Developed Countries

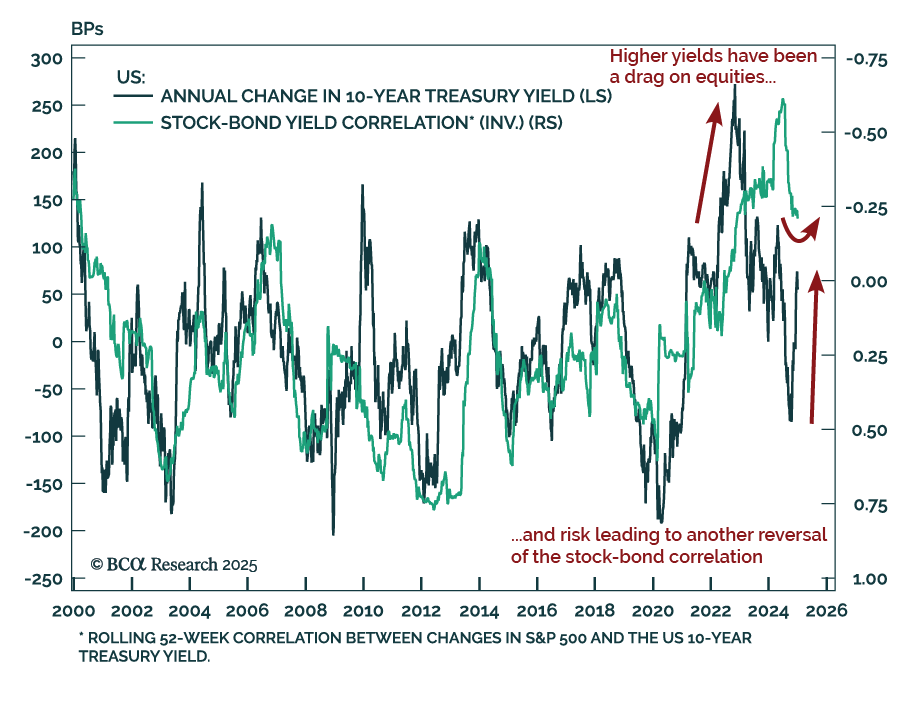

The post-COVID inflation impacted the most important cross-asset relationship: the stock-bond correlation. Higher inflation expectations pushed yields higher, leading to a correction in bond and stock prices. As price pressures receded, bond yields fell and…

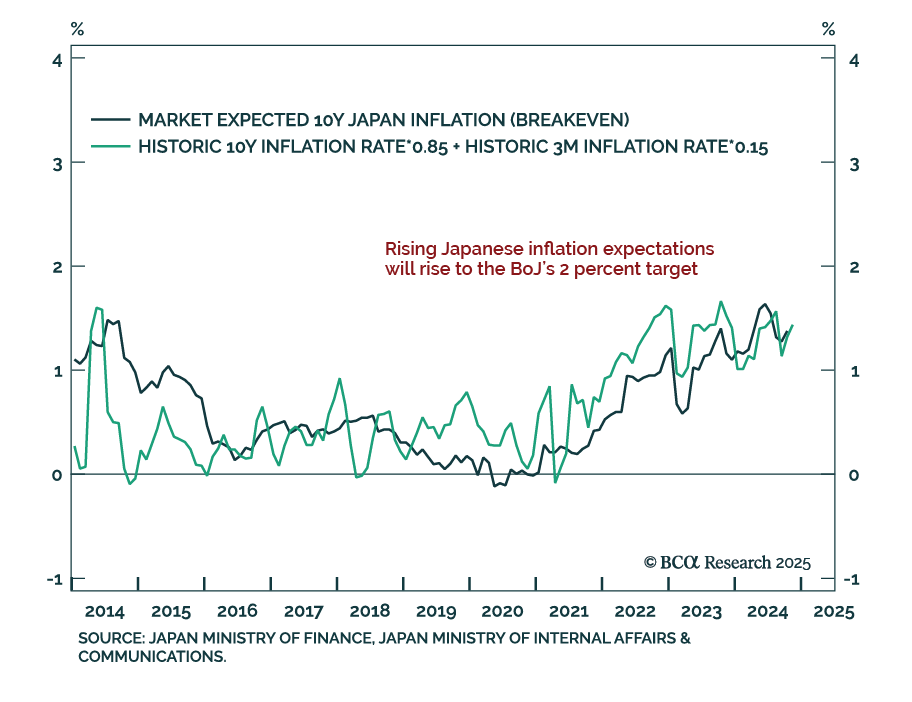

Our Counterpoint Strategy team sees Japanese real yields as the key risk to global equities. Rising inflation expectations in developed markets, excluding Japan, will keep inflation above target and limit further rate cuts. However, in Japan, inflation…

In most developed economies, rising inflation expectations will lift them further above the 2 percent target, limiting the scope for further interest rate cuts. But in Japan, rising inflation expectations will lift them up to the BoJ’s 2 percent target, removing the BoJ’s justification for its zero-interest rate policy. The normalisation of Japan’s monetary policy poses a big structural risk to stocks because Japan has been the main source of financial market liquidity, and thereby, of rising stock market valuations. From a timing perspective though, wait until the complexities of the price trends in USD/JPY and/or Nasdaq versus 30-year T-bond have collapsed. Plus: go tactically long copper.

November factory orders in Germany widely missed estimates, falling by 5.4% m/m, worsening the 1.5% October decline. Excluding major orders, which often distort the overall picture, core new orders fell 1.7% y/y after growing 5.7% in October. The European…

Our GeoMacro strategists published their Alpha Report, outlining their view that President Trump will have to pare back his fiscal ambitions to avoid a bond market riot. The long end of the US bond market continues to sell off, reinforcing our…

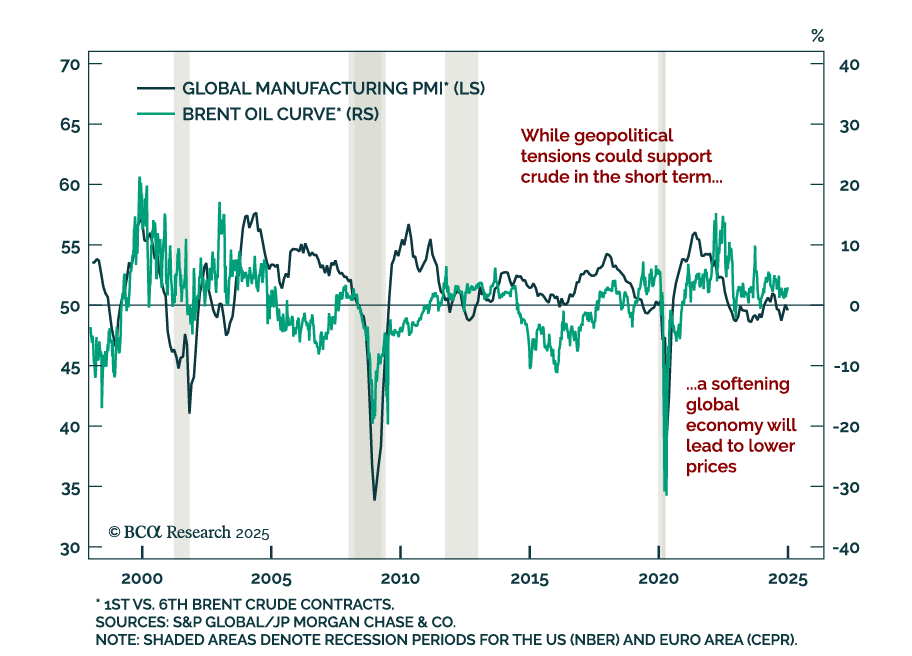

Oil prices have broken out above resistance from a tight trading range since the holidays. We attribute this latest rally to geopolitical tremors more than a vote of confidence from markets on global growth given softening data. The global economy is…

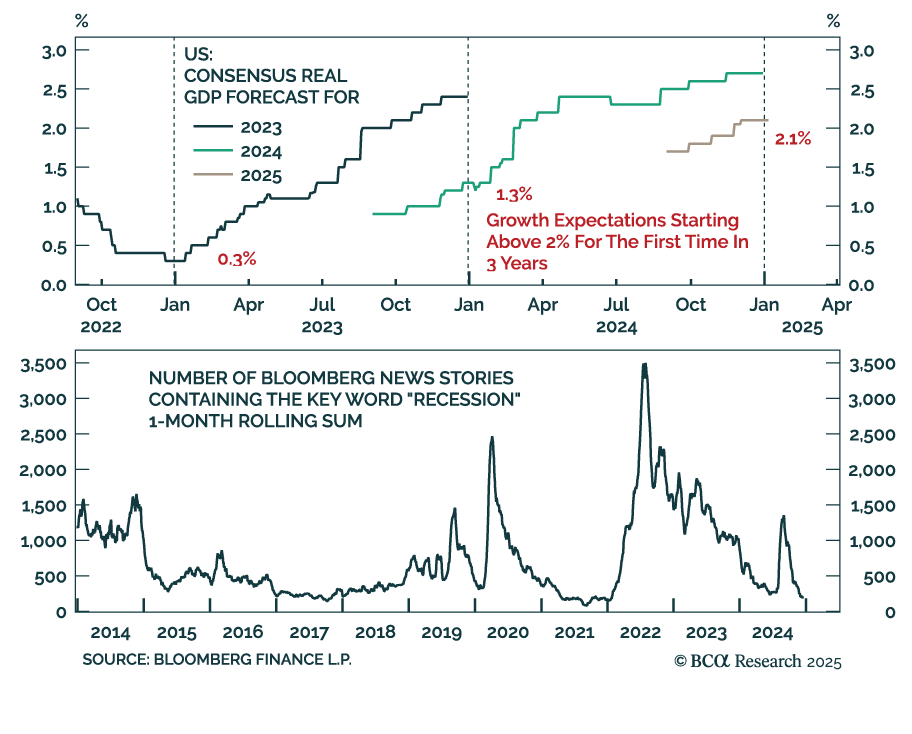

Our Global Asset Allocation strategists published their monthly tactical asset allocation report, where they illustrate booming expectations in the US will be self-limiting. For the first time since 2022, US GDP growth is expected to start the year above…

The December ISM Services PMI beat estimates, increasing to 54.1 from 52.1 in November. All subcomponents increased except for employment, which nonetheless remains in expansion. The prices paid component was especially strong, increasing to 64.4 from…

Job openings once again beat expectations in November, increasing to 8.1m from 7.8m in October. However, hires and quits decreased and layoffs increased. The gap between quits and layoffs, a leading indicator of labor market demand, ticked down. The jobs gap,…

December euro area inflation met expectations, with headline HICP printing at 2.4% y/y from 2.2% in November, and core steady at 2.7%, above the ECB’s target. Services inflation remains elevated at 4.0% y/y, up from 3.9% a month prior. While services…