Developed Countries

This week, our screeners cover views on Trump 2.0, defensive US equity sectors, and a pullback in Singapore equities. Our first screener aims to hedge longer term inflation risks that Trump 2.0 will likely generate, targeting US equities that are highly correlated with future inflation expectations. Our second screener identifies several defensive sectors that are worth consideration, in case of a tactical pullback in US equities. Lastly, we pick out Singapore stocks that are cheap and high safety, should a pullback occur in the local bourse given weakening macro and technical conditions.

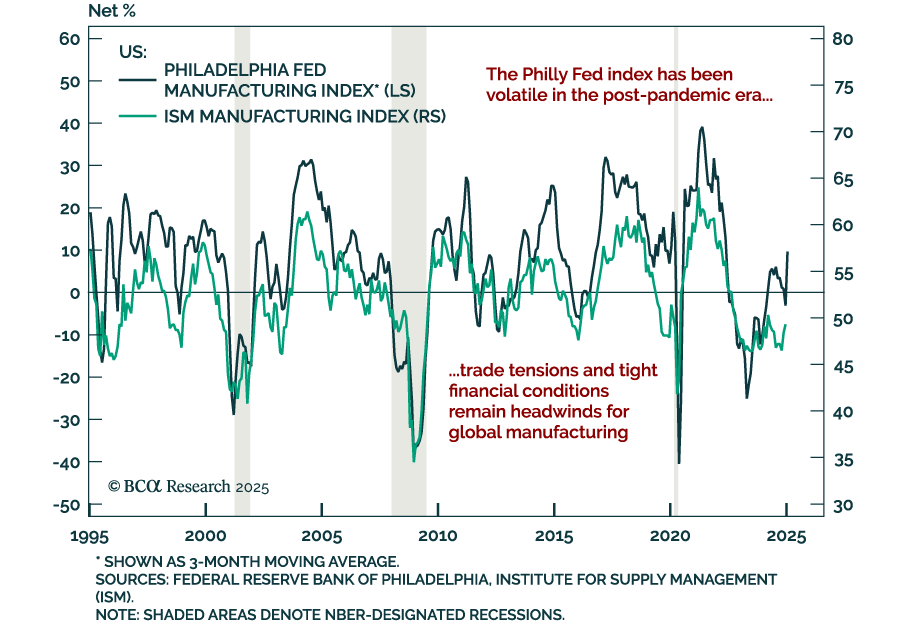

The January Philly Fed Manufacturing index blew past estimates, soaring to 44.3 vs. a revised 10.9 points contraction in December. Most subcomponents rose for both the current and expected categories. Measures of prices paid and received also ticked…

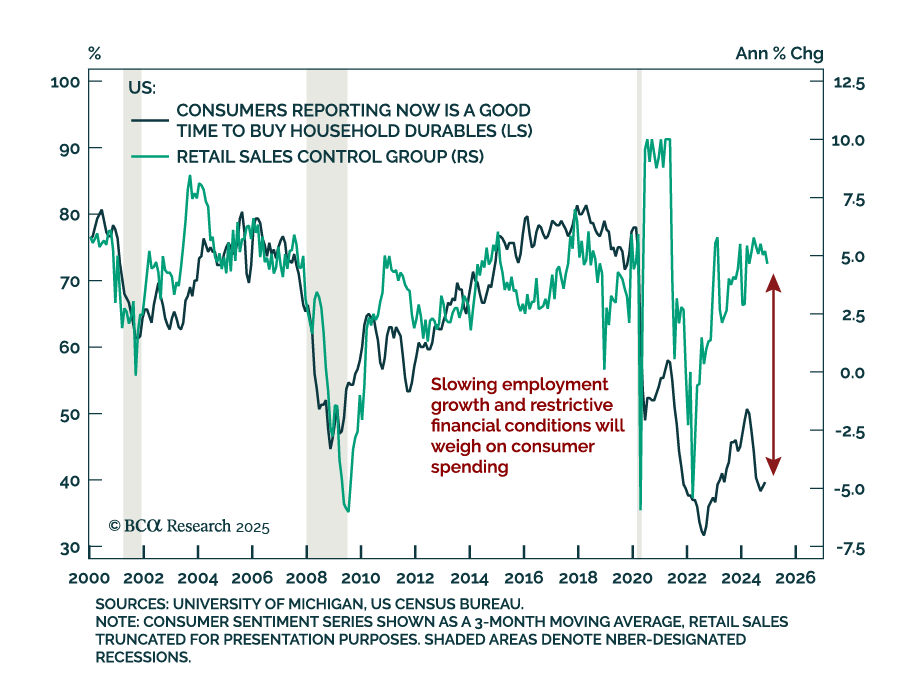

December US retail sales missed estimates, with the headline number printing at 0.4% m/m, a decline from an upwardly revised 0.8% in November. On the positive side, the control group beat estimates at 0.7%. Netting it all out, the report was uninspiring,…

Please join us for a BCA Expert Webcast, Thursday, January 16 at 10:00 AM EDT, with Brendan Kelly, former Director for China Economics on the US National Security Council, veteran of the New York Federal Reserve, Treasury Department, Defense Department, and life member of the Council on Foreign Relations.

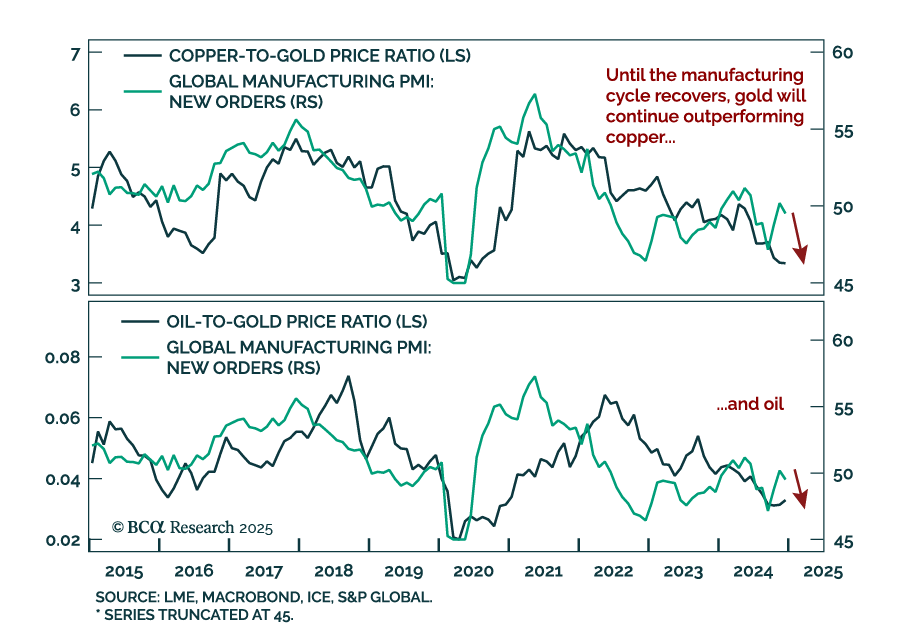

Our Commodities & Energy strategists published a special report outlining three themes they see in the space for 2025. The themes are the following: Sluggish global demand and weak industrial activity will likely weigh on cyclical commodities,…

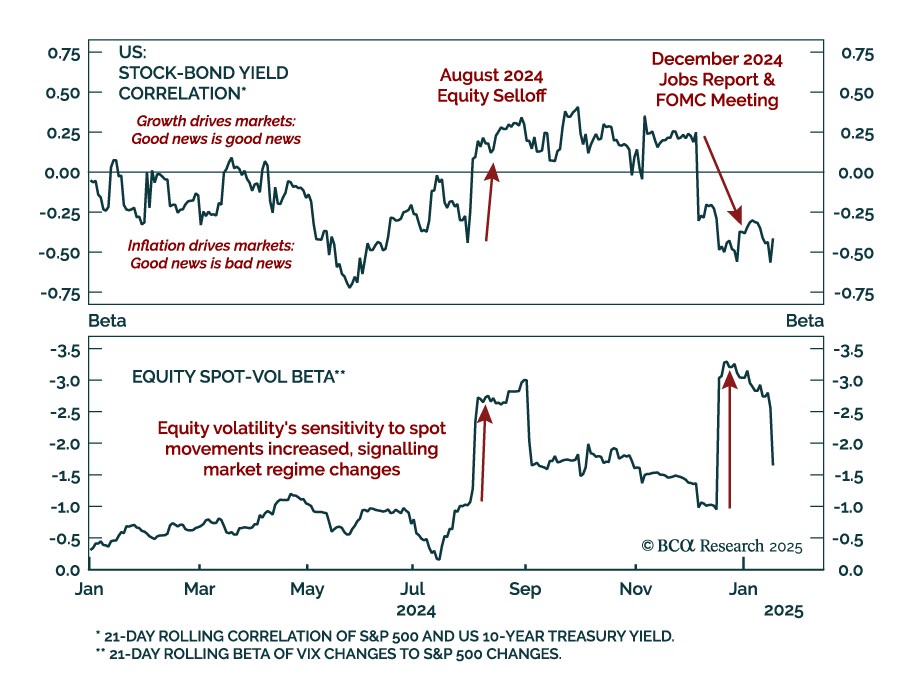

Two main market events defined 2024, highlighting how assets will react to economic data on the tactical horizon. The August 2024 selloff marked a positive shift in the stock-bond yield correlation, as higher odds of a “hard landing” were priced in, after…

The December US CPI came in better than expected. While headline CPI met estimates of 0.4% m/m (2.9% y/y), core surprised to the downside at 0.2% m/m, decelerating to 3.2% y/y from 3.3%. Moderation in core annual inflation was driven by both goods, which are…

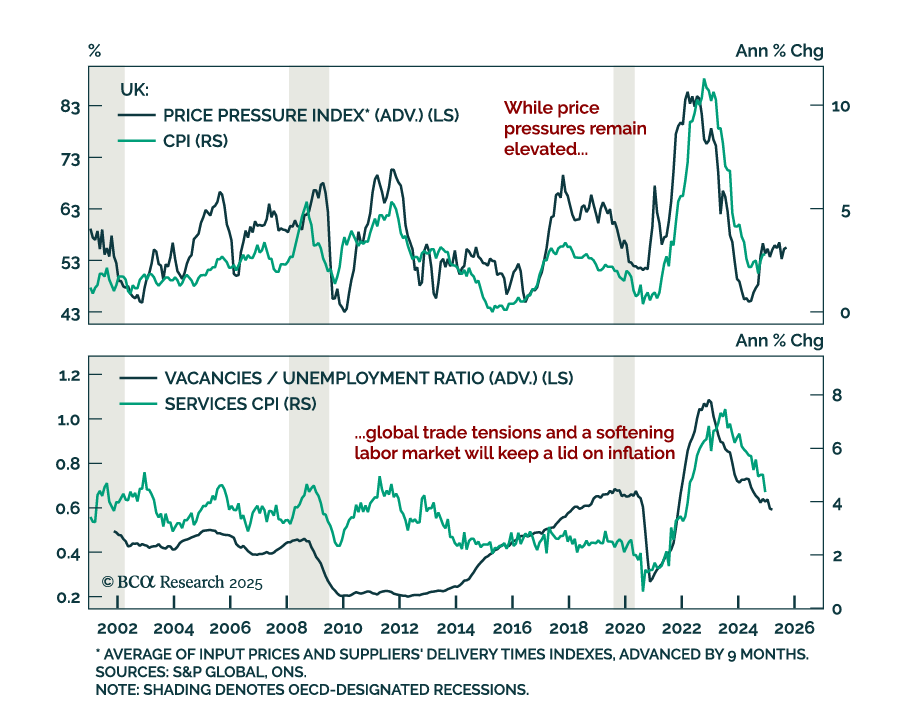

UK inflation surprised to the downside in December. Headline inflation retreated below estimates to 2.5% y/y from an eight-month high of 2.6% in November. Core inflation also decreased below estimates, printing 3.2% vs. 3.5% in November. Services inflation,…

Our Global Investment Strategy (GIS) team believes the US economy is not as strong as commonly believed, and that equity valuations offer little buffer given the risk of incoming macro shocks. The US economy is more fragile than it appears, with risks…

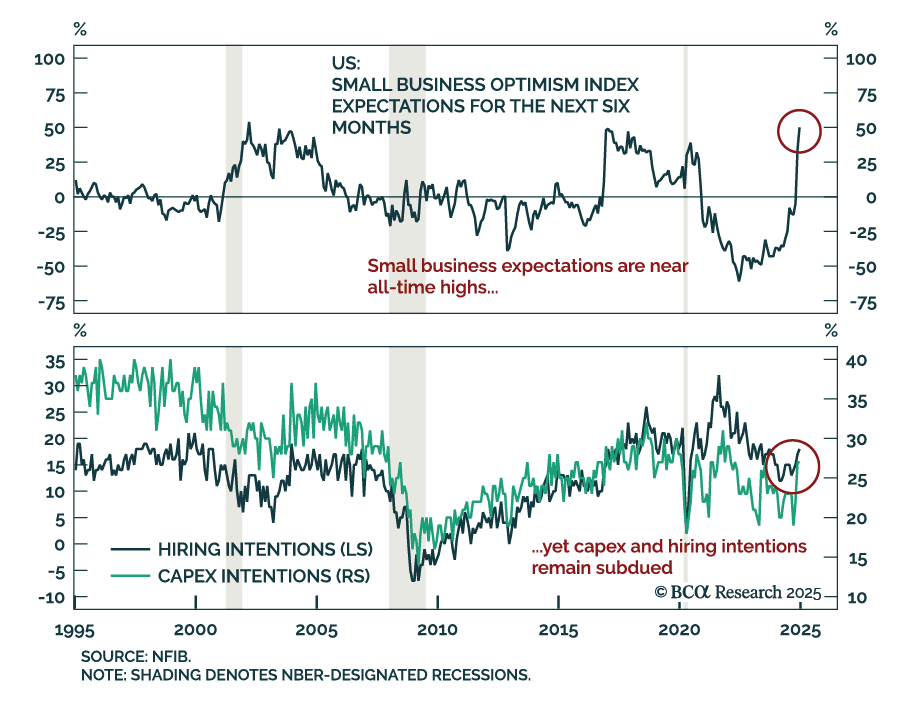

The December NFIB Small Business Optimism Index beat expectations, jumping to 105.1 from 101.7 in November. Most index subcomponents increased, led by measure of expectations, notably for the state of the economy and real sales. After jumping 39 percentage…