Developed Countries

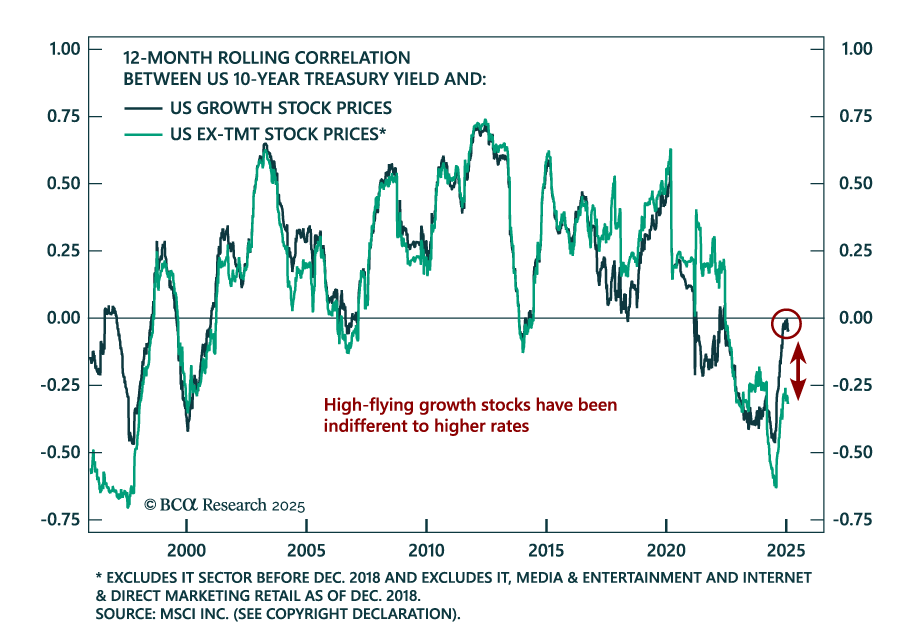

Our Chart Of The Week comes from Arthur Budaghyan, Chief Strategist of our Emerging Markets and China Investment Strategy services. Arthur highlights an important dichotomy in the US stock-bond yield correlation. In the past 12 months, US growth stocks…

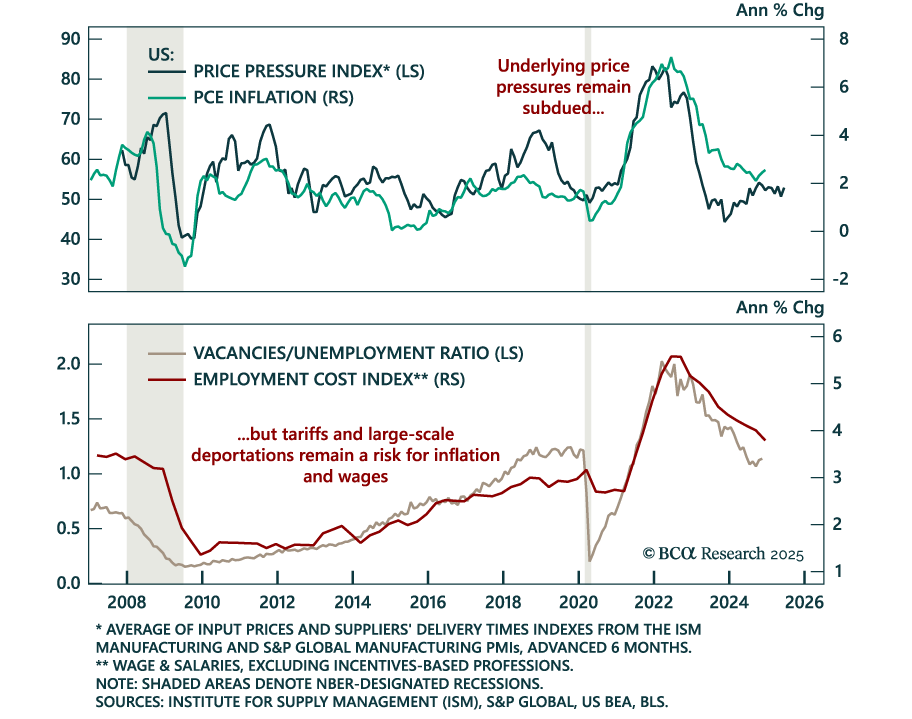

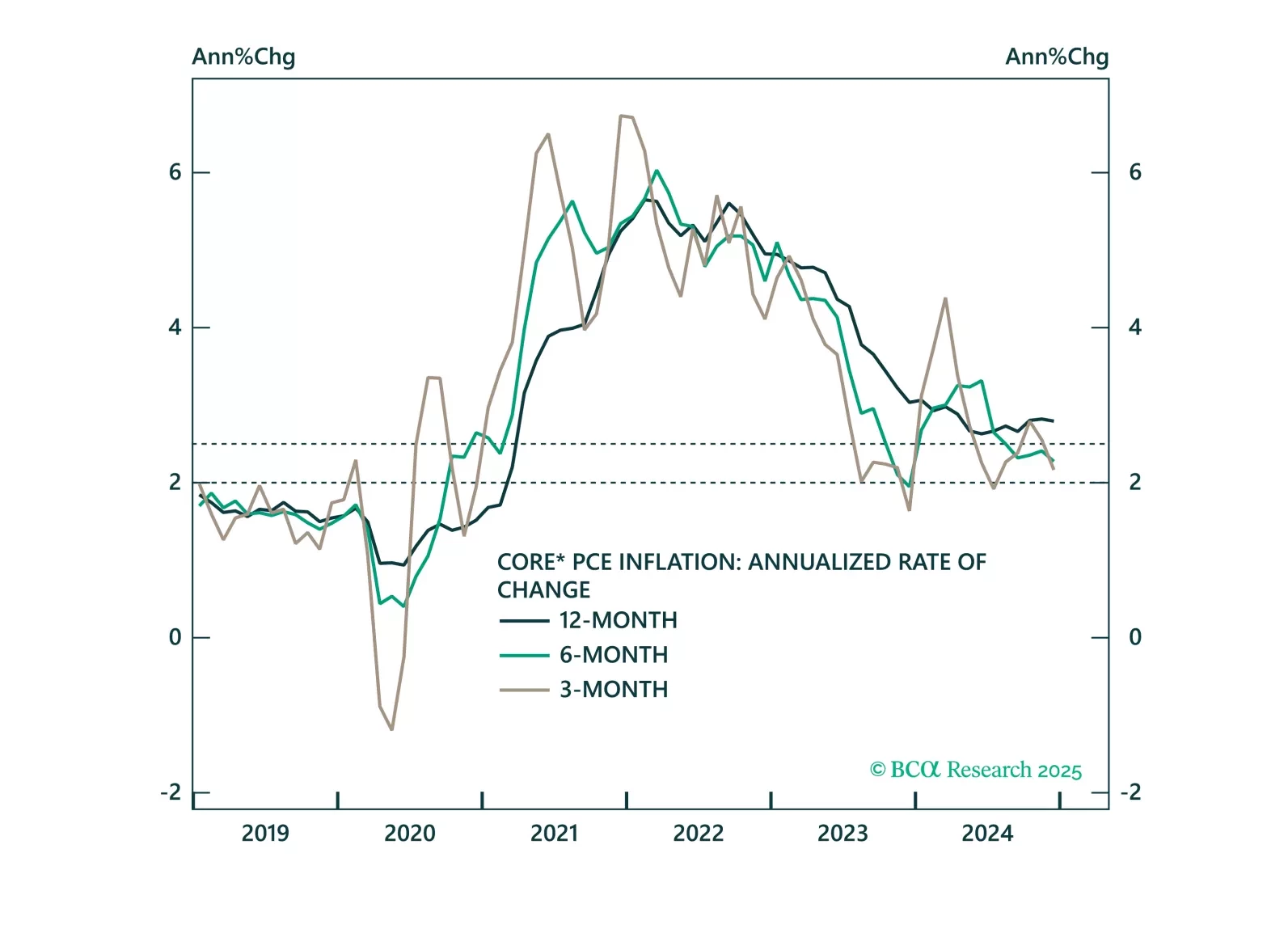

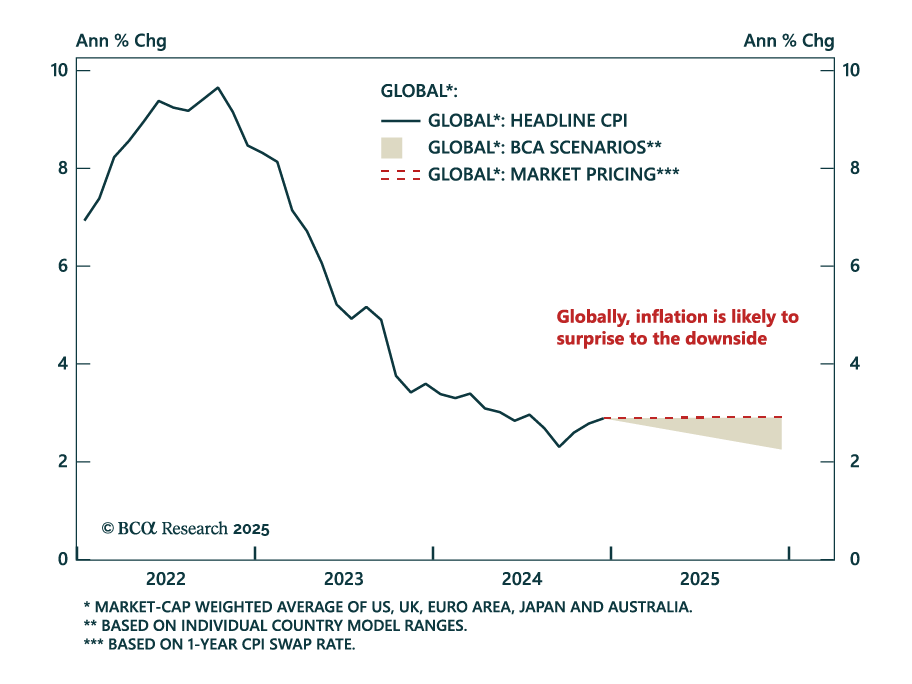

December PCE inflation was in line with expectations, with headline inflation at 0.3% m/m (2.6% y/y) and core at 0.2% m/m (2.8% y/y). The Q4 employment cost index also came in line with expectations at 0.9% q/q. Inflation is currently running below the Fed’s…

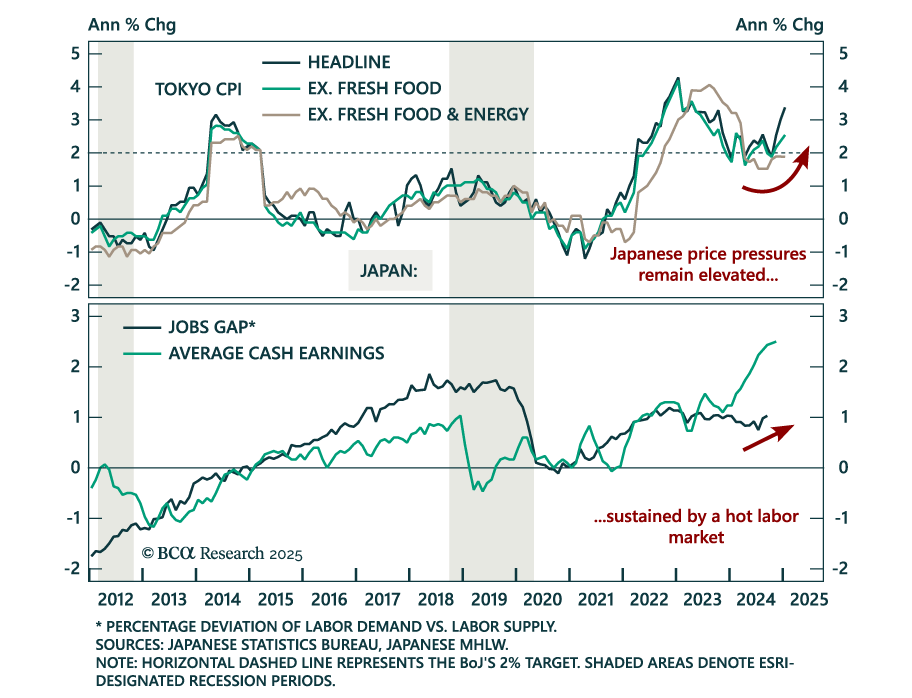

The January Tokyo CPI came in stronger than expected, with headline inflation accelerating to 3.4% y/y from 3.0%, and “core core” (ex. fresh food and energy) accelerating to 1.9% from 1.8%. The jobless rate also decreased 0.1% to 2.4% in…

Core PCE inflation came in soft this morning and is tracking well below the Fed’s 2025 forecast. We highlight three upside risks to inflation and preview next week’s employment report.

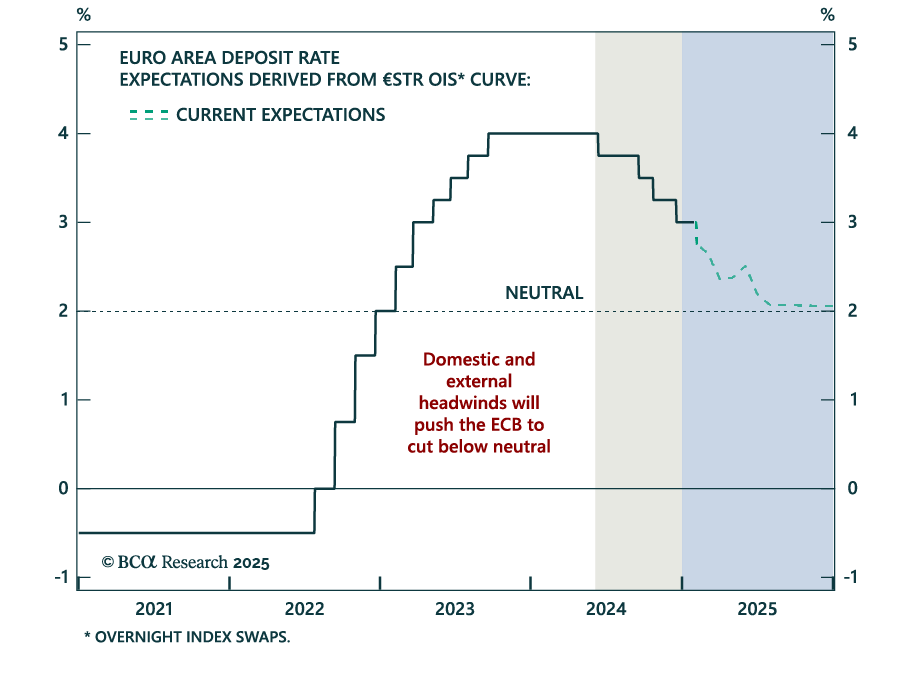

The ECB cut its deposit rate to 2.75%, as was widely anticipated. President Christine Lagarde did not provide any fireworks, but the Governing Council’s message was clear: Policy is restrictive, and inflation will fall further. As a result, if we combine our economic forecasts for the Eurozone with Frankfurt’s data dependency, we continue to expect the ECB’s deposit rate to settle below 2%. Consequently, German bond yields have downside, and the euro has yet to bottomed.

The ECB cut by 25 bps as expected, bringing the deposit facility rate to 2.75%. Despite avoiding committing to a path for policy, President Lagarde reiterated the disinflationary process is “well on track”, and did not push against current market pricing,…

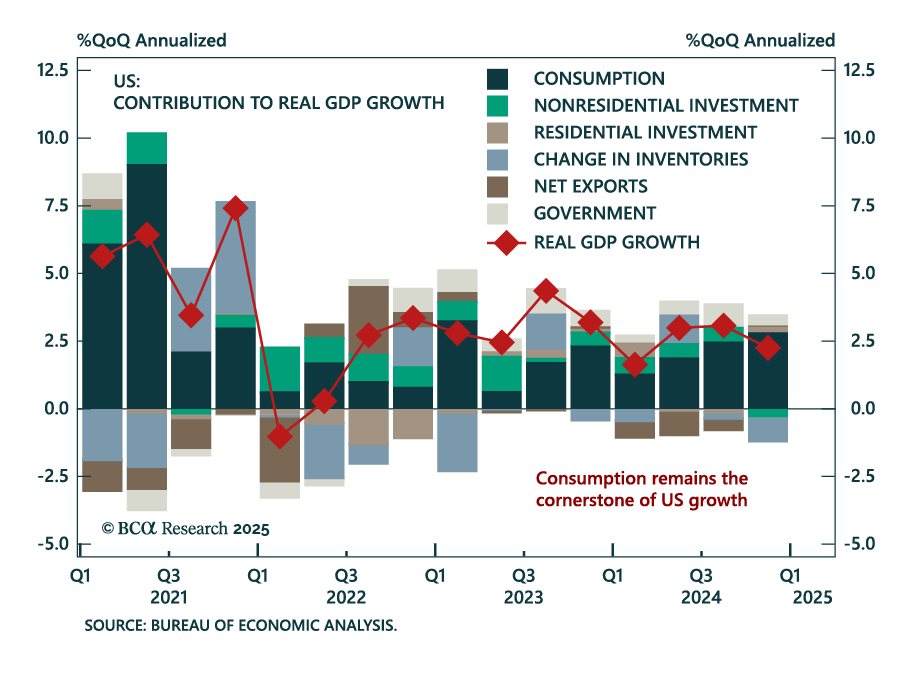

Advanced Q4 US GDP missed estimates, slowing down to 2.3% quarterly annualized growth from 3.1%. The weakness was however driven by inventories. Consumer spending beat estimates and accelerated to 4.2% from 3.7% in Q3. Growth is still above trend as the US…

Our Global Fixed Income strategists assessed the risk of a second wave of inflation, and discussed the opportunities within the inflation-linked bond (ILB) market. Global disinflation remains on track, though energy prices and tariffs pose upside risks.…

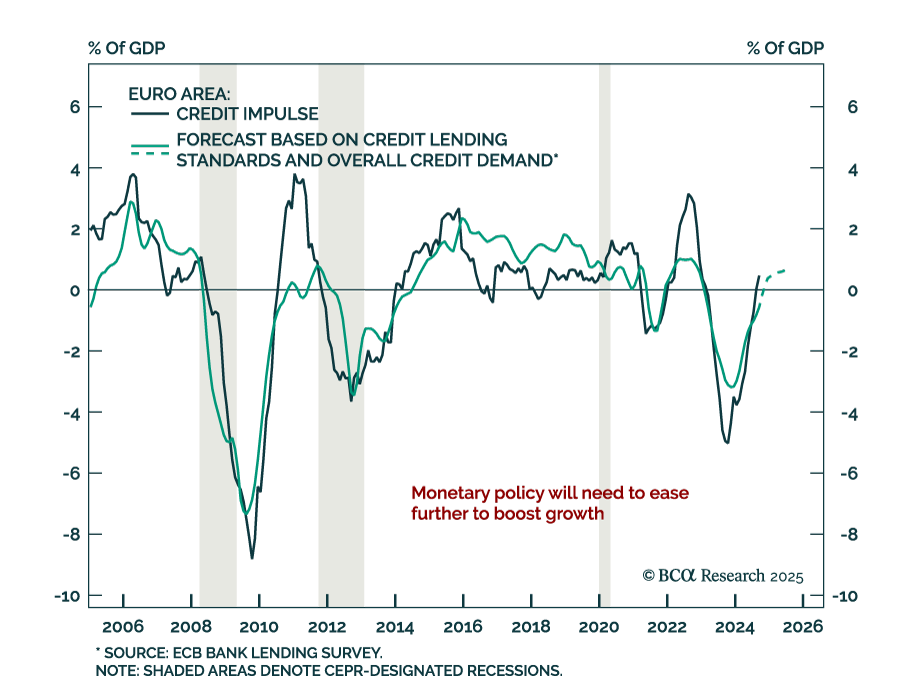

The January 2025 ECB bank lending survey saw a net tightening of credit standards in Q4 2024. Credit standards were tightened for business and consumer lending, and were roughly unchanged for home mortgage loans. Banks expect further tightening across all…

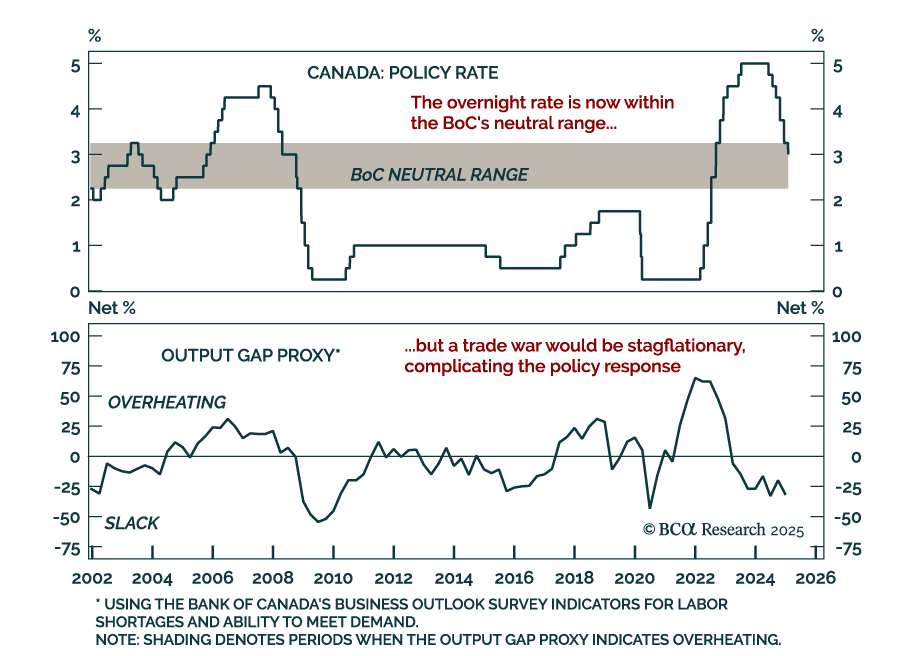

The Bank of Canada cut by 25 bps to 3% as expected, and announced the end of quantitative tightening. This sixth consecutive cut brings the policy rate further into neutral territory, estimated to be in the 2.25%-to-3.25% range. The BoC assessed…