Developed Countries

What is the outlook for the European housing market amid rising mortgage rates and the energy crisis? Does housing represent a systemic risk? Can households weather the storm? And what are the opportunities, if any?

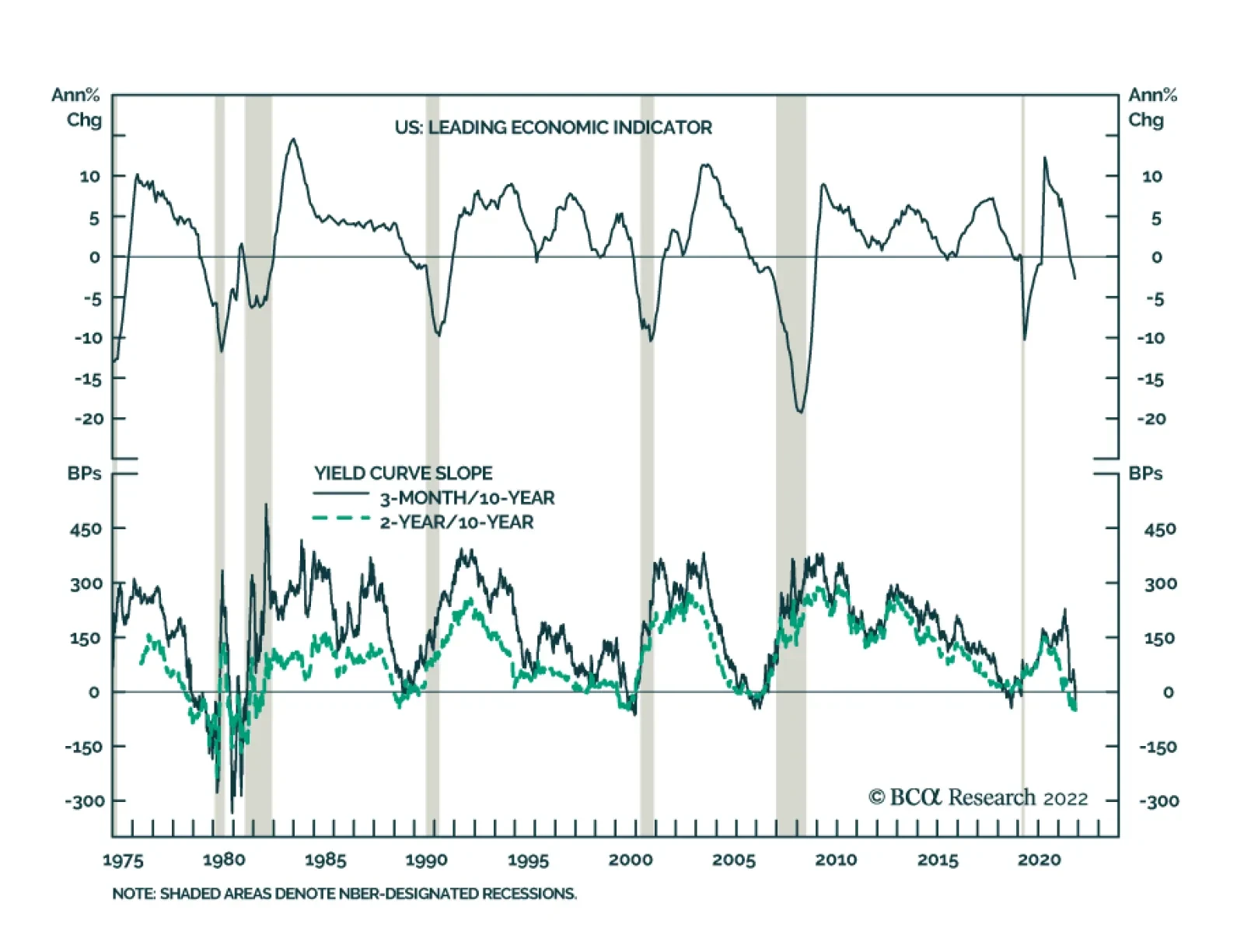

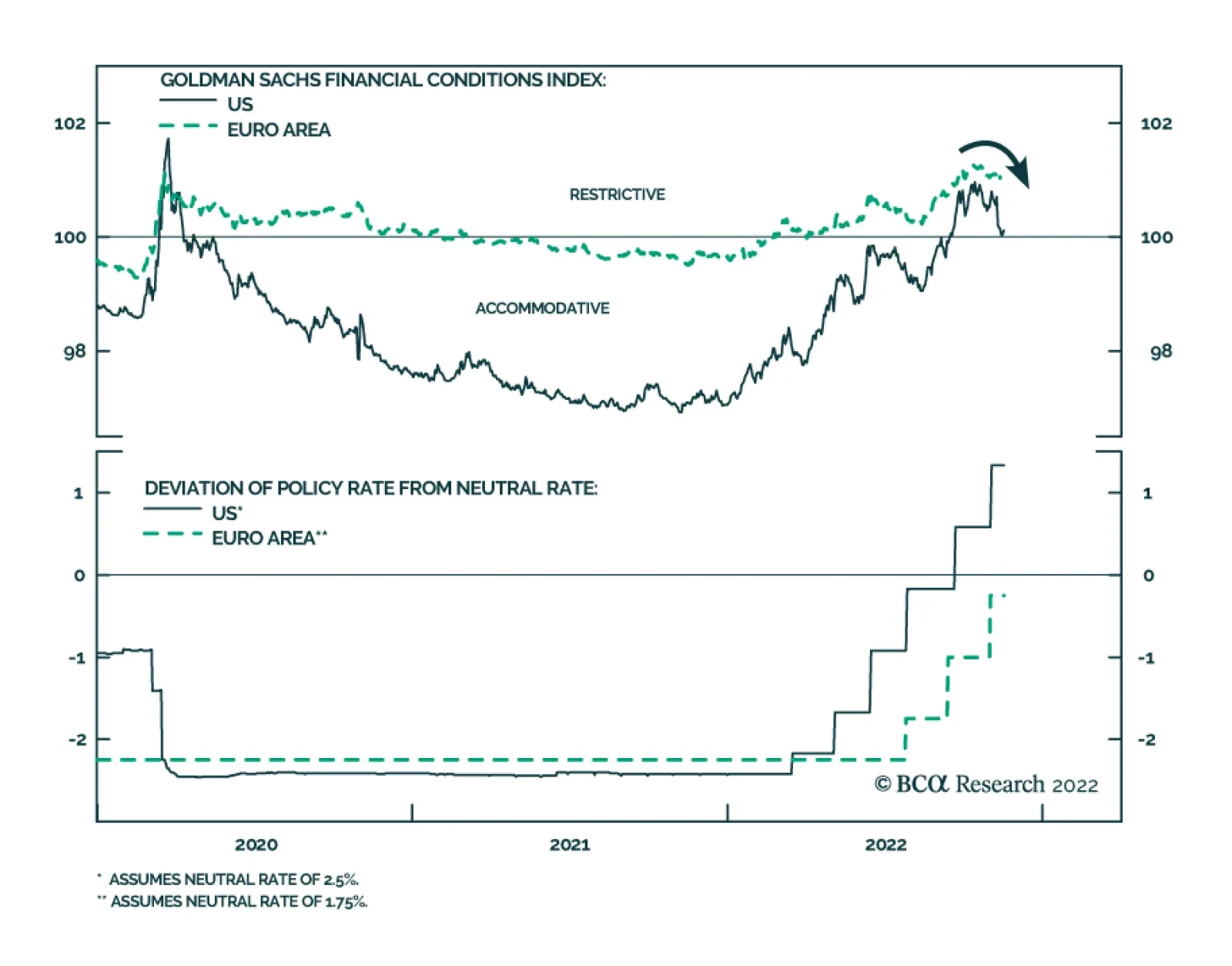

The narrative that the US can tolerate much higher interest rates, compared to the rest of the world has helped the dollar in 2022. In this report, we examine the sustainability of this thesis, from our holistic assessment of global growth indicators.

Our 4Q22 and 2023 Brent forecasts remain at $100/bbl and $116/bbl. Upside price risk continues to dominate oil markets. We remain long the XOP and COMT ETFs to retain exposure to oil and gas producers’ equities, and higher commodity prices and further backwardation, particularly in copper.