Developed Countries

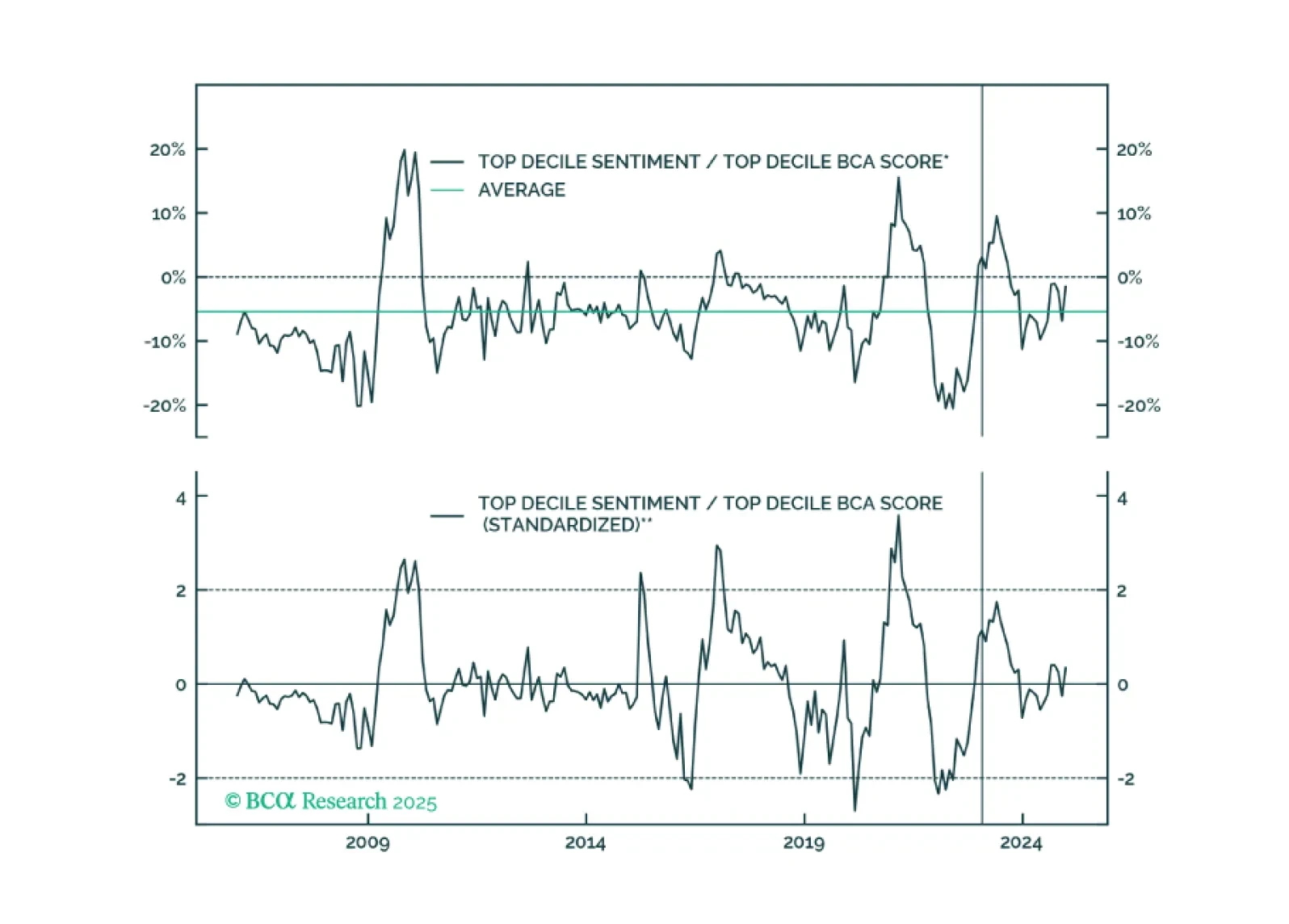

Sentiment will stay positive for now, but downside risks are rising. Investors should proceed cautiously in stock picking and portfolio construction at this juncture, given rising economic and policy uncertainty, which threaten market sentiment, and more broadly, the current bull-market.

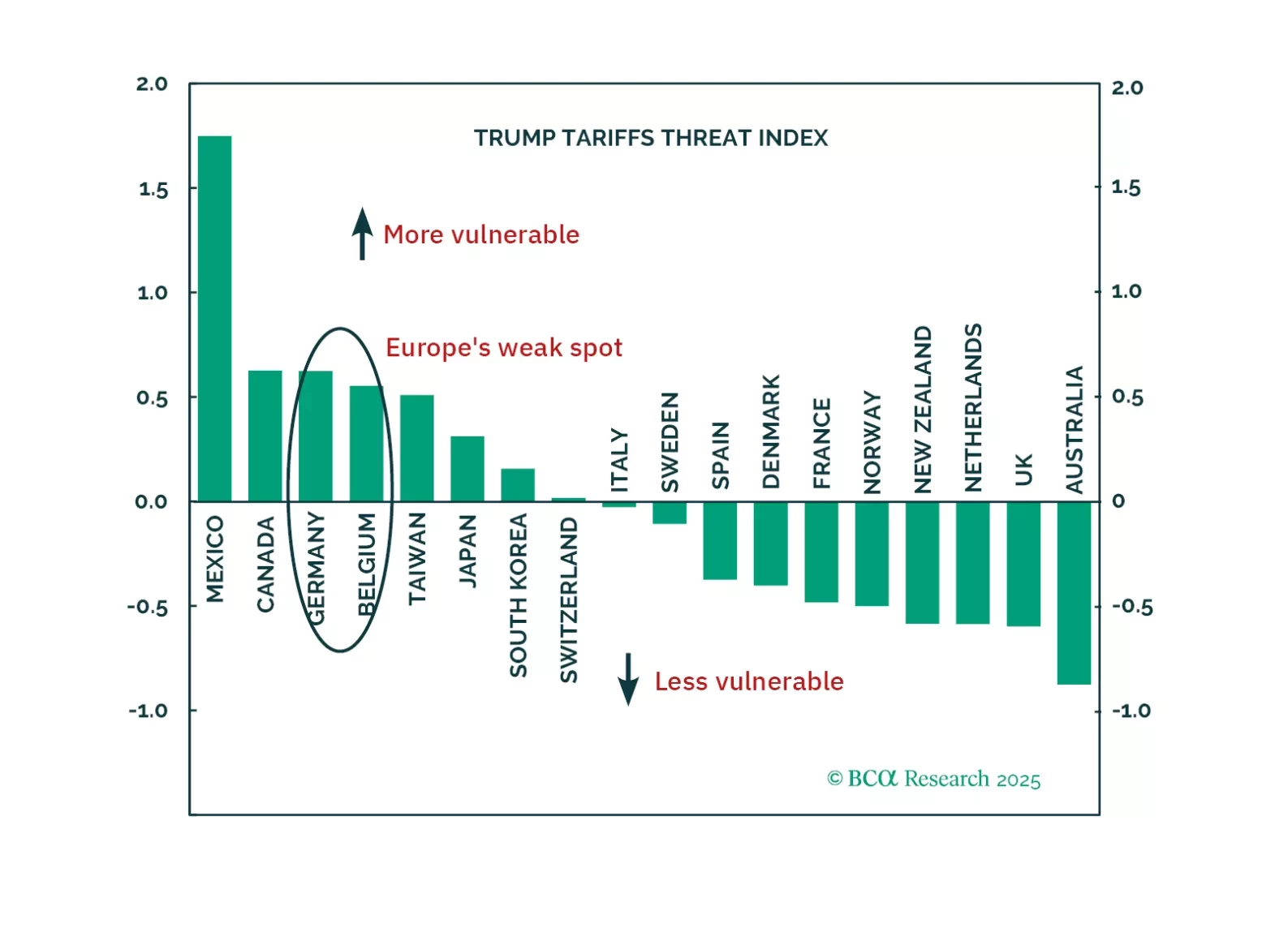

President Trump is about to be inaugurated. Investors often assume all his policies will hurt Europe, but the reality is more nuanced.

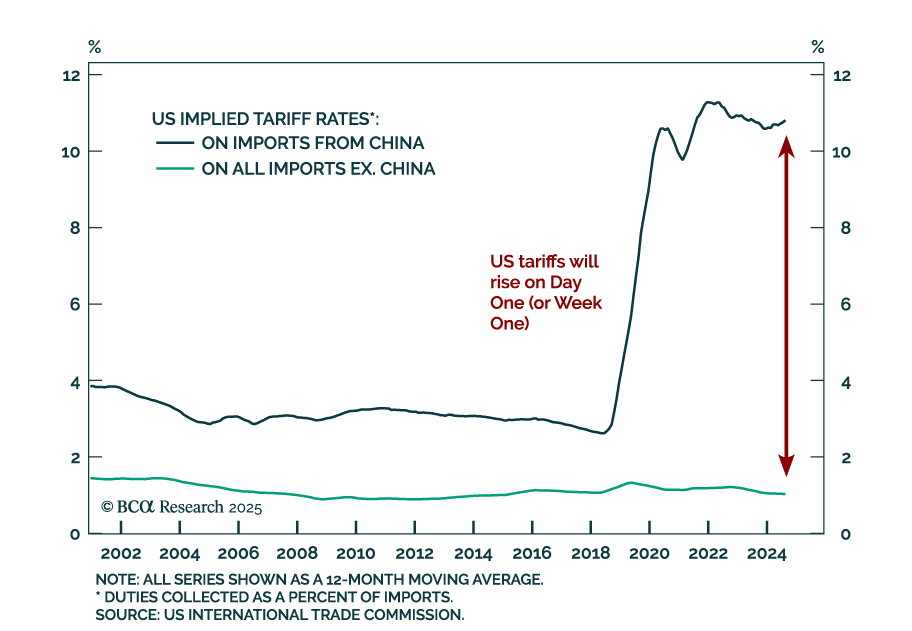

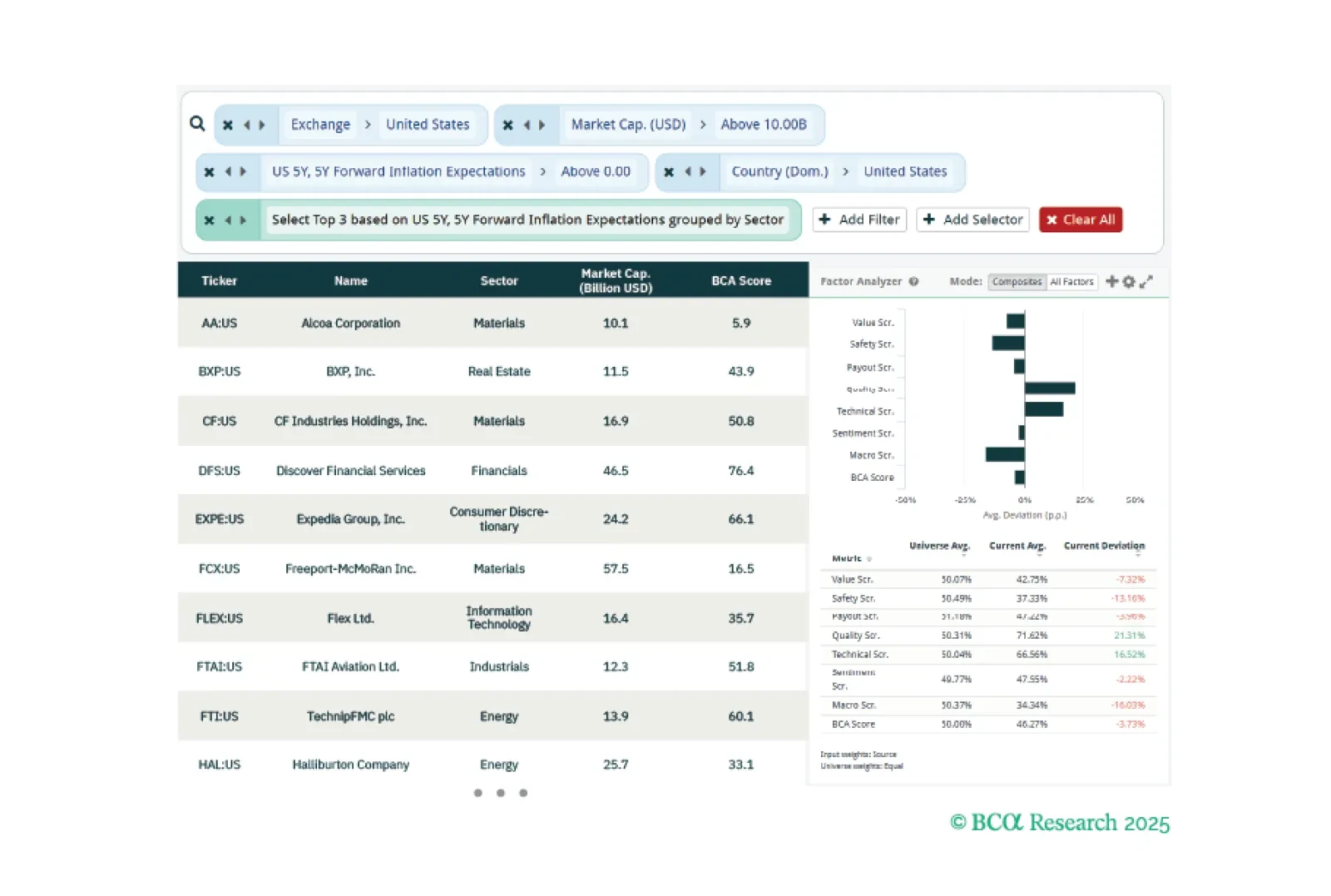

This week, our screeners cover views on Trump 2.0, defensive US equity sectors, and a pullback in Singapore equities. Our first screener aims to hedge longer term inflation risks that Trump 2.0 will likely generate, targeting US equities that are highly correlated with future inflation expectations. Our second screener identifies several defensive sectors that are worth consideration, in case of a tactical pullback in US equities. Lastly, we pick out Singapore stocks that are cheap and high safety, should a pullback occur in the local bourse given weakening macro and technical conditions.