Developed Countries

In this week’s report, we look at whether global growth conditions remain conducive for a continued decline in the dollar. Our findings are mixed, while there are some economic green shoots, the overall growth picture remains weak. This argues for some consolidation of dollar losses in the near term.

While the housing downturn will be fairly mild in the US, it will be more severe abroad. Continue to favor bonds of countries whose housing fundamentals will limit rate hikes.

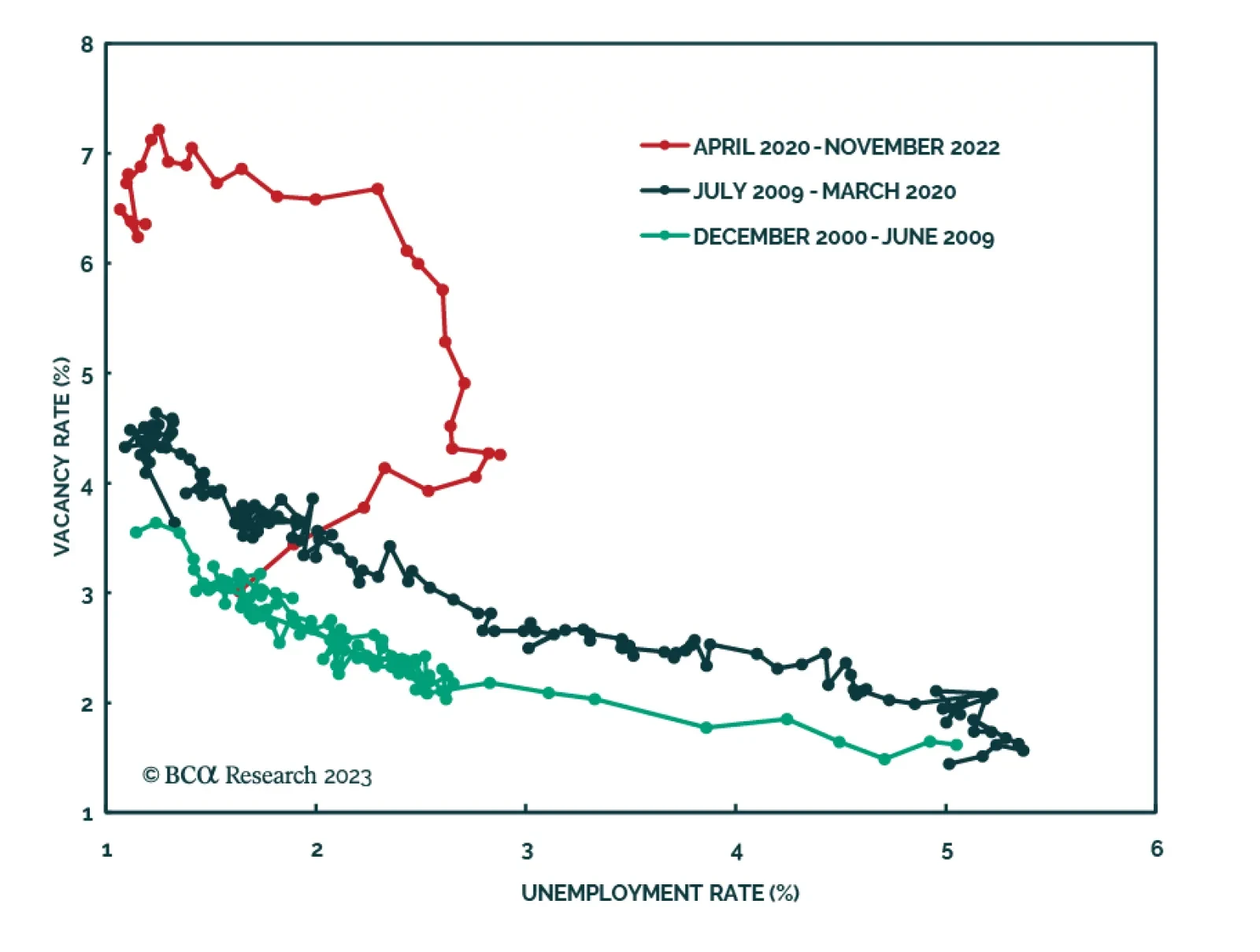

The crucial question for 2023 is: will the US and UK Beveridge Curves shift back inwards to their pre-pandemic versions, ushering in a soft landing? Or, will we slide down the new post-pandemic Beveridge Curves into recession? Plus: we reveal the most important chart for Europe and the most important chart for China in early 2023.

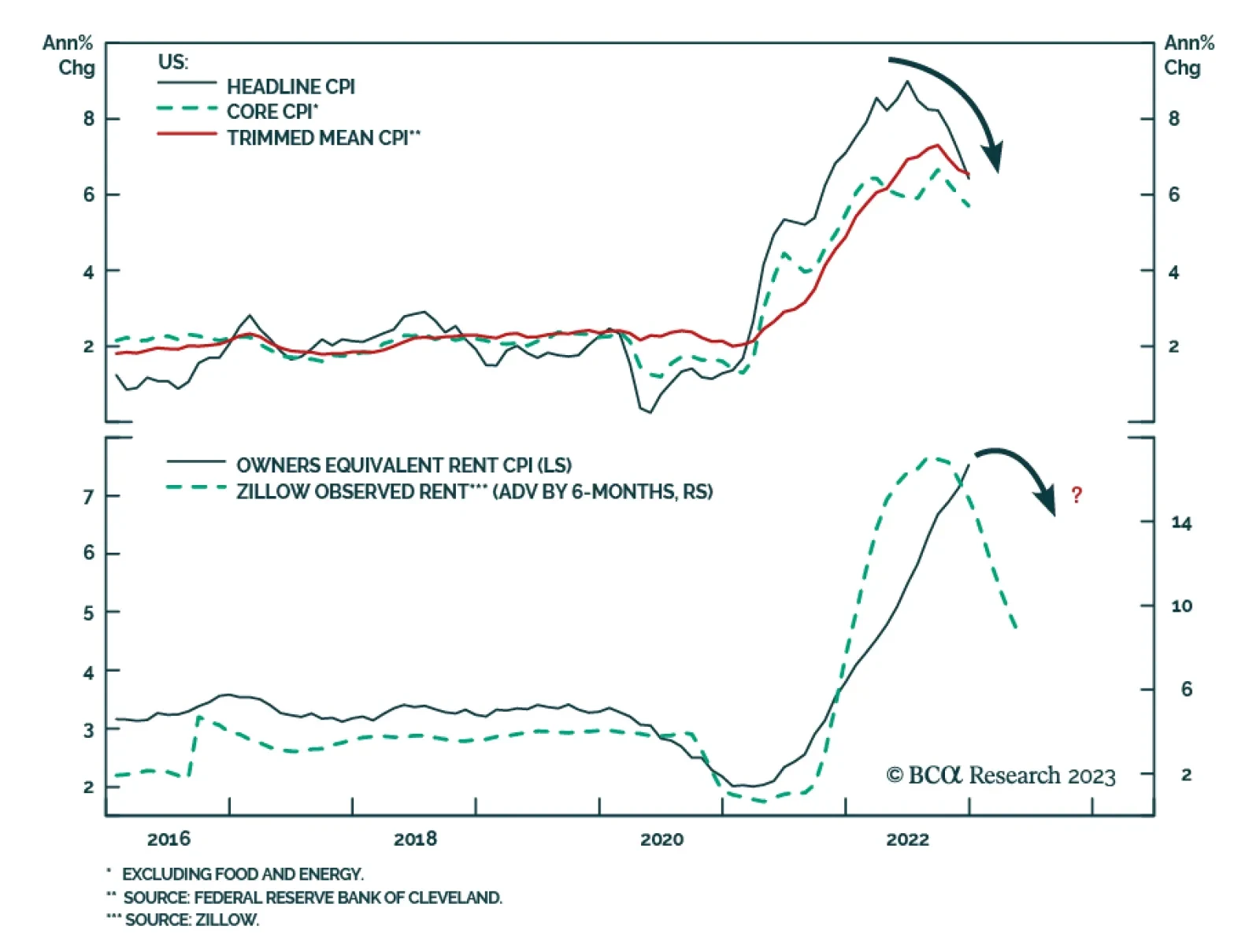

The Fed will respond to December’s CPI report by downshifting to a 25 bps hike pace next month. We anticipate two more 25 bps hikes before the Fed goes on hold.

Why will Chinese consumer spending recover but not its industrial sectors? Will China's reopening boost the global business cycle and inflation? How fast will US core inflation fall and what are the implications for corporate profits? Are global equities pricing in enough bad news/profit contraction?