Developed Countries

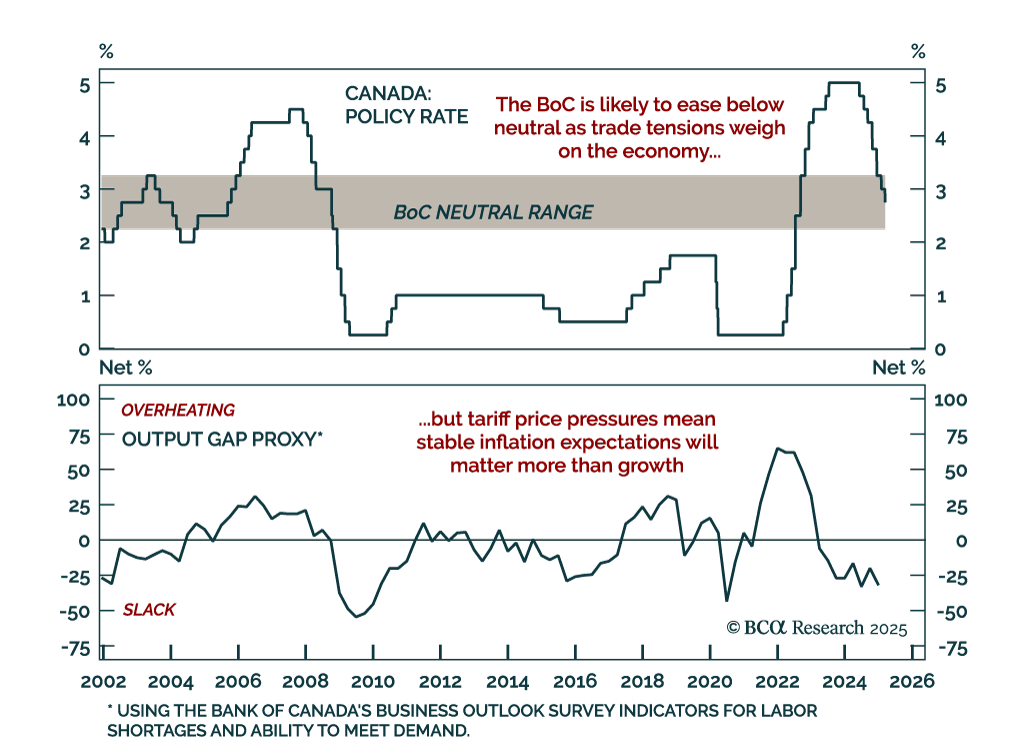

The Bank of Canada cut by 25 bps to 2.75% as expected. This seventh consecutive cut brings the policy rate further into neutral territory, estimated to be in the 2.25%-to-3.25% range. The BoC is in a tough place. The trade war will ultimately be…

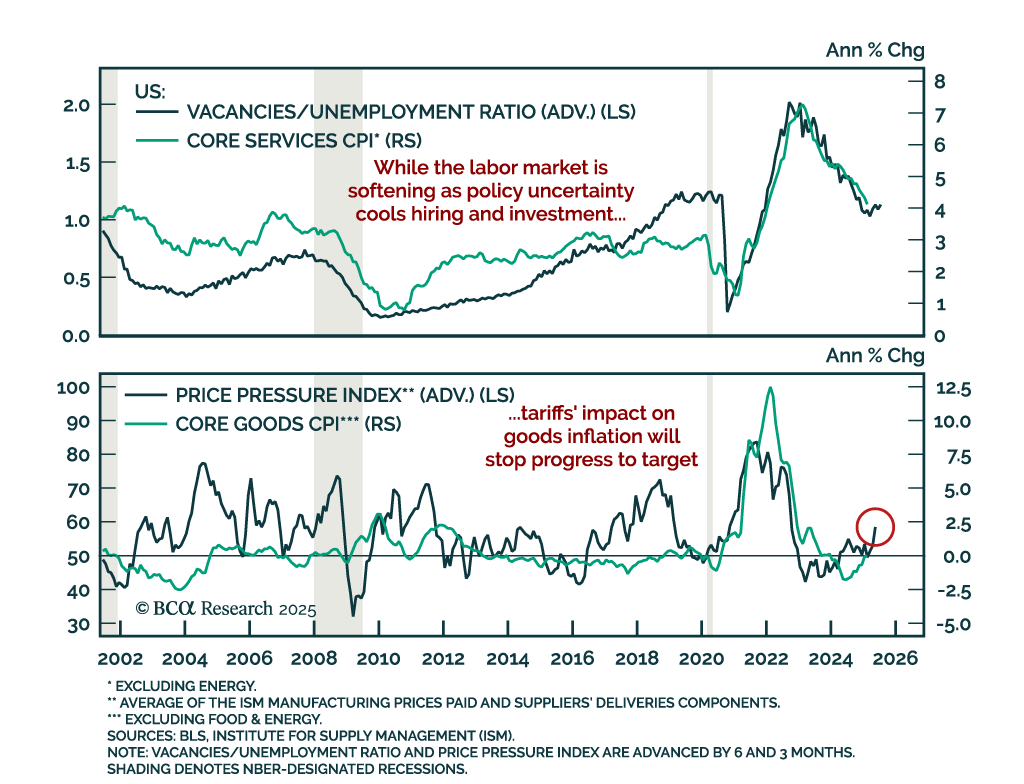

The February US CPI came in cooler than expected. Headline inflation decelerated to 0.2% m/m (2.8% y/y), as did core which now stands at 3.1% y/y. Core services inflation declined while core goods inflation was roughly unchanged. Inflation is headed…

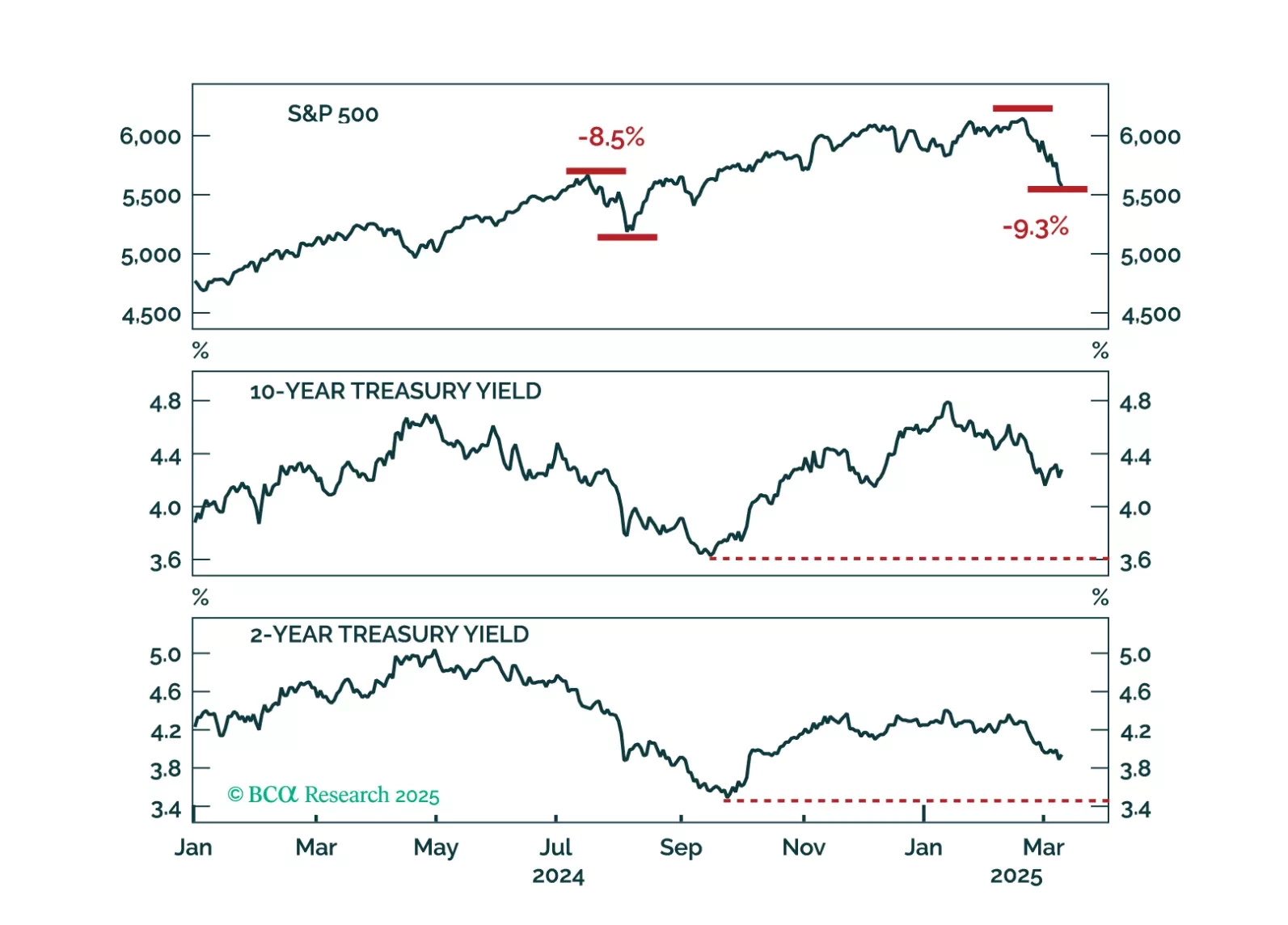

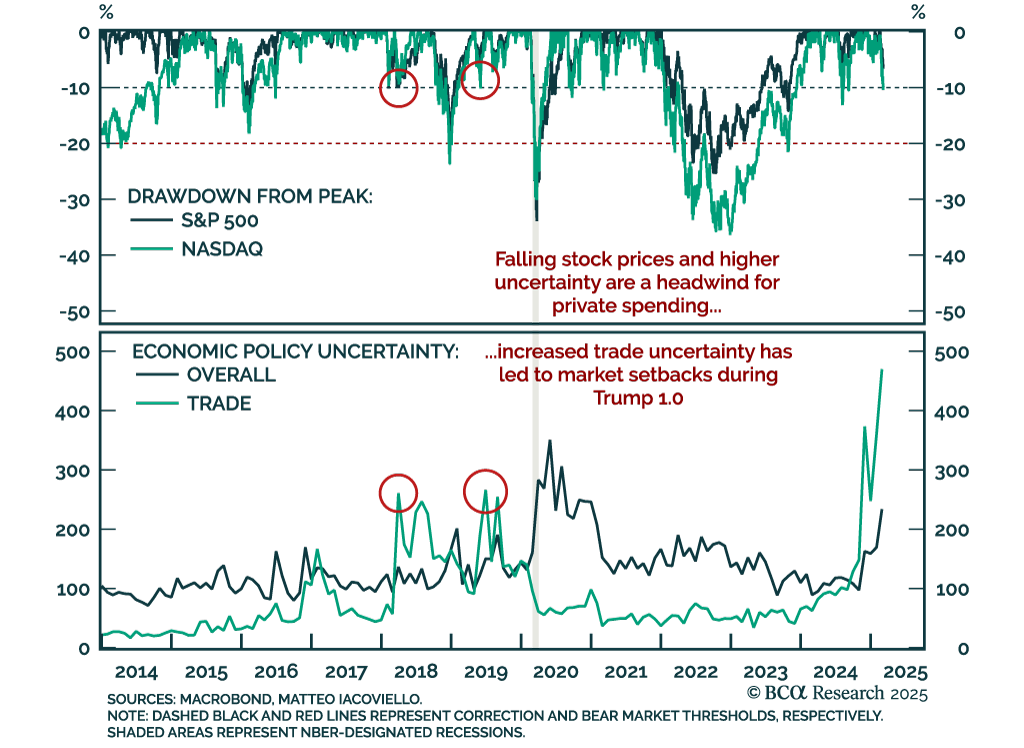

A falling stock market and sticky bond yields represent the worst of both worlds for investors. We interrogate why bond yields haven’t dropped more given the large selloff seen in equities.

Our US investment strategists believe the Trump administration’s resolve to cut spending as well as tariff uncertainty have increased the probability of a recession.The Department of Government Efficiency’s sweeping cuts may accelerate a US recession,…

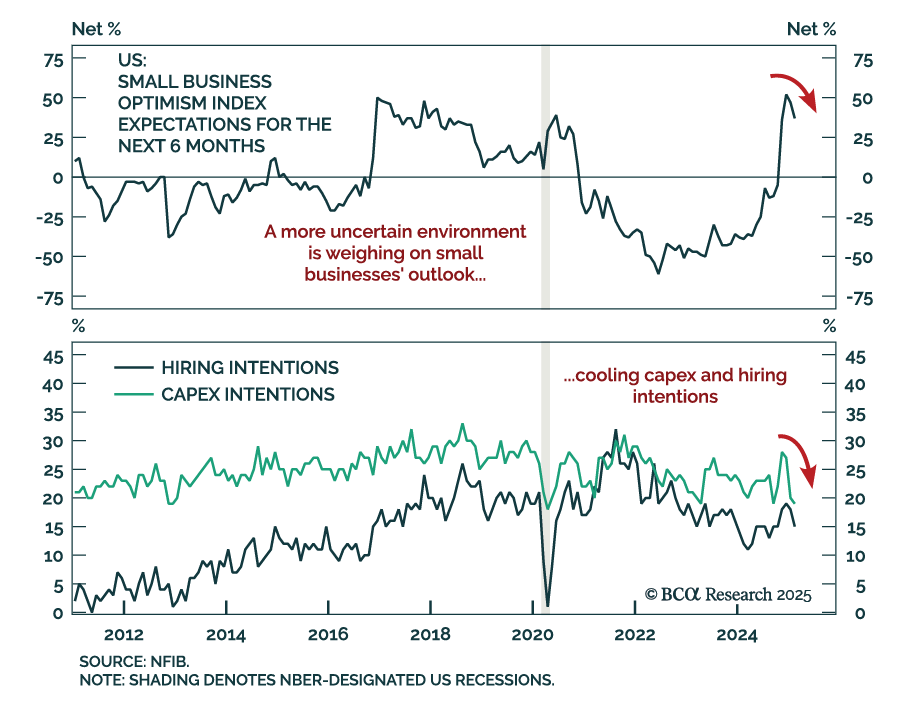

The February NFIB Small Business Optimism index decreased more than expected to 100.7 from 102.8. The decline extends the reversal seen since the November US election as policy optimism yields to uncertainty. The signal from the report was stagflationary…

After affirming he does not look at the stock market, President Trump said he cannot exclude the possibility of a recession as he rushes to implement his agenda before the 2026 midterms. Could a President willingly start a recession? A President’s…

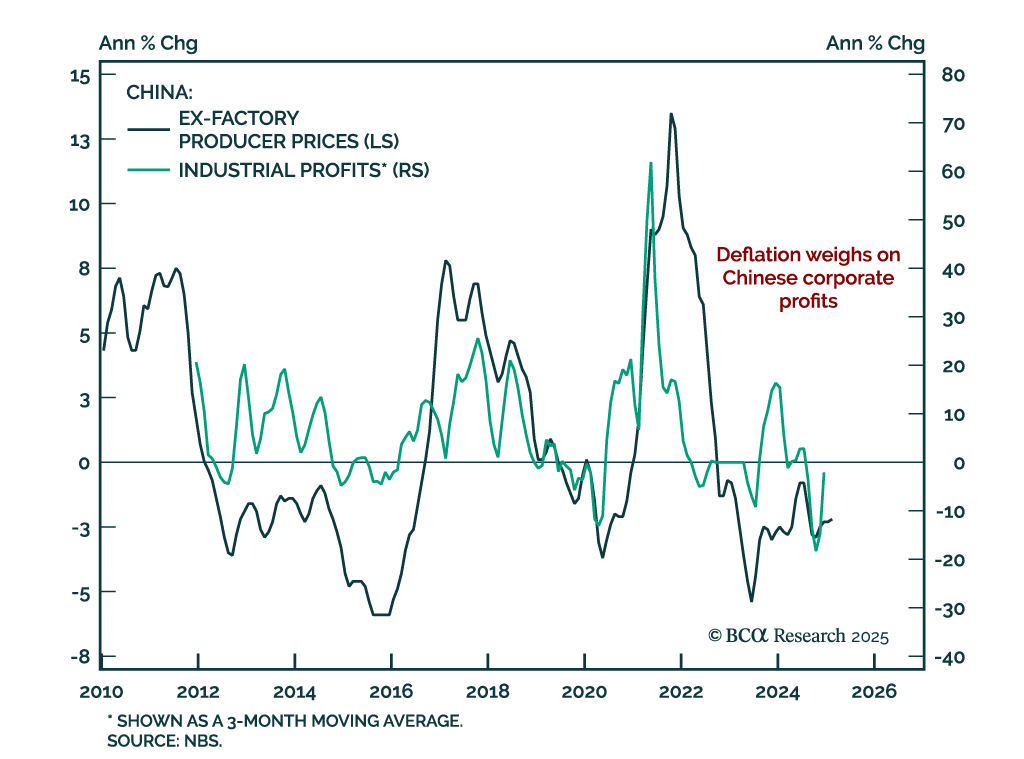

China’s February consumer prices fell 0.7% y/y after expanding on an annual basis in January. Producer price deflation stood at -2.2% y/y, roughly unchanged from a month prior. China’s first quarter data is heavily influenced by seasonality, as the shifting…

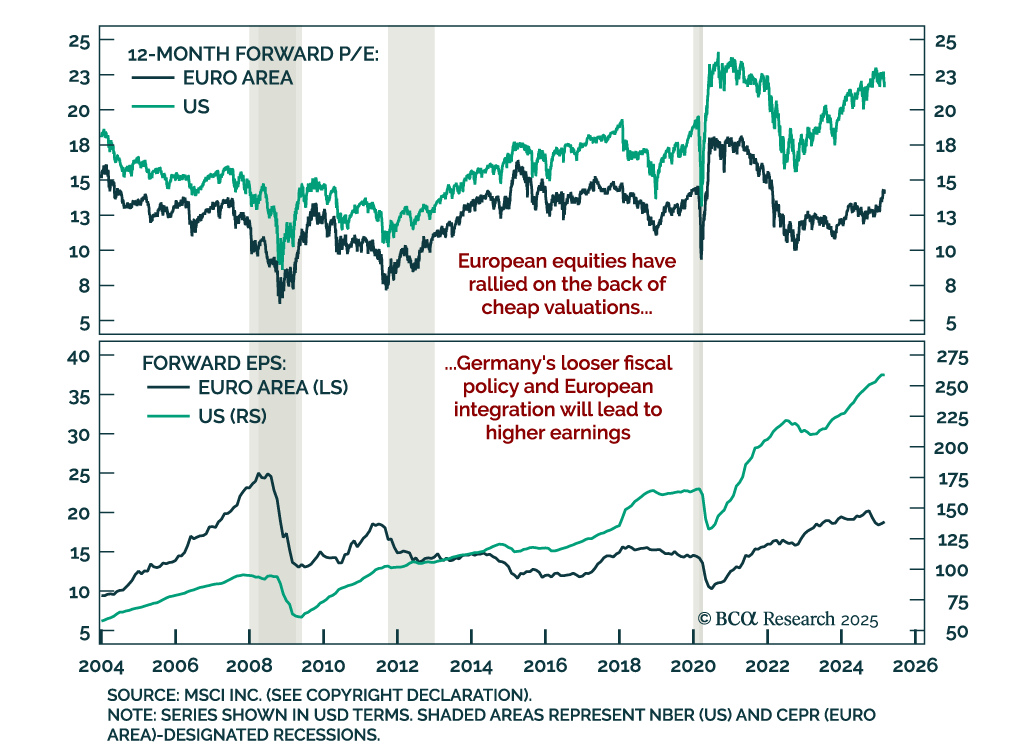

After entering 2025 with depressed growth expectations, measures of European sentiment have seemingly bottomed, and European assets rallied. However, given the changing geopolitical order and Europe’s forceful response thus far, are we at a structural turning…

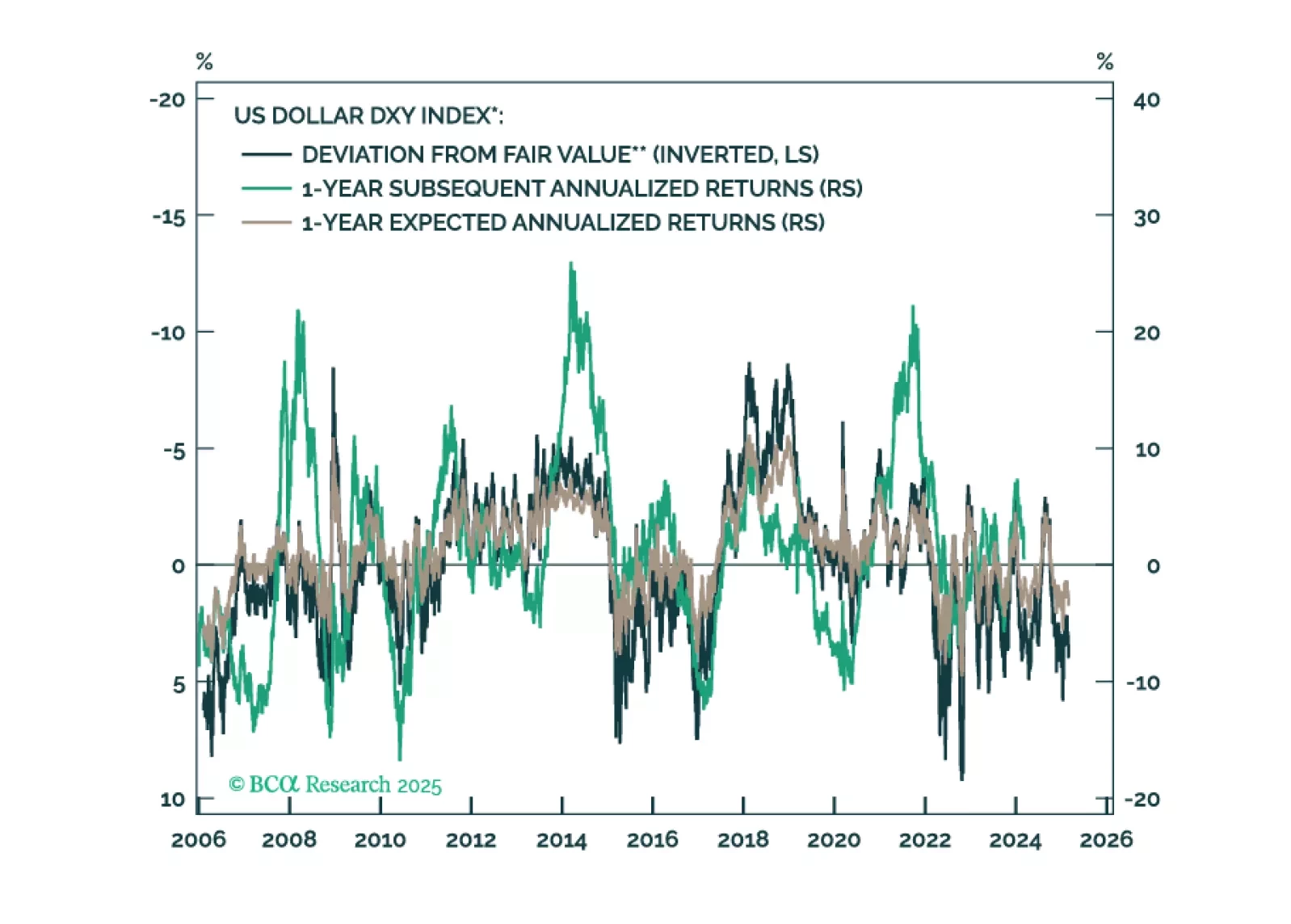

This report is our Part III series on valuation and subsequent returns, where we recalibrate our short-term models to emphasize signals over the next nine-to-twelve months. We will henceforth call these models STTM: Short Term Timing Models.

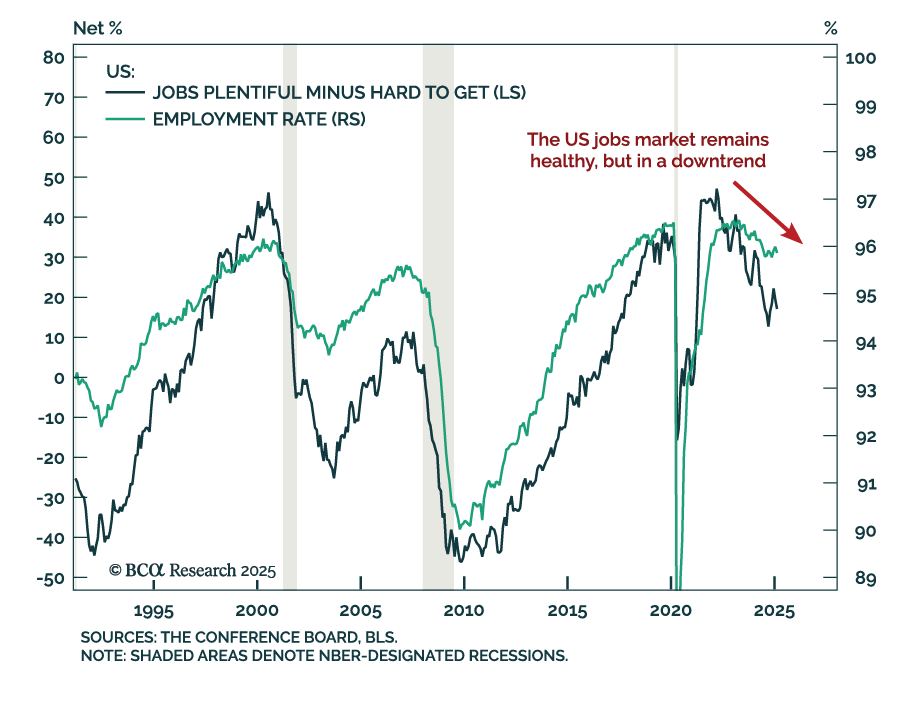

The February US jobs report was slightly weaker than expected, reflecting a slowing but still healthy labor market. At 151k, payrolls missed estimates. January’s number was revised down from 143k to 125k, bringing the 3-month moving average below 200k. The…