Developed Countries

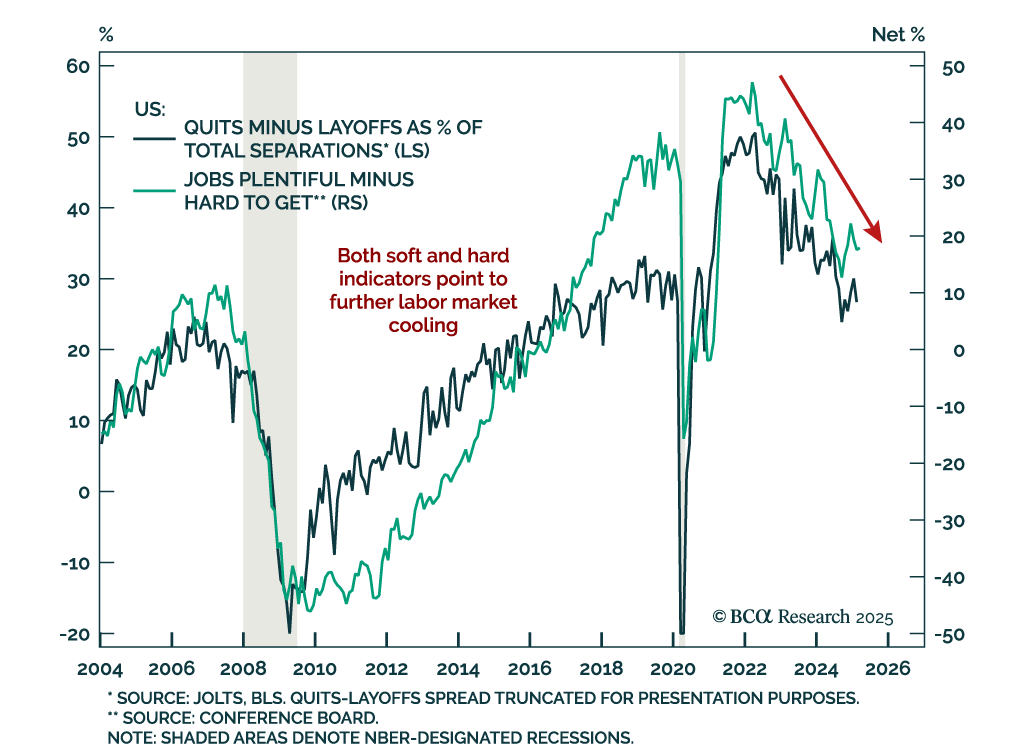

Labor market data continues to cool, reinforcing our overweight in government bonds and above-benchmark duration stance. February job openings fell to 7.6m, below expectations. Declining quits and rising layoffs signal that labor market slack is increasing.…

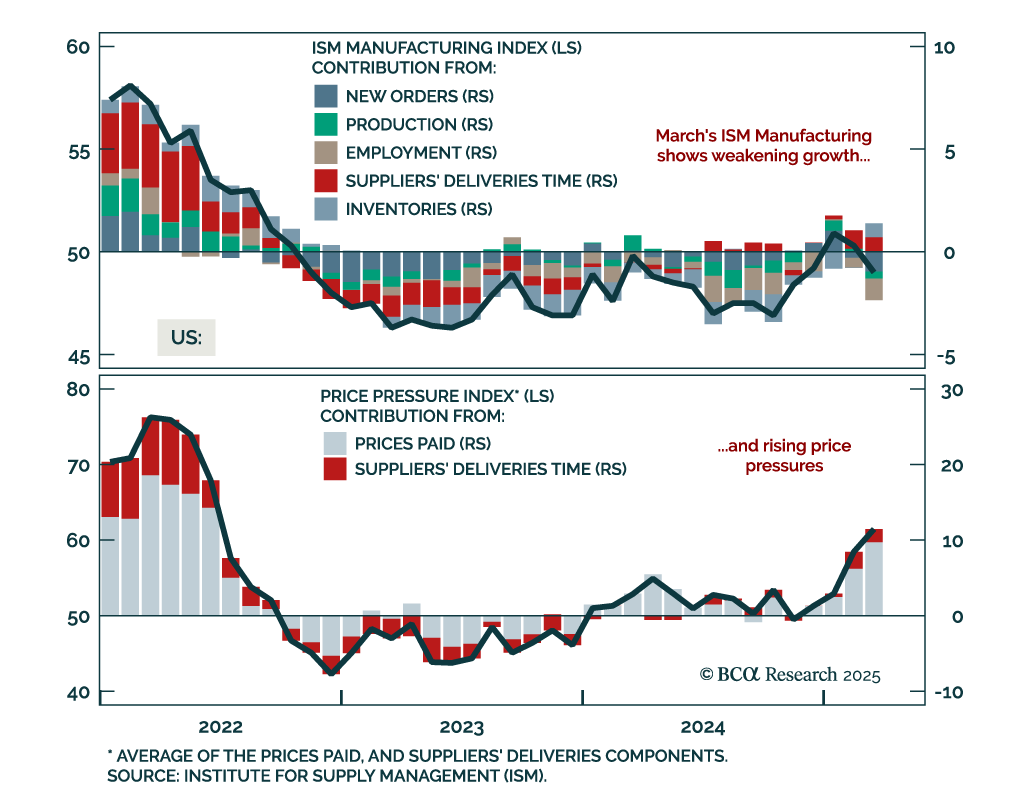

The March ISM Manufacturing adds to the recent stagflationary impulse, but markets remain focused on the growth drag, reinforcing our defensive asset allocation. The headline index fell more than expected to 49.0 from 50.3, with new orders and employment…

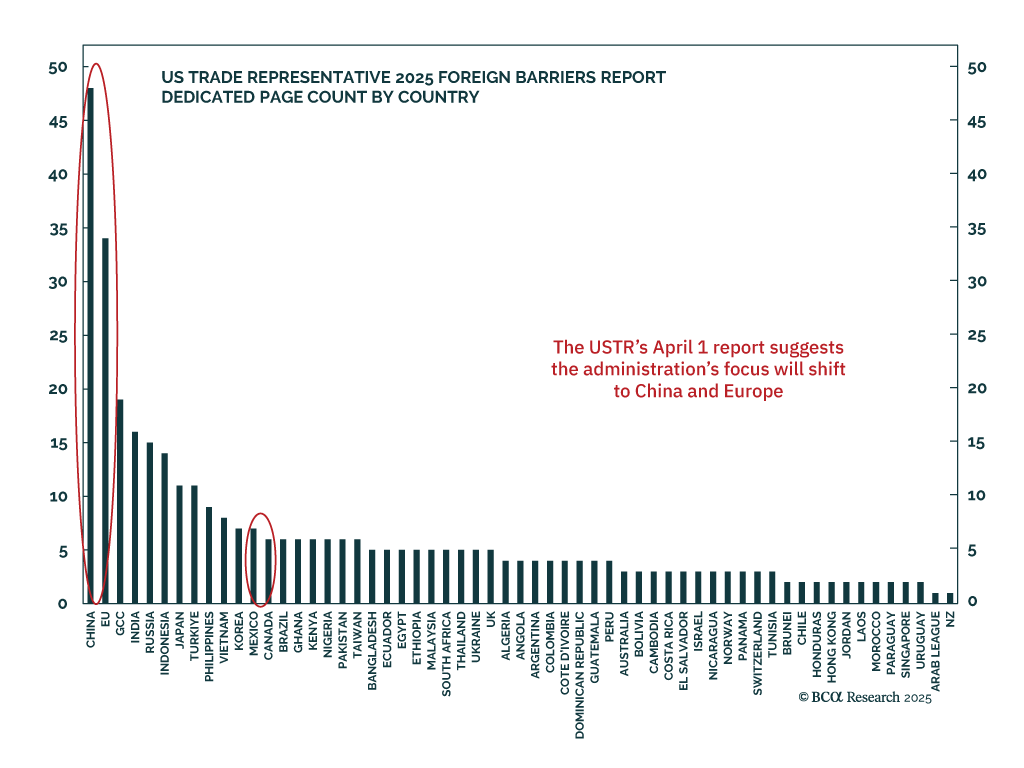

April 2 may mark peak trade tensions, but the path forward remains highly uncertain, supporting our underweight on risk assets and industrial commodities. The USTR’s long-awaited report on trade barriers will guide the next phase of US trade policy. While the…

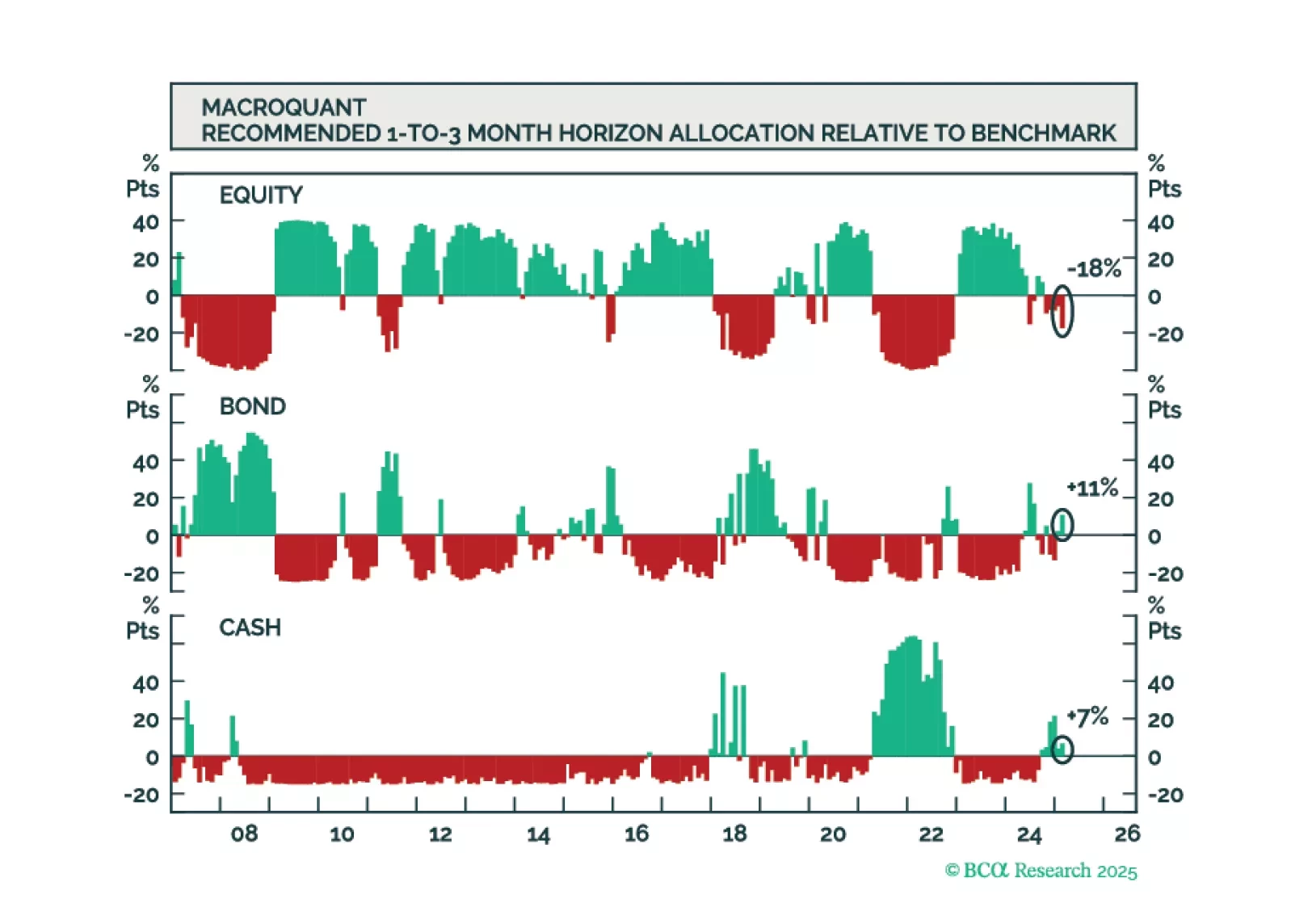

Going into April, MacroQuant recommends a modest underweight on stocks, offset by an overweight on bonds and cash. While MacroQuant is modestly bearish on stocks, we suspect that the downside risks to equities may be greater than what the model assumes.

Going into April, MacroQuant recommends a modest underweight on stocks, offset by an overweight on bonds and cash. While MacroQuant is modestly bearish on stocks, we suspect that the downside risks to equities may be greater than what the model assumes.

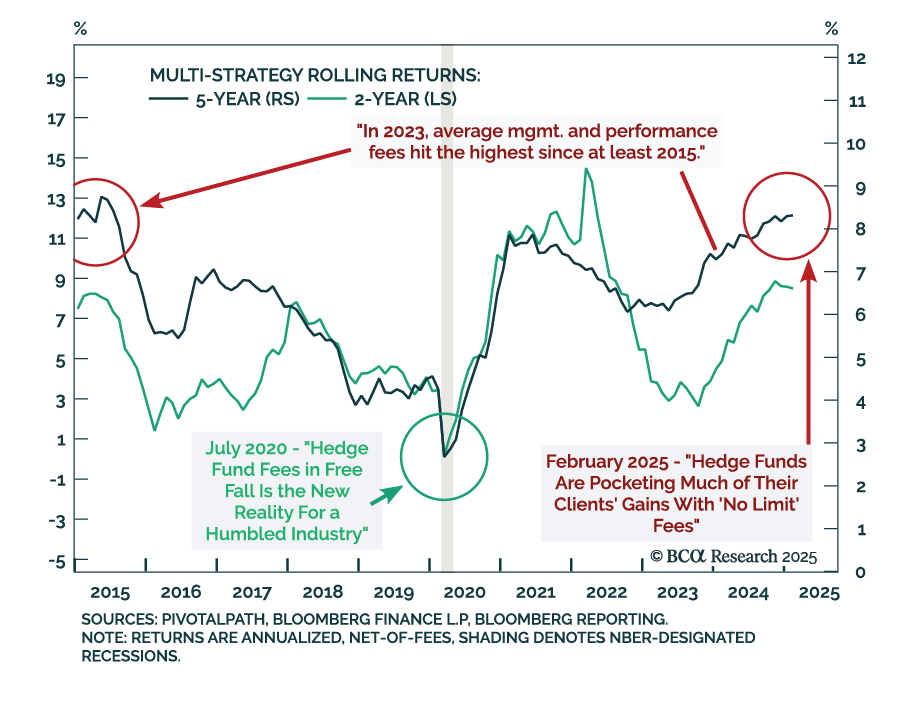

Our Private Markets & Alternatives strategists remain structurally positive but cyclically underweight on Multi-Strategy Hedge Funds. While these funds have delivered consistent alpha and valuable diversification, current market conditions offer more…

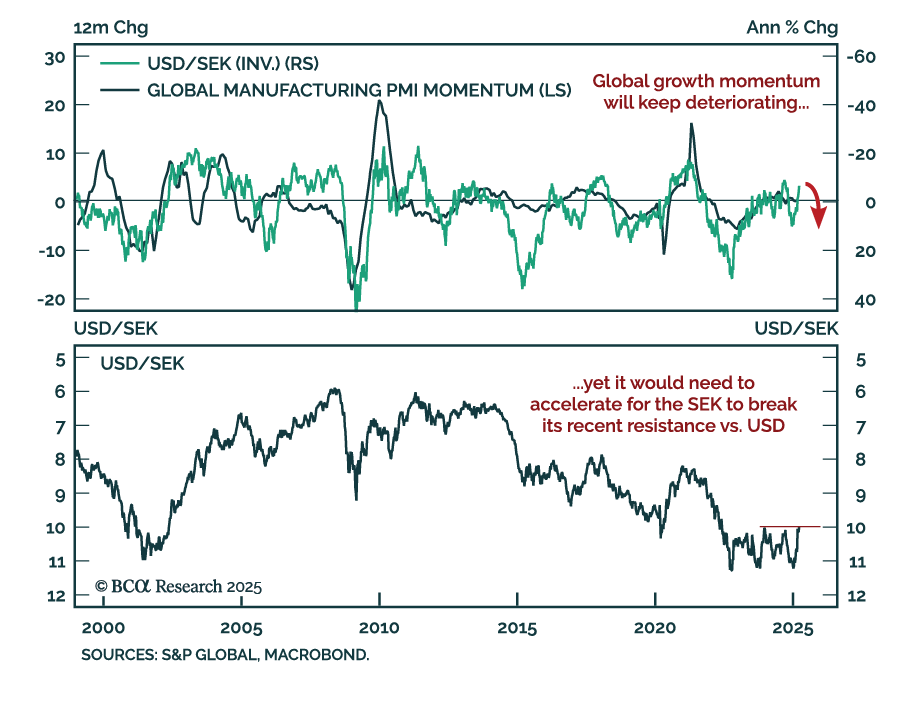

The SEK’s sharp rally is losing steam as local data weakens and EUR strength looks stretched. After appreciating more than 10% against the USD year-to-date, the krona is now showing signs of fatigue. Recent Swedish data has disappointed, with the Economic…

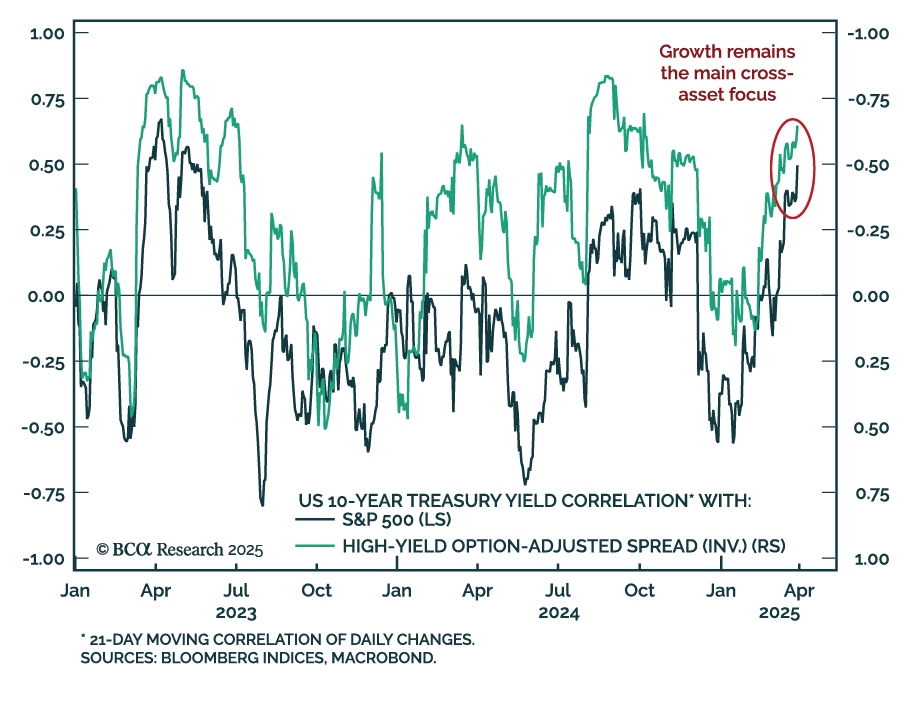

Markets are responding to the growth drag of stagflation, not the inflation impulse, reinforcing our defensive stance. Despite rising short-term inflation pressures in the US, risk assets and bond yields continue to move together, with the stock–bond yield…

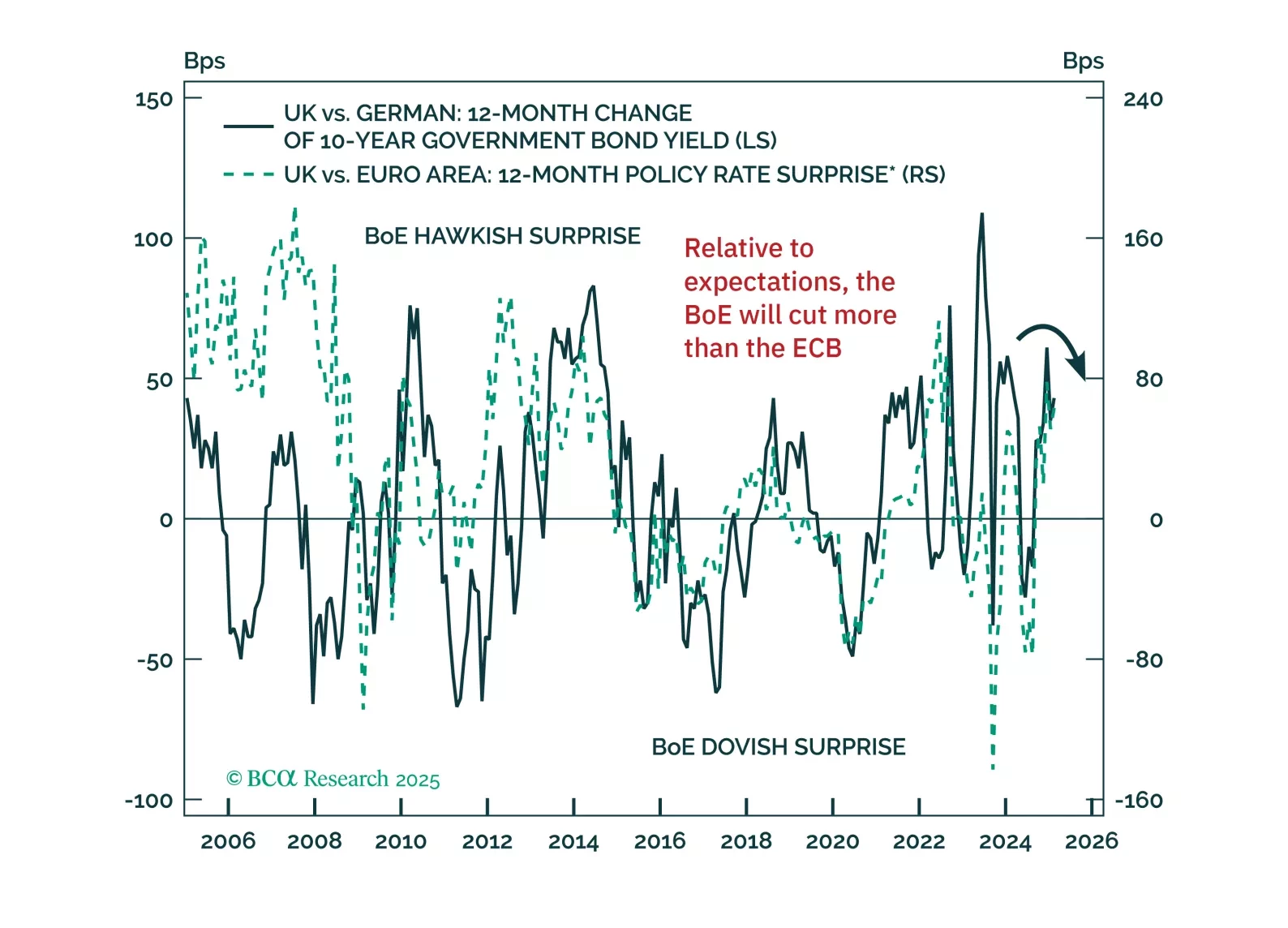

With economic headwinds building and fiscal dynamics shifting, bond markets are at a turning point. Our latest note outlines why German bund yields are set to decline and why UK gilts are poised to outperform — and how to position accordingly.

Markets may be bracing for April 2, but the real surprise could be how unsurprising it ends up being. Our Chart Of The Week comes from GeoMacro Chief Strategist Marko Papic, who sees the looming tariff salvo as the peak of de-globalization panic. With Beltway…