Developed Countries

Stay defensive until recession risks are verifiably dispelled. Favor government bonds over stocks.

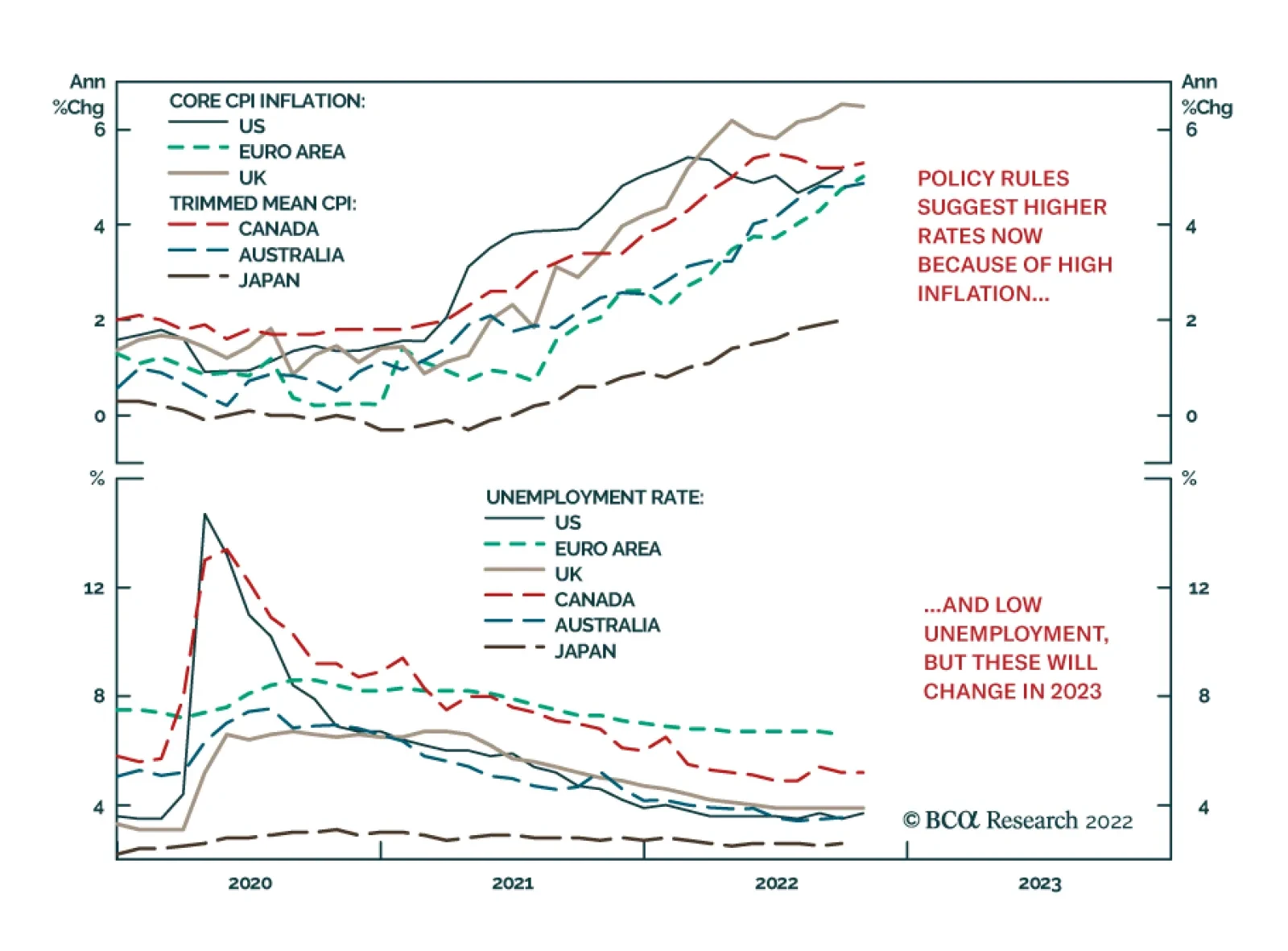

In this Special Report, we consider what some common monetary policy rules are recommending for the major central banks and derive conclusions on duration strategy and country allocation for bond investors. We conclude that rate hike expectations in most countries may appear appropriate given the current global backdrop of high inflation and low unemployment, but look elevated on a forward-looking basis versus slowing global growth and peaking global inflation.

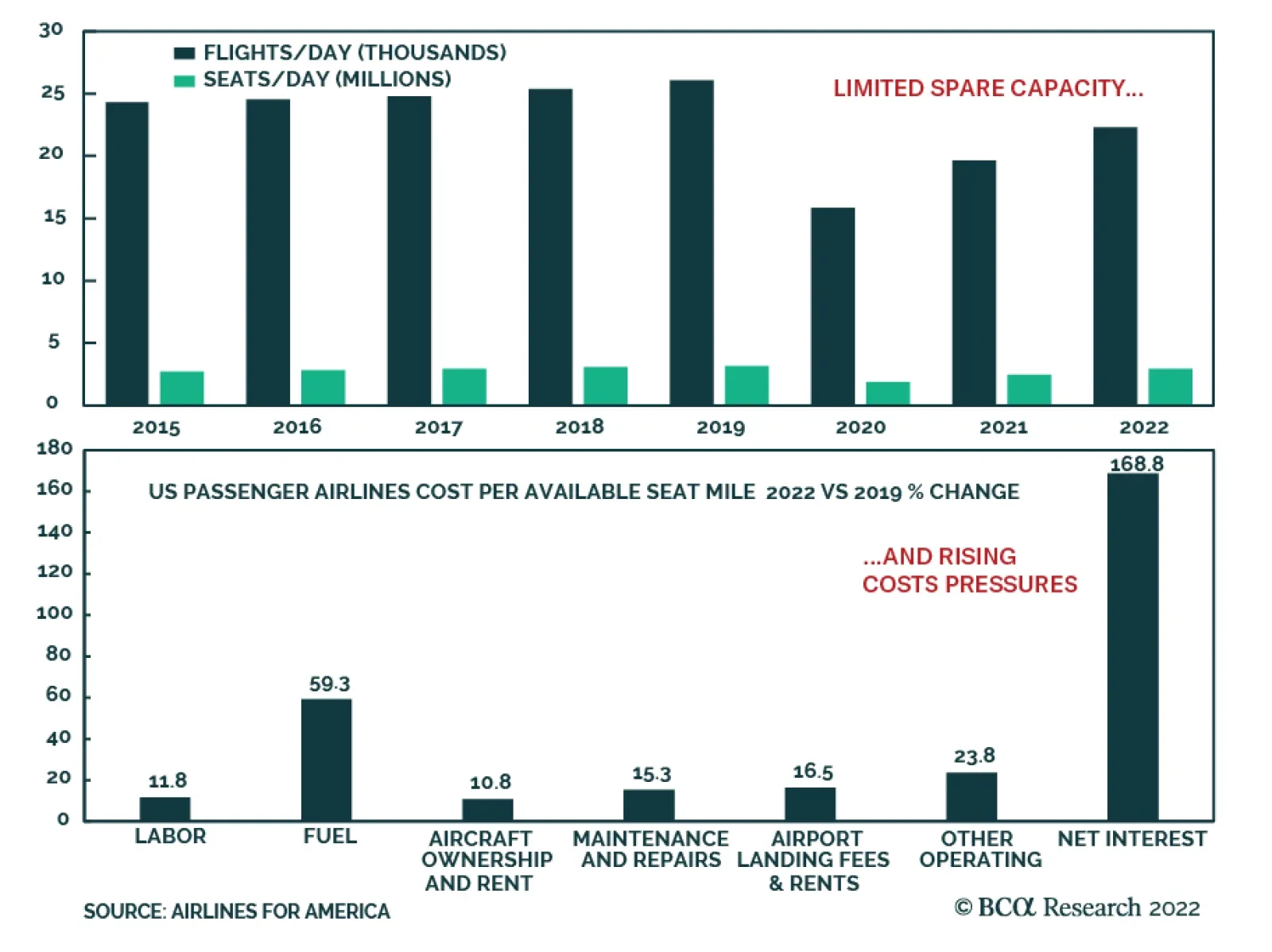

Airlines have staged an impressive recovery this year, exceeding all expectations. While companies are optimistic, we are cautious. Just as pent-up demand for travel will fade, headwinds from slowing growth and high inflation will intensify. While it is highly likely that Airlines will continue to rally into the yearend, we will stick to our underweight as our three-to-six-month outlook remains negative.

The latest CPI and PPI releases, the modestly less hawkish turn in Fed officials’ comments and evidence that consumers continue to spend with some relish support our constructive near-term views on equities and the economy.