Developed Countries

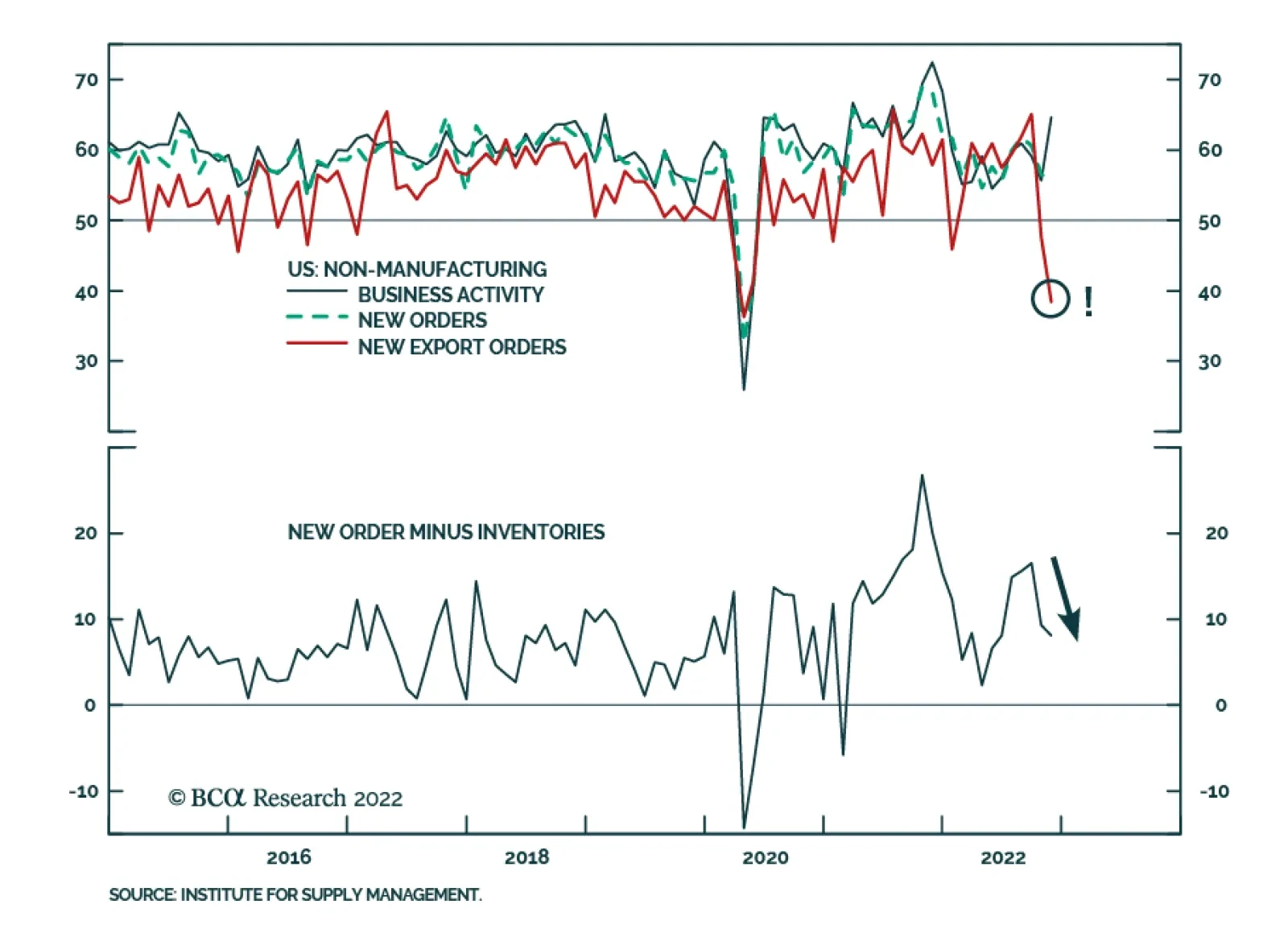

The ISM Services PMI surprised to the upside, unexpectedly expanding at a faster pace in November. The headline index rose by 2.1 ppts to 56.5, led by the business activity and import sub-indices which rose by 9.0 and 9.1 ppts to 64.7 and 59.5, respectively.…

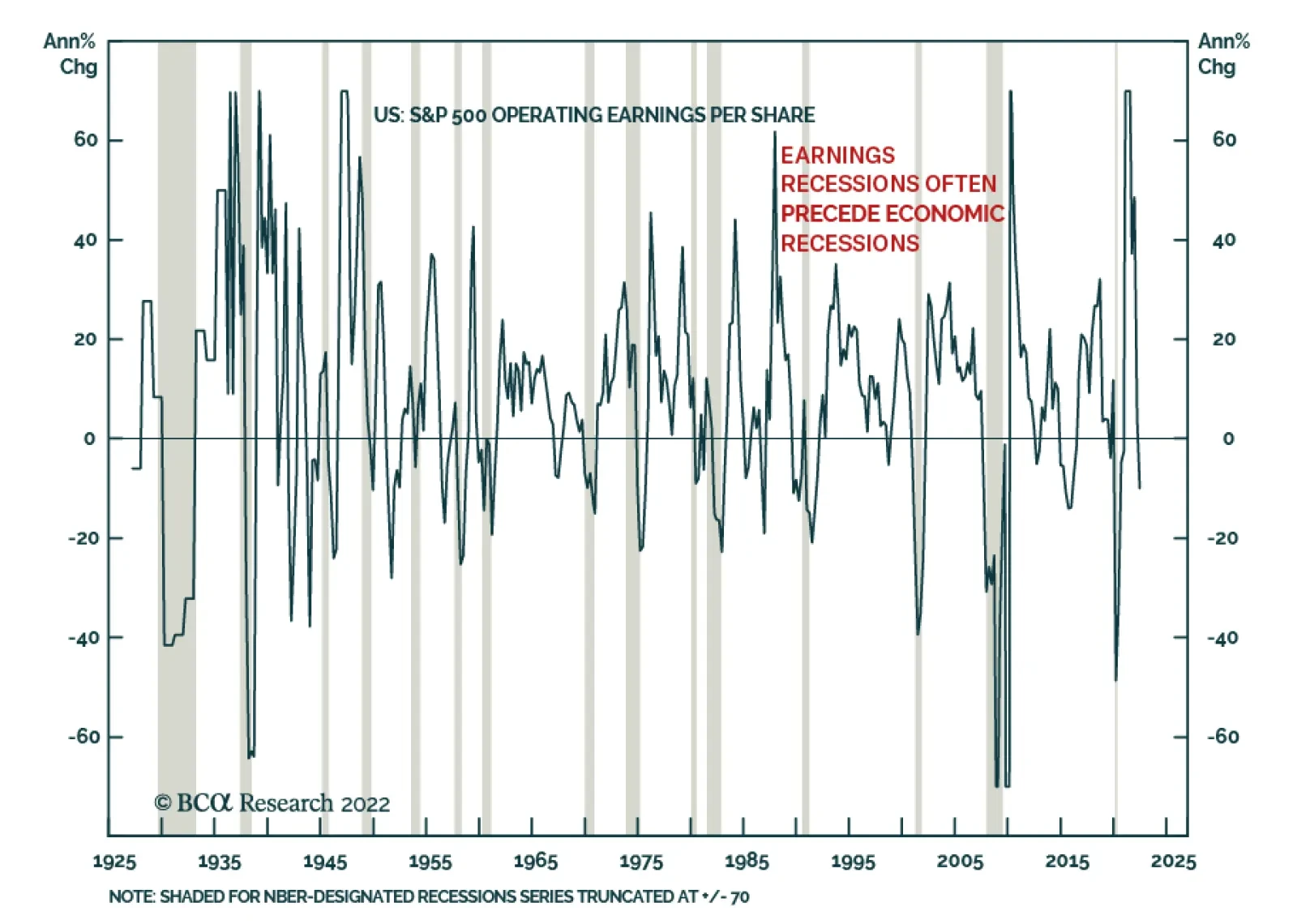

BCA Research’s US Equity Strategy service concludes that earnings will continue on a downward path in 2023, and analyst downgrades are highly likely. Earnings growth is key to 2023 equity performance. With economic growth deteriorating, it is reasonable to…

Labor market strength and consumers’ evident willingness to dip into their pandemic savings keep our optimistic consumer thesis intact. We remain tactically overweight equities.

European inflation will decline through 2023, which will greatly help households and consumption. But can European inflation remain low after that?

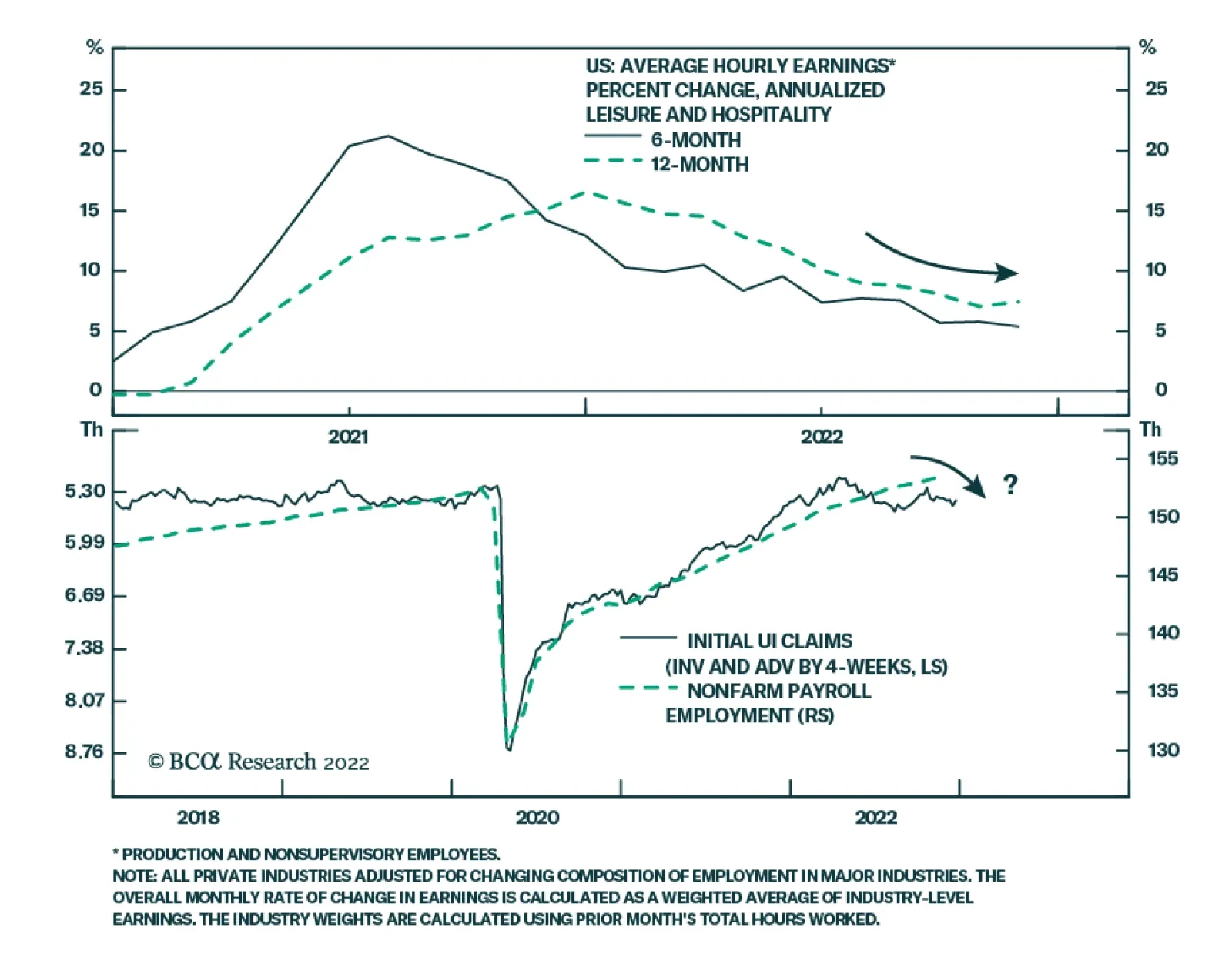

US nonfarm payrolls increased by a greater-than-expected 263 thousand jobs in November, following an upwardly revised 284 thousand gain in October. Although the participation rate edged down to 62.1%, the unemployment rate was unchanged at 3.7%. Most notably,…

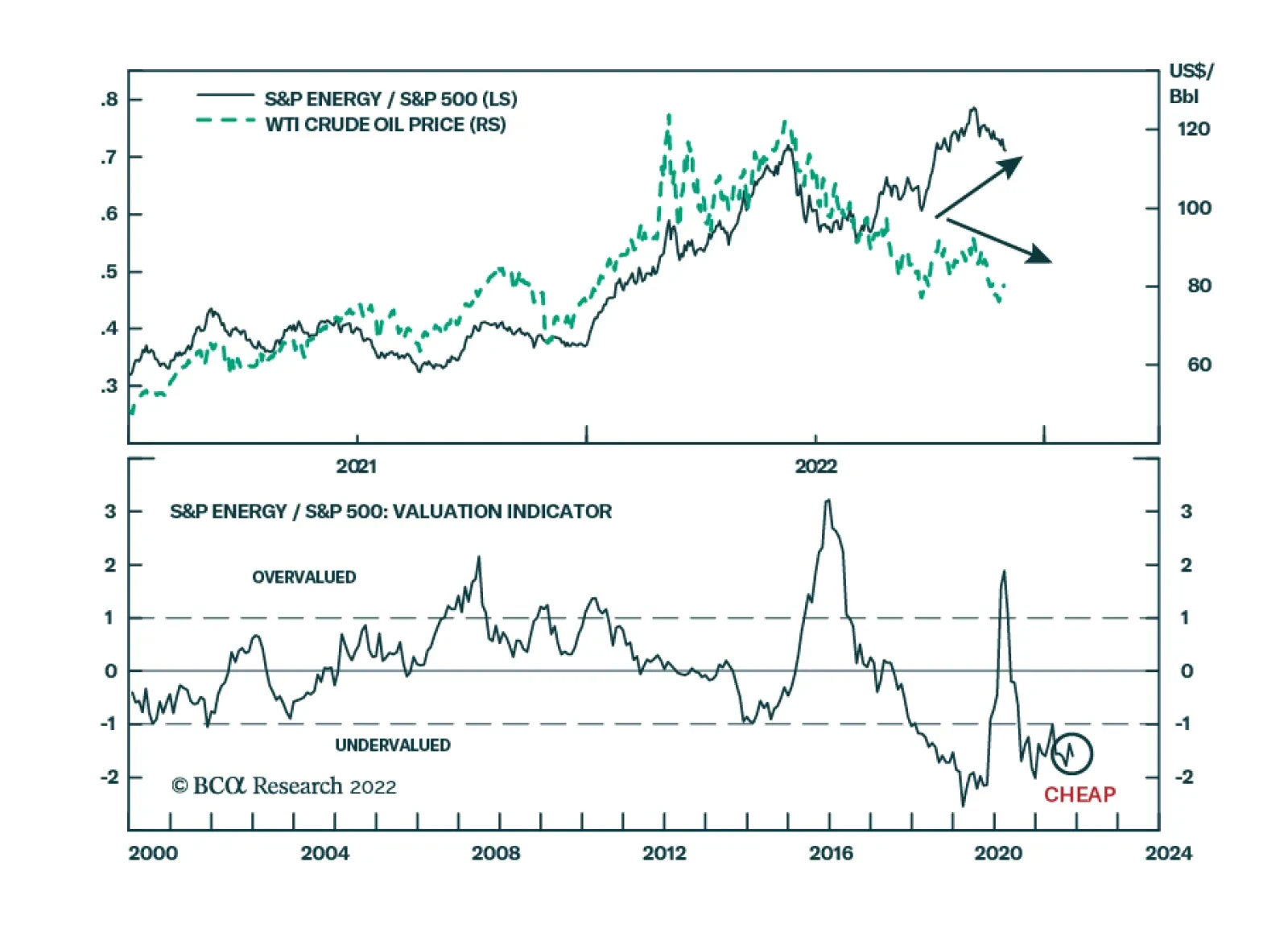

Over the past few months, energy equities have diverged from oil prices. Although the price of West Texas Intermediate crude oil has fallen by 4% since mid-July, the S&P Energy index has gained 34.4% over this period, outperforming the S&P 500 by…

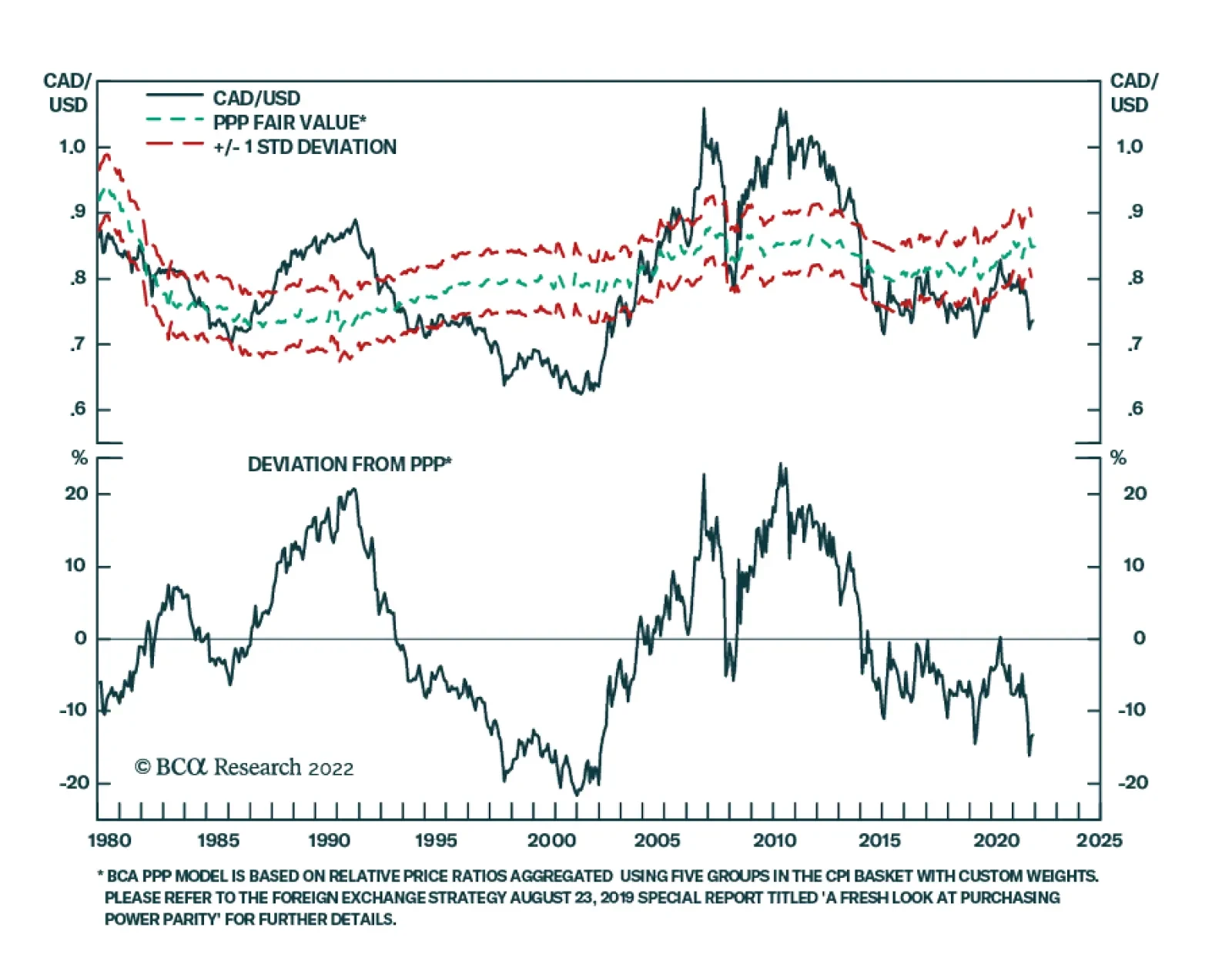

According to BCA Research’s Foreign Exchange Strategy service, there are four fundamental reasons to position for higher energy prices that will support the Canadian dollar. The US is becoming the marginal supplier of natural gas to the world. Energy…

MacroQuant is overweight bonds, underweight equities, and neutral on cash. Within the equity universe, the model is underweight the US and overweight Japan, the UK, and Australia.

Commodity currencies have been rather resilient, despite the broad rise in the dollar this year. In our view, we are about to experience a big rotation in commodity currency market performance at the crosses, from NZD, to CAD and finally to AUD.

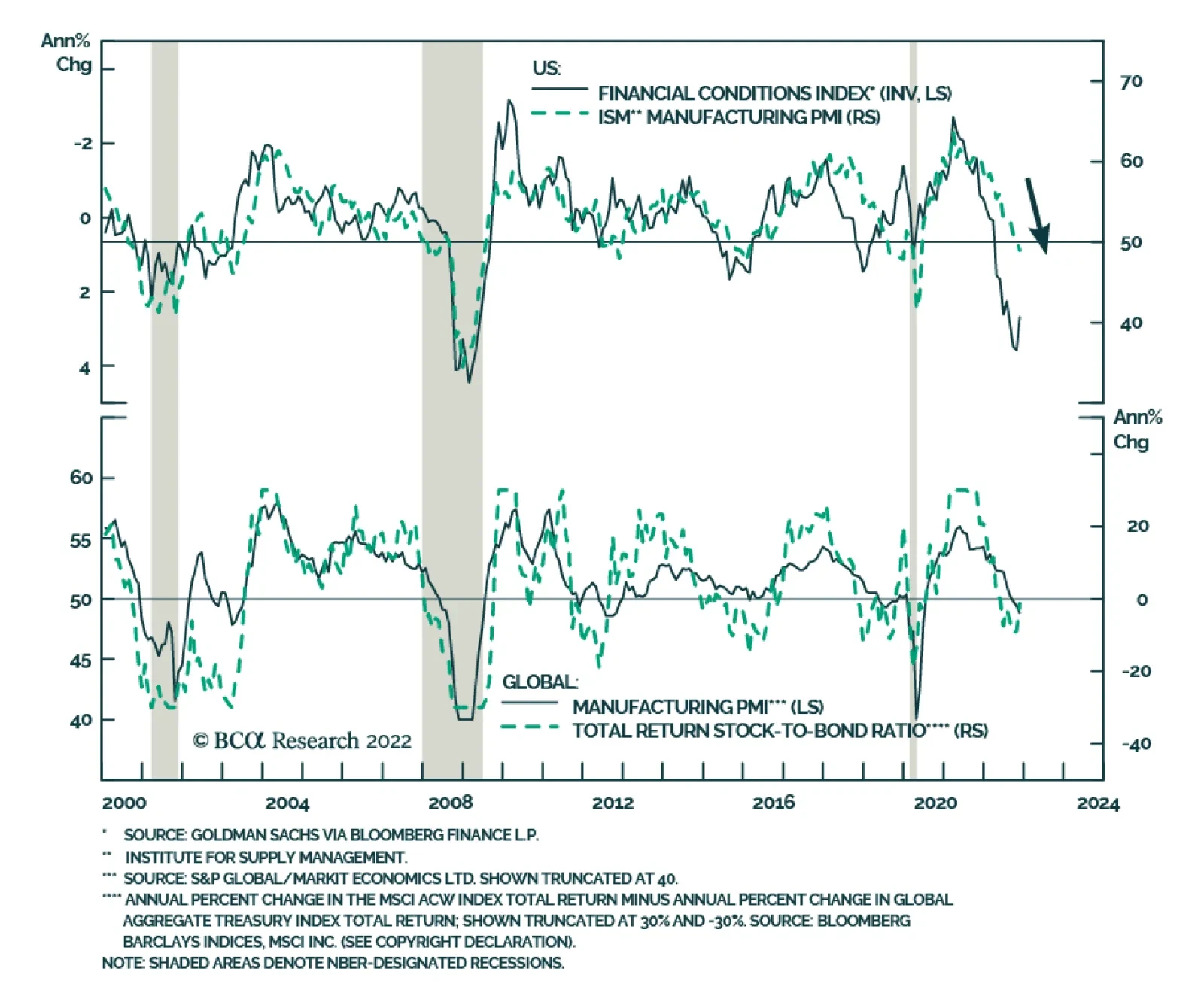

The ISM Manufacturing PMI contracted in November for the first time since mid-2020. It fell to 49.3 from 50.2, corroborating the downbeat signal from the alternative S&P Global PMI which declined by 2.7 points to 47.7. Details of the report underscore…