Developed Countries

Today, we are sending you the BCA annual outlook for 2023. The report is an edited transcript of our recent conversation with Mr. X and his daughter, Ms. X, who are long-time BCA clients with whom we discuss the economic and financial market outlook for the next twelve months toward the end of each year.

In this report, we look at the possibility of a dollar decline during any pending recession. In our view, the evidence is mixed. We are probably in one of the most anticipated recessions in recent history, and the dollar has risen a lot. But the dollar also tends to rise during most recessions. We recommend a neutral stance on the DXY, with a bet on some trades at the crosses.

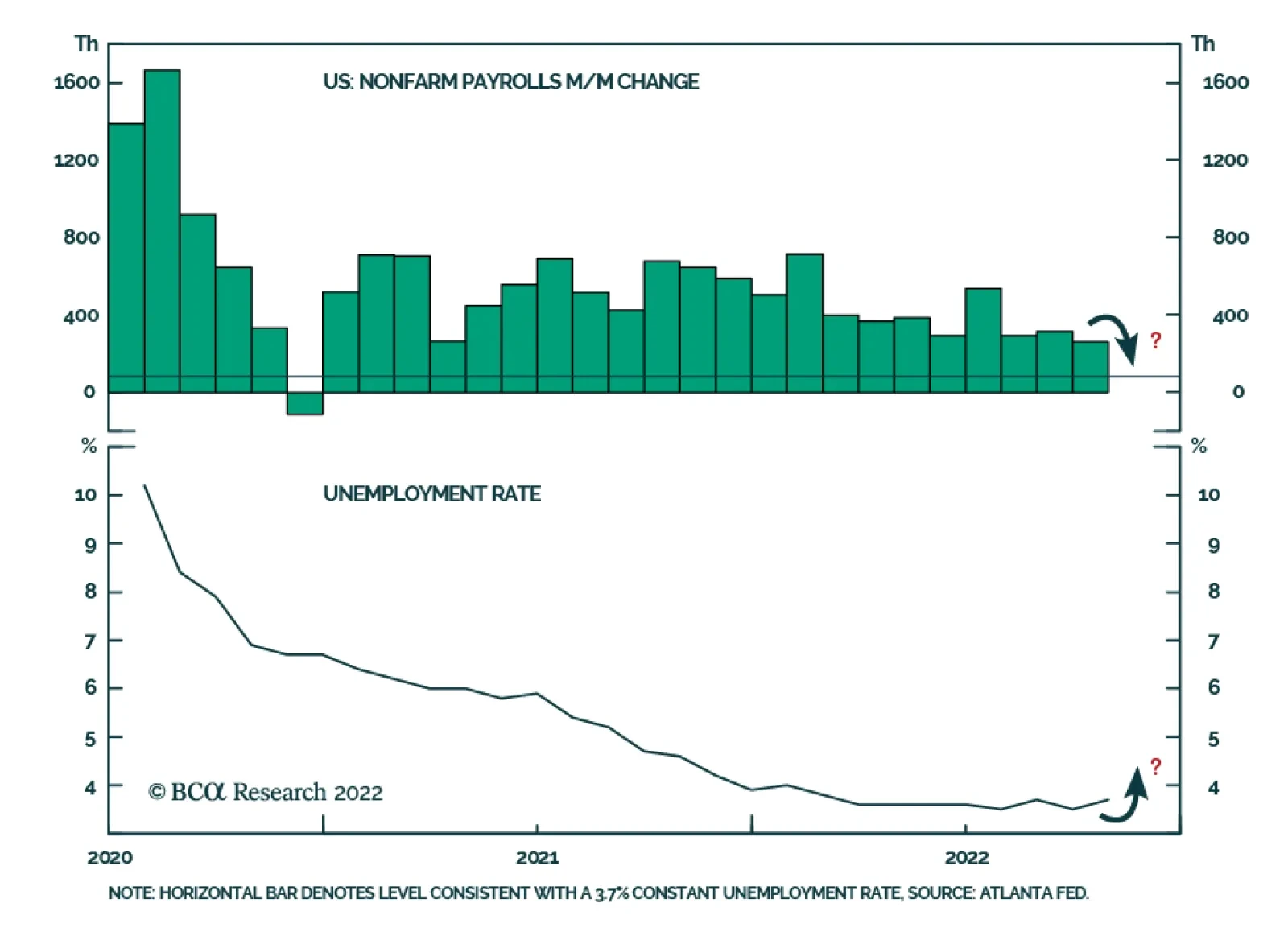

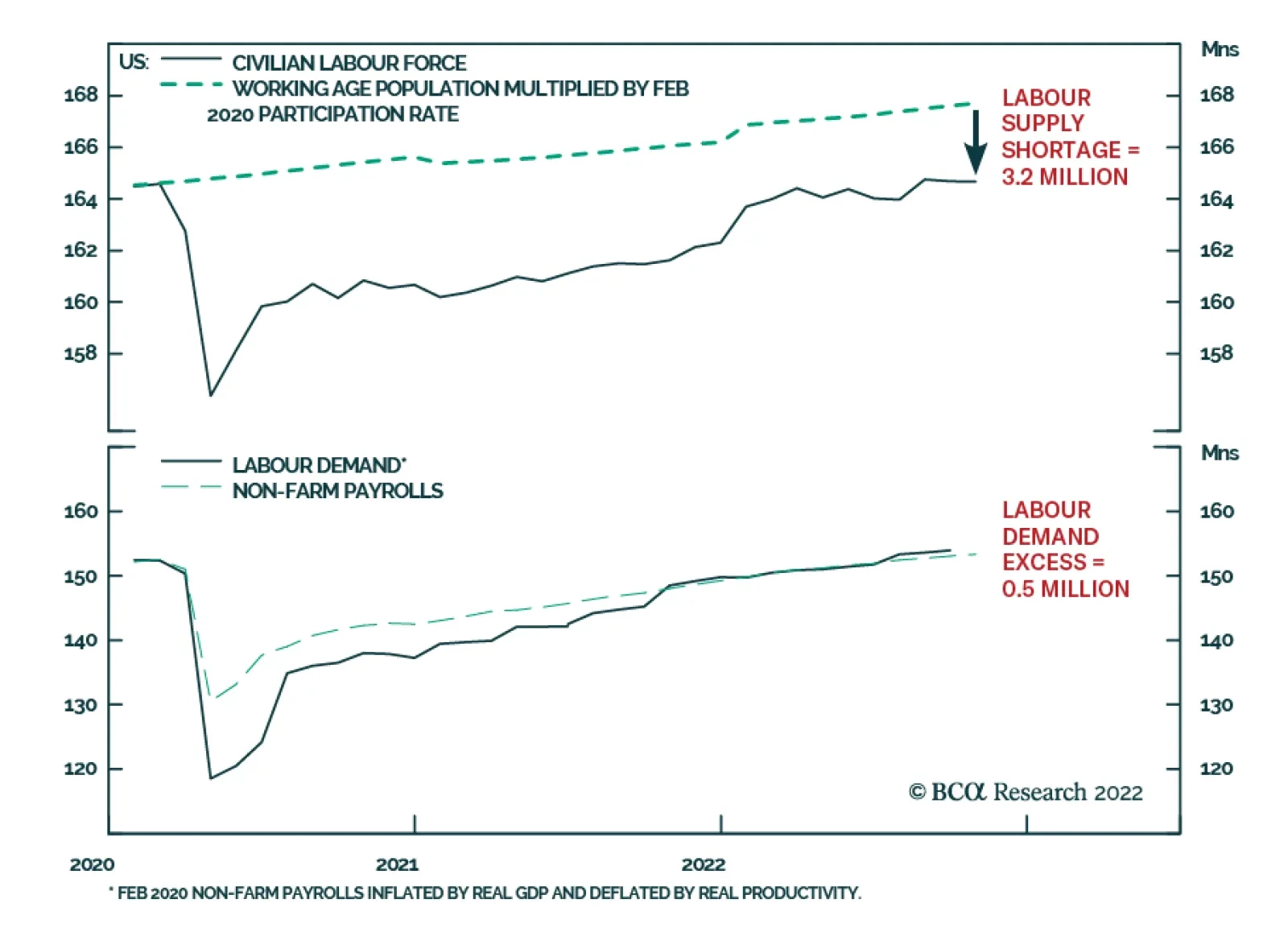

Excess job vacancies in the US and UK reflect a labour market that cannot efficiently match unemployed workers with vacant jobs. This is because excess job vacancies reflect the shortage of labour supply in the 50 plus age cohort, whose skills are difficult to replace. In economic jargon, the post-pandemic ‘Beveridge curve’ has shifted outwards. Absent an unlikely shift in the Beveridge curve to its pre-pandemic version, killing US wage inflation will mean killing jobs. And killing jobs will mean killing profits. We go through the investment implications.