Developed Countries

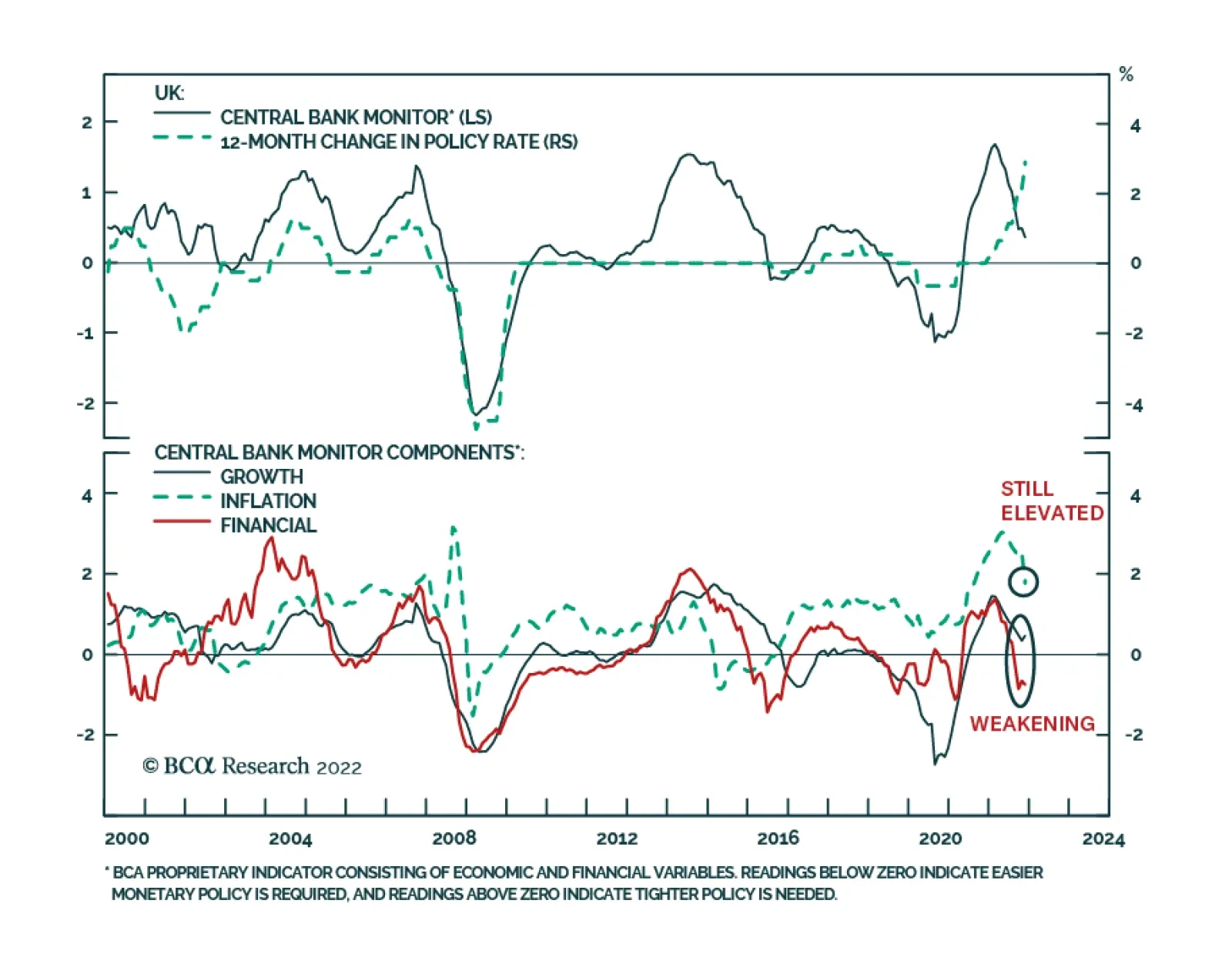

Price pressures remain intense in the UK. Headline CPI inflation jumped from 10.1% y/y to a 41-year high of 11.1% in October – surpassing expectations of a milder acceleration to 10.7%. Similarly, the month-on-month rate surged from 0.5% to 2.0%. Meanwhile,…

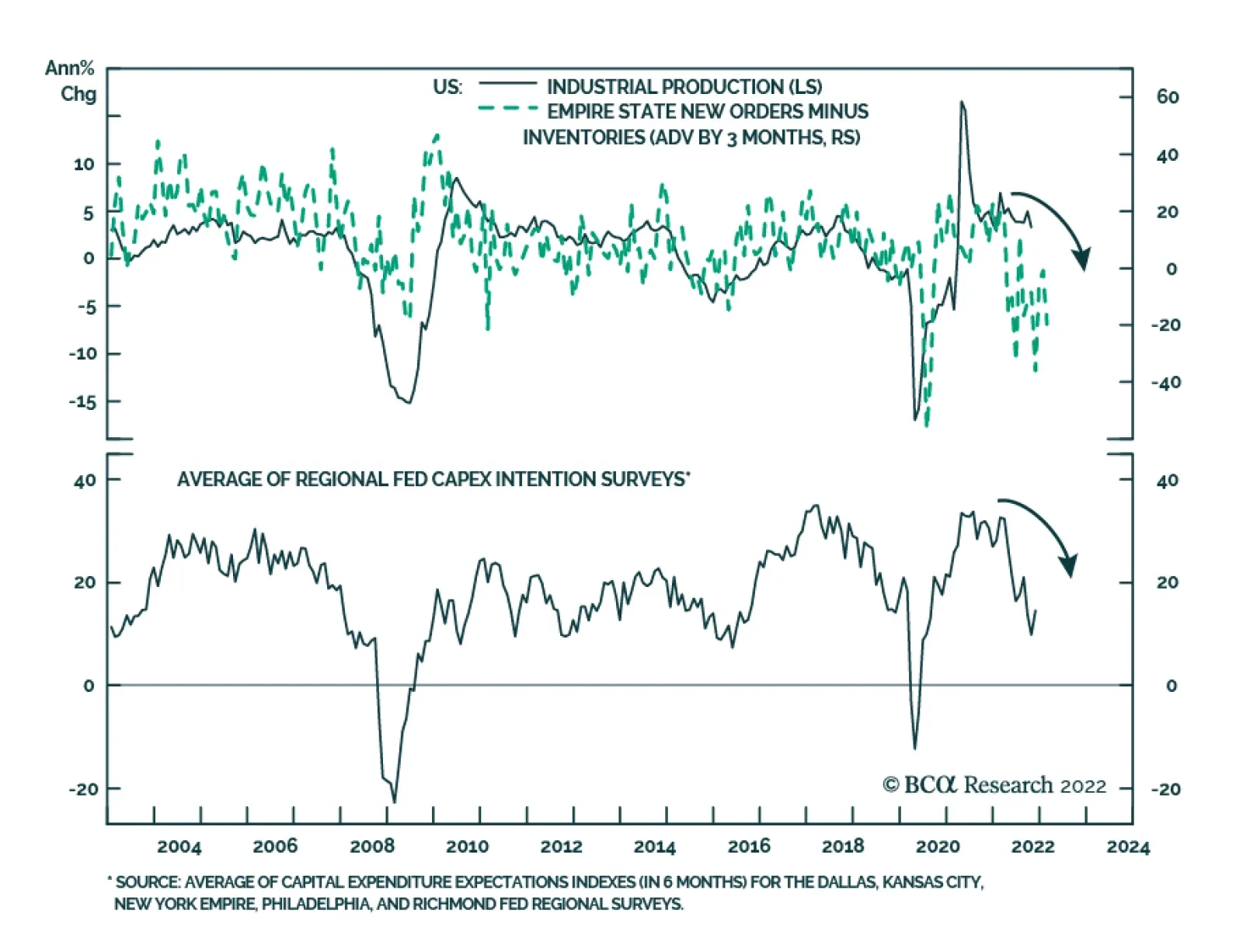

US industrial production contracted by 0.1% m/m in October, following a downwardly revised 0.1% m/m increase. Notably, manufacturing output inched up by only 0.1% m/m and the previous three months of expansion have all been revised significantly lower. …

The Reserve Bank of Australia is among the global central banks that are leading the dovish shift in the monetary tightening cycle. Specifically, elevated private sector debt raises the economy’s sensitivity to higher interest rates, ultimately limiting the…

The messages from the deteriorating fundamental backdrop (tight monetary policy, slowing global growth) and improved credit valuation (elevated 12-month breakeven spreads) are giving conflicting signals on corporate bond strategy. We are putting more weight on the fundamentals and are staying with an overall underweight stance on global investment grade corporates, with a slight bias towards Europe given more attractive spread valuations. At the same time, we see selective opportunities in sectors where risk-adjusted spreads are wide as signaled by our individual country sector valuation models, like US Energy and euro area Financials.

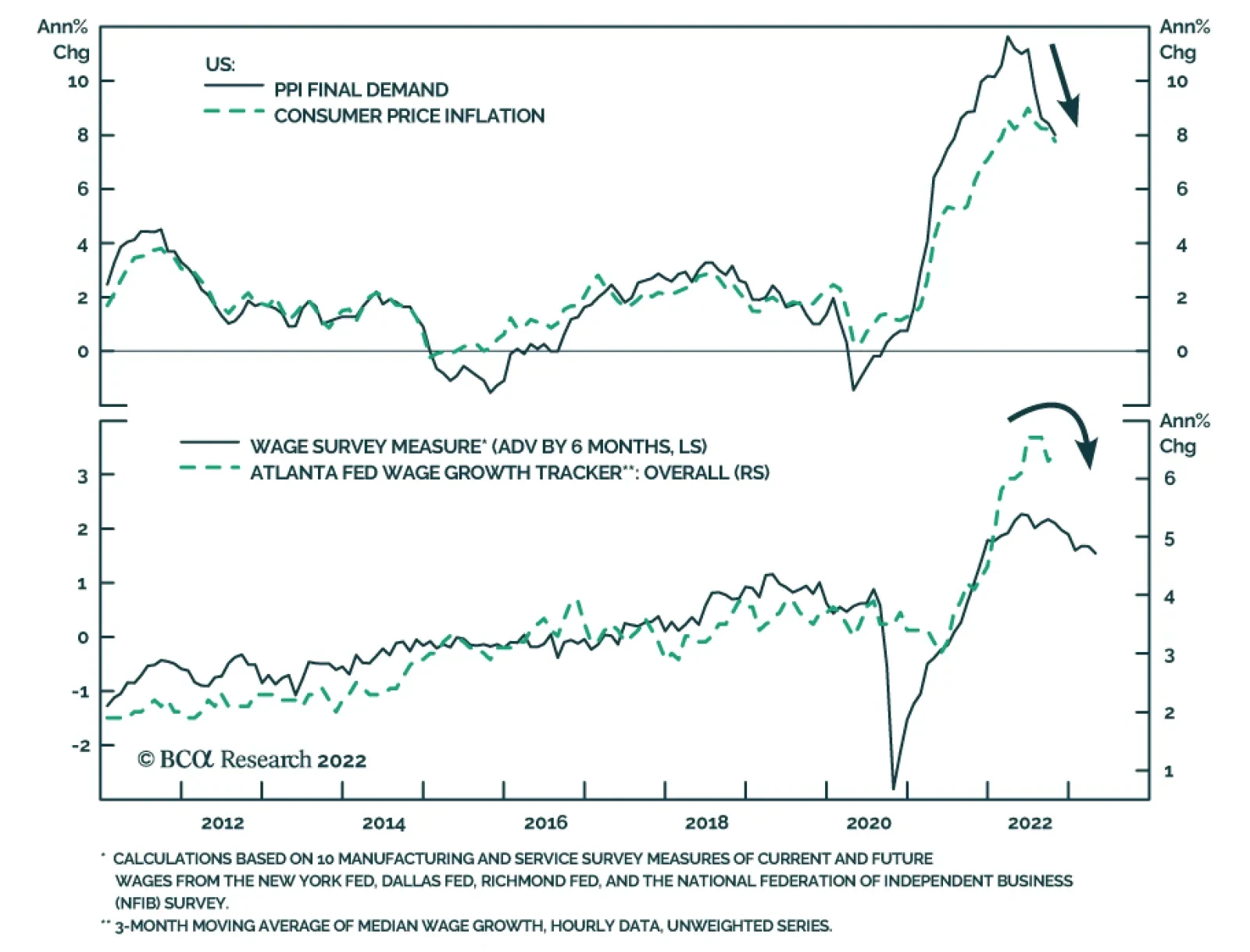

US PPI inflation slowed to a lower-than-expected 8.0% y/y in October from a downwardly revised 8.4% y/y. Similarly, core PPI inflation eased to 6.7% y/y from 7.1% y/y, below expectations of 7.2% y/y. Both core goods and services contributed to the decline. …

November’s reading of the ZEW Indicator of Economic Sentiment reveals that investors are becoming less pessimistic about the Eurozone economy. The expectations and current situation indices for Germany and the Euro Area jumped significantly above consensus…

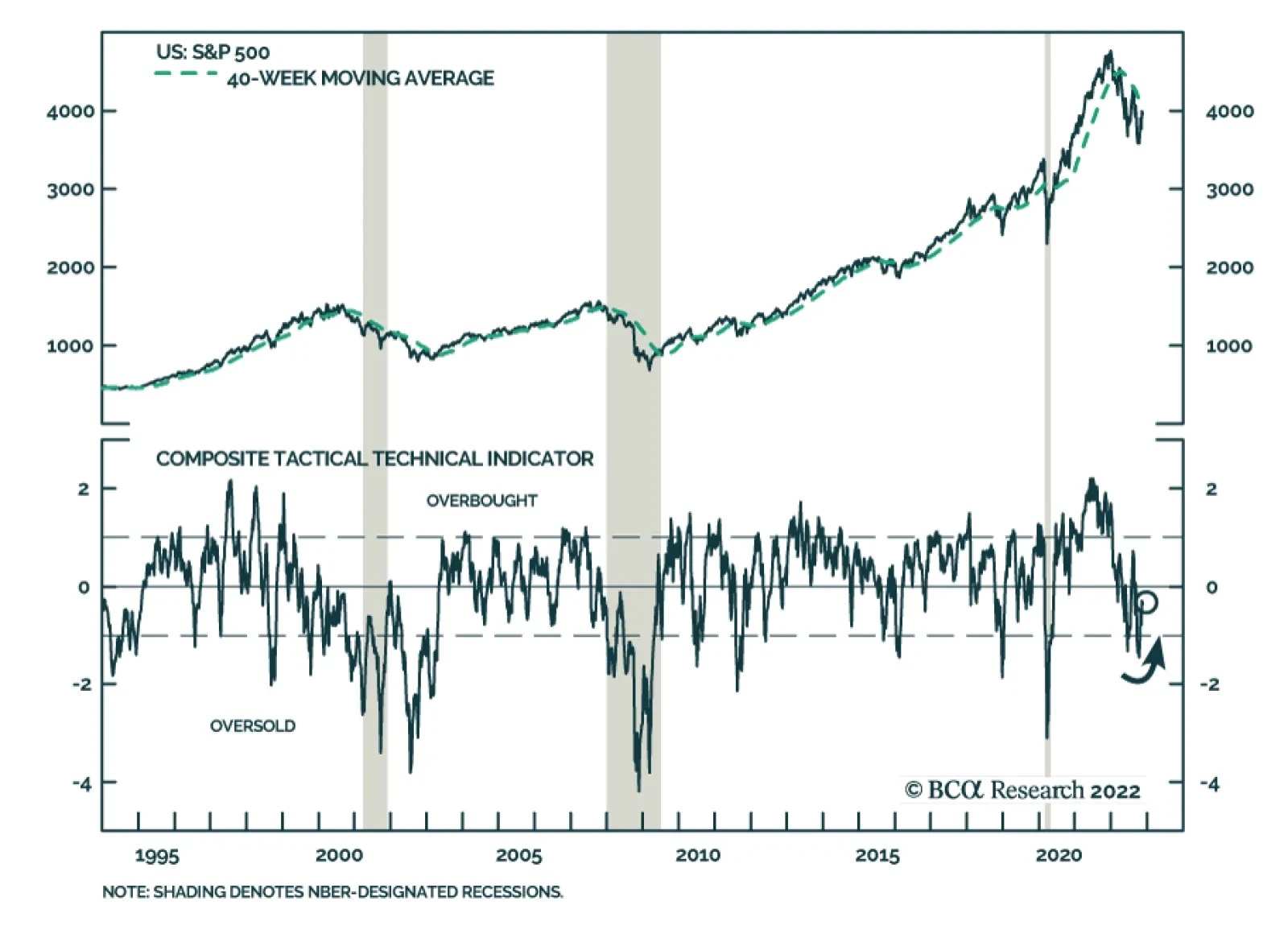

The Fed’s aggressive hawkish pivot at the start of the year triggered a sharp selloff in US equities that pushed the S&P 500 deep in oversold territory. Just one month ago, our composite tactical technical indicator was signaling that the equity drawdown…

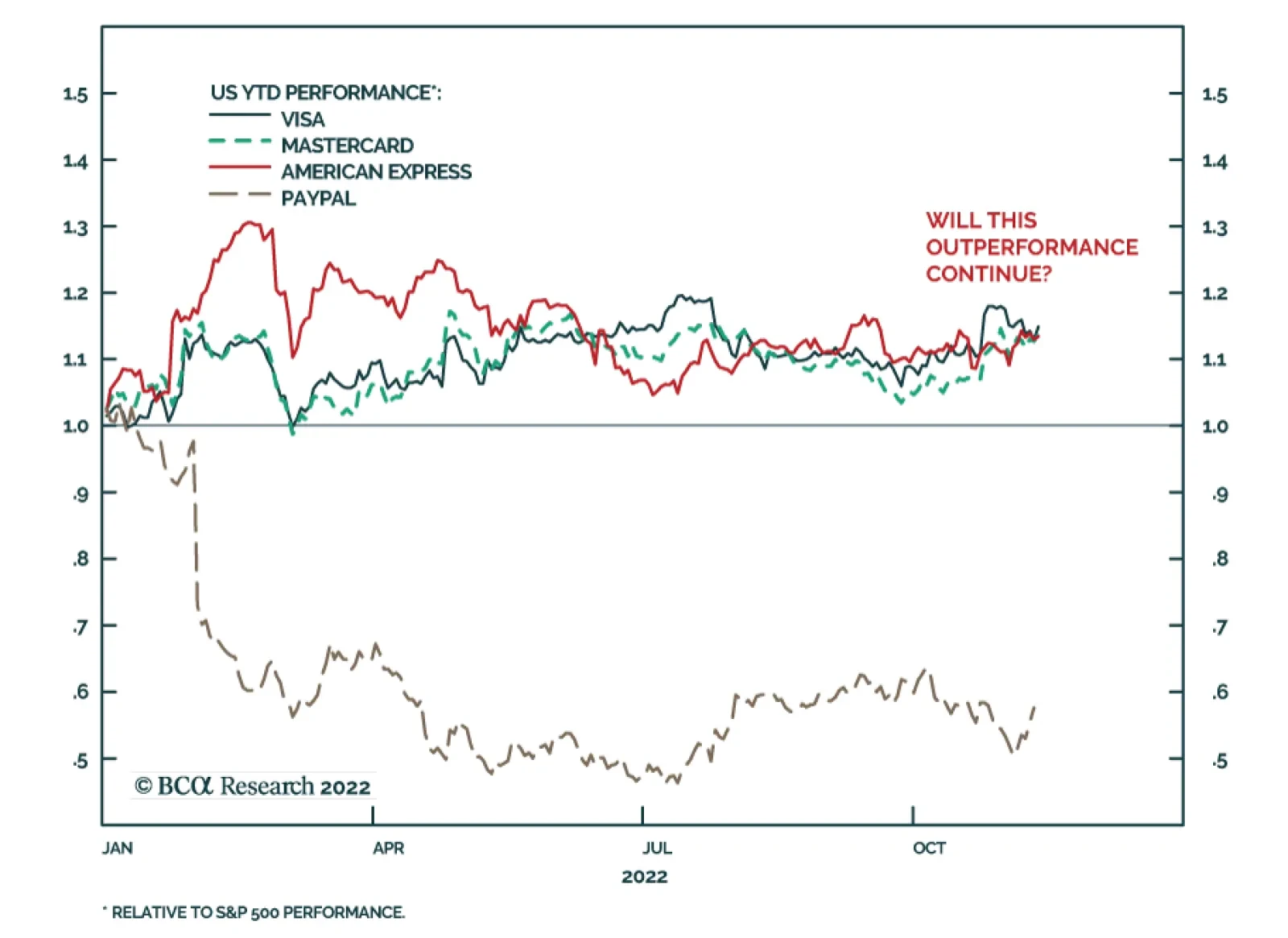

BCA Research’s US Equity Strategy service is overweight credit card companies, but only over a short investment horizon. All of the largest credit card processing companies, such as Visa, Mastercard, and American Express, have delivered strong Q3-22 sales…

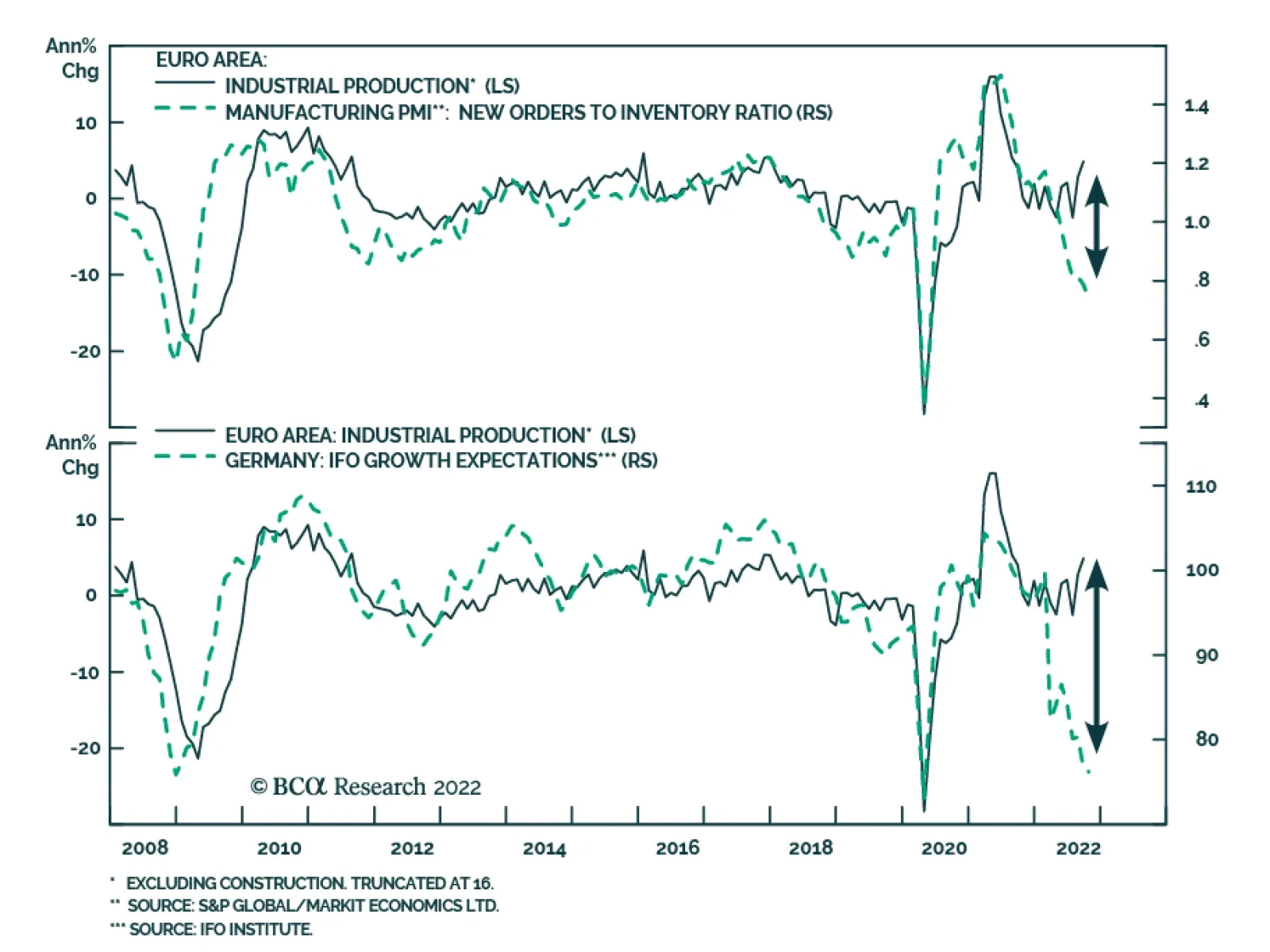

Euro Area industrial production expanded by 4.9% y/y in September, following an upwardly revised 2.8% y/y and beating expectations of a 3.0% y/y increase. Similarly, the 0.9% m/m increase also exceeded consensus estimates of 0.5% m/m. Higher production of…

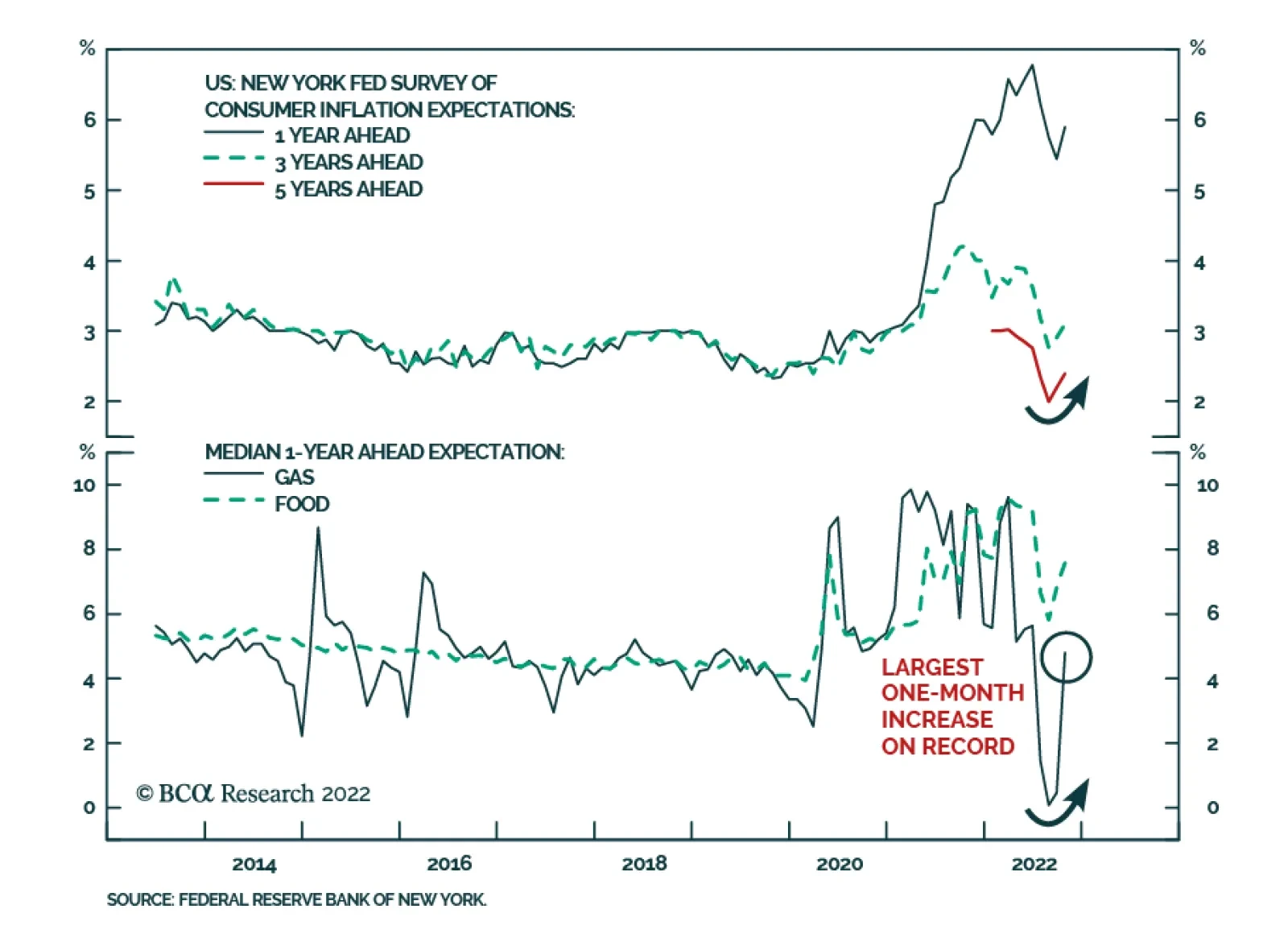

Results from the New York Fed’s October Survey of Consumer Expectations underscore that the Fed still has its work cut out for it. Household inflation expectations rebounded with median one-year-ahead expectations increasing from 5.4% to 5.9%,…