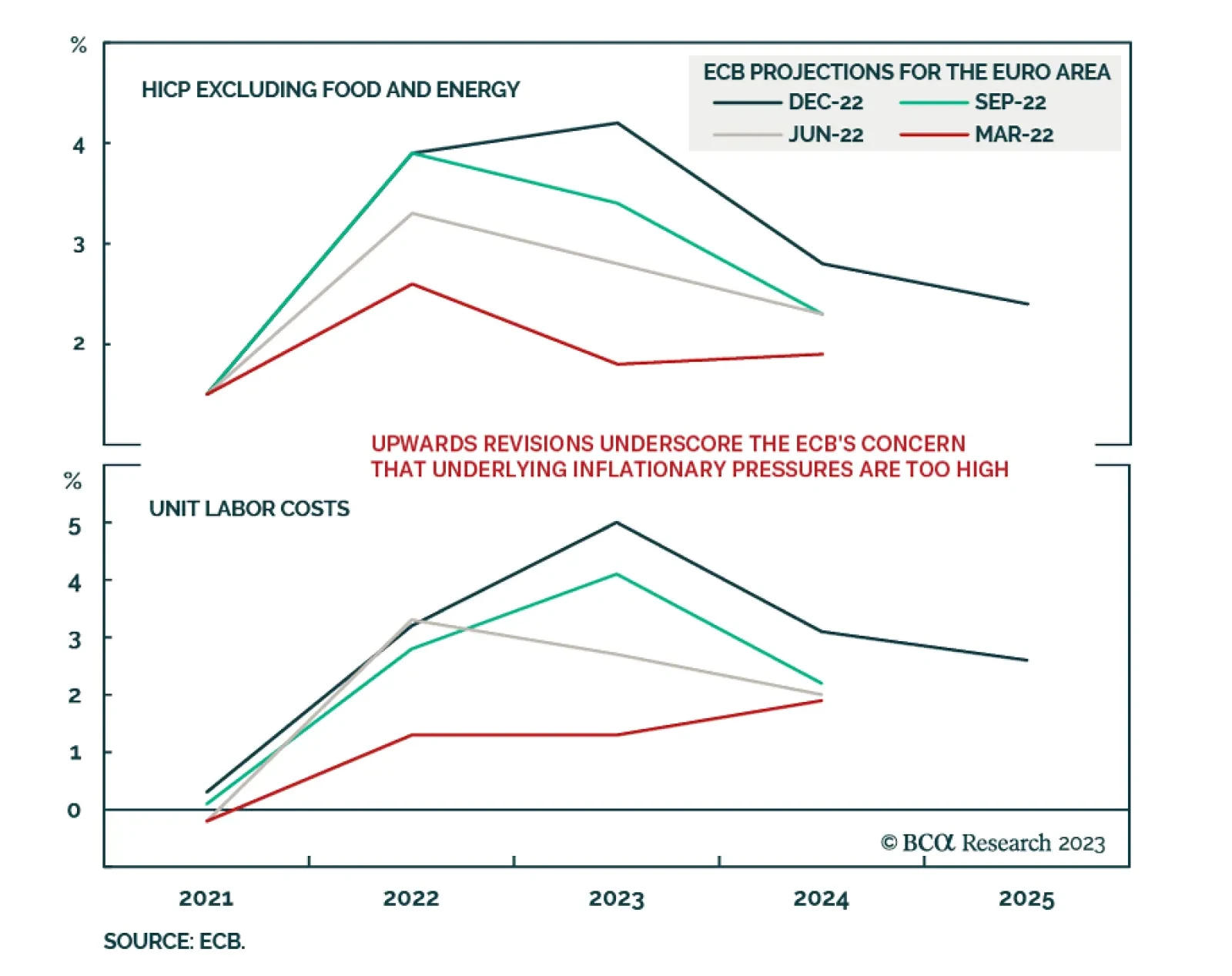

The tone of the minutes from the ECB’s December meeting was decidedly hawkish. The release emphasized that Governing Council members agree that the tightening cycle is far from over given their view that risks to the inflation outlook are skewed to the…

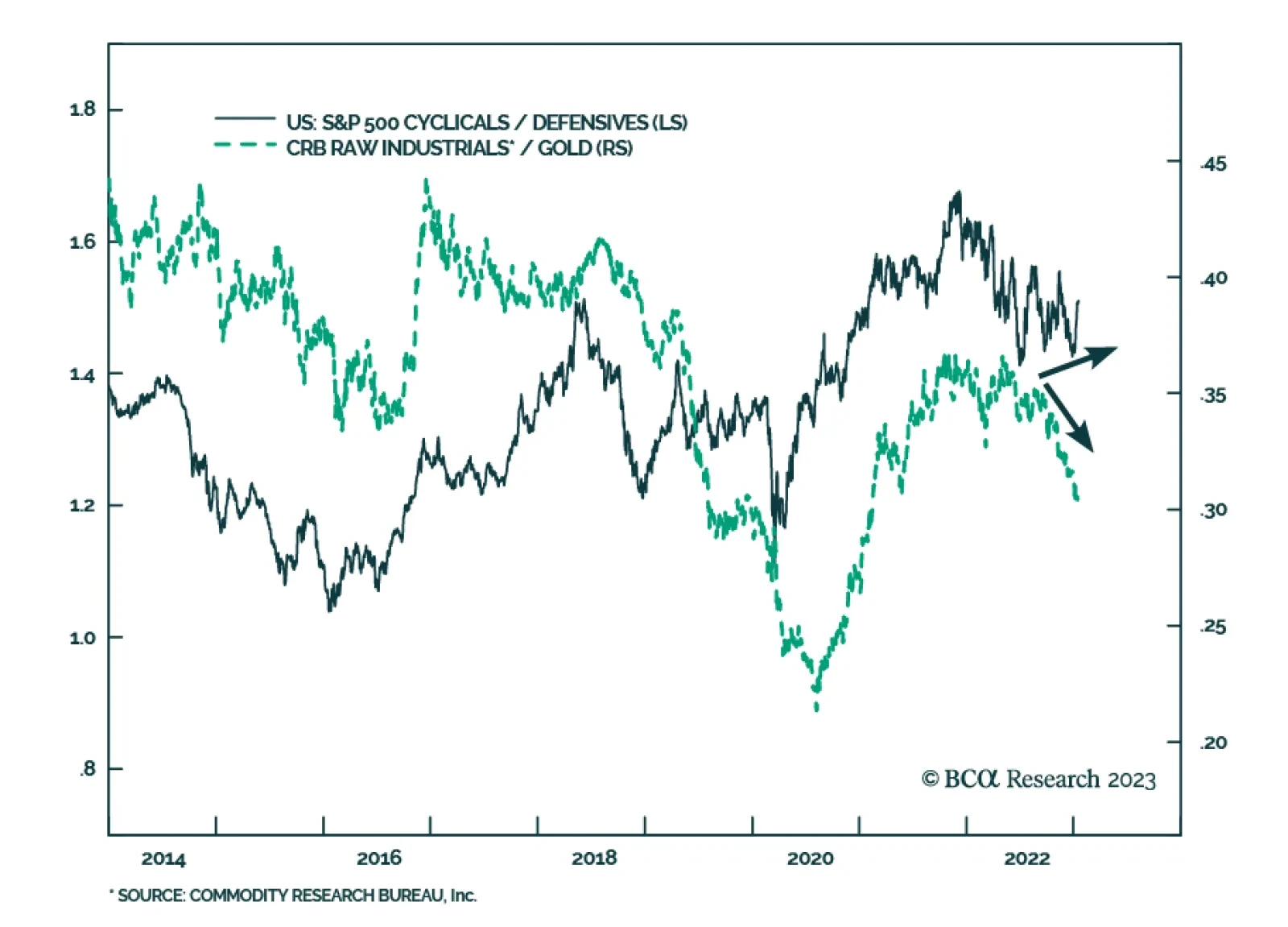

The signal from commodity markets warns against the durability of the outperformance of US cyclical equities relative to defensives. In particular, while most commodities have benefitted from a weakening dollar in recent months, the CRB Raw Industrials…

China’s re-opening – powered by the fiscal and monetary stimulus required to achieve at least 5% real GDP growth after flattish 2022 growth – and a weaker USD will catalyze demand growth this year and next, lifting global oil consumption by close to 2mm and 1.7mm b/d in 2023 and 2024. We lowered our Brent forecast slightly for this year to $110/bbl, and expect 2024 prices to average $115/bbl. WTI will trade $4-$6/bbl lower.

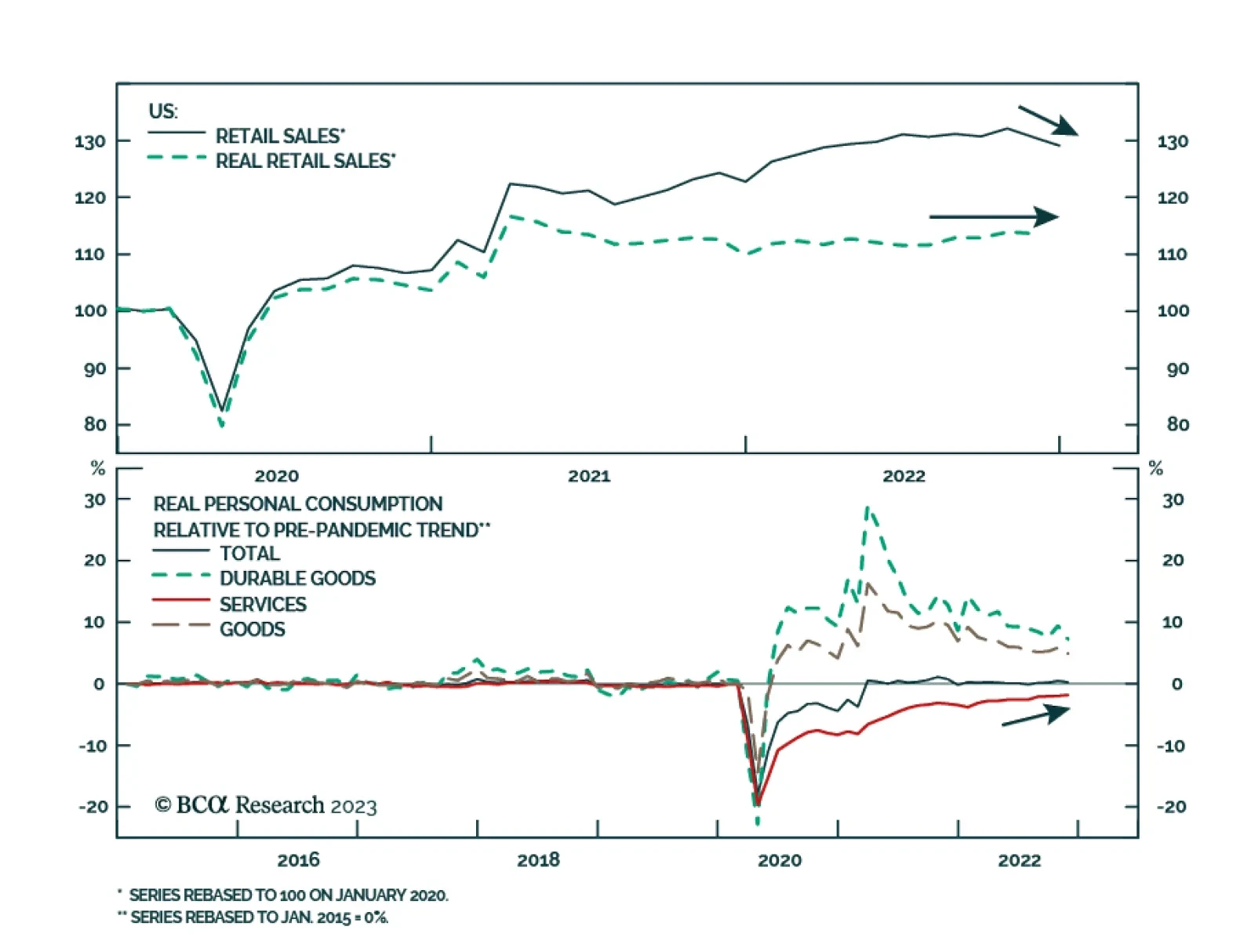

Preliminary estimates indicate that the value of US retail sales fell by a larger-than-expected 1.1% in December following a downwardly revised 1% decrease in November, marking the largest monthly decline since December 2021. Department stores (-6.6% m/m),…

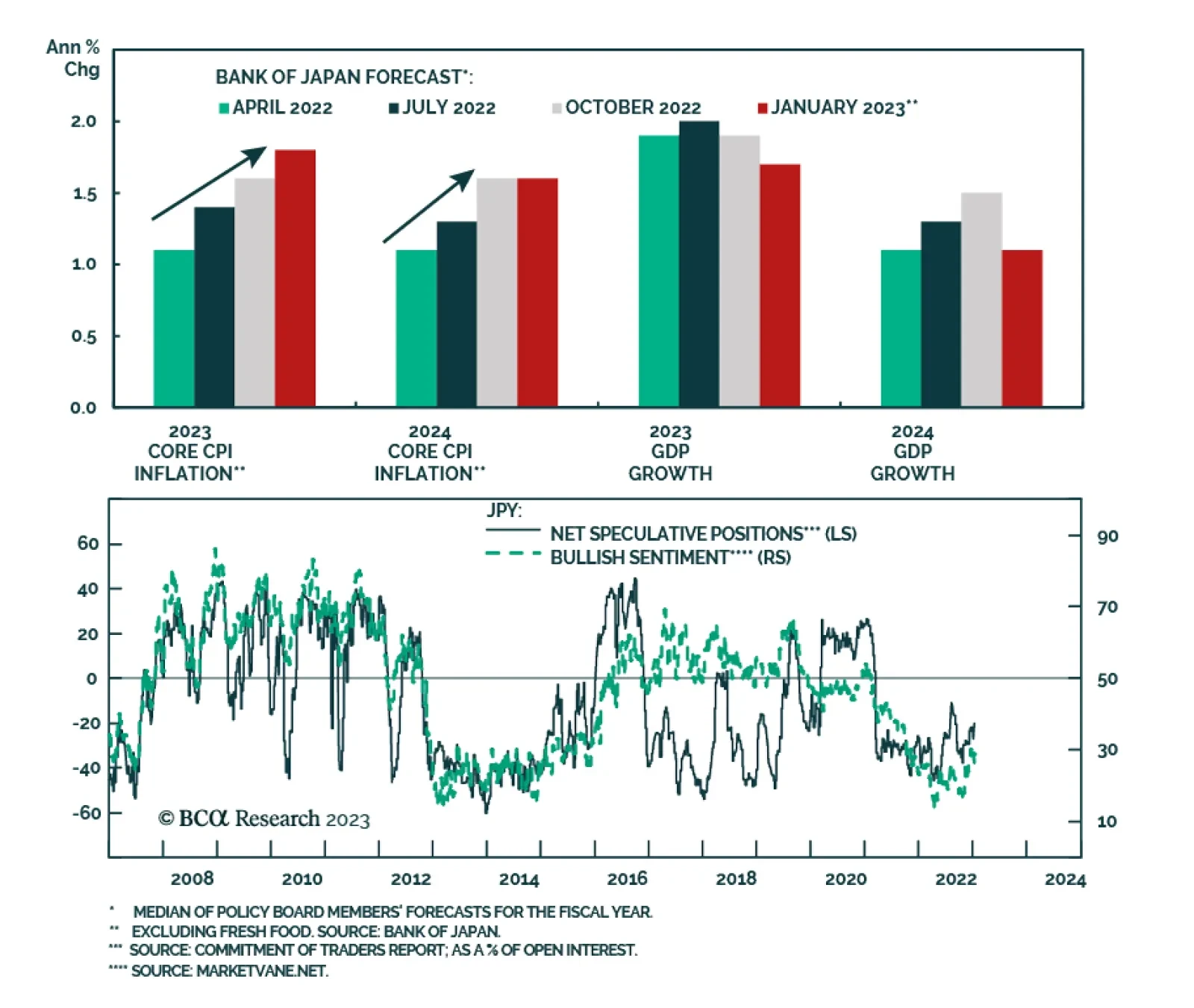

After having unexpectedly doubled its Yield Curve Control (YCC) cap on 10-year government bond yields from 0.25% to 0.5% at its December meeting, the Bank of Japan (BoJ) did not adjust its policy further in January. Instead, the monetary policy statement…

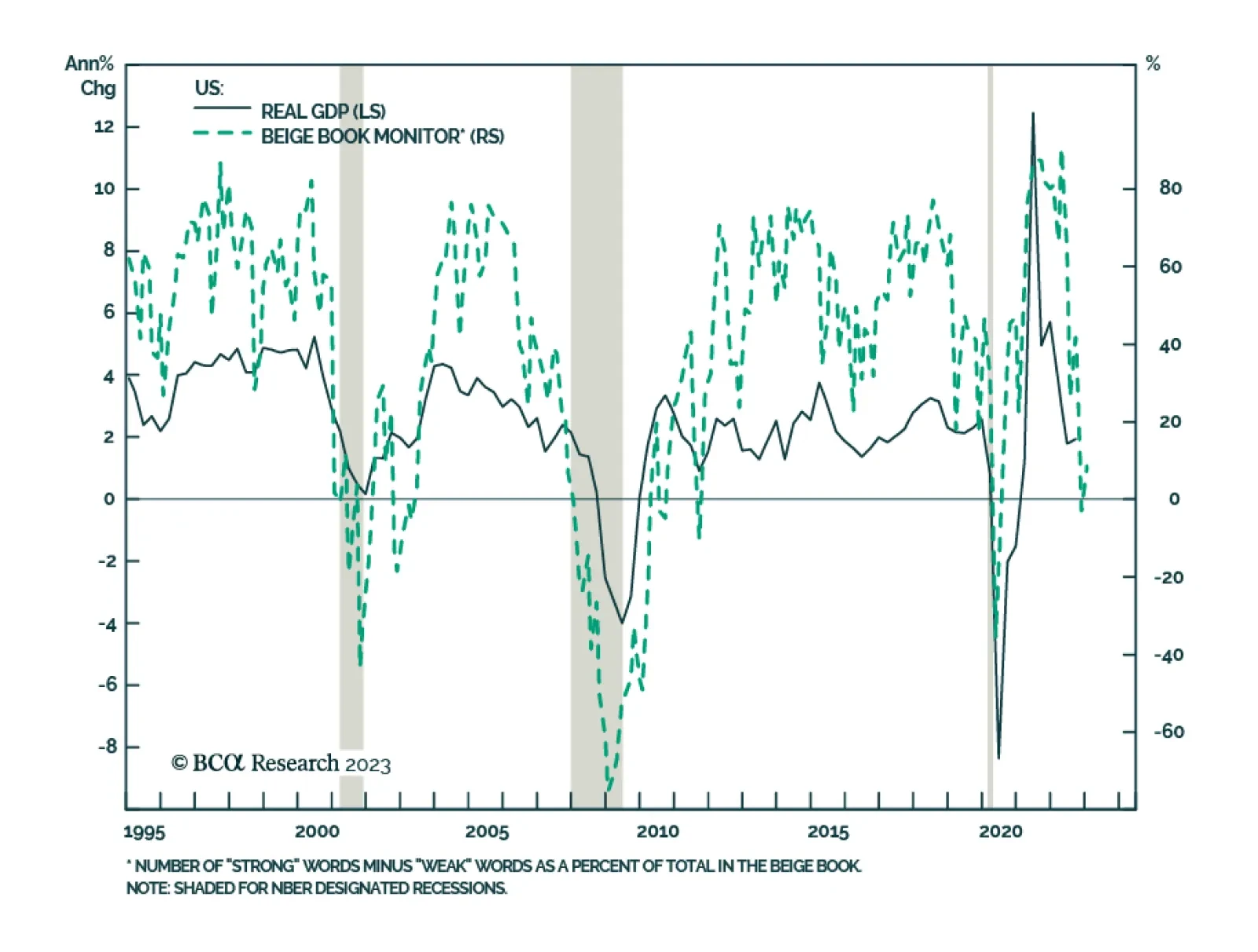

The Fed Beige Book continues to provide a somber outlook for the US economy. It highlighted that “overall economic activity was relatively unchanged since the previous report” and that “contacts generally expected little growth in the months ahead.” In…

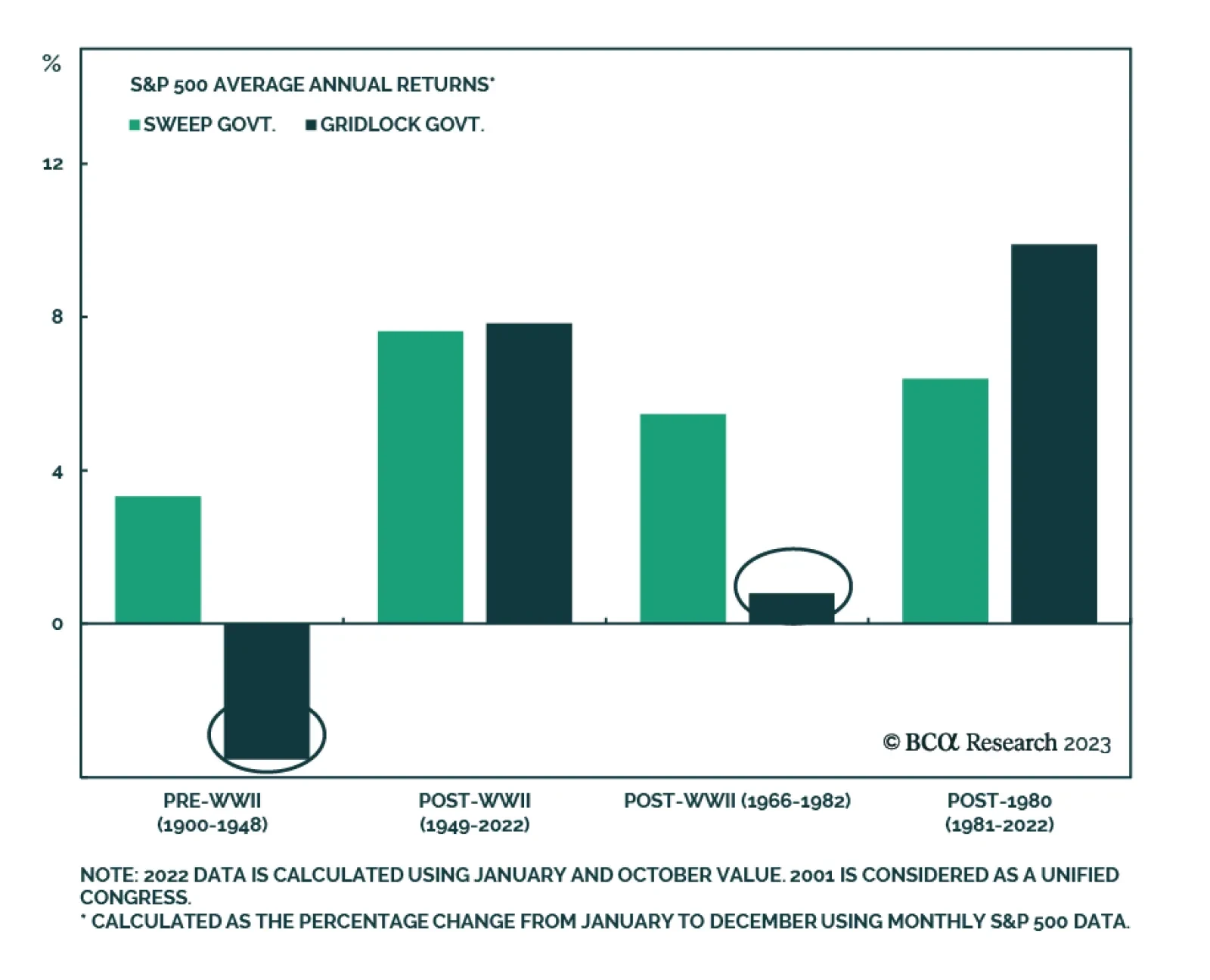

According to BCA Research’s US Political Strategy service, the US political and geopolitical context has not yet verifiably improved, and they doubt it will prior to 2024. Any market rally will be capped at an unexpected time over the coming months. The US…

Investors should stay defensive on recession risks until they subside meaningfully.

We remain bullish the yen, despite the BoJ maintaining yield curve control. In this report, we outline a few reasons for this stance.