Developed Countries

This week’s report examines the state of the global monetary tightening cycle and addresses some frequently asked questions about the Fed’s QT program. New yield curve trades are recommended for the US and German yield curves.

This Fed is a single mandate Fed which won’t consider the job done until inflation reaches a 2% target. Concerns about slowing growth will displace concerns about inflation. Equities will bottom shortly before economic growth bottoms. Until then we recommend a defensive portfolio tilt, and offer a few tactical and strategic ideas for the overweights.

Stay short Greater China assets. Stay long Japanese yen. Hold back on Brazil for now but look forward to opportunities in future.

The ECB increased interest rates and announced the start of its balance sheet wind down; yet, markets took the news as a dovish outcome. Are we really getting close to the end of the ECB’s tightening campaign? How asset prices will react?

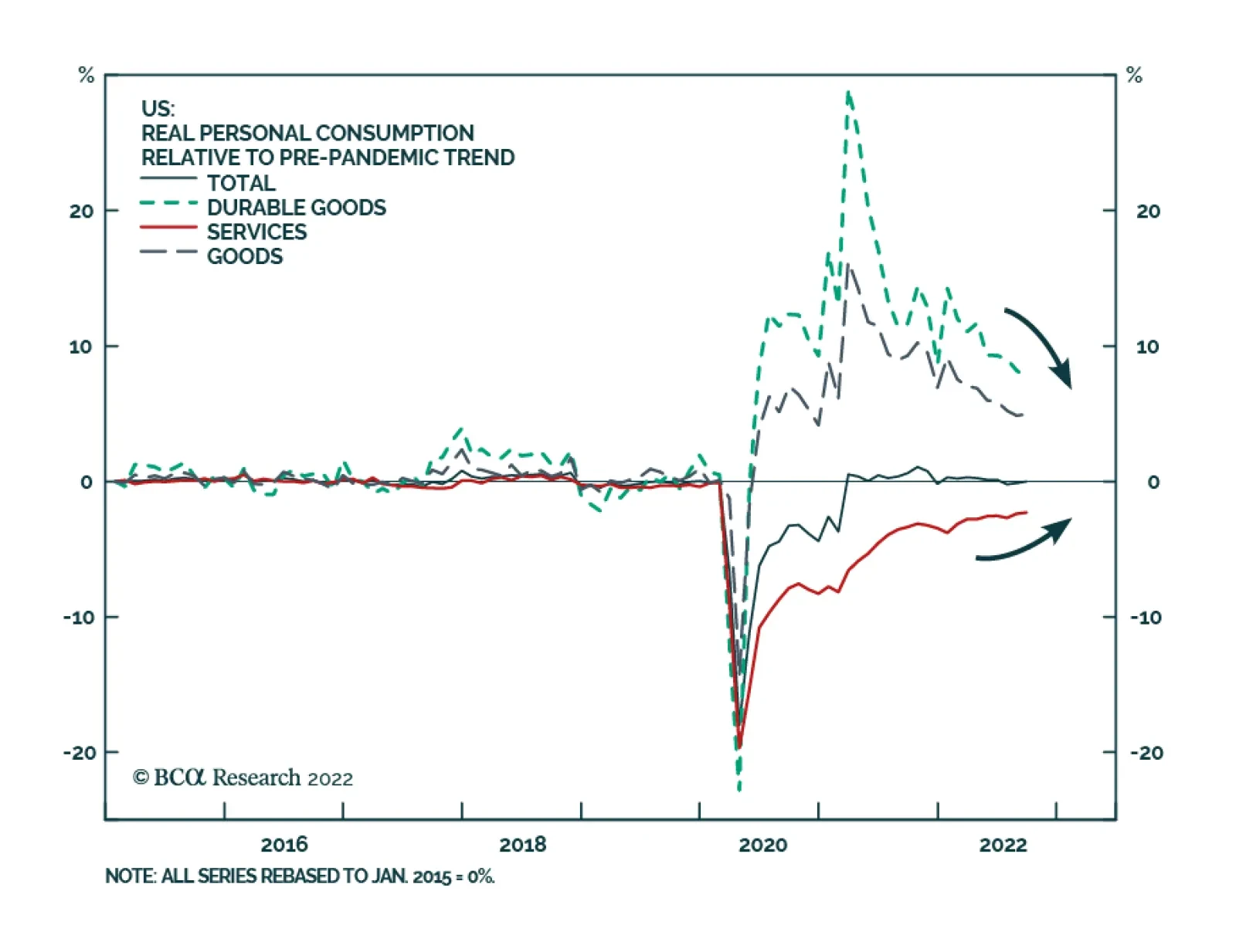

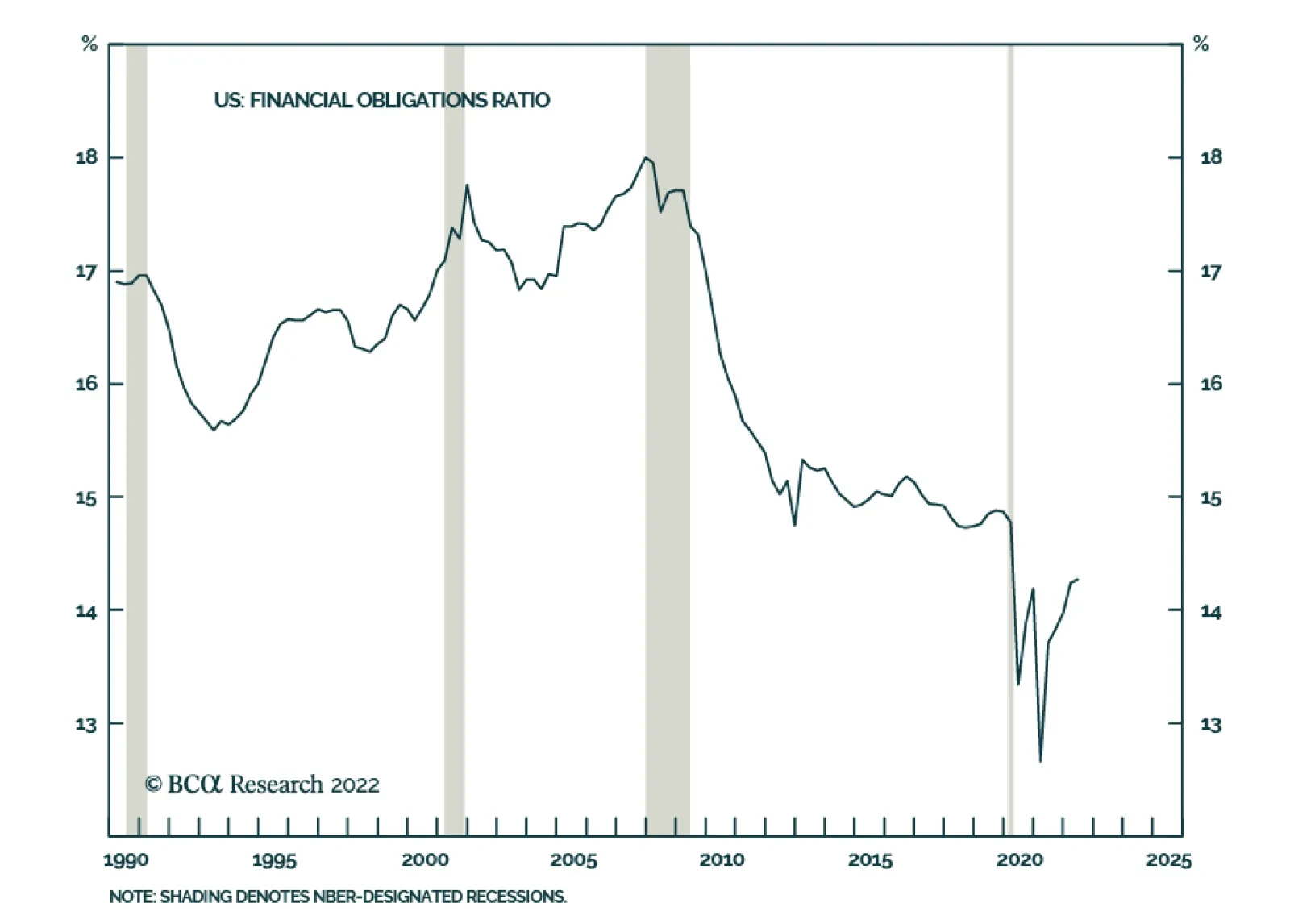

We remain constructive on the economy and equities in the near term because consumers show no sign of hunkering down, US homeowners are largely impervious to higher mortgage rates and our latest survey of storefront occupancies on Lower Fifth Avenue highlighted some encouraging developments.